Download Financial Ratios and Sources of Short and Long-Term Finance and more Study notes Financial Management in PDF only on Docsity!

Sources of Finance

Table of Contents:

Section Section Title Slide No.

- Ratios 3

- (^) Short term sources of finance 16

- (^) Long term sources of finance 22

- (^) Thank You 31

The Quick Ratio is sometimes called the "acid-test" ratio and is one of the best measures of liquidity. Quick Ratio = Cash + Government Securities + Receivables / Total Current Liabilities. The Quick Ratio is a much more exacting measure than the Current Ratio. It helps answer the question: "If all sales revenues should disappear, could my business meet its current obligations with the readily convertible `quick' funds on hand?“ An acid-test of 1:1 is considered satisfactory

Quick Ratios

- (^) This ratio reveals how well inventory is being managed.

- (^) Inventory Turnover Ratio = Net Sales / Average Inventory at Cost

- (^) It shows the velocity of conversion of stock into sale

- (^) High IT shows efficient management because more frequently the stocks are sold, lesser amount of money required to finance the inventory Inventory Turnover Ratio

• The ROI is perhaps the most important ratio of all. It is the

percentage of return on funds invested in the business by its

owners. In short, this ratio tells the owner whether or not all

the effort put into the business has been worthwhile. If the

ROI is less than the rate of return on an alternative, risk-free

investment such as a bank savings account, the owner may

be wiser to sell the company, put the money in such a

savings instrument, and avoid the daily struggles of small

business management. The ROI is calculated as follows:

• Return on Investment = Net Profit before Tax / Net Worth

Return on Investment (ROI) Ratio

Debtors turnover ratio or accounts receivable turnover

ratio indicates the velocity of debt collection of a firm.

In simple words it indicates the number of times average

debtors (receivable) are turned over during a year.

[Debtors Turnover Ratio = Net Credit Sales / Average

Trade Debtors]

it help to find average collection period= means number

of days a firm has to wait before its recievables are

converted into cash.

Debtors turnover ratio:

- (^) Operating Ratio = [(Cost of goods sold + Operating expenses) / Net sales] × 100

- (^) Operating ratio shows the operational efficiency of the business. Lower operating ratio shows higher operating profit and vice versa. An operating ratio ranging between 75% and 80% is generally considered as standard for manufacturing concerns Operating Ratio:

- (^) [Capital Gearing Ratio = Equity Share Capital / Fixed Interest Bearing Funds]

- (^) It is used to describe relationship between equity share capital including reserves and surplus to preference share capital and loans.

- (^) Firm can be highly geared if equity shares are more which is good. Capital Gearing Ratio:

LIQUIDITY & SOLVENCY RATIOS

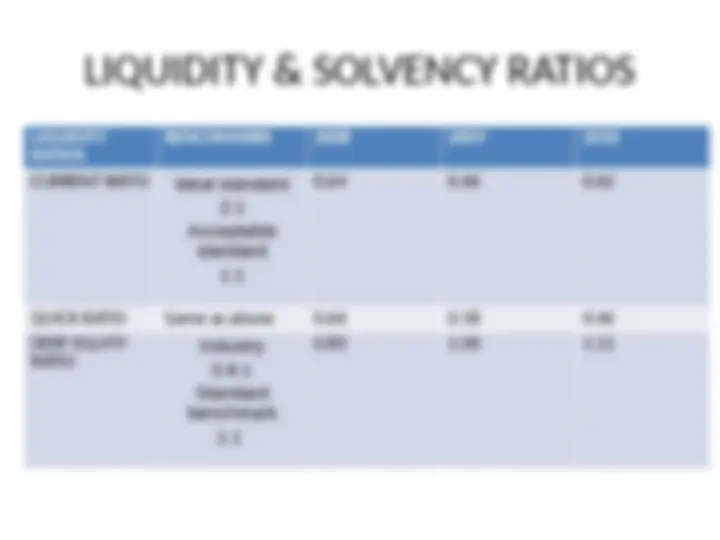

LIQUIDITY

RATIOS

BENCHMARKS 2008 2009 2010

CURRENT RATIO (^) Ideal standard 2: Acceptable standard 1:

QUICK RATIO Same as above 0.66 0.58 0. DEBT EQUITY RATIO Industry 0.6: Standard benchmark 1:

