1

Financial

Statement

Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

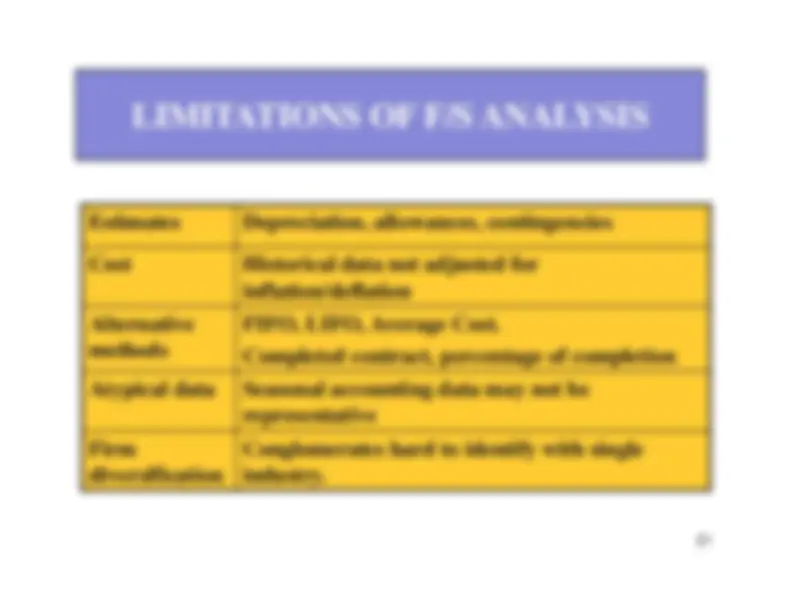

An overview of financial statement analysis, including the statement of cash flows, balance sheet, income statement, and statement of changes in owner's equity. It covers horizontal, vertical, and ratio analysis techniques, offering formulas and examples for profitability, turnover, and debt-related ratios. The document also discusses the limitations of financial statement analysis, such as estimates, historical cost, alternative methods, atypical data, and firm diversification. It is a useful resource for understanding how to interpret and analyze financial statements to assess a company's performance and financial health. Useful for university students and lifelong learners.

Typology: Cheat Sheet

1 / 21

This page cannot be seen from the preview

Don't miss anything!

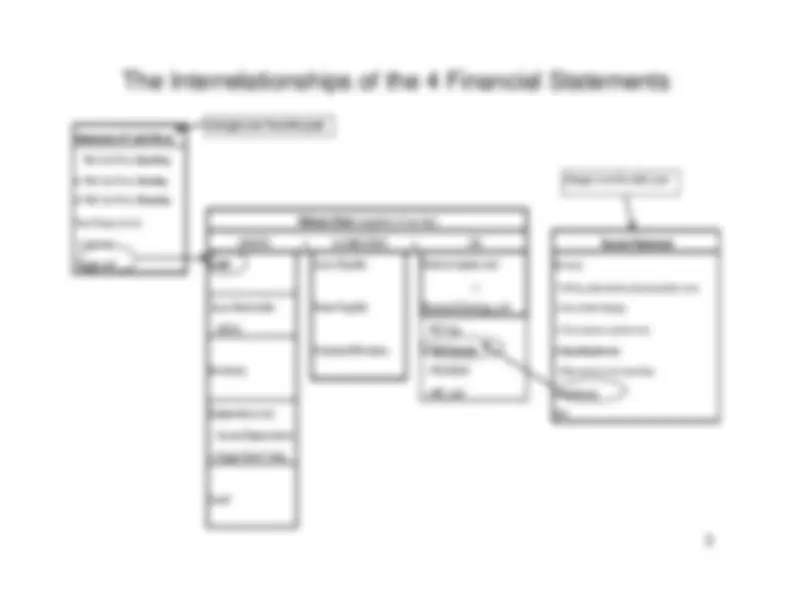

Statement of Cash Flows For the year ended December 31, 20x

Net cash flows from operating activitiesNet cash used by investing activitiesNet cash provided by financing activitiesIncrease in cash balanceBeginning cash balance (12/31/x1)

Ending cash balance (12/31/x2)

