Download Financial Reporting and Analysis and more Study Guides, Projects, Research Financial Accounting in PDF only on Docsity!

FINANCIAL REPORTING AND ANALYSIS

UNIT 1 : ACTIVITIES

REQUIRED

Use the transactions of SS Stores provided below to prepare the following financial statements:

- Statement of Comprehensive Income for the month ended 30 April 2023.

- Statement of Changes in Equity for the month ended 30 April 2023.

- Statement of Financial Position as at 30 April 2023. INFORMATION Date Transactions of SS Stores for April 2023 01 The proprietor, V. Bheki, commenced her business by depositing R200 000 directly into the bank account of the business. 01 A loan of R100 000 was obtained from Benbank and a direct deposit was made into the account of the business. 05 Purchased stationery from FD Stationers by means of an electronic funds transfer (EFT), R800. 07 Purchased equipment from JK Furnishers via EFT, R40 000. 09 Purchased trading goods on credit from VB Wholesalers, R 44 000. 12 Paid the monthly rental to CS Agency, R4 000. 17 Sold goods on credit to T. Tall for R 3 000 (Cost R2 000). 18 Cash sales as per cash register tape, R21 000 (Cost R14 000). 19 An EFT for R10 000 was made to VB Wholesalers in part settlement of account. Received a discount of R300 on this payment. 23 V. Bheki, the proprietor, took goods at cost for her personal use, R 700. 25 Purchased consumables on credit from RAQ Suppliers, R2 000. 27 Sub-let part of the premises to a tenant, HiHo Boutique. Received a direct deposit of R1 0 00 from them. 28 Received R500 cash from T. Tall in part settlement of his account. Allowed him a discount of R20. 29 Paid the water and electricity bill to the municipality, R3 000. 30 Salaries and wages were paid to the employees, R10 000. 30 Cash sales of merchandise to date, R3 6 000 (cost R24 000). 30 Paid interest on loan to Benbank for April 2023 at a rate of 12% per annum.

FINANCIAL REPORTING AND ANALYSIS

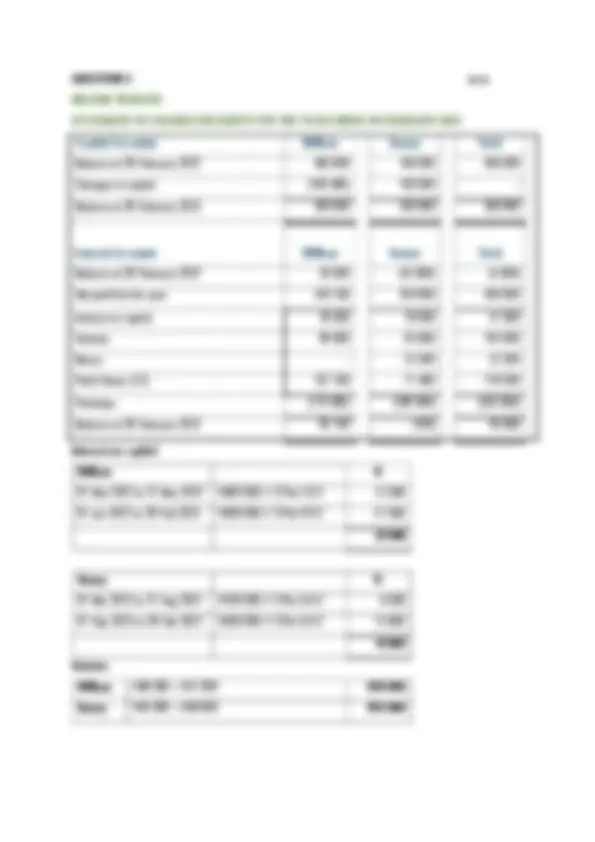

UNIT 1 : SOLUTIONS (Figures in red are the dates of the transactions)

