Portfolio Risk Calculation: A simple

illustration

Finance II

11th November 2009

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

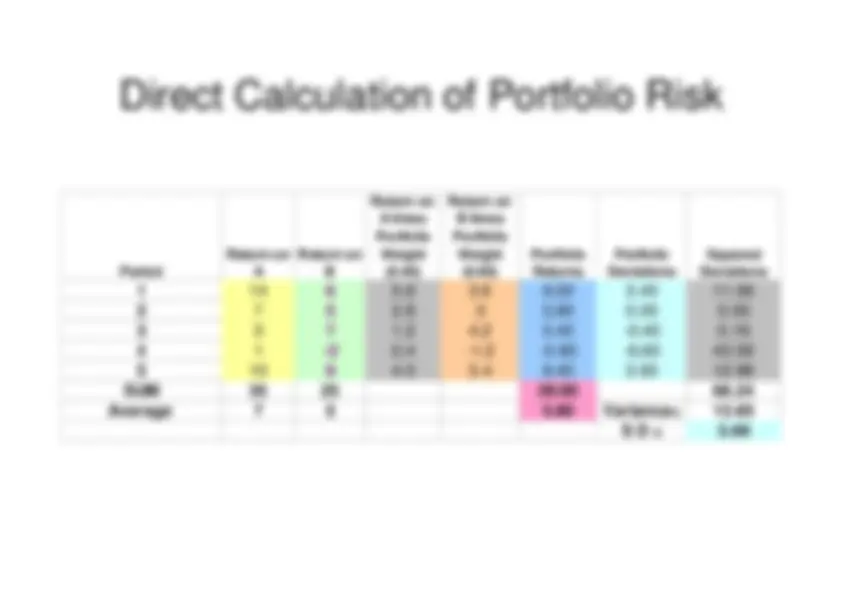

An illustration of portfolio risk calculation using two securities a and b. The portfolio weights, return deviations, squared deviations, and calculations for both direct and indirect methods of portfolio risk calculation. Additionally, the document shows an example of calculating portfolio risk using market data.

Typology: Lecture notes

1 / 7

This page cannot be seen from the preview

Don't miss anything!

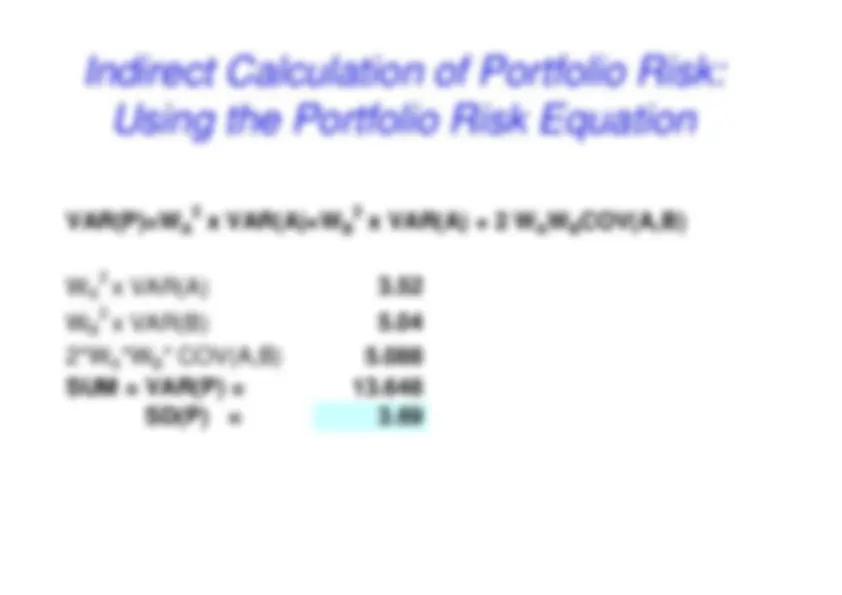

There are two securities under consideration for inclusion in a portfolio, A and B

VAR(P)=W

x VAR(A)+W

x VAR(A) + 2 W

W

COV(A,B)

W

x VAR(A)

3.

W

x VAR(B)

5.

2*W

*W

5.

SUM = VAR(P) =

13.

SD(P)

=

3.

Calculating Portfolio Risk Using

Market Data

Portfolio Risk Calculation Continued

1 and 2

1and 3

1and 4

1and 5

2 and 3

2 and 4

2 and 5

c

ulating portfolio

3 and 4

3 and 5

4 and 5

Use Excel Function