Download Expectations and Investment and more Study notes Lease Finance and Investment Banking in PDF only on Docsity!

Expectations and Investment^1

Nicola Gennaioli Yueran Ma Andrei Shleifer Universita’ Bocconi Harvard University

May 2015

Abstract

Using micro data from Duke University quarterly survey of Chief Financial Officers, we show that corporate investment plans as well as actual investment are well explained by CFOs’ expectations of earnings growth. The information in expectations data is not subsumed by traditional variables, such as Tobin’s Q or discount rates. We also show that errors in CFO expectations of earnings growth are predictable from past earnings and other data, pointing to extrapolative structure of expectations and suggesting that expectations may not be rational. This evidence, like earlier findings in finance, points to the usefulness of data on actual expectations for understanding economic behavior.

(^1) We are deeply grateful to John Graham and Campbell Harvey for providing data from the CFO survey, and to Joy Tianjiao Tong for helping us to access the data. We thank our discussants Monika Piazzesi and Chris Sims, as well as Gary Chamberlain, Martin Eichenbaum, Carlo Favero, Robin Greenwood, Luigi Guiso, Sam Hanson, Chen Lian, Jonathan Parker, Fabiano Schivardi, Jim Stock, and Mirko Wiederholt for useful suggestions. We also thank Yang You for research assistance.

1. Introduction

One of the basic principles of economics in general, and macroeconomics in particular, is

that expectations influence decisions. In line with this principle, the use of survey-based

expectations data has been the mainstay of macroeconomic analysis since the 1940s, analyzing

variables such as railroad shippers’ forecasts. NBER published several volumes on data of this

kind, such as The Quality and Economic Significance of Anticipations Data (1960), showing that

forecasts help to explain real decisions by firms, including investment and production.

The use of expectations data took a nosedive following the Rational Expectations

Revolution. First, under rational expectations, the model itself dictates what expectations rational

agents should hold to be consistent with the model (Muth, 1961), so anticipations data are

redundant. Second, economists became skeptical about the quality of expectations data; in fact

this skepticism predates rational expectations (Manski, 2004). According to Prescott (1977),

“Like utility, expectations are not observed, and surveys cannot be used to test the rational

expectations hypothesis” (underlining his). In finance, as in macroeconomics, the Efficient

Markets Hypothesis implies that expectations of asset returns are predicted by the model

(Campbell and Cochrane, 1999 ; Lettau and Ludvigson, 2001), so expectations data are not

commonly used.

In our view, the marginalization of research on survey expectations deprives economists of

extremely valuable information. Whether or not survey expectations predict behavior is an

empirical question. Moreover, the rational expectations assumption should not be taken for

granted, but rather confronted with actual expectations data, imperfect as they are. Today, we

have theoretical models that do not rely on the rational expectations assumption and make

testable predictions, as well as expectations data to compare alternative models. Indeed, Manski

(2004) argues forcefully and convincingly that expectations data are necessary to distinguish

alternative models in economics.

As an illustration, take the case of finance, where data on expectations of asset returns have

been rejected as uninformative (e.g. Cochrane, 2011). Yet there is mounting evidence that

expectations are highly consistent across different surveys of different types of investors, that

they have a fairly clear extrapolative structure, that they predict investor behavior, and that they

are useful in predicting returns (e.g., Greenwood and Shleifer, 2014). Most important,

Our paper is related to several very large strands of research. Most clearly, it is related to a

large literature on determinants of investment, such as Barro ( 1990 ), Hayashi (1982), Fazzari,

Hubbard, and Petersen (1988), Morck et al. (1990), Lamont (2000), and many others. Four

papers are particularly closely related to our work. Cummins, Hassett and Oliner (2006) replace

the traditional market-based Tobin’s Q used in investment equations by Q computed using

analyst expectations data, and find that the fit of the equation is much better. Guiso, Pistaferri,

and Suryanarayanan (2006) use direct expectations data on Italian firms to study the relationship

between expectations, investment plans, and actual investment. Arif and Lee (2014) use

accounting data to show that high aggregate investment precedes earnings disappointments, and

argue that fluctuations in investor sentiment account for the evidence. Greenwood and Hanson

(2015) study specifically the shipping industry, and find evidence of boom-bust cycles driven by

volatile (and incorrect) expectations and investment that follows them.

Our paper is also related to research on expectations in macroeconomics. A large literature

studies inflation expectations and their rationality (e.g. Figlewski and Wachtel, 1981; Zarnowitz,

1985; Keane and Runkle, 1990 ; Ang, Bakaert, and Wei, 2007; Monti, 2010; Del Negro and

Eusepi, 2011; Coibion and Gorodnichenko, 2012, forthcoming; Smets, Warne, and Wouters,

2014). Souleles (2004) finds that consumer expectations are biased and inefficient, yet are strong

predictors of household spending. Burnside, Eichenbaum, and Rebelo (2015) present a model of

“social dynamics” in beliefs about home prices, and match the model to survey expectations data.