SS STORES

STATEMENT OF COMPREHENSIVE INCOME FOR THE MONTH ENDED 30 APRIL 2023

WORKINGS R

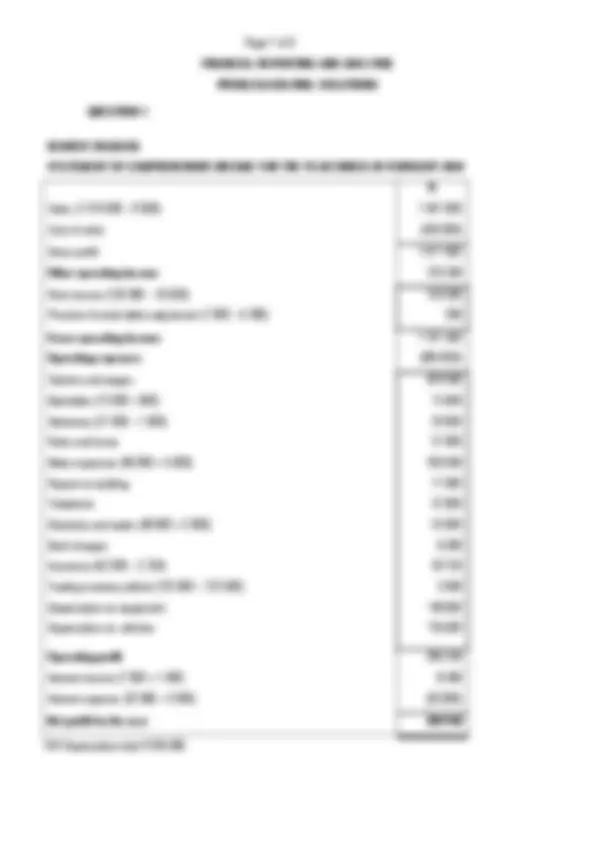

Sales 17 R3 000 + 18 R21 000 + 30 R36 000 60 000 Cost of sales 17 R2 000 + 18 R14 000 + 30 R24 000 (40 000) Gross profit R60 000 – R40 000 20 000 Other operating income R300 + R1 000 1 300 Discount received 19 300 Rent income 27 1 000 Gross operating income R20 000 + R1 300 21 300 Operating expenses R800 + R4 000 + R2 000 + R20 + R3 000 + R10 000 (19 820) Stationery 05 800 Rent expense 12 4 000 Consumable stores 25 2 000 Discount allowed 28 20 Water and electricity 29 3 000 Salaries and wages (^) 30 10 000 Operating profit R21 300 – R19 820 1 480 Interest income 0 Interest expense 30 R100 000 X 12% X 1/12 (1 000) Net profit for the month R1 480 – R1 000 **480

STATEMENT OF CHANGES IN EQUITY FOR THE MONTH ENDED 30 APRIL 2023 R** Balance on 31 March 2023 0 Additional capital contributed 01 200 000 Net profit for the month (See statement of comprehensive income) 480 Drawings 23 (700) Balance on 30 April 2023 199 780

- Cash from debtor (28th): Cash and cash equivalents +; Trade and other receivables – : Discount allowed +; Trade and other receivables –

FINANCIAL REPORTING AND ANALYSIS

UNIT 2: ACTIVITIES

REQUIRED

Use the information provided below to prepare the following financial statements:

- Statement of Comprehensive Income for the year ended 28 February 2023.

- Statement of changes in Equity for the year ended 28 February 2023.

