Real Estate Development – Principals and Process

Chapters 7-9 Finance

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The goals of borrowers and lenders in real estate development finance, the primary negotiable items in loan agreements, and the use of appraisals in measuring investment performance. It includes definitions, calculations, and examples of net present value (npv), discount rate, internal rate of return (irr), and the gross rent multiplier.

Typology: Slides

1 / 74

This page cannot be seen from the preview

Don't miss anything!

Real Estate Development – Principals and Process Chapters 7-9 Finance

APPRAISALS

Cost Approach – What is the cost of the property? What would cost to replace?

Market Approach – What is the current price being paid for similar properties sold in the area?

Income Approach-What is the current value of the future income stream to be generated by the property?

LOAN CONSTANT

Constant – The annual debt service of a mortgage as percent of the loan.

$100,000 @ 10% for 20 Years = constant. $100,000 x .1158026 = $ 11,580.26 per year or $ 965.02 per month

$100,000 @ 11.5% for 43 Years = constant. $100,000 x .1158443 = $11,584.43 per year or $965.37 Per Month

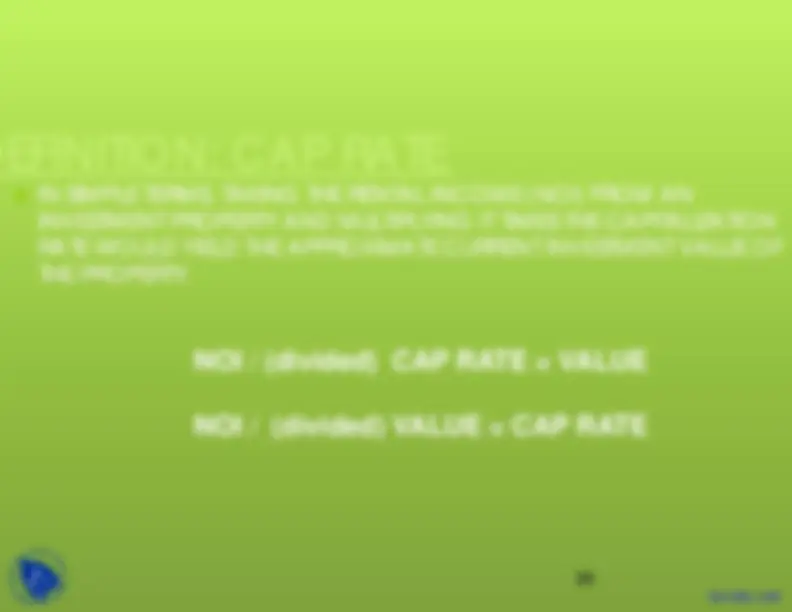

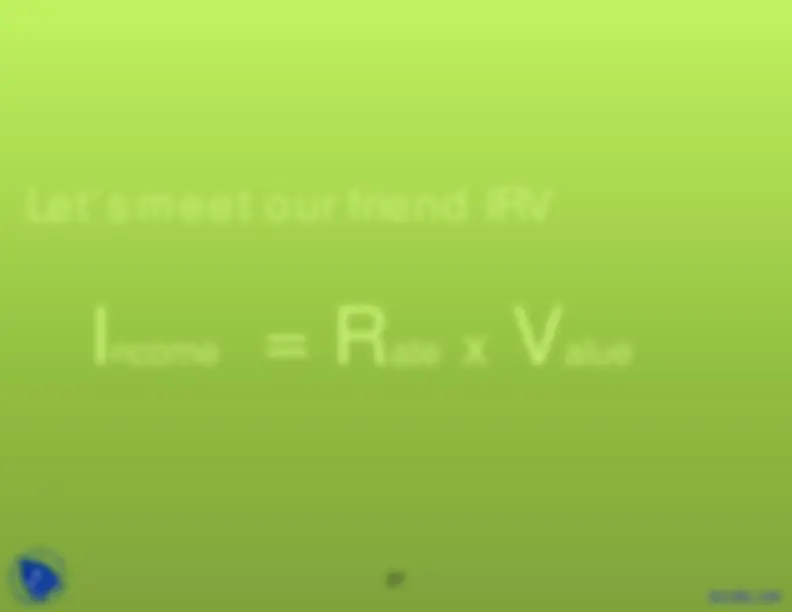

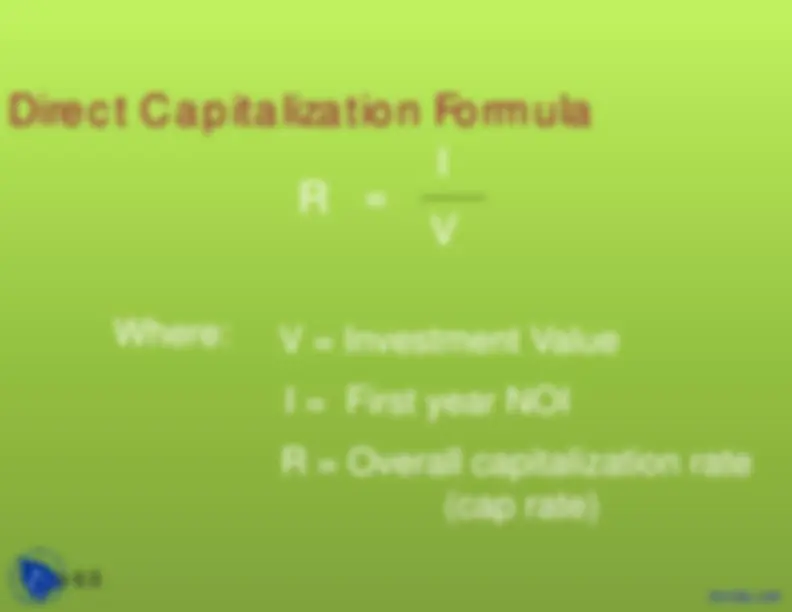

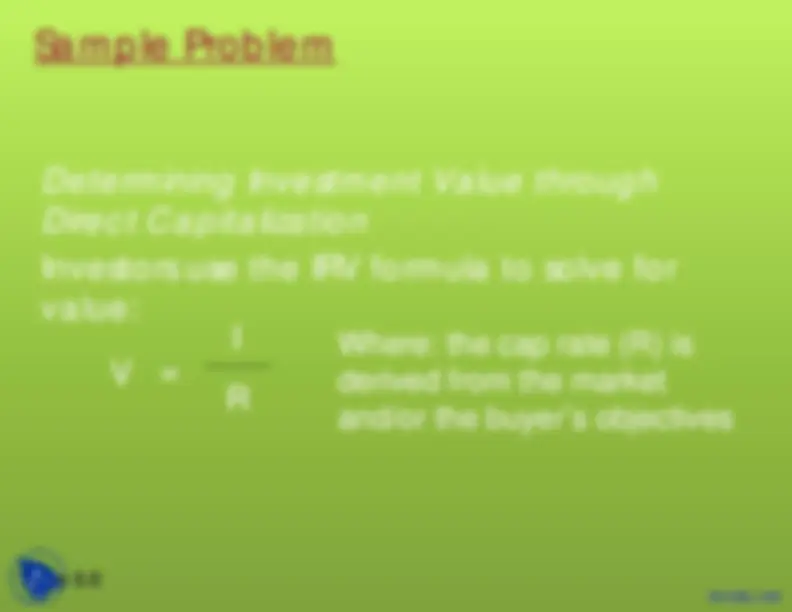

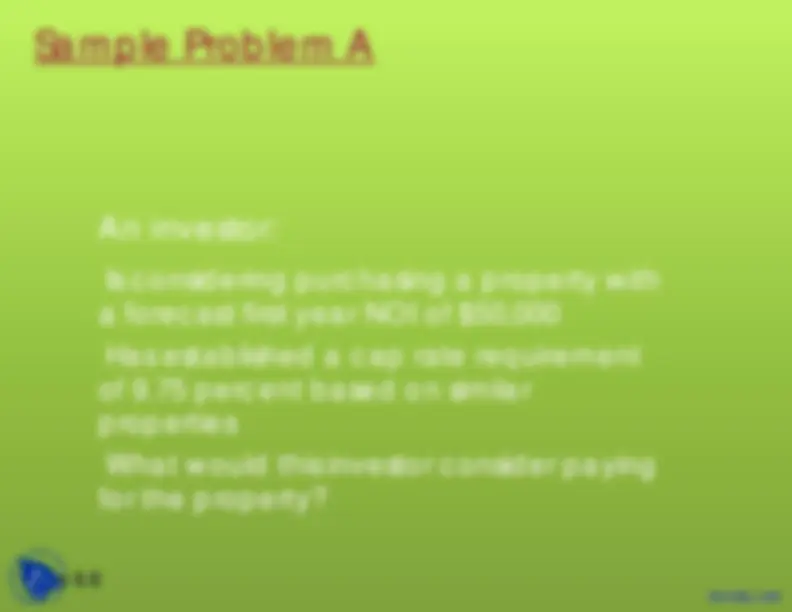

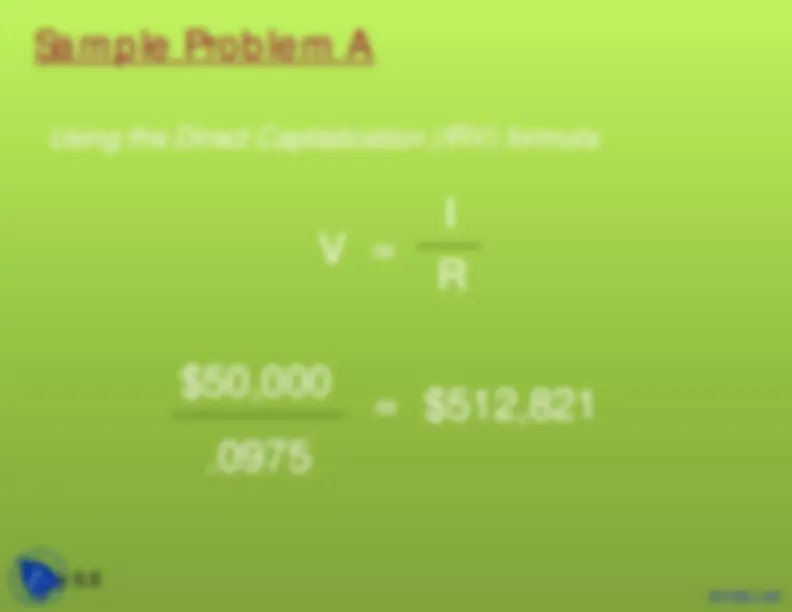

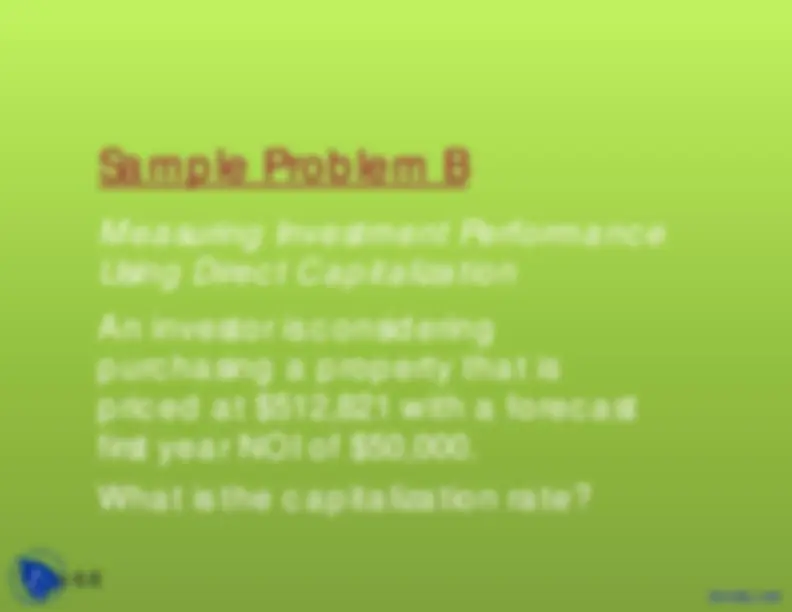

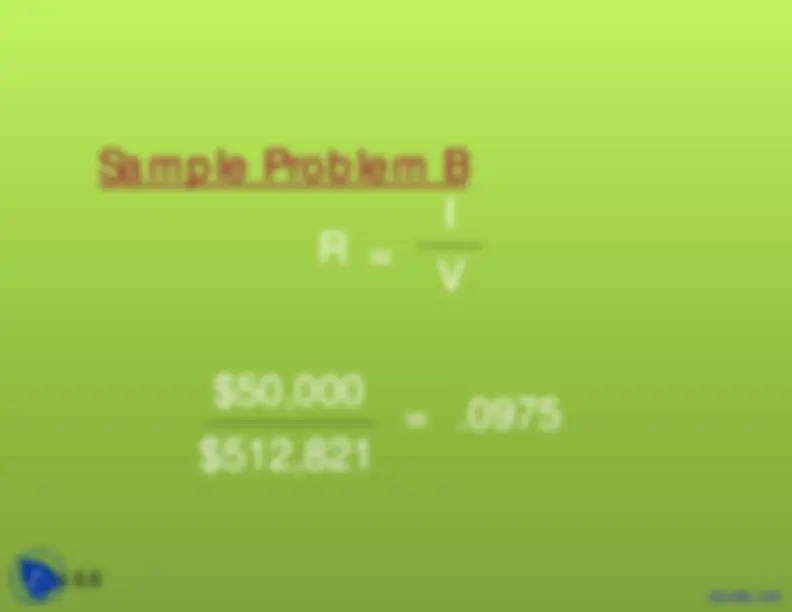

INCOME APPROACH

TO VALUE

Value = Net Income Before Debt Service

Capitalization Rate

OTHER FORMULAS

TO KNOW

Coverage Ratio = Net Income Before Debt Service Loan Payment

Loan Payment = Net Income Before Debt Service Coverage Ratio