Fuhrer (2015) shows that survey expectations improve the performance of DSGE models. Some

research suggests that analyst expectations of corporate profits are rational at very short horizons

(Keane and Runkle, 1998), although the overwhelming majority of studies reject rationality of

analyst forecasts (De Bondt and Thaler, 1990; Abarbanell, 1991; La Porta, 1996; Liu and Su,

2005; Hribar and McInnis, 2012 ). There is also a literature on expectations shocks in

macroeconomics, which generally maintains the assumption of rational expectations (Lorenzoni,

2009; Angeletos and La’O, 2009; Levchenko and Pandalai-Nayar, 2015).

Perhaps most closely related to our work is research in behavioral finance, where biases in

expectations have been examined for many years (e.g., Cutler, Poterba, and Summers, 1990 ;

DeLong et al. 1990). Some of the recent papers include Amronin and Sharpe (forthcoming),

Bacchetta, Mertens and Wincoop (2009), Hirshleifer and Yu (2012), and Greenwood and Shleifer

(2014), to which we return later. Several of these papers find that investor expectations are

extrapolative. In the bond market, Piazzesi, Salomao, and Schneider (201 5 ) use data on interest

rate forecasts and also find substantial deviations from rationality. Vissing-Jorgensen ( 2003 ) and

Fuster et al. (2011) are two recent Macro Annual papers that also address expectations formation

and rationality.

In the next section, we briefly summarize some of the evidence on the relationship between

investor expectations and asset prices, and address some of the criticisms of expectations data.

Section 3 describes our data. Section 4 presents a simple Q-theory model of expectations and

investment that organizes our empirical work. Section 5 follows with the basic empirical results

on expectations and investment. Section 6 examines the structure of expectations. Section 7

concludes with a brief discussion of implications of the evidence for macroeconomics.

2. Recent Research on Expectations and Asset Prices in Finance

Before turning to our main results on investment, we briefly summarize recent research on

expectations and stock market returns, which illustrates the usefulness of expectations data. In

recent models with time-varying expected returns (e.g., Campbell and Cochrane, 1999 ; Lettau

and Ludvigson, 2001), expected returns (ER) are given by required returns, which in turn depend

on consumption: investors require higher returns when consumption is low (relative to some

benchmark), and lower returns when consumption is high. This research does not generally use

data on expectations. Rather, it adopts a rational expectations approach in which ERs are

determined by the model itself, so the ER is inferred from the joint distribution of consumption

and realized returns.

As discussed in the introduction, recent work has started to use actual expectations data. For

our purposes, the most relevant paper is Greenwood and Shleifer (2014). They use data on

expectations of returns from six different surveys of investors, including a Gallup survey,

investor newsletters, and the survey of CFOs of large corporations that we use in the current

paper. The paper reports four main findings relevant to our analysis, which we summarize in

Tables 1 and 2.

First, expectations of aggregate stock returns are highly correlated across investor surveys,

despite the fact that different datasets survey different investors and ask somewhat different

each variable is available.

3.1 Expectations Data

We have data on the expectations of two groups of people: CFOs and equity analysts. We

first describe these data and then show that expectations of CFOs and equity analysts are highly

correlated.

A. CFO Expectations

Our data on CFO expectations come from the Duke/CFO Magazine Business Outlook

Survey led by John Graham and Campbell Harvey, which was launched in July 1996 and takes

place on a quarterly basis. Each quarter, the survey asks CFOs their views about the US economy

and corporate policies, as well as their expectations of future firm performance and operational

plans.^2 Starting in 1998, the CFO survey consistently asks respondents their expectations of the

future twelve month growth of key corporate variables, including earnings, capital spending, and

employment, among others. The original question is presented to the CFOs as follows:

Relative to the previous 12 months, what will be your company's PERCENTAGE CHANGE

during the next 12 months? (e.g., +3%, - 2%, etc.) [Leave blank if not applicable]

Earnings: ________; Cash on balance sheet: ________; Capital spending: ________; Prices of your product: ________; Number of domestic full-time employees: ________; Wage: ________; Dividends: ________...

(Selected items are listed as examples. For a complete listing, please refer to original

questionnaires posted on the CFO survey’s website.)

We use CFOs’ answers on earnings growth over the next twelve months as the main proxy

for CFO expectations of future profitability. As the survey does not ask for expectations beyond

the next twelve months, we will explain in Section 4 how we interpret and extract information

from earnings expectations over the next twelve months.