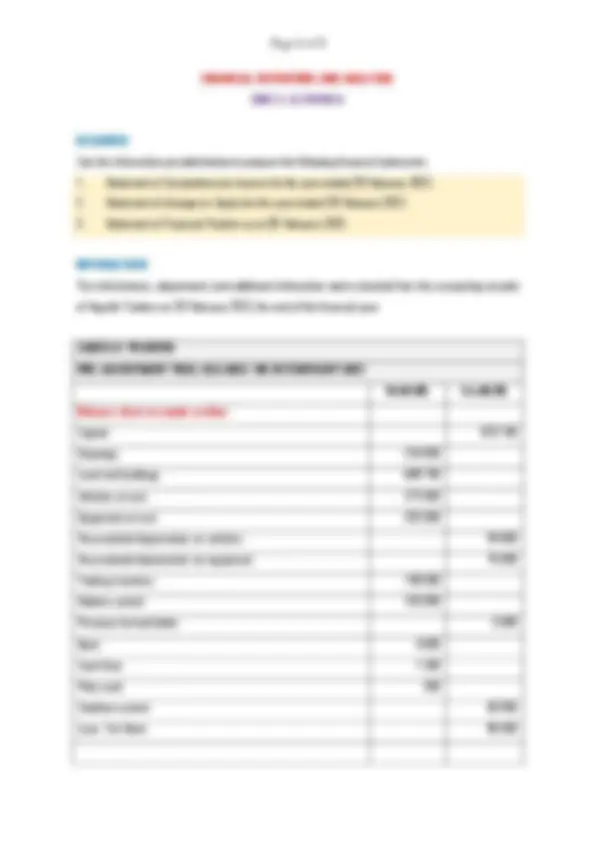

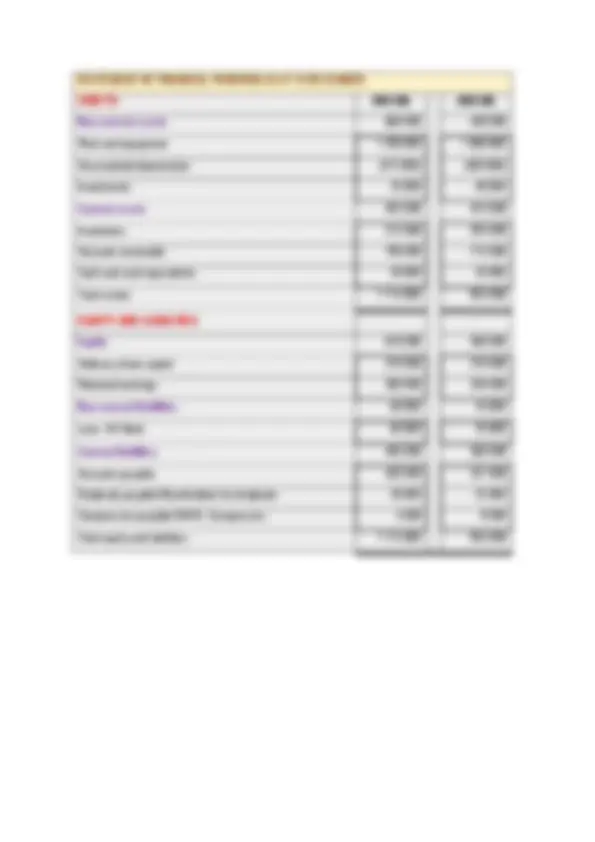

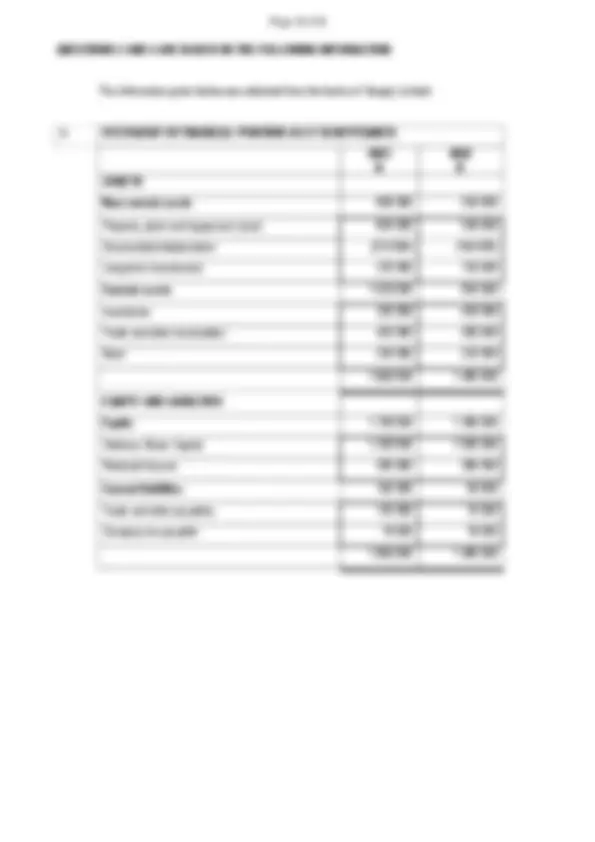

- Statement of Financial Position as at 28 February 2023. INFORMATION The trial balance, adjustments and additional information were extracted from the accounting records of Aquelle Traders on 28 February 2023 , the end of the financial year. AQUELLE TRADERS PRE-ADJUSTMENT TRIAL BALANCE ON 28 FEBRUARY 2023 Debit (R) Credit (R) Balance sheet accounts section Capital 870 700 Drawings 234 000 Land and buildings 608 700 Vehicles at cost 275 000 Equipment at cost 203 000 Accumulated depreciation on vehicles 94 000 Accumulated depreciation on equipment 70 000 Trading inventory 140 000 Debtors control 103 000 Provision for bad debts 5 000 Bank 4 000 Cash float 1 500 Petty cash 500 Creditors control 60 000 Loan: Tek Bank 96 000

30 November 2023.

- Interest on loan outstanding on 28 February 2023 amounted to R2 000. Note: Repayments totalling R24 000 (excluding interest) are expected to be made in the next financial year to reduce the loan balance.

- Depreciation must be brought into account each year as follows: 9.1 On vehicles at 20% per annum using the diminishing balance method. Hint: % (Cost price – Accumulated depreciation) 9.2 On equipment at 15% per annum on cost. Hint: % of Cost price