Note: The above are derived at Lenders request.

Loan Amount = Net Income Before Debt Service Coverage Ratio Loan Constant

Total Development Cost

Return on Equity = Cash Flow Equity

Cash Flow = Equity x Return on Equity

Learning Objectives

Identify available methods for measuring

investment performance

Define, calculate and interpret measures

of investment performance for selected

sample investments

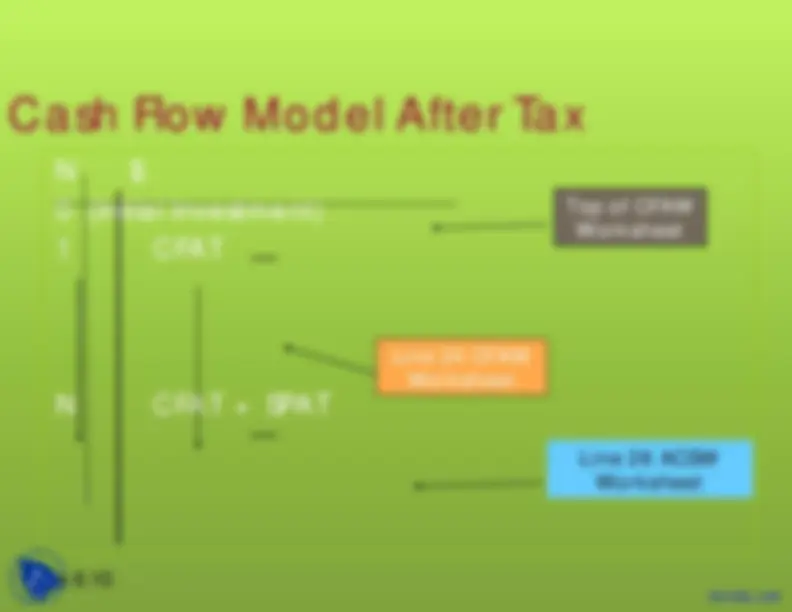

Explain how the Cash Flow Model and its T-

bar are used in the measurement of

investment performance

Page 6.