MANAGEMENT EFFICIENCY RATIOS

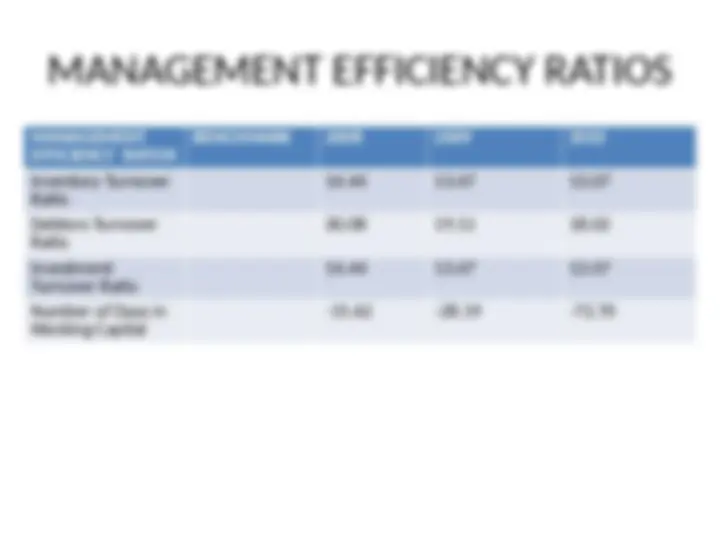

MANAGEMENT

EFFICIENCY RATIOS

BENCHMARK 2008 2009 2010

Inventory Turnover Ratio

Debtors Turnover Ratio

Investment Turnover Ratio

Number of Days in Working Capital

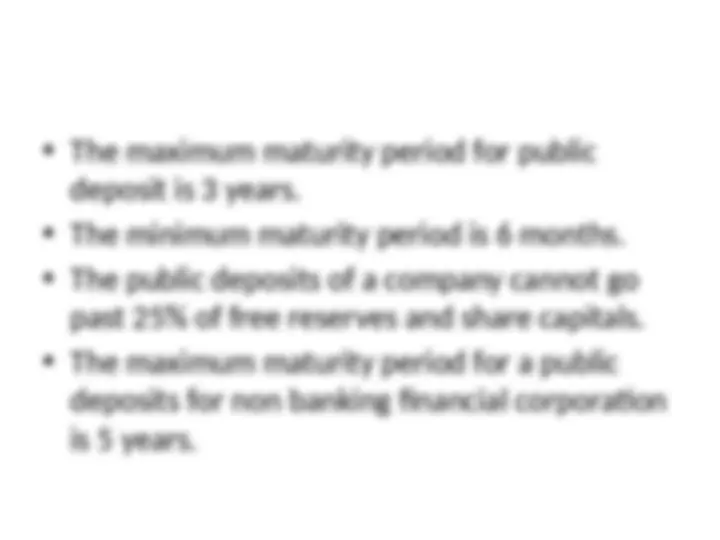

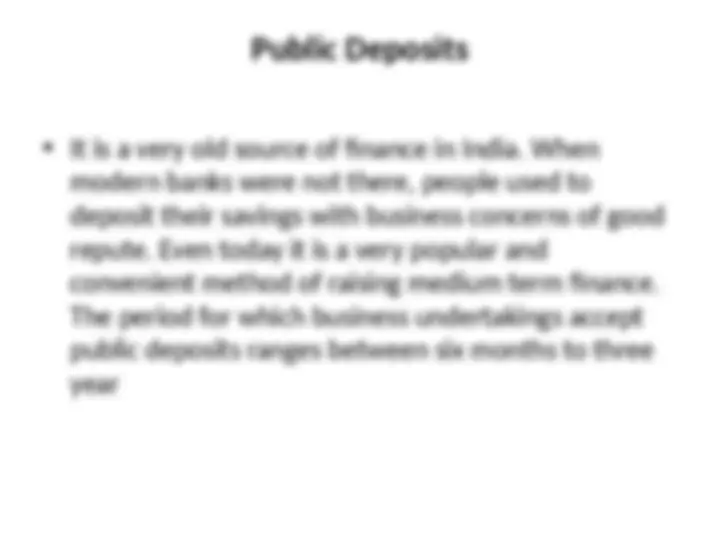

Short-term finance serves following purposes :

1. It facilitates the smooth running of business operations by meeting

day to day financial requirements.

2. It enables firms to hold stock of raw materials and finished product.

3. With the availability of short-term finance goods can be sold on

credit. Sales are for a certain period and collection of money

from debtors takes time. During this time gap, production continues

and money will be needed to finance various operations of the

business.

4. Short-term finance becomes more essential when it is necessary

to increase the volume of production at a short notice

• Bank loans – when bank make advance in lumsome it is called

loan .entire amount is paid in cash or by credit to his account. necessity of paying interest on the payment, repayment periods from 1 year upwards but generally no longer than 5 or 10 years at most. They provide short term loan to meet working capital requirment.

- (^) Overdraft facilities – the right to be able to withdraw funds you do not currently have - (^) Provides flexibility for a firm - (^) Interest only paid on the amount overdrawn - (^) Overdraft limit – the maximum amount allowed to be drawn - the firm does not have to use all of this limit

Short Term Sources of finance

Trade credit – Trade credit refers to credit granted to manufactures and

traders by the suppliers of raw material, finished goods, components, etc. Usuall

business enterprises buy supplies on a 30 to 90 days credit. This means

that the goods are delivered but payments are not made until the expiry

of period of credit. This type of credit does not make the funds available

in cash but it facilitates purchases without making immediate payment.

This is quite a popular source of finance.

Factoring –=A factor is a financial institution which offer services relating to management and financing of debts arrising out of credit sales. The sale of debt to a specialist firm who secures payment and charges a commission for the service. Accruals – provides the opportunity to secure the use of capital without ownership – effectively a hire agreement.

- (^) Installment credit : this is another method by which the assets are purchased and the possession of goods is taken immediately but payment is made in installments over a pre determine period of time.

- (^) Advances : some business house get advances from their customer and agents against orders and this sources is a short term sources of finances for them .it is cheap sources of finances and in order to minimise their investment in working capital.