FINANCIAL REPORTING AND ANALYSIS: UNIT 2: SOLUTIONS

AQUELLE TRADERS

NOTES TO THE FINANCIAL STATEMENTS

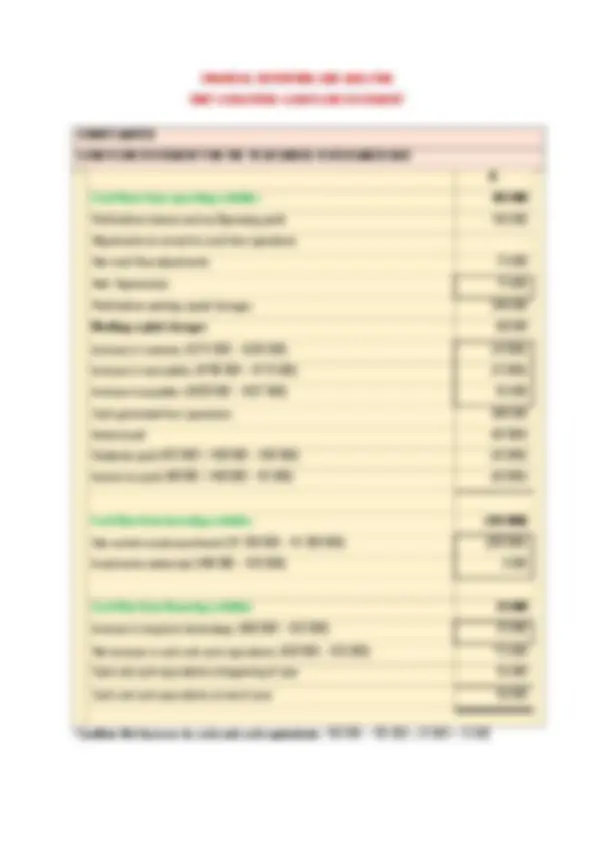

FIXED/TANGIBLE ASSETS Land and buildings Vehicles Equipment Total Carrying value at beginning of year 608 700 181 000 133 000 922 700 Cost 608 700 275 000 203 000 1 086 700 Accumulated depreciation 0 (94 000) (70 000) (164 000) Additions at cost 0 Disposals at carrying value 0 Depreciation 0 (36 200) (30 450) (66 650) Carrying value at end of year 608 700 144 800 102 550 856 050 Cost 608 700 275 000 203 000 1 086 700 Accumulated depreciation 0 (130 200) (100 450) (230 650) INVENTORIES Inventories consist of: Merchandise 136 000 Stationery 1 000 137 000 LONG-TERM BORROWINGS Loan from Tek Bank 96 000 Less: Instalment payable within one year, transferred to current liabilities (24 000) 72 000

QUESTION 2 A01/

REQUIRED

Prepare the Statement of Changes in Equity for the year ended 28 February 2023. INFORMATION The information given below was extracted from the accounting records of Wilson Traders, a partnership business with William and Sonny as partners. Extract from the trial balance of Wilson Traders on 28 February 2023 Debit (R) Credit (R) Capital: William 300 000 Capital: Sonny 200 000 Current a/c: William (01 March 2022 ) 20 000 Current a/c: Sonny (01 March 2022 ) 25 000 Drawings: William 170 000 Drawings: Sonny 180 000 The following must be considered: (a) On 28 February 2023 the Statement of Comprehensive Income reflected a net profit of R450 000. (b) The partners are entitled to interest at 12% p.a. on their capital balances. Note : William decreased his capital by R100 000 on 01 June 2022 whilst Sonny increased his capital by R100 000 on 01 September 2022. These capital changes have been recorded. (c) The partners are entitled to the following monthly salaries for each of the two six-month periods: 01 March 2022 to 31 August 2022 01 September 2022 to 28 February 2023 William R8 000 R8 500 Sonny R7 500 R8 000 (d) Sonny is entitled to a bonus equal to 5% of the net profit before any of the above appropriations have been considered. (e) The remaining profit/loss must be shared between William and Sonny in the ratio of their capital balances at the end of the financial year.