As of December 31, 20x

As of December 31, 20x

Income Statement

Cash

For the year ended December 31, 20x

Cash

Other Current Assets

Other Current Assets

Long-term Investments

Revenues

Long-term Investments

Long-term Assets

Expenses

Long-term Assets

Intangible Assets

Net Income

Intangible Assets

Total Assets

Total Assets

Statement of Changes in Owner's Equity

Current Liabilities

For the year ended December 31, 20x

Current Liabilities

Long-term Liabilities

Long-term Liabilities

Joe Owner, capital, 1/1/x

Joe Owner, Capital

Plus: Investments by owner

Joe Owner, Capital

Plus: Net Income

Total Liabilities and Equity

Less: Withdrawals by owner

Total Liabilities and Equity

Joe Owner, capital, 12/31/x

Liabilities and Owner's Equity

Assets

Liabilities and Owner's Equity

Assets

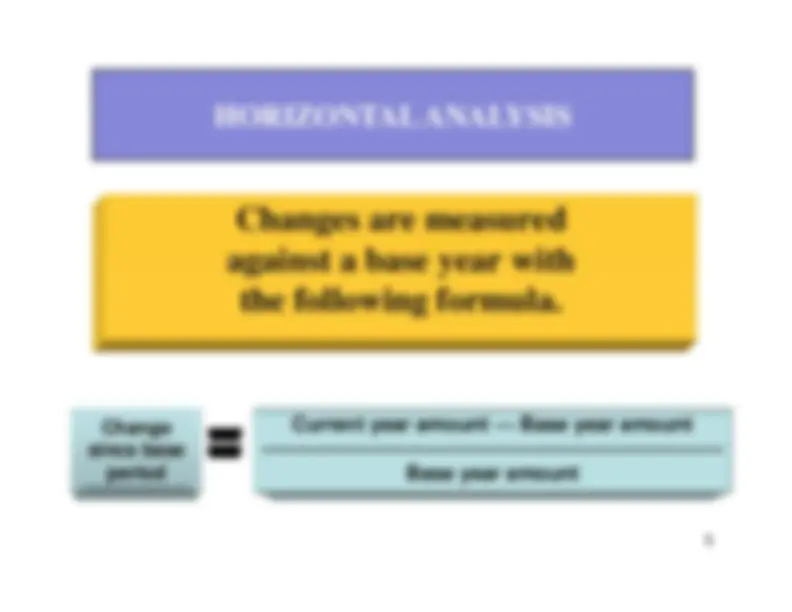

ANALYSIS TOOLS

HORIZONTAL (TREND) ANALYSISevaluates a series of financial statement

data over a period of time.^ VERTICAL ANALYSIS

expresses each item in a financial statement as a percent of a base amount

RATIO ANALYSIS

expresses the relationship among

selected items of financial statement data.

Changes are measured against a base year with

the following formula.

Current year amount — Base year amount

———————————————————————

Base year amount

Change since base

period

HORIZONTAL ANALYSIS

HORIZONTAL ANALYSISOF INCOME STATEMENT

HORIZONTAL ANALYSIS

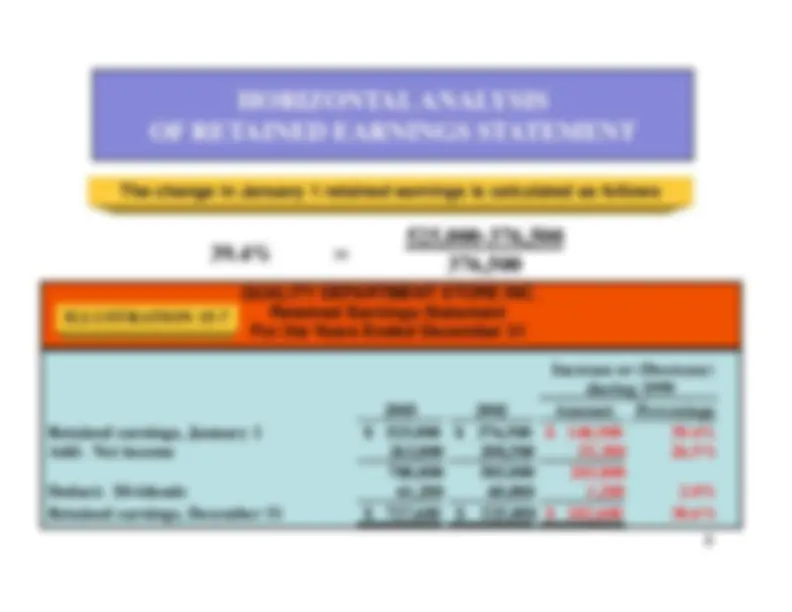

OF RETAINED EARNINGS STATEMENT

QUALITY DEPARTMENT STORE INC.