We then use CFOs’ answers on capital spending growth in the next twelve months as a

proxy for firms’ current investment plans. In the empirical analysis, we investigate how

investment plans relate to expectations of future profitability. We adopt this approach in light of

(^2) Graham and Harvey (2011) provide a detailed description of the survey. Historical questionnaires are available at http://www.cfosurvey.org.

well documented lags between decisions to invest and actual investment spending (Lamont,

2000). With lags in investment implementation, current expectations about future profitability

may not translate into capital expenditures instantly. Instead, they will affect current investment

plans, and show up in actual investment spending with some delay. As a result, it can be more

straightforward to detect the impact of earnings expectations by looking at investment plans. We

discuss this issue in more detail in Sections 4 and 5.

Our analyses use both aggregate time series and firm-level panel data. Aggregate variables

are revenue-weighted averages of firm-level responses, and they are published on the CFO

survey’s website. While the survey does not require CFOs to identify themselves, some

respondents voluntarily disclose this information. It is then possible to match a fraction of the

firm-level responses with data from CRSP and Compustat to perform firm-level tests. For

example, Ben-David, Graham, and Harvey (2013) use matched firm-level data to study how

managerial miscalibration affects corporate financial policies. Because there are privacy

restrictions associated with these data, Graham and Harvey helped us implement firm-level

analysis using a subsample of their matched dataset. The firm-level data we use has 1, 133

firm-year observations, spanning from 2005Q1 to 2012Q4.^3 We exclude firms that have

negative earnings in the past twelve months because in that case earnings growth is not

well-defined. We also winsorize outliers at the 1% level.

B. Analyst Expectations

We obtain data on equity analysts’ expectations of future firm performance from the

Institutional Brokers’ Estimate System (IBES) dataset. Beginning in the 1980s, IBES collects

analyst forecasts of quarterly earnings per share (EPS) for the next one to up to twelve quarters.

We take consensus EPS forecasts (i.e. average forecast for a given firm-quarter in the future) and

compute forecasts of total earnings by multiplying by the number of shares outstanding. To

compare the results with those using CFO expectations, we compute analyst expectations of

future twelve months earnings growth. We calculate aggregate analyst expectations of future

twelve months earnings growth by summing up expected future earnings of all firms in the next

four quarters, and then divide by the sum of earnings of all firms in the past four quarters. We

calculate firm-level analyst expectations of future earnings growth by taking the forecast of total

(^3) The number of observations in our firm-level regressions can be smaller because some respondents do not answer all questions.

realized earnings from IBES Actuals files, which closely track earnings as reported by

companies in their earnings announcements. These are the numbers that analyst forecasts aim to

match and the earnings metric that managers tend to use the most.^4 In the rest of the paper we

refer to IBES actual earnings as “earnings”, and GAAP earnings as “net income”.

Table 3 presents summary statistics of firms for which we have firm-level CFO expectations

(Panel A) and analyst expectations (Panel B), as well as all non-financial firms in Compustat

(Panel C). For comparability, the statistics in Panel B and Panel C are generated based on the

time period for which we have firm-level CFO expectations (i.e. from 2005 through 2012). We

can see that firms with analyst expectations are mostly larger than the median Compustat firm,

and firms with CFO expectations are generally even larger. Firms with CFO and analyst

expectations also appear to be more profitable than firms in the full Compustat sample in terms

of net income, but otherwise very similar in terms of sales, investment, book-to-market, and Q.

4. Expectations and Firm Investment: Empirical Specifications

We motivate our empirical specification with a basic Q-theory model. A firm is run by a risk

neutral owner who discounts the future by factor 𝛽 < 1,^5 and the firm’s horizon is infinite. In

the model, we interpret each period 𝑡 to be twelve months. The firm’s output in period 𝑡 is

obtained by combining capital and labor using a constant returns to scale production function

𝐴𝑡𝐾𝑡𝛼𝐿1−𝛼𝑡. At the beginning of period 𝑡, the owner hires labor 𝐿𝑡 at wage 𝑤 and makes

decisions about investment during this year 𝐼𝑡. Investment takes one year to implement, so

𝐾𝑡+1 = (1 − 𝛿)𝐾𝑡 + 𝐼𝑡, where 𝛿 is capital depreciation rate. The firm’s optimal policy in year 𝑡

maximizes the expected present value of earnings:

𝑚𝑎𝑥{𝐼𝑠,𝐿𝑠}𝑠≥𝑡 𝔼𝑡 {∑ 𝛽𝑠−𝑡[𝐴𝑠𝐾𝑠𝛼𝐿1−𝛼𝑠^ − 𝑤𝐿𝑠 − 𝐶(𝐼𝑠, 𝐾𝑠)] 𝑠≥𝑡

subject to 𝐾𝑠+1 = (1 − 𝛿)𝐾𝑠 + 𝐼𝑠. We assume the commonly used quadratic investment costs:

𝐾𝑠^ − 𝑎)

2 𝐾𝑠,

which allow for convex adjustment costs (𝑏 > 0) and displays constant returns to scale.