FINANCIAL REPORTING AND ANALYSIS

SOLUTIONS: UNIT 3

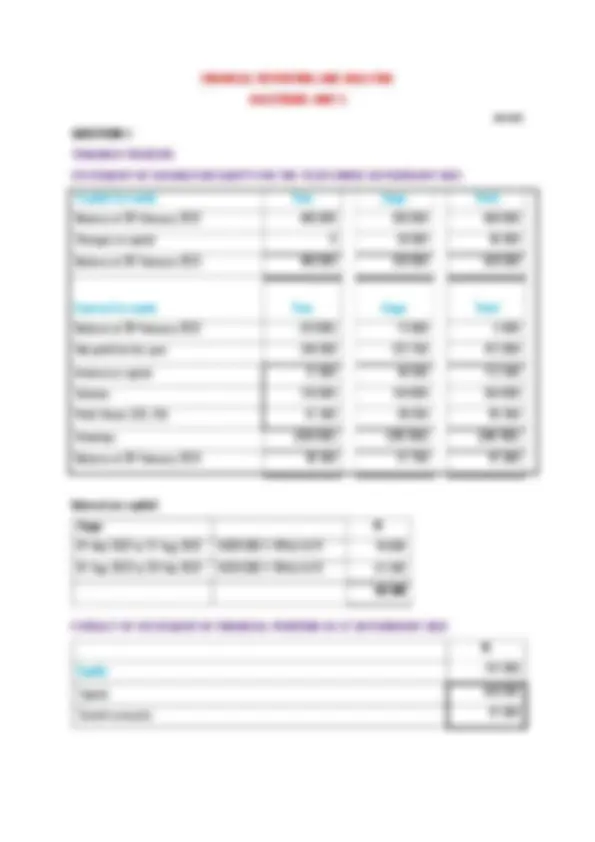

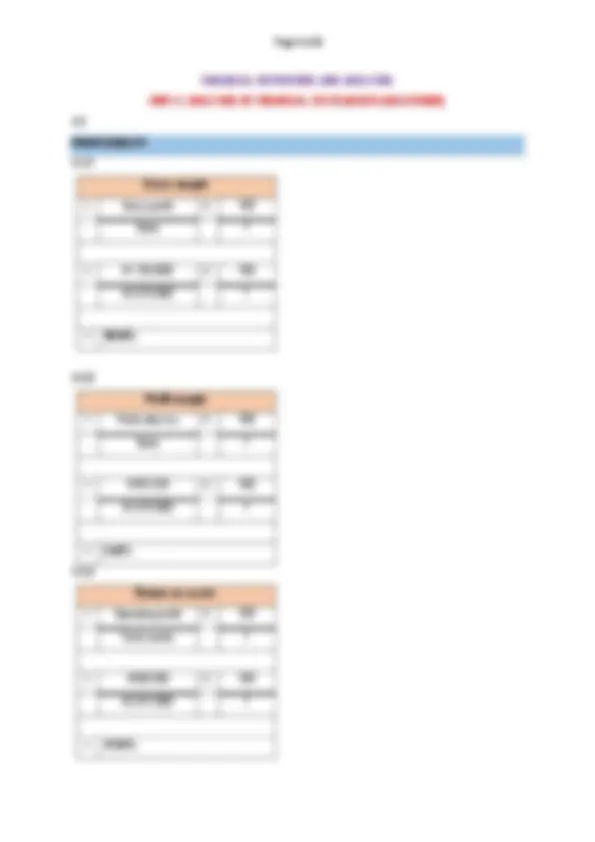

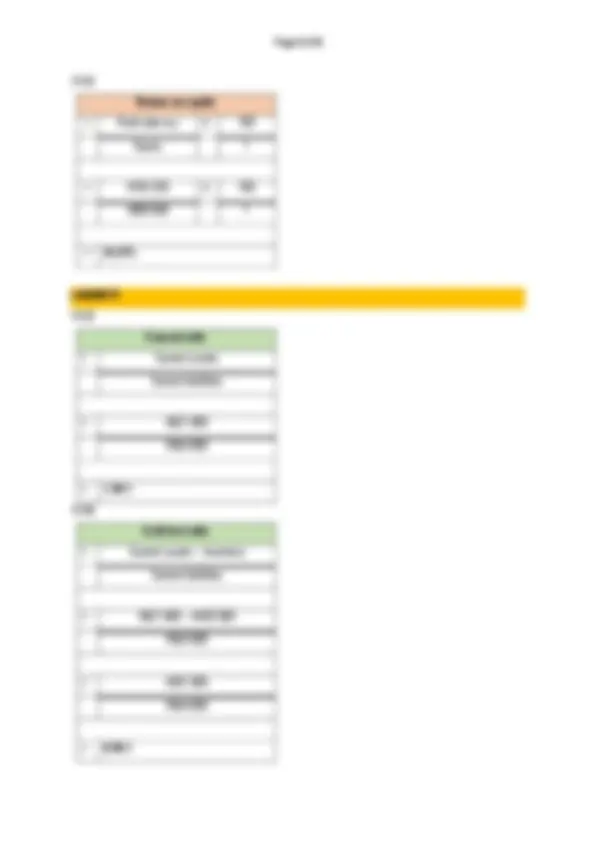

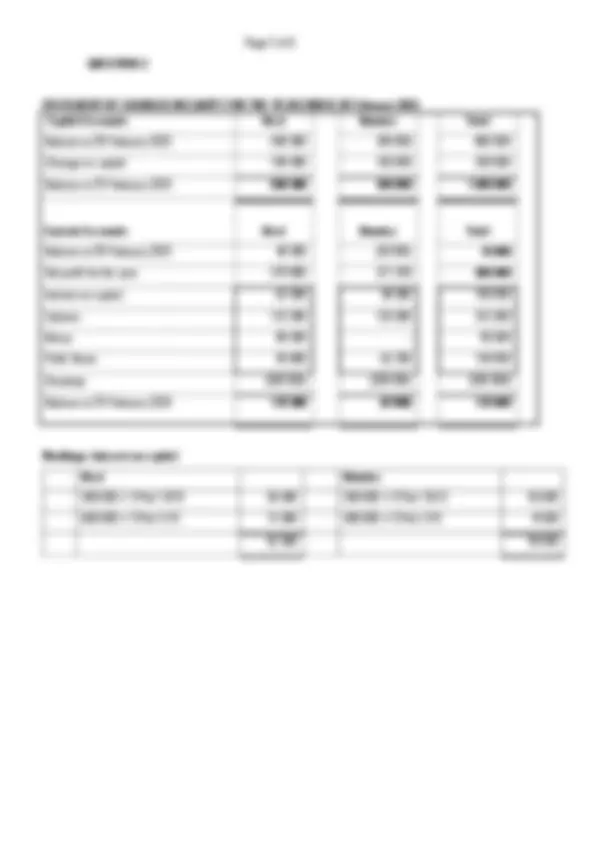

A0 2 /16RS QUESTION 1 TOMANGO TRADERS STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 28 FEBRUARY 2023 Capital Accounts Tom Ango Total Balance at 28 February 2022 400 000 200 000 600 000 Changes in capital 0 50 000 50 000 Balance at 28 February 2023 400 000 250 000 650 000 Current Accounts Tom Ango Total Balance at 28 February 2022 (10 000) 15 000 5 000 Net profit for the year 249 300 222 700 472 000 Interest on capital 72 000 40 500 112 500 Salaries 120 000 144 000 264 000 Profit Share (3/5; 2/5) 57 300 38 200 95 500 Drawings (200 000) (180 000) (380 000) Balance at 28 February 2023 39 300 57 700 97 000 Interest on capital: Ango R 01 Mar 2022 to 31 Aug 2022 R 200 000 X 1 8 % X 6 /12 18 000 01 Sep 2022 to 29 Feb 2023 R 250 000 X 1 8 % X 6 /12 22 5 00 40 500 EXTRACT OF STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 2023 R Equity 747 000 Capital 650 000 Current accounts 97 000

