Download Financial Statement Analysis: Non-Current Assets - Depreciation and Intangibles and more Study Guides, Projects, Research Finance in PDF only on Docsity!

Financial Statement Analysis

Non-Current Tangible and Intangible

(Fixed) Assets

firm operations.

- Non-current (fixed) assets include

- intangible assets such as goodwill and

- tangible such as property, plant and equipment.

- Three main stages are relevant for the examination of

the financial reporting and analysis issues:

Acquiring the Asset: the Capitalisation

Decision

- The costs of acquiring resources that provide services over

more than one operating cycle are capitalised and carried

as non-current assets on the balance sheet.

- All costs incurred until the asset is ready for use must be

capitalised.

- Conceptual merits of capitalisation and expensing are

debatable in the case of some components and certain

categories of acquisition costs.

- The decision to capitalise or expense interest during

construction, software development costs, research and

development costs, and exploration costs for oil and gas

properties depends to some extent on management choice.

Profit variability

- Firms that capitalise costs and depreciate them over

time will show “smoother” patterns of reported income.

- Firms that expense costs as incurred will tend to have

greater variance in reported profit.

Levels of profit

- The effects on profitability depend on how profit is

measured. As the discussion on profit variability implies, the effect on reported profits or return on sales depends on the actual pattern of expenditures

- On the other hand, because expensing firms show lower

assets (and equity) on the balance sheet, as the firms grows larger, their ROA/ROE measures are higher when compared to firms that capitalise costs.

Property, plant and equipment

- Property, plant and equipment (PPE) are tangible assets that an

entity holds for its own use or for rental to others that the entity

expects to use during more than one period.

- The consumption of PPE is reflected through a depreciation charge

designed to reduce the asset to its residual value over its useful life.

- Where assets are revalued they will be shown at fair value (for

property this would be market value) at the date of revaluation, less

any subsequent accumulated depreciation and impairment losses.

- Any revaluation gain is taken straight to equity (Revaluation

Reserve) and losses treated as an expense in income statement.

- A company will assess any impairment losses at each balance

sheet date. Wherever indicators of impairment exist, a review for

impairment will be carried out and the company will charge any loss

in value to the income statement.

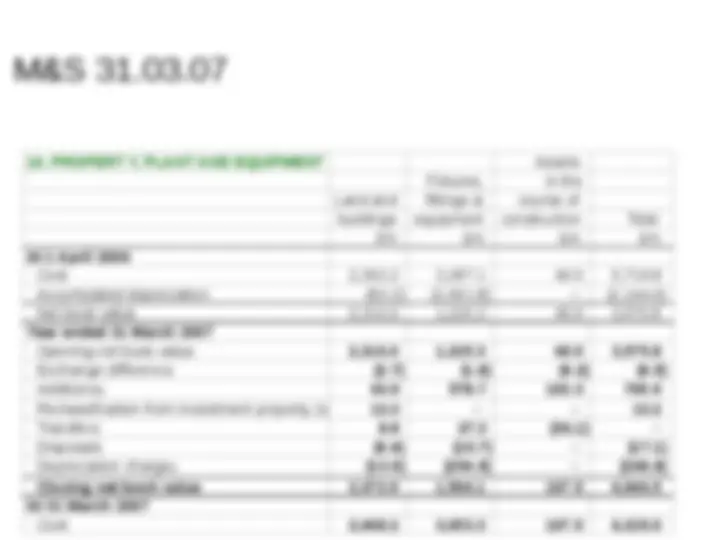

Accumulated depreciation (95.3) (2,089.2) – (2,184.5) Net book value 2,372.9 1,564.1 107.5 4,044.

- Capitalisation of Interest

- For the purposes of analysis, remove any capitalised interest

from fixed assets and add it to interest expense, thus lowering

profit.

- The interest coverage ratio should be calculated with capitalised

interest included in interest expense. Otherwise it will be

distorted.

- Leased assets

- PPE under a finance lease is recognised by a lessee at the lower

of the present value of the minimum lease payments and the fair

- A controversial area; what can and cannot be recognised

as an intangible asset.

- Intangible asset = “an identifiable nonmonetary asset

without physical substance”

- Intangible assets bought separately are capitalised at cost.

- Intangible assets obtained in the course of acquiring a business are

recognised separately from goodwill if their value can be measured

reliably on initial recognition.

- Goodwill is non-identifiable

- Examples:-

- Concessions, patents, licences, trademarks.

- Brands.