(^4) We performed detailed checks and verified that IBES actual earnings indeed appear to be closest to forecasts by managers and analysts, in terms of accounting treatment, magnitude, variance, and variation over time. 5 The assumption of risk neutrality and constant discount rate is for simplicity of exposition. The framework can be extended to incorporate time-varying discount rates, as derived in Lettau and Ludvigson (2002). In our empirical analysis in Section 4.2 and Section 4.3, we will explicitly consider time-varying discount rates.

In the optimization problem above, the operator 𝔼𝑡(. )^ denotes the owner’s expectations

conditional on his information at the beginning of year 𝑡, computed according to his possibly

distorted beliefs. We allow for departures from rational expectations, but restrict to beliefs that

preserve the law of iterated expectations. By standard arguments, Appendix A shows that the

firm’s optimal investment chosen at the beginning of year 𝑡 is described by:

𝐼𝑡 𝐾𝑡^ = (𝑎 −

𝔼𝑡[∑^ 𝑠≥𝑡+1 𝛽𝑠−(𝑡+1)Π𝑠]

𝐾𝑡+^.^

where Π𝑠 = 𝐴𝑠𝐾𝑠𝛼𝐿1−𝛼𝑠^ − 𝑤𝐿𝑠 − 𝐶(𝐼𝑠, 𝐾𝑠)^ denotes the firm’s earnings in year s. Equation (1)

corresponds to a generic Q-theory equation with quadratic adjustment costs, which takes the

form 𝐼𝑡/𝐾𝑡 = 𝜂 + 𝛾𝑄𝑡.

To estimate Equation (1), ideally we would like to know expectations of earnings in all

future periods. This is unfortunately not feasible in practice. For instance, CFOs only report

expectations of earnings growth in the next twelve months. Formally, in the CFO survey we only

have information about 𝔼𝑡(Π𝑡), namely expectations at the beginning of year 𝑡 about earnings

Π𝑡 in the following twelve months (which are not yet known, so expectations are well-defined).

With respect to investment, we have information on: i) planned investment over the next twelve

months, and ii) actual capital spending in each quarter. We denote investment plans for the next

twelve months as 𝐼𝑡𝑝^ , which captures the plan made at the beginning of the year about

investment in the rest of the year.

Given implementation lags in the investment process, it may be most straightforward to test

how expectations at a given point in time affect firms’ investment plans.^6 Accordingly, we

approximate Equation (1) by

𝐼𝑡𝑝 𝐾𝑡

This approximation is reliable if expectations about the level of future earnings display

significant persistence, namely 𝔼𝑡(Π𝑡)/𝐾𝑡 is not too far from 𝔼𝑡(Π𝑡+1)/𝐾𝑡+1 and more

(^6) Plans are particularly helpful in the context of our data, where we observe forward looking expectations once a quarter rather than once a year. With lags in investment implementation, it is unlikely that expectations in a given quarter will be immediately reflected in capital spending in the same quarter, or even fully incorporated into capital spending in the next quarter. In comparison, investment plans would be more responsive to contemporaneous expectations. When managers become more optimistic, they would revise their plans upward. As plans get implemented over time, the impact on actual capital expenditures can show up with some delay. For this reason, it is more straightforward to start testing the impact of expectations by looking at investment plans.

increase in planned investment. In Equation (3) we need to control for the change in capital stock

because both investment and profitability are affected by the size of capital stock. We can also

arrive at a specification very similar to Equation (3) in a simpler setting with time to build but

without adjustment costs.^7 Empirically we use Equation (3) to map a basic investment model to

testable predictions in our dataset. We refrain from testing the parameter restrictions implied by a

strict adherence to the approximated Q equation.

While investment plans are a convenient starting point to detect the impact of expectations,

for Equation (2) to be informative about how expectations influence investment, it must also be

the case that plans are closely related to realizations. In Section 5.3, we show that investment

plans are highly correlated with actual capital spending over the planned period. In other words,

a significant fraction of capital spending over the next few quarters appears to be determined by

ex ante investment plans, consistent with previous findings by Lamont (2000). To the extent that

there is a close correspondence between investment plans and realized investment over the

planned period, it would also be of interest to test how current expectations translate into actual

capital spending in the next twelve months. This additional test allows us to further assess

whether expectations have a substantial impact on actual investment activities. We present results

from these tests in Section 5.3.