R

FINANCIAL REPORTING AND ANALYSIS

REQUIRED

Prepare the Statement of Comprehensive Income for the year ended 31 December 2023 , Statement INFORMATION The information given below was extracted from the accounting records of Woodford Ltd, on 31 December 2023 (the end of the financial year).

Dividends Statement of changes in equity : Show both the interim and final dividends in the Retained Earnings column (amounts in brackets) Statement of financial position : Show the final dividend which is unpaid (Trade and other payables) Ordinary share dividends R200 000 in the trial balance refers to the interim dividend which would have been paid during the year. Details regarding the final dividend will be found in the adjustments and additional information. Dividend calculation: Number of shares issued/sold X Dividend per share

FINANCIAL REPORTING AND ANALYSIS

UNIT 4 (FINANCIAL STATEMENTS OF A COMPANY): SOLUTIONS

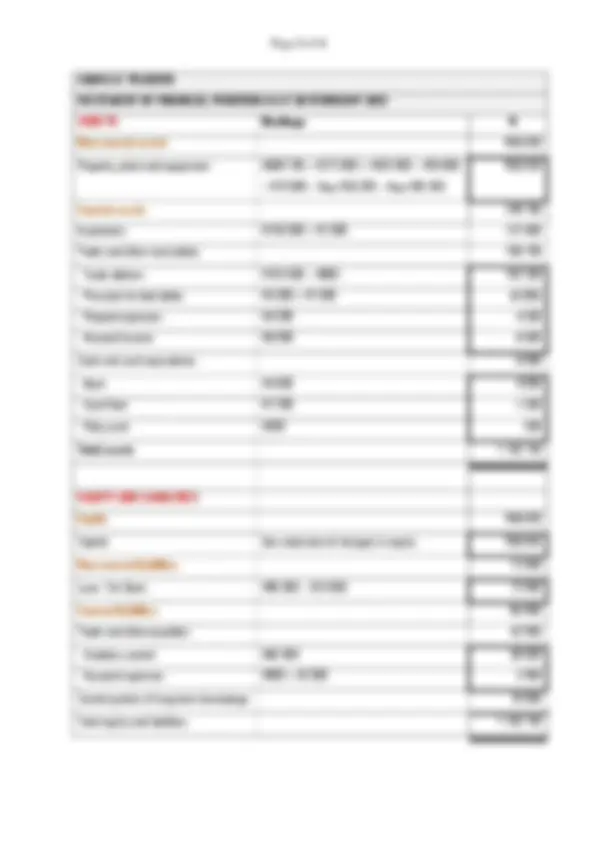

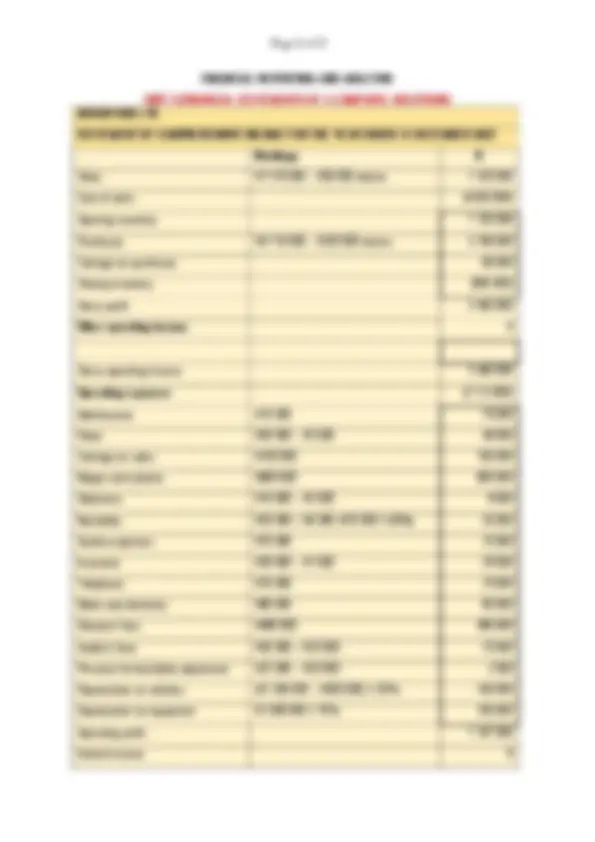

- STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 2 8 FEBRUARY AQUELLE TRADERS