Learning Objectives

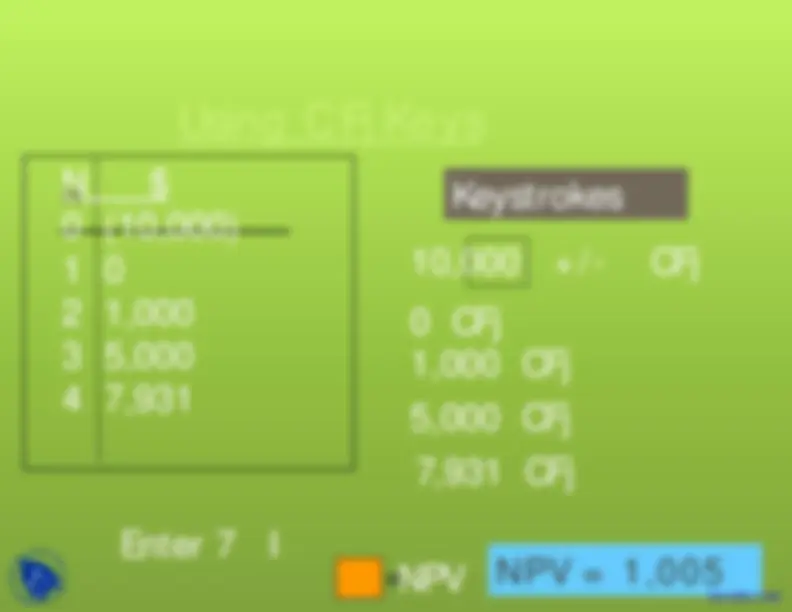

Define, calculate, and interpret net present value (NPV) as a measure of investment performance for selected sample investments