5. Expectations and Investment

In this section, we test the relationship between investment decisions and earnings

expectations. We focus on CFO expectations, and provide supplementary results using

expectations of equity analysts. We begin by studying investment plans. In Section 5.1 we

consider the role of expectations at the aggregate level, and in Section 5.2 we consider the role of

(^7) One might also consider an alternative approximation of Equation (1) of the following form 𝐼𝑡−1/ 𝐾𝑡−1 ≈ 𝜃̂ 0 + 𝜃̂ 1 𝔼𝑡(Π𝑡)/𝐾𝑡 where 𝐼𝑡−1 denotes realized investment in the past twelve months, and 𝔼𝑡(Π𝑡), as before, is current expectations of earnings in the next twelve months. This approximation is reasonable under two conditions. As in the case of Equation (2), it should be that expectations over future earnings are stable. Moreover, it has to be that respondents received little information and barely updated their beliefs in the past twelve months, so that current expectations about next twelve month earnings, namely 𝔼𝑡(Π𝑡), is close to expectations four quarters ago about earnings over the same period, namely 𝔼𝑡−1(Π𝑡). We find this approximation to be less tenable for several reasons. First, from time to time new information arrives over a twelve month period that has a significant impact on people’s beliefs. (This can happen even if earnings processes are highly persistent, for example, if it is a random walk.) Second, given implementation lags in real world investment activities, actual capital spending over a twelve month period tends to be particularly influenced by decisions made at the beginning of the period. As a result, realized capital spending in year 𝑡 − 1, 𝐼𝑡−1, may not be well explained by expectations at the end of year 𝑡 − 1. In light of these observations, we use the approximation in Equation (2) in the rest of our analysis.

expectations at the firm level. Then, in Section 5.3 we evaluate the relationship between plans

and realized investment, and document the link between expectations and actual capital

spending.

5.1 Expectations and Investment Plans: Aggregate Evidence

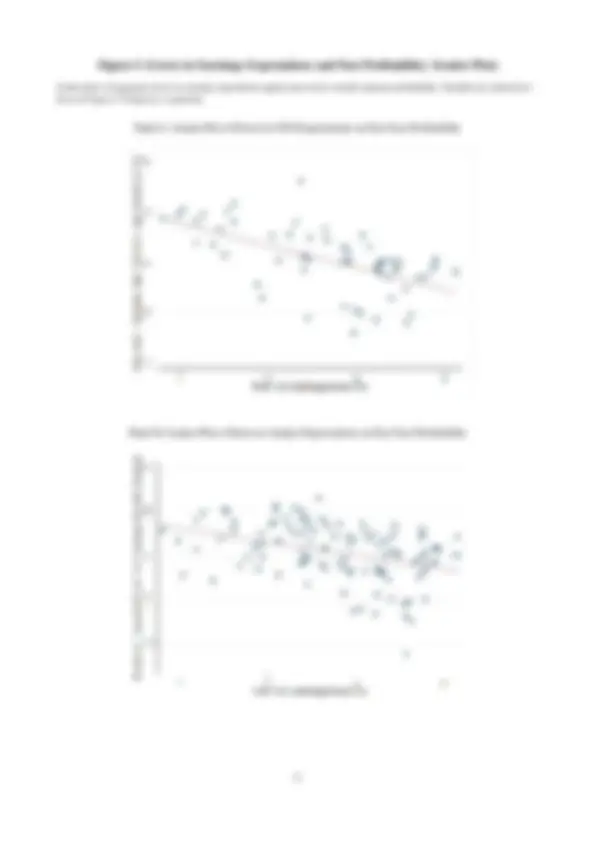

Figure 3 visually represents the association between aggregate CFO expectations and

aggregate investment. Panel A plots CFOs’ expectations of next twelve month earnings growth,

along with planned investment growth in the next twelve months. Panel B adds to Panel A actual

aggregate investment growth in the next twelve months. We see that there is a strong

comovement between earnings expectations and investment plans, and between investment plans

and actual capital spending. At the very least, expectations data do not appear to be

uninformative noise.