- Sales R 1 277 000 – R15 Workings R

- Gross profit Cost of sales R 700 000 (700 000)

- Other operating income

- Rent income R 66 000 + R 6 000 (R66 000 ÷ 11)

- Discount received R2

- Gross operating income

- Wages R123 Operating expenses (313 850)

- Bank charges R4

- Packing materials R37

- Advertising R18

- Rates R7

- Bad debts R2 000 + R800 (R2 000 X 40%)

- Discount allowed

- Stationery R20 000 – R1

- Water and electricity R9

- Insurance R16 000 – R4 500 (R6 000 ÷ 12 X 9)

- Telephone R9 000 + R900

- Donation

- Trading inventory deficit R140 000 – Donation R1 000 – R136

- Provision for bad debts adjustment R6 000 – R5000

- Depreciation on vehicles (R275 000 – R94 000) X 20%

- Depreciation on equipment R203 000 X 15%

- Operating profit

- Interest income

- Net profit for the year Interest expense R10 000 + R2 000 (12 000)

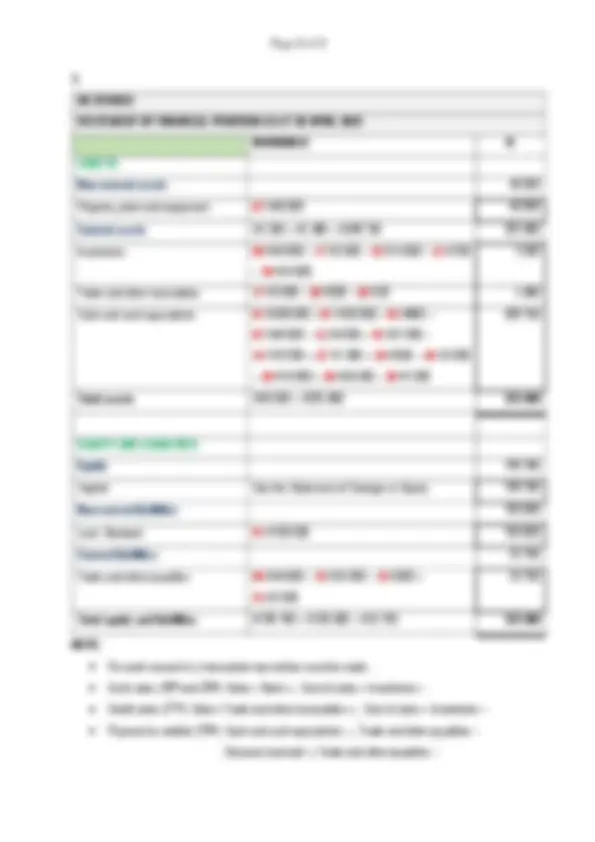

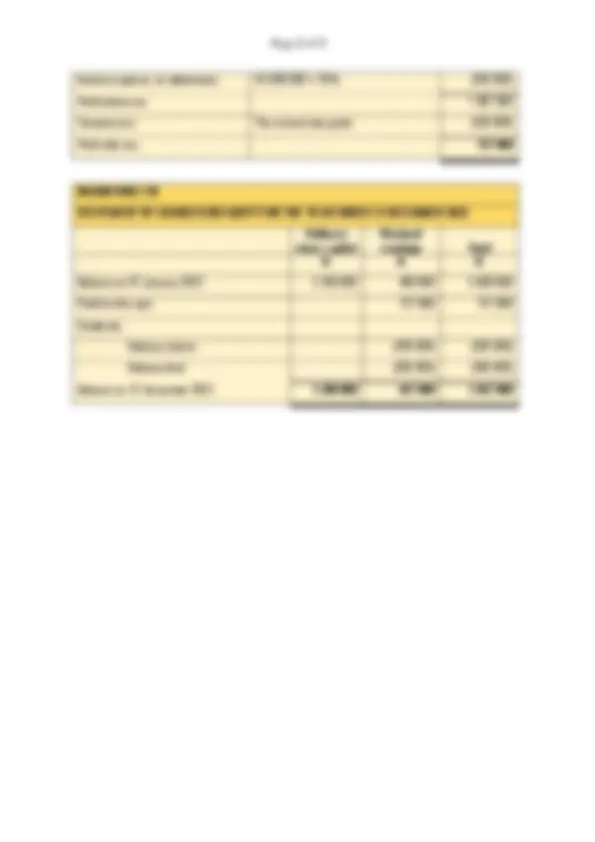

- STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY

- Non-current assets ASSETS Workings R

- Property, plant and equipment R 608 700 + R 275 000 + R 203 000 – R

- – R 70 000 – Dep R 36 200 – Dep R

- Current assets

- Inventories R 136 000 + R

- Trade and other receivables

- Trade debtors R 103 000 – R

- Prepaid expenses R Provision for bad debts R 5 000 + R 1 000 (6 000)

