Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An overview of capital budgeting, its importance in financial management, and the process of making long-term investment decisions. It covers the concept of cash flows, cash flow patterns, steps in the capital budgeting process, types of capital budgeting projects, and various capital budgeting techniques. The document emphasizes the significance of maximizing shareholder wealth through careful evaluation of investment projects.

Typology: Summaries

1 / 52

This page cannot be seen from the preview

Don't miss anything!

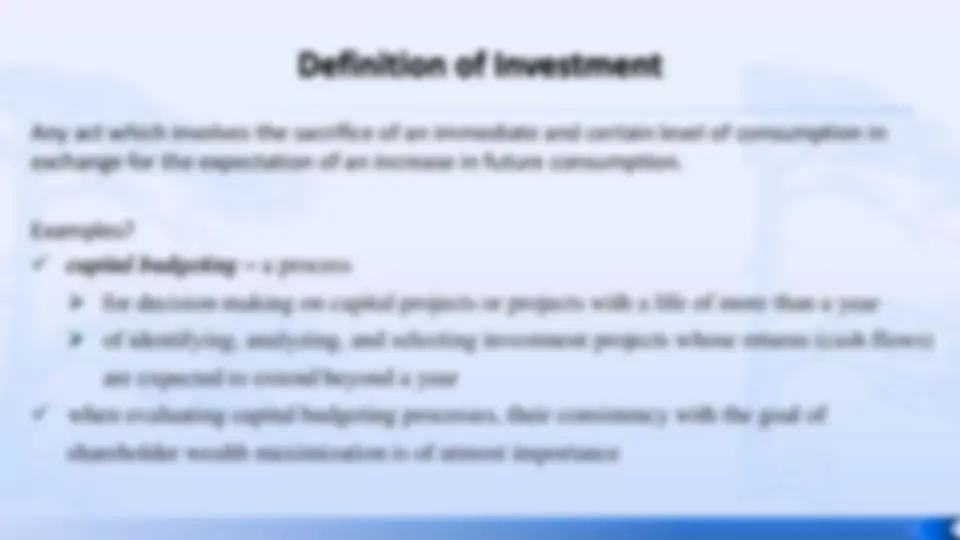

What is investment

Why do we need for investment Appraisal

How to apply the investment appraisal techniques

What are Advantages and disadvantages of different investment appraisal techniques

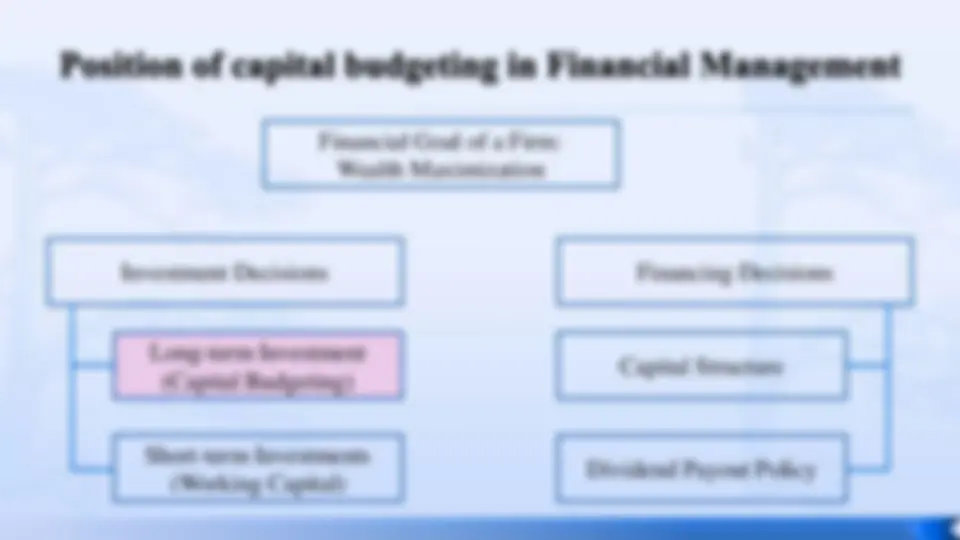

Financial Goal of a Firm:

Wealth Maximization

Investment Decisions Financing Decisions

Short-term Investments

(Working Capital)

Long-term Investment

(Capital Budgeting)

Dividend Payout Policy

Capital Structure

✓ It is the most significant financial activity of the firm

✓ It determines the core activities of the firm over a long term future

✓ It must be made carefully and rationally

Wrong decisions could be costly

Difficult and expensive to reverse

Organisation objectives

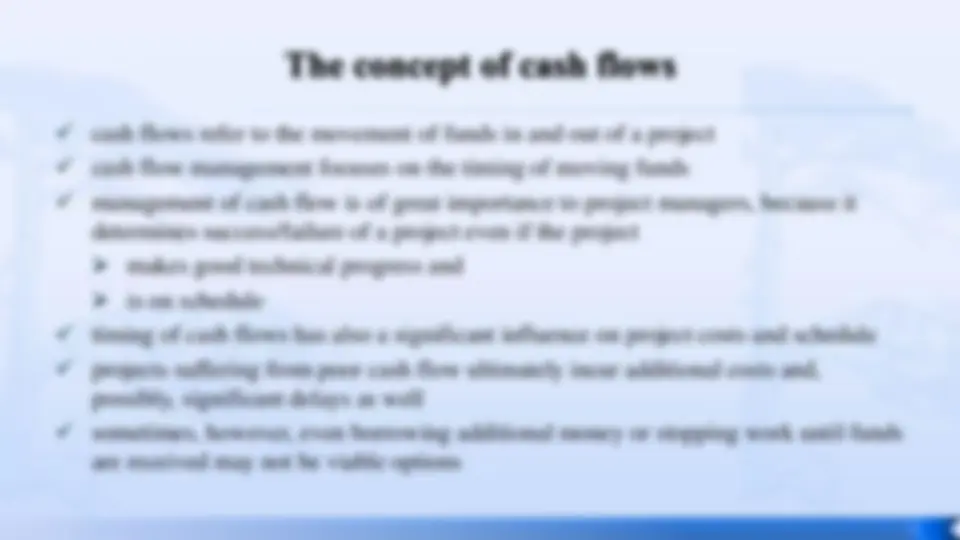

✓ cash flows refer to the movement of funds in and out of a project

✓ cash flow management focuses on the timing of moving funds

✓ management of cash flow is of great importance to project managers, because it

determines success/failure of a project even if the project

➢ makes good technical progress and

➢ is on schedule

✓ timing of cash flows has also a significant influence on project costs and schedule

✓ projects suffering from poor cash flow ultimately incur additional costs and,

possibly, significant delays as well

✓ sometimes, however, even borrowing additional money or stopping work until funds