We then estimate versions of Equation (3) using quarterly regressions:

∆CAPX̂q𝑡 = α + βEq^ ∗𝑡^ [∆Earnings] + λXq𝑡 + ϵq𝑡

where ∆CAPX̂q𝑡 is planned investment growth in the next twelve months reported in quarter q𝑡,

and Eq^ ∗𝑡^ [∆Earnings]^ is CFO expectations of next twelve month earnings growth reported in

quarter q𝑡. Xq𝑡 includes past change in capital stock as shown in Equation ( 3 ), as well as a set

of additional controls we discuss below. We use Newey-West standard errors with twelve lags.^8

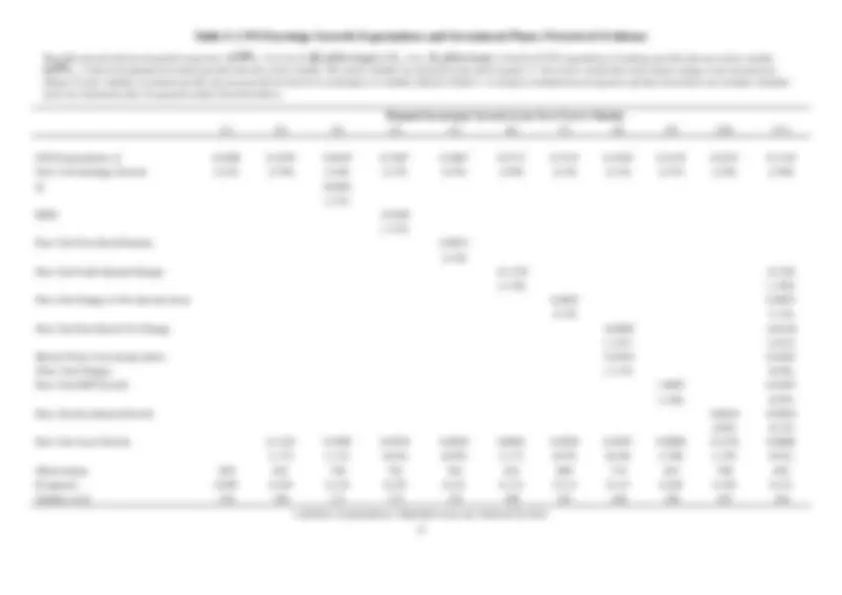

Table (4) columns (1) and (2) report our baseline results. We find that CFOs’ earnings

expectations have significant explanatory power for firms’ investment plans, both statistically

and economically. A one standard deviation increase in earnings growth expectations is

associated with a 0.8 standard deviation increase in planned investment growth.^9 Put differently,

a one percentage point increase in CFO expectations is accompanied by a 0.6 percentage point

increase in planned investment growth. 10 Quantitatively, CFO expectations have major

(^8) We check the autocorrelation structure of the errors: Autocorrelations are mostly limited to the first four lags, due to the overlapping structure of our data; autocorrelations after four lags are minimal. Our empirical results are not sensitive to alternative choices of Newey 9 - West lags. At the aggregate level, during the period where we have CFO expectations data, the standard deviation of planned investment growth is about 0.05, and the standard deviation of 10 earnings growth expectations is 0.07. 0.07*0.6/0.05=0.8. Due to lags in investment implementation it is also possible that, at a given quarter, part of the capital spending that firms expect to make in the next twelve months are determined by decisions made, for example, in the last quarter, and therefore affected by expectations then. In aggregate data, we can include lagged expectations, in which case current expectations and past expectations with two lags are significant, and jointly highly significant. Unfortunately, it is difficult to include lagged

that equity Q is highly persistent and does not line up well with fluctuations in investment

activities. In our context, to explain investment growth, the direct theoretical counterpart is not Q

in levels, but the log change in Q. Barro (1990) shows changes in Q are almost equivalent to

stock returns. He finds that changes in Q from the beginning of year 𝑡 − 1 to the beginning of

year 𝑡 is highly correlated with investment growth in year 𝑡, and stock returns from the

beginning of year 𝑡 − 1 to the beginning of year 𝑡 perform incrementally better. In column (4),

we include past twelve month stock returns. The coefficient on this variable is positive and

statistically significant, as predicted by theory. The coefficient on CFO expectations remains

large and highly significant.^12 The views of CFOs appear to contain a substantial amount of

additional information for investment plans not captured by equity Q.

Philippon (2009) finds that a proxy of Q obtained from bond yields is also highly correlated

with investment activities. Philippon’s bond Q series end in 2007, which is five years before the

end of our sample. However, bond Q is highly correlated with credit spread. For example, the

correlation between changes in bond Q and changes in credit spread over four quarters is 0.84. In

column (5), we include changes in credit spread in the past four quarters in lieu of bond Q. In

addition, credit spread can be relevant as a control also because it may reflect credit availability

and financial constraints. The coefficient on this variable is negative and significant—consistent

with theory—but CFO expectations retain significant explanatory power.