- Accrued income R6

- Cash and cash equivalents

- Bank R4

- Cash float R1

- Petty cash R

- Total assets

- Equity EQUITY AND LIABILITIES

- Capital See statement of changes in equity

- Non-current liabilities

- Loan: Tek Bank R 96 000 – R

- Current liabilities

- Trade and other payables

- Creditors control R60

- Accrued expenses R900 + R

- Current portion of long-term borrowings

- Total equity and liabilities

- EXTRACT OF STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY

- Equity^595

- Capital

- Current accounts

- FINACCBRESUB02/ UNIT 4 (FINANCIAL STATEMENTS OF A COMPANY): ACTIVITIES AND NOTES

- 31 December of Changes in Equity for the year ended 31 December 2023 and Statement of Financial Position as at

- PRE-ADJUSTMENT TRIAL BALANCE AS AT 31 DECEMBER WOODFORD LTD

- Ordinary share capital Balance Sheet Accounts Section Debit (R) Credit (R)

- Retained earnings

- Land and buildings

- Vehicles (cost)

- Equipment (cost)

- Accumulated depreciation on vehicles

- Accumulated depreciation on equipment

- Debentures (10% p.a.)

- Debtors control

- Provision for bad debts

- Bank

- Creditors control

- South African Revenue Services (Company tax)

- Sales Nominal accounts section

- Opening inventory

- Purchases

- Sales returns

- Purchases returns

- Carriage on purchases

- Maintenance

- Rates

- Carriage on sales

- Wages and salaries

- Stationery

- Bad debts

- Sundry expenses

- Insurance

- Telephone

- Water and electricity

- Directors’ fees

- Auditor’s fees

- Ordinary share dividends

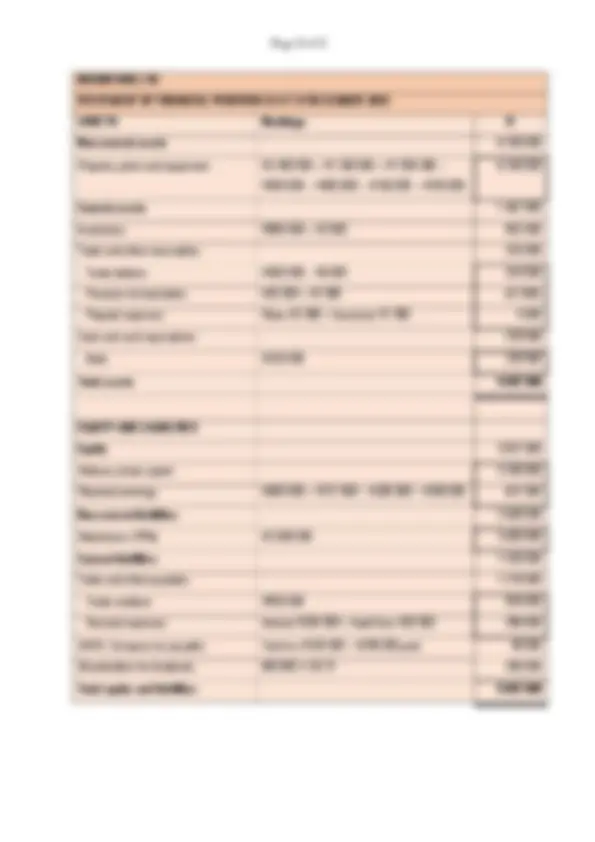

- STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER WOODFORD LTD

- Sales R7 570 000 – R 50 000 returns Workings R

- Opening inventory Cost of sales (4 060 000)

- Purchases R4 110 000 – R 330 000 returns

- Carriage on purchases

- Gross profit Closing inventory (90 0 000)

- Other operating income

- Gross operating income

- Maintenance R Operating expenses (2 113 0 00)

- Rates R 50 000 – R

- Carriage on sales R

- Wages and salaries R

- Stationery R 10 000 – R

- Bad debts R 20 000 + R 6 000 (R 10 000 X 60%)

- Sundry expenses R

- Insurance R 30 000 – R1

- Telephone R

- Water and electricity R

- Directors’ fees R

- Auditor’s fees R 50 000 + R

- Provision for bad debts adjustment R22 000 – R

- Depreciation on vehicles (R 1 300 000 – R 500 000) X 20%

- Depreciation on equipment R 1 000 000 X 10%

- Operating profit

- Interest income