are received may not be viable options

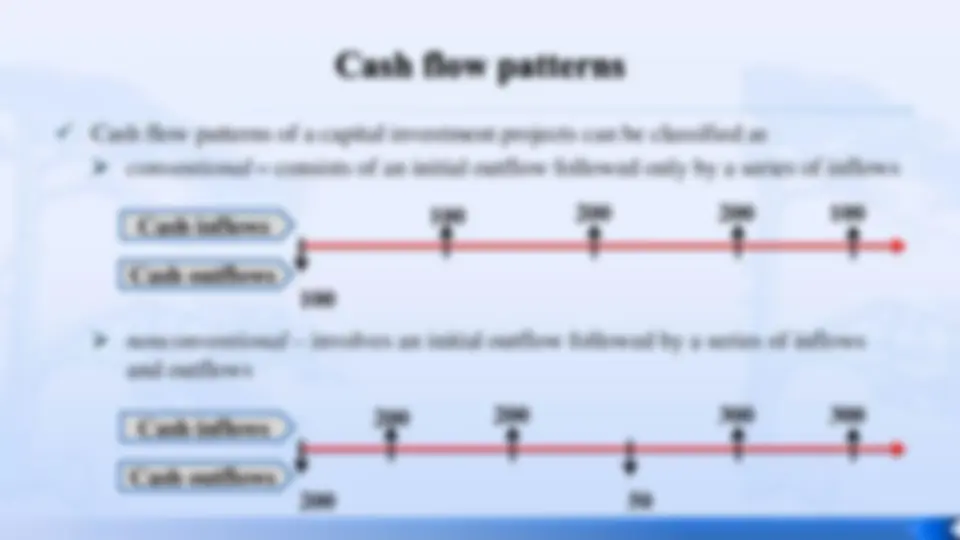

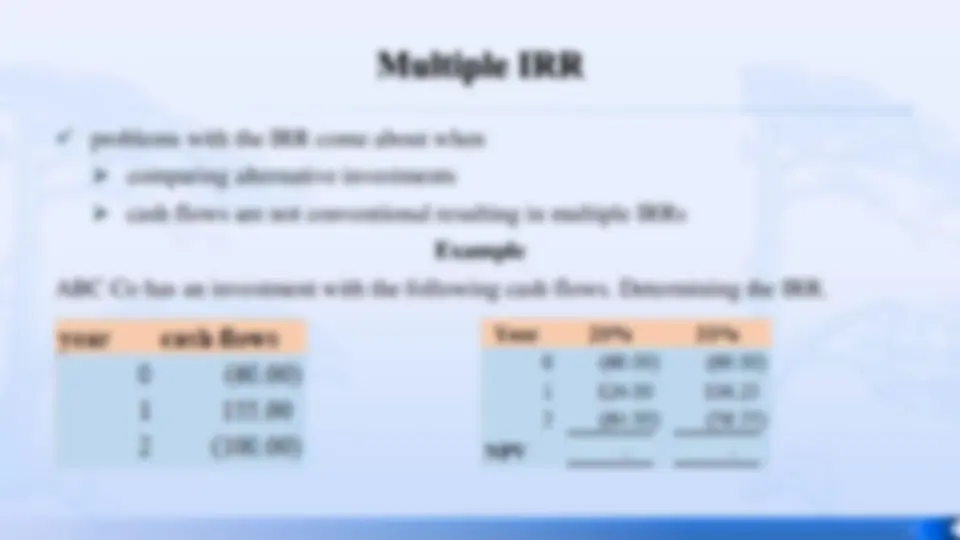

✓ Cash flow patterns of a capital investment projects can be classified as

➢ conventional – consists of an initial outflow followed only by a series of inflows

➢ nonconventional – involves an initial outflow followed by a series of inflows

and outflows

Cash outflows

Cash inflows

Cash outflows

Cash inflows

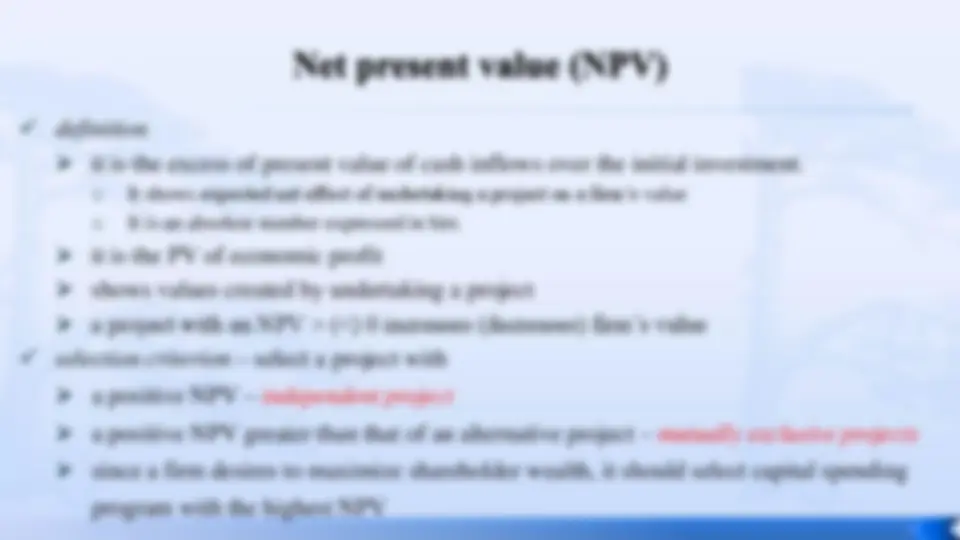

➢ independent projects – accept/reject decision for a project is not affected by the accept/reject