Overall, CFO expectations explain investment plans beyond market-based Q proxies,

statistically and economically. Indeed, CFOs may possess information that markets participants

either do not possess or process imperfectly. To the extent that managers’ and markets’ views

differ, it is natural that managers’ beliefs have a major impact on investment decisions. As we

show in Section 5.3, this result also extends to actual capital spending.

5.1.2. CFO Expectations and Alternative Theories of Investment

We now test the role of expectations against alternative theories of investment. We introduce

a set of variables motivated by these theories, which are the key controls in our analysis.

Time-varying Discount Rates

(^12) As illustrated in Section 4, proxies of Q are supposed to represent the Q model precisely, whereas survey data can only represent it approximately. Thus it may not be surprising that Q proxies remain significant in regressions that include survey expectations.

A prominent idea in traditional finance holds that variations in required returns, or discount

rates, are central to explaining investment in both financial and real assets (e.g. Cochrane 1991,

2011). Lamont (2000) postulates that firm investments rise and fall in response to changes in

discount rates so that high investment growth is associated with low future stock returns. Lettau

and Ludvigson (2002) argue that time-varying risk premia, as proxied for by the

consumption-wealth ratio (known as cay ), can forecast future investment growth. In Table 4

columns (6) to (8), we control for three common measures of discount rates: log dividend yield,

cay , and the surplus consumption ratio as constructed by Campbell and Cochrane (1999). cay is

somewhat significant, surplus consumption is not, and dividend yield tends to enter with the

wrong sign. The explanatory power of CFO expectations is unaffected. We get similar results if

we include these variables in past twelve month changes instead of in levels.

We can also control for risk premia implied by long run risks models, as constructed by

Bansal, Kiku, Shaliastovich, and Yaron (2014). Unfortunately their series is annual, which leaves

us with few observations. We interpolate the series to quarterly frequencies in multiple ways and

find it tends to enter with the wrong sign. Taken together, none of these variables compare in

their explanatory power to CFO expectations, and their inclusion does not have much of an

influence on the coefficient on expectations.^13

Because proxies for discount rates are generally quite persistent, their coefficients can suffer

from Stambaugh (1999) biases. In our case, Stambaugh bias will tend to attenuate the

coefficients on discount rates toward zero or make them have the wrong sign.^14 In Appendix C

Table C6, we report Stambaugh bias adjusted results, using a multivariate version of the

bootstrap method in Baker, Taliaferro, and Wurgler (2006). The bias adjusted results are very

similar.

Financing Constraints

A well-known empirical result, dating back to Fazzari, Hubbard, and Petersen (1988), is that

investment is positively correlated with recent firm cash flows. The leading interpretation is that

(^13) Our results also resonate with recent findings by Sharpe and Suarez (2013) and Kothari, Lewellen, and Warner (201 4 ) that changes in discount rates and user cost of capital have limited impact on investment, and that corporations appear to apply constant hurdle rates 14 in making investment decisions. Stambaugh bias arises when predictor variables are relatively persistent, and innovations in predictor variables and outcome variables are correlated. In theory, investment should be high when discount rates are low. Thus we would expect a negative coefficient on discount rates. To the extent that innovations in investment and discount rates are negatively correlated, Stambaugh bias will be upward, pushing the coefficient on discount rates closer to or above zero.

5.1.3. Reverse Causality

One possible concern is our baseline results could be affected by reverse causality.

Specifically, if a firm plans to invest a lot in the next twelve months, managers might also expect

earnings to increase as investment leads to more output and sales. This mechanism seems

unlikely to be driving our results. First, investment in the next twelve months generally does not

translate into output and sales immediately. Second, even if it does, investment is an incremental

addition to the capital stock. It is unlikely that a one percent increase in investment (which

increases the firm’s capital stock by much less than one percent) can instantly lead to a one

percent or more increase in firm earnings, as would be required to match the magnitude of

coefficients in the data.

We further address the reverse causality concern in supplementary tests, drawing on another

question in the CFO survey, which asks respondents to rate their optimism about the US

economy on a scale from 0 to 100 (with 0 being the least optimistic and 100 the most optimistic).

In Appendix C Table C1, we show that CFOs’ optimism about the US economy is significantly

positively correlated with investment. It is hard to argue that firms’ investment plans will

mechanically cause CFOs to be more optimistic about the US economy. Instead, this result is

very much in line with previous findings that firms’ expectations and sentiments appear to be a

key driver of investment activities.

In Appendix C Table C2, we present the same set of tests using analyst expectations. We find

analyst expectations are also significantly correlated with investment plans, although not

surprisingly the magnitude of the relationship is smaller; the coefficients on analyst expectations

are generally about one half of the size of the coefficients on CFO expectations. The evidence

suggests that expectations elicited from different sources are consistent, and there are general

views shared by managers and the market that play an important role in shaping aggregate

investment dynamics.