Define discount rate and explain its various uses

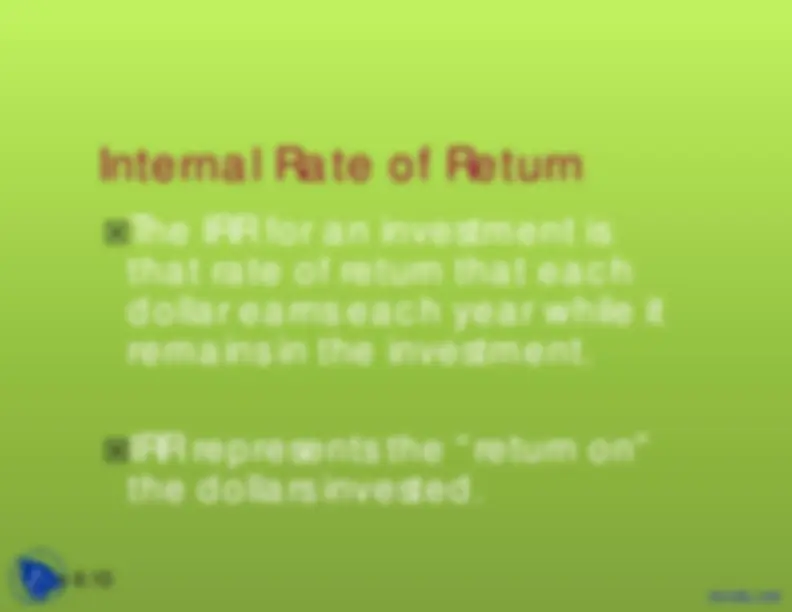

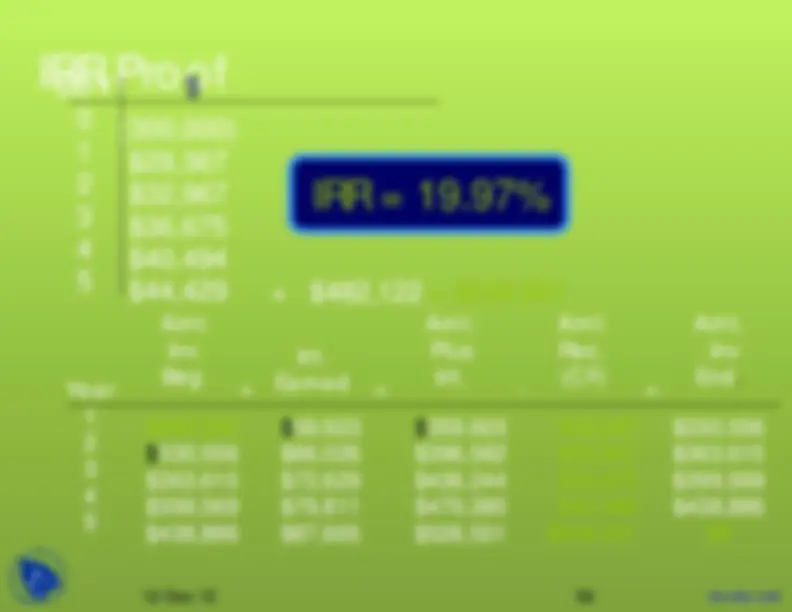

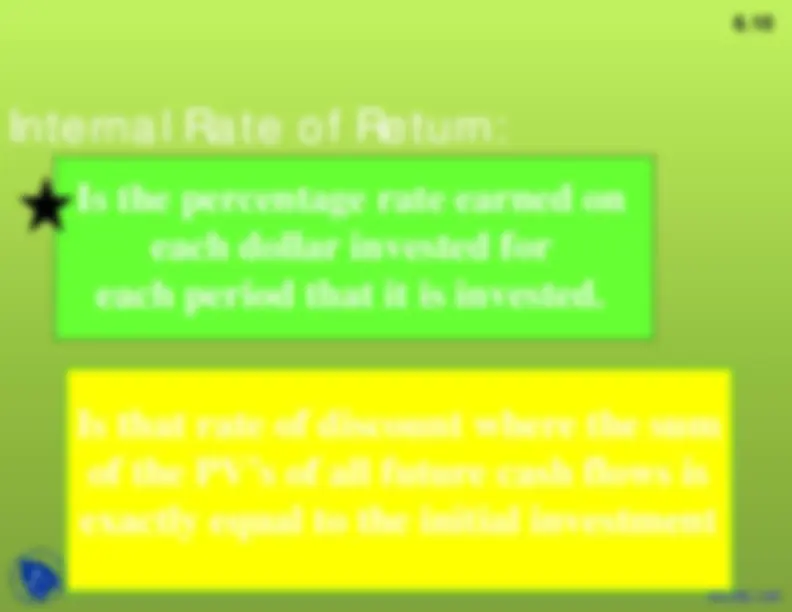

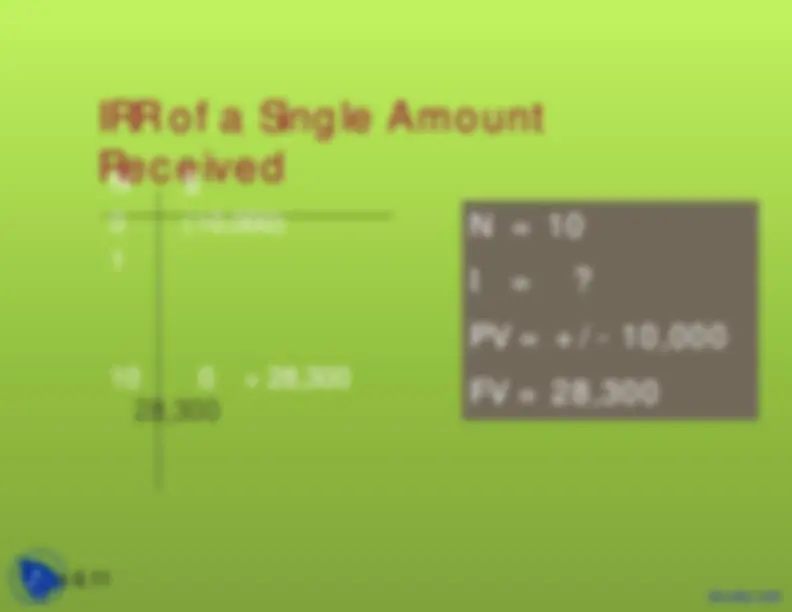

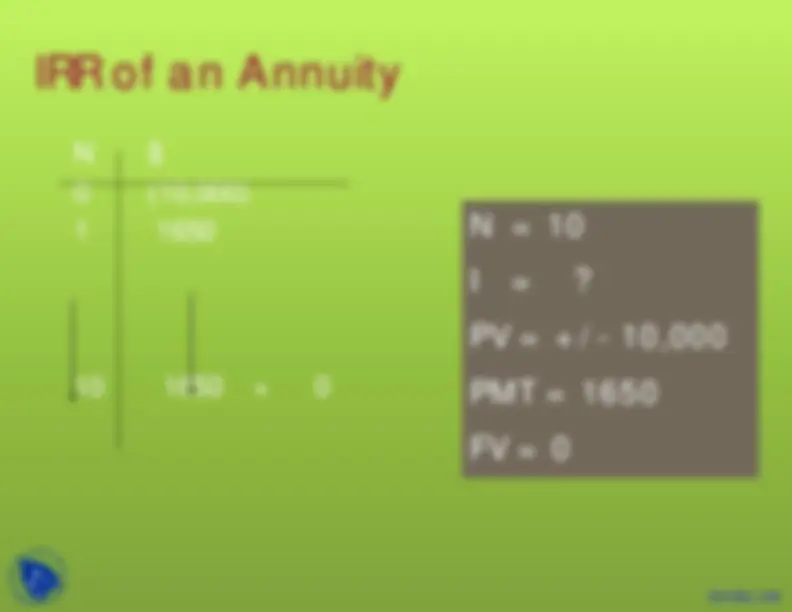

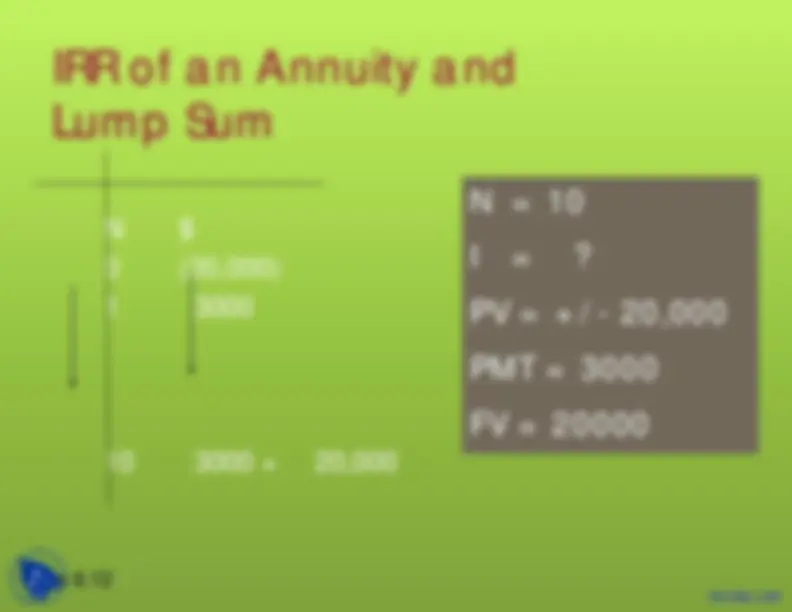

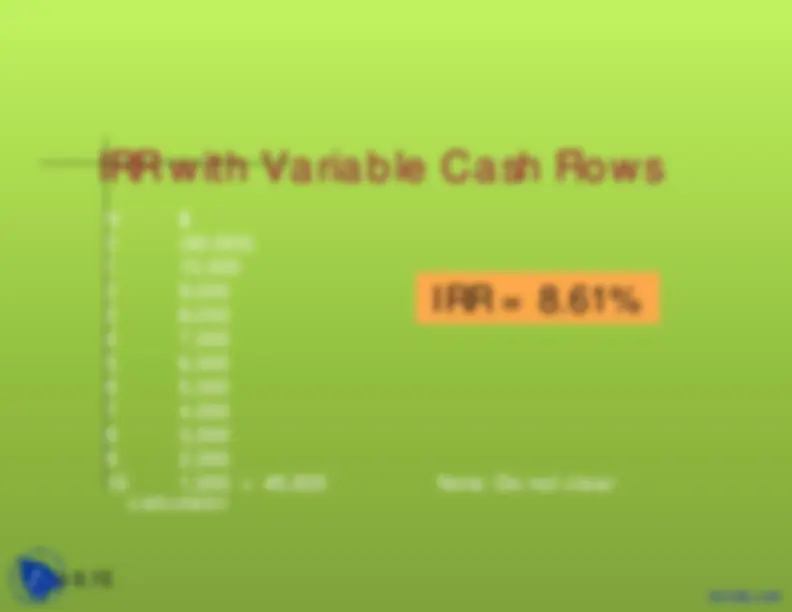

Define, calculate, and interpret internal rate of return (IRR) as a measure if investment performance for selected sample investments

Page 6.

Sales Comparison Approach

The sales comparison approach may

be used to determine what a buyer