decisions of other projects

➢ mutually exclusive projects – selection of one alternative precludes selection of another

alternative

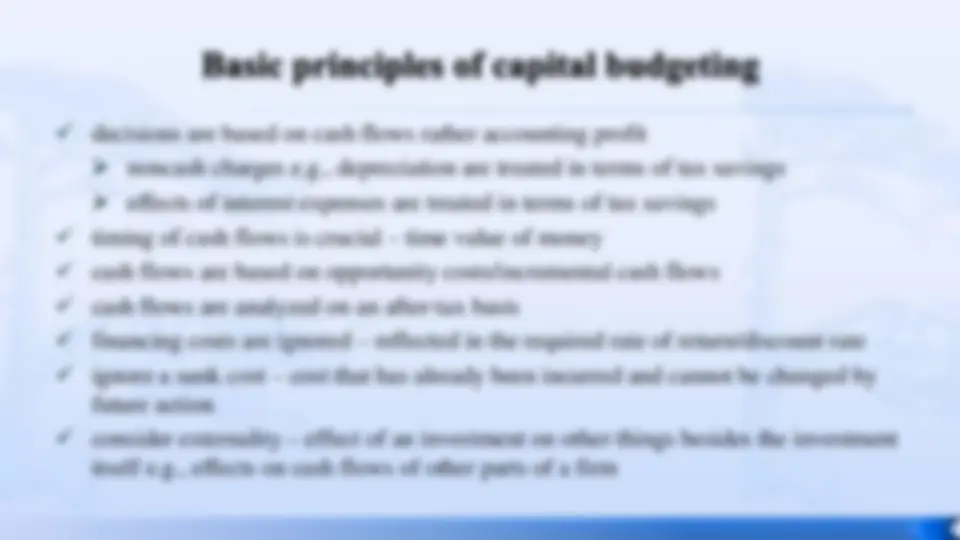

✓ decisions are based on cash flows rather accounting profit

➢ noncash charges e.g., depreciation are treated in terms of tax savings

➢ effects of interest expenses are treated in terms of tax savings

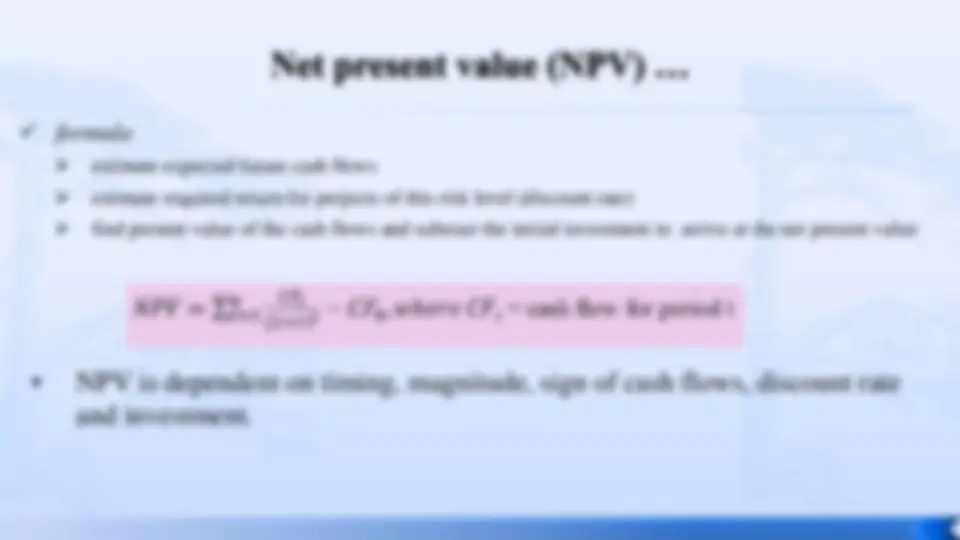

✓ timing of cash flows is crucial – time value of money

✓ cash flows are based on opportunity costs/incremental cash flows

✓ cash flows are analyzed on an after-tax basis

✓ financing costs are ignored – reflected in the required rate of return/discount rate