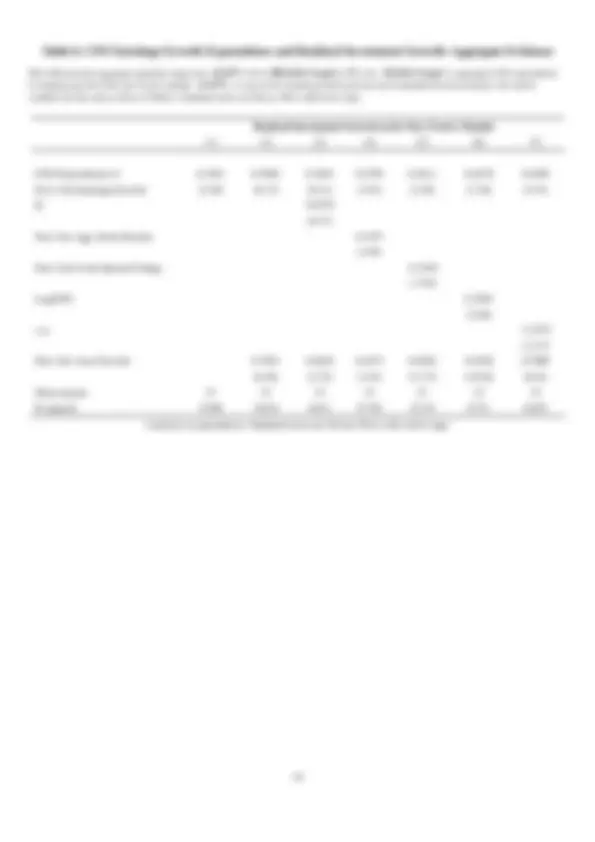

5. 2 Expectations and Investment Plans: Firm-level Evidence

In Table 5, we repeat our analysis at the firm level. As before, we start with CFO data. We

estimate

∆CAPX̂i,q𝑡 = α + ζ𝑖 + βE𝑖,q^ ∗^ 𝑡[∆Earnings𝑖] + λXi,q𝑡 + ϵi,q𝑡

We report baseline results with firm fixed effects. Results are very similar without fixed effects,

or with dynamic panel estimators.^16 Table 5 shows that at the firm level, CFO expectations

continue to have substantial explanatory power for investment decisions. The response of a

firm’s investment plans to CFO expectations is similar in magnitude to the relationship unveiled

in the aggregate analysis of Table 4: When CFOs expect earnings growth to increase by one

percentage point, planned investment growth increases by 0.4 percentage points on average. We

then compare CFO expectations with firm-level Q and past twelve month firm stock returns. We

use the book-to-market ratio as a proxy for firm-level required returns, and all other firm-level

controls directly correspond to their aggregate counterparts in Table 4. After including these

controls, alone or together, CFO expectations remain statistically and economically significant.

We also examine results adding time fixed effects and the findings are similar.

In Appendix C Table C3 we replicate the firm-level analysis with analyst expectations. The

results show that analyst expectations about a firm’s earnings growth can also explain investment

plans. As before, the size of the coefficients on analyst expectations is about one half of that on

CFO expectations. While CFO expectations play a more dominant role, business outlook shared

by managers and specialist analysts is nonetheless informative about investment decisions.

5.3 From Plans to Realized Investment

A premise for our analysis in Sections 5.1 and 5.2 is that investment plans are key

determinants of actual capital spending. With lags in investment implementation, expectations in

a given quarter may not translate into realized investment instantly, so changes in plans can help

us pinpoint the impact of expectations, and plans will turn into capital expenditures over a period

of time. In this section, we evaluate this proposition empirically. In Figure 3 Panel B it is evident

that, at the aggregate level, plans and realized investment over the planned period are closely

related. The raw correlation between the two series is 0.78.^17 Figure 3 Panel B also shows that

(^16) To the extent that strict exogeneity may not be satisfied, fixed effect estimators may be biased in finite sample. In our context, it will bias the coefficient on earnings expectations downwards. Regressions without fixed effects and those using dynamic panel methods show that the bias does not appear to be very important. Given that we do not always continuously observe individual firms in the CFO sample, it is difficult to take first differences and use lagged instruments. Instead, for dynamic panel estimations we apply the forward orthogonal deviations (FOD) transformation as in Arellano and Bover (1995). 17 Figure 2 uses aggregate investment as measured by private non-residential fixed investment from NIPA. We can alternatively use capital expenditures data from Flow of Funds or Compustat, and results are very similar.