will pay for a property given the price

per square foot or per unit.

Price/square foot

Total square feet of building

Investment Value

×

Page 6.

Sales Comparison Approach

otal Square feet of building

= Price per square foot

Page 6.

Gross Rent Multipliers (GRM)

Calculates the investment value of a

property by using the “gross rents”

anticipates the property will produce

The GRM used is derived from

comparable properties in the

marketplace and may be adjusted by

the investor to reflect specific

requirements

Page 6.

Gross Rent Multiplier × Forecast 1 st^ Year PRI = Value

Determining Investment Value Using

the Gross Rent Multiplier

Property is forecast to have $100,000 first year PRI

Potential buyer GRM Requirement is 7

Investment value is calculated as:

7 × $100,000 = $700,

Page 6.

Sample Problem

Property is forecast to have $100,000 first year PRI

Potential buyer GRM Requirement is 7

Investment value is calculated as:

= Gross Rent Multiplier

$700,

$100,

= 7

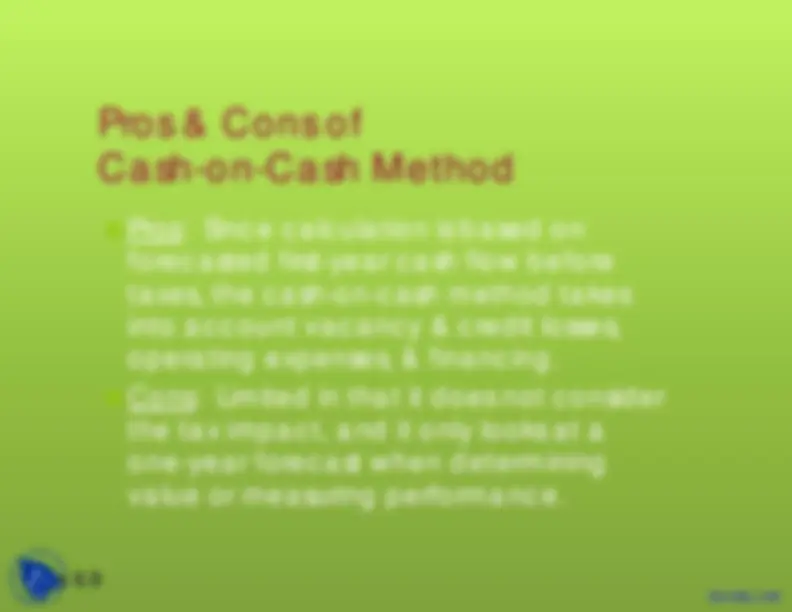

Pros & Cons of Gross Rent

Pros Multiplier

Cons

Any vacancy and credit losses

Any operating expenses

Financing

Any tax impact