✓ ignore a sunk cost – cost that has already been incurred and cannot be changed by

future action

✓ consider externality – effect of an investment on other things besides the investment

itself e.g., effects on cash flows of other parts of a firm

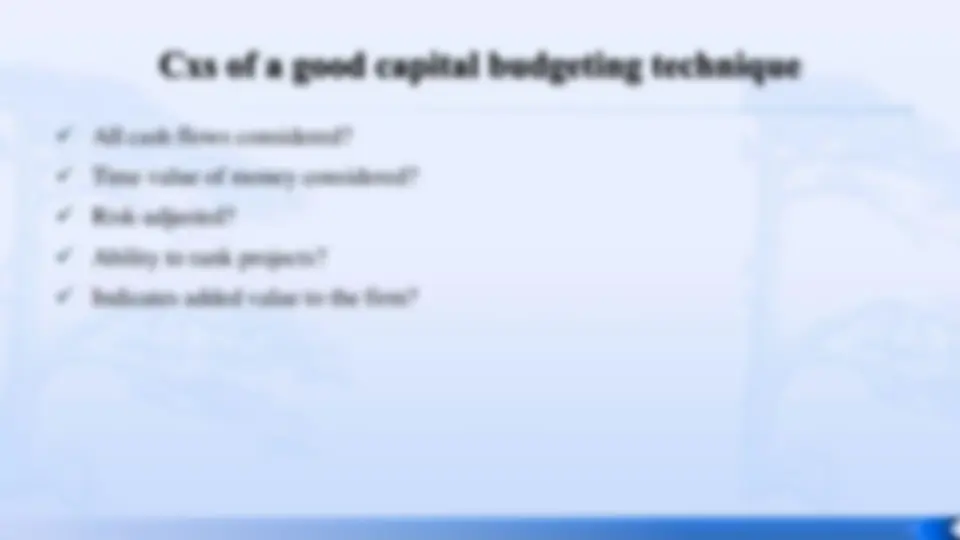

✓ All cash flows considered?

✓ Time value of money considered?

✓ Risk-adjusted?

✓ Ability to rank projects?

✓ Indicates added value to the firm?

