CHAPTER 10:

REPLICATION, SYNTHETICS

AND ARBITRAGE

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

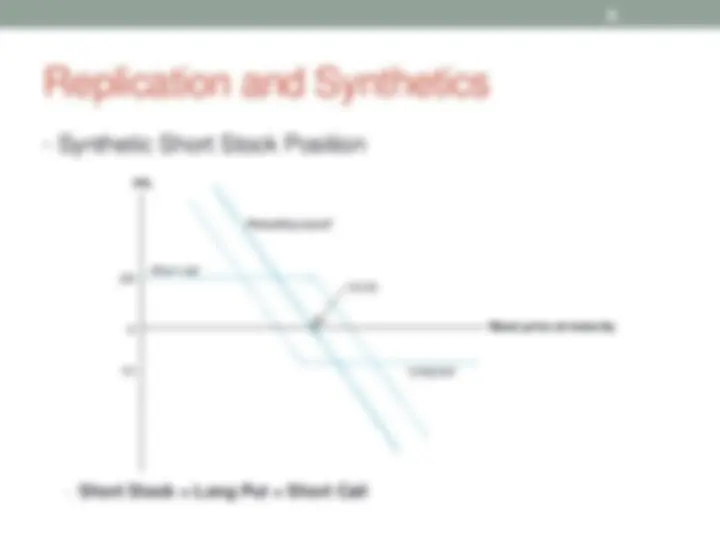

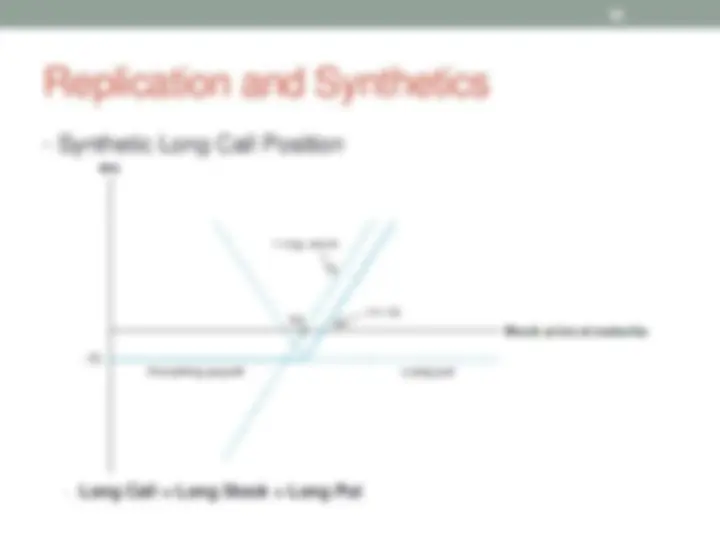

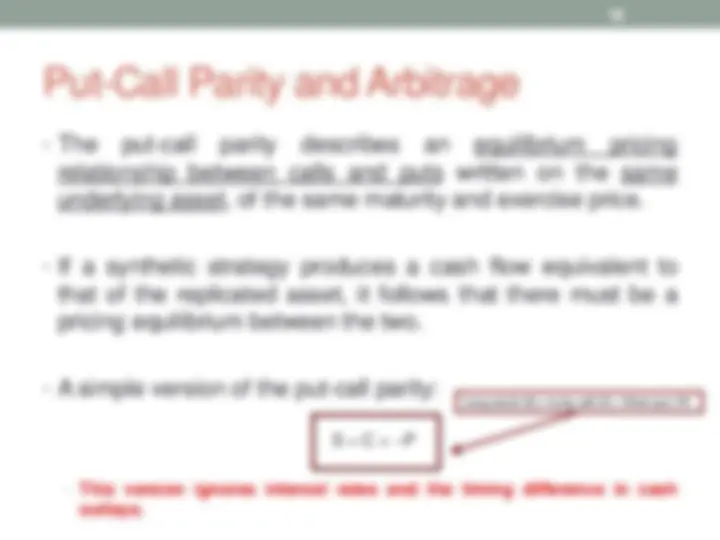

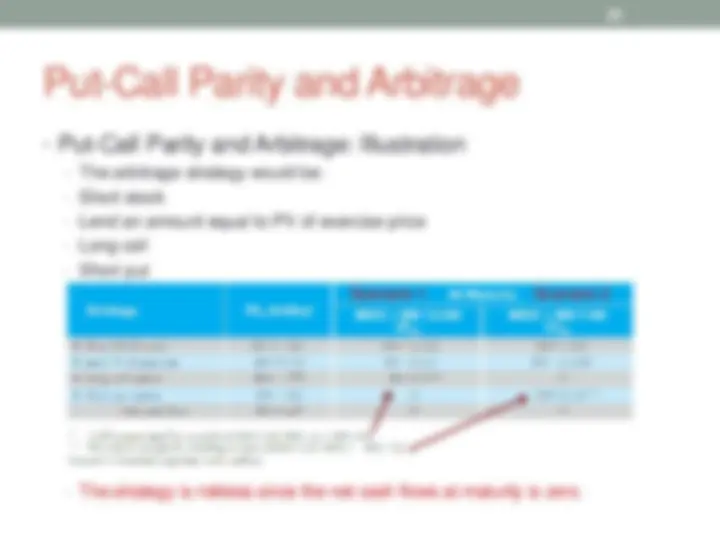

This chapter delves into the concepts of replication and synthetics in finance, focusing on the put-call parity relationship. It explains how to create synthetic positions using options and the underlying asset, demonstrating how arbitrage opportunities arise when there is a deviation from the put-call parity. The chapter provides practical examples and illustrations to solidify understanding.

Typology: Lecture notes

1 / 34

This page cannot be seen from the preview

Don't miss anything!

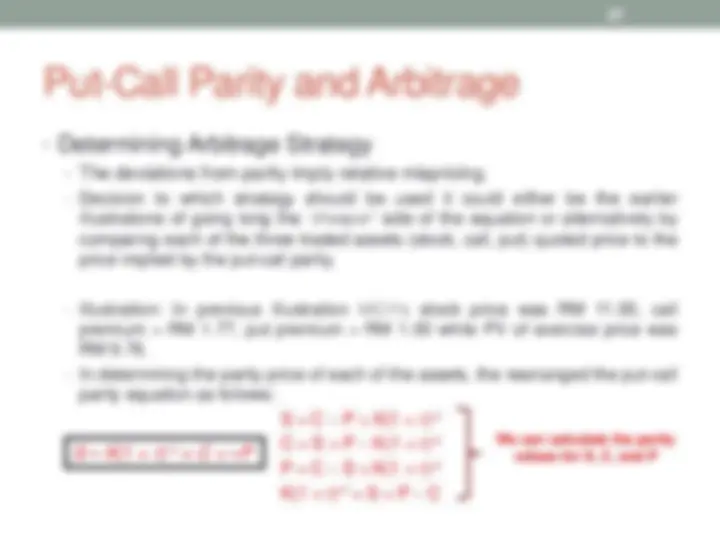

` S – K ( 1 + r ) – t^ = C + – P