Cashflow Estimation

S S S Kumar

Financial Management

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

A comprehensive guide on cash flow estimation, focusing on incremental cash flows in the context of financial management. The author emphasizes the importance of accurate cash flow information for making sound business decisions. General guidelines for cash flow estimation, incremental cash flows calculation, and deconstructing the basic cash flow pattern. It also discusses relevant points to remember when dealing with sunk costs, opportunity costs, inflation treatment, and overhead allocations.

Typology: Exercises

1 / 17

This page cannot be seen from the preview

Don't miss anything!

Financial Management

Cashflows and capital budgeting (^) Decisions are only as good as the information used to make them. Cashflows estimation is a multi disciplinary approach

Incremental cash flows (^) Incremental cash flows are cash flows that will occur if a project is accepted, but that will not occur if the investment is rejected. “What is different if project is accepted?” The cash flows of the firm with the project minus the cash flows of the firm without the project Project CFt Firm'sCFt with project Firm'sCFt without project

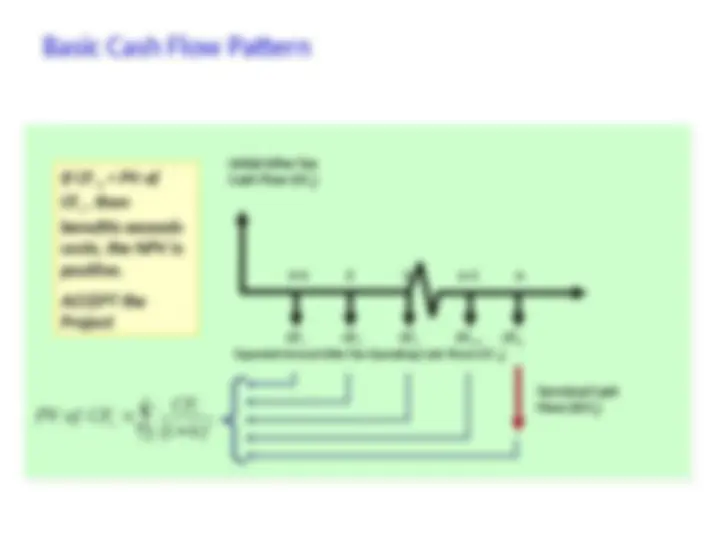

Basic Cash Flow Pattern Initial After-Tax Cash Flow ( CF 0 ) Expected Annual After-Tax Operating Cash Flows ( CF (^) tt ) t= 1 2 3 n-1 n CF 1 CF 2 CF 3 CFN-1 CFN Terminal Cash Flow ( ECFn ) If CF 0 < PV of CFt , then benefits exceeds costs, the NPV is positive. ACCEPT the Project n t t t t k CF PV of CF 1 (^1 )

Initial cashflow (^) The initial cashflow is basically the amount of money the firm has to spend to get the new project started. Cash outflow at beginning of project (time period zero) (^) Includes cost of acquiring fixed assets (purchase price plus other costs incurred in getting asset to your company and up and running, such as shipping, installation, etc.) Also includes changes in net working capital caused by proposed project

Net working capital (^) Increase in NWC = outflow (additional cost of project) (^) Decrease in NWC = inflow (savings created by project)

Terminal Cashflows Include after tax salvage value and reduction in net working capital

Terminal Cashflows (^) Include after tax salvage value and reduction in net working capital

Why? (^) The cost of capital already incorporates interest and dividend affects in the analysis by way of discounting process. (^) If we include them as cash flows, we would be double counting capital costs.

Cashflows: points to remember (^) Sunk costs (^) Opportunity costs Inflation treatment (^) Overhead allocations Include all externalities

16 Cashflows: points to remember Example: Currently your salary is Rs 12 lakhs per annum. You decide to enroll in this programme by opting for a half – pay job for this year. The annual tuition fees for the programme is approximately Rs.250,000. What is the total cost of your PG course?

17