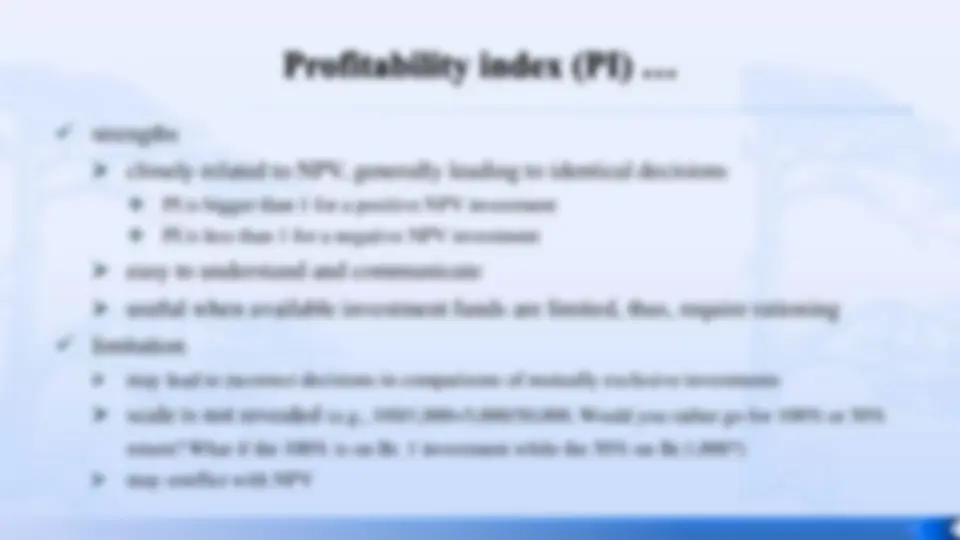

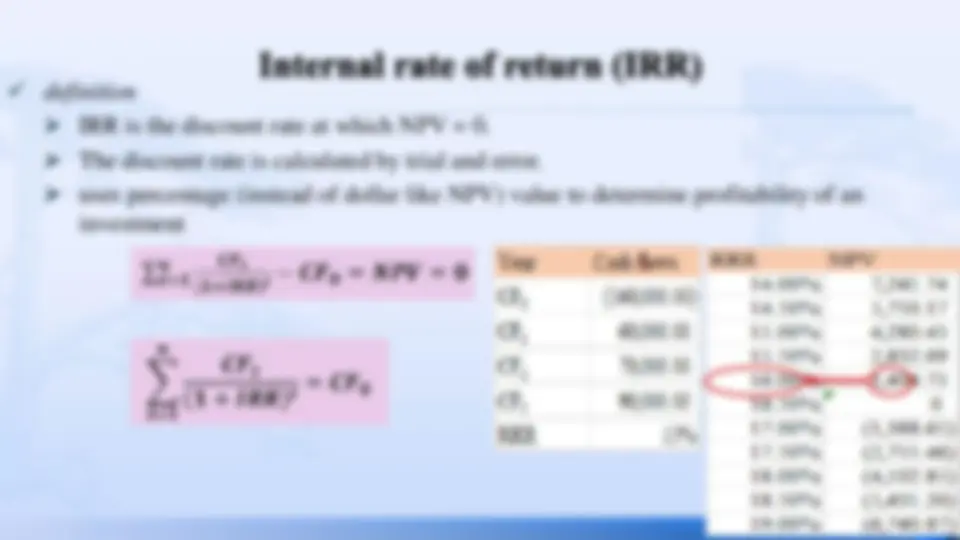

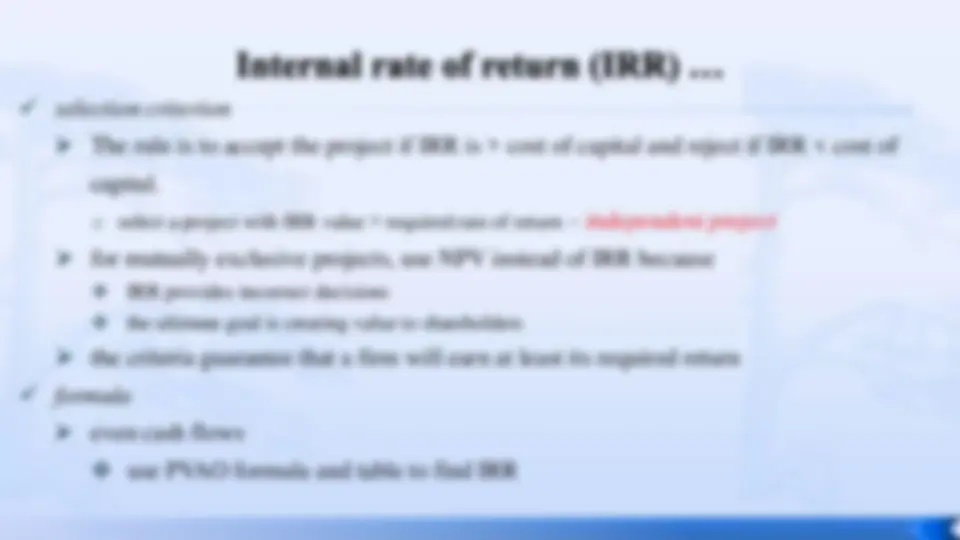

➢ modern/discounted cash flow methods (DCF)

❖ consider time value of money

❖ include NPV, profitability-index (benefit-cost ratio), IRR, and discounted

payback period

❖ each method requires estimating cash flows and their timing for each project

❑ after tax cash outflows (costs) and inflows (revenues/savings)

❖ each method requires estimating project’s risk to determine an appropriate

discount rate (opportunity cost of capital)

❖ main weakness of DCF methods is that some of the above data is difficult to

obtain

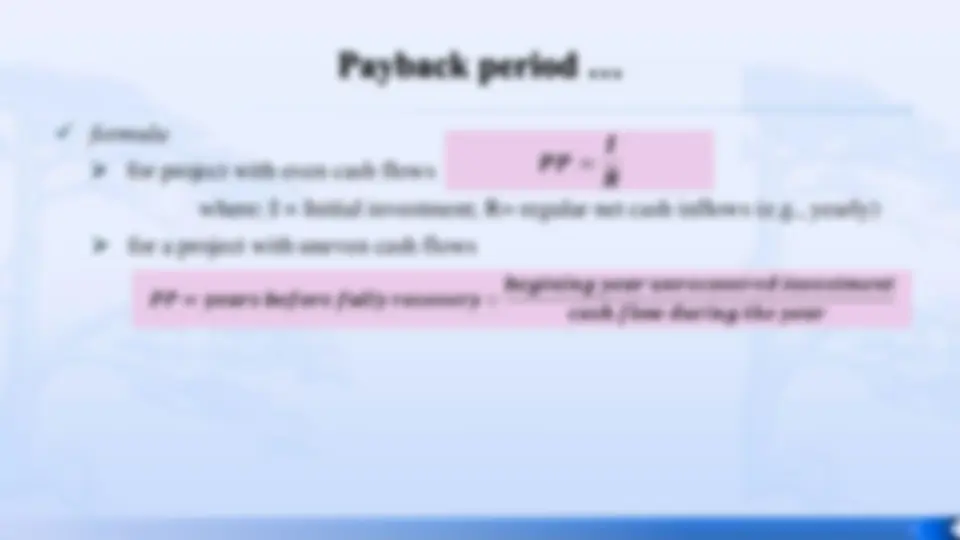

✓ Payback method – length of time it takes to repay the cost of initial investment

o one of the simplest ways of measuring an investment’s worth.

✓ selection criterion – select a project with a payback period

➢ less than a cutoff – independent project

➢ shorter than that of an alternative project – mutually exclusive projects

❑ The rule is to accept those projects that have a payback period less than the limit set by

the management.

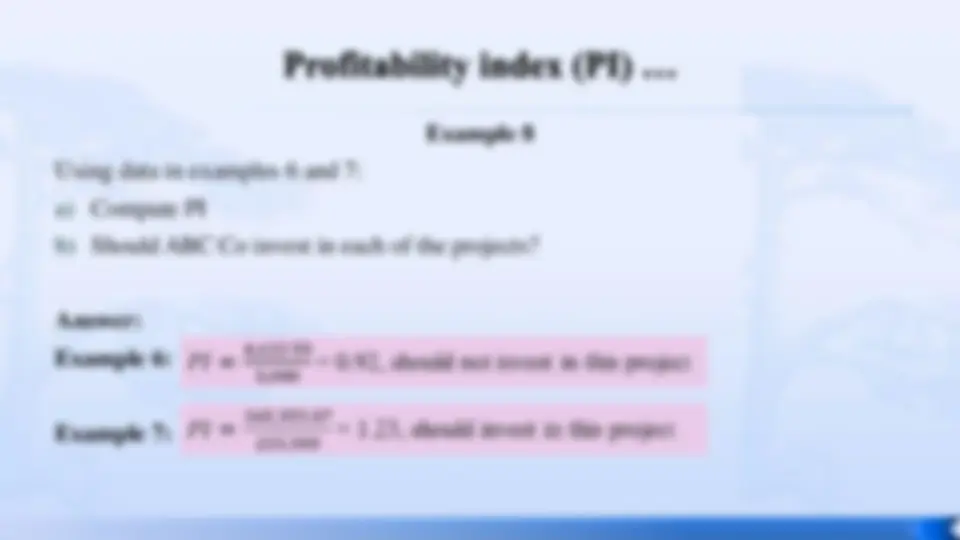

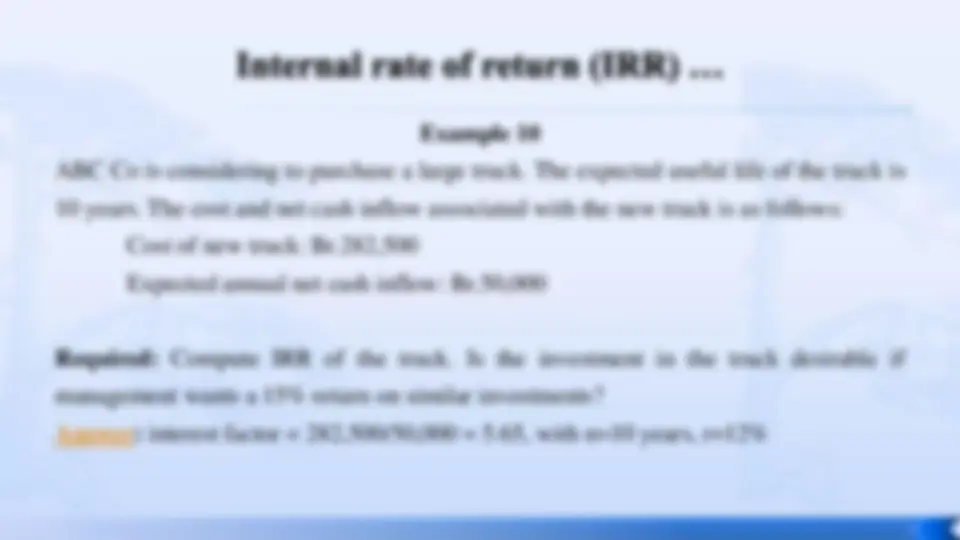

Example 1

ABC Co is considering to purchase a new machine for Br. 360 , 000. The life of the

machine is 10 years. The machine will reduce annual costs by Br. 50 , 000.

Required:

a) Compute the payback period for the machine.

b) Would the company purchase the new machine if the maximum desired payback

period of the management is 8 years?

c) Would the company purchase the new machine if the useful life of the machine is 5

years instead of 10 years? Why?

Answers: a) 7 years, 2 months & 12 days, b) yes! , c) no!, the machine ends without recovering its cost

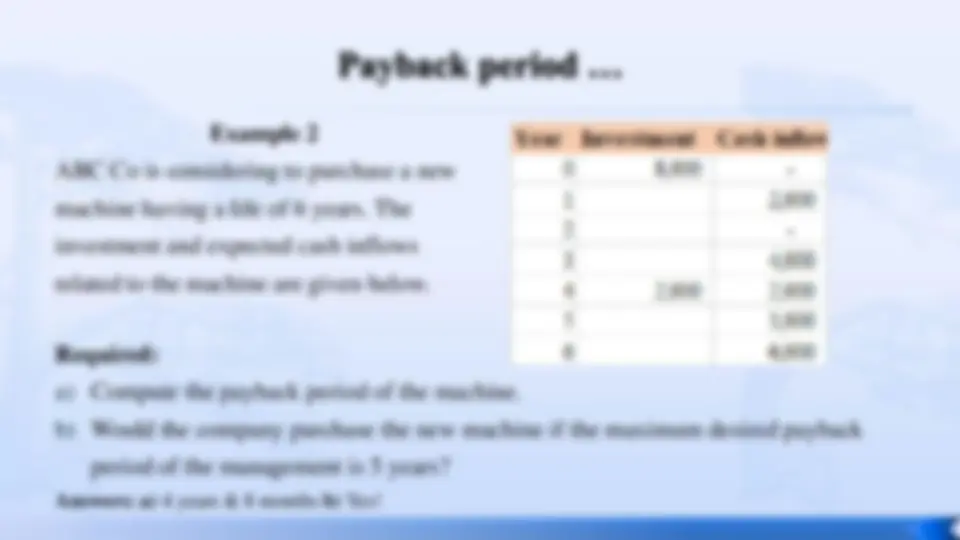

Example 2

ABC Co is considering to purchase a new

machine having a life of 6 years. The

investment and expected cash inflows

related to the machine are given below.

Required:

a) Compute the payback period of the machine.

b) Would the company purchase the new machine if the maximum desired payback

period of the management is 5 years?

Answers: a) 4 years & 8 months b) Yes!