Retained Earnings Statement For the Years Ended December 31

Increase or (Decrease)

during 1999

2003

2002

Amount

Percentage

Retained earnings, January 1

$

525,

$^

376,

$

148,

39.4%

Add: Net income

263,

208,

55,

26.5%

788,

585,

203,

Deduct: Dividends

61,

60,

1,

2.0%

Retained earnings, December 31

$

727,

$^

525,000 $

202,

38.6%

ILLUSTRATION 15-

39.4%

525,000-376,

376,

=

The change in January 1 retained earnings is calculated as follows

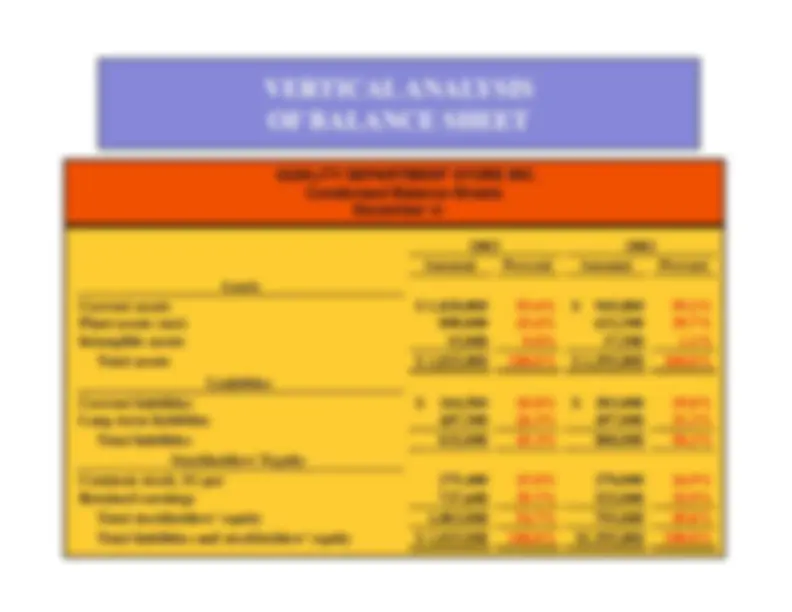

QUALITY DEPARTMENT STORE INC

.

Condensed Balance Sheets

December

31

2003

2002

Amount

Percent

Amount

Percent

Assets

Current assets

$ 1,020,

55.6%

$^

945,

59.2%

Plant assets (net)

800,

43.6%

632,

39.7%

Intangible assets

15,

0.8%

17,

1.1%

Total assets

$ 1,835,

100.0%

$ 1,595,

100.0%

Liabilities

Current liabilities

$^

344,

18.8%

$^

303,

19.0%

Long-term liabilities

487,

26.5%

497,

31.2%

Total liabilities

832,

45.3%

800,

50.2%

Stockholders’ Equity

Common stock, $1 par

275,

15.0%

270,

16.9%

Retained earnings

727,

39.7%

525,

32.9%

Total stockholders’ equity

1,003,

54.7%

795,

49.8%

Total liabilities and stockholders’ equity

$ 1,835,

100.0%

$1,595,

100.0%

VERTICAL ANALYSISOF BALANCE SHEET

QUALITY DEPARTMENT STORE INC

.

Condensed Income Statements For the

Years

Ended December 31

2003

2002

Amount

Percent

Amount

Percent

Sales

$ 2,195,

104.7%

$ 1,960,

106.7%

Sales returns and allowances

98,

4.7%

123,

6.7%

Net sales

2,097,

100.0%

1,837,

100.0%

Cost of goods sold

1,281,

61.1%

1,140,

62.1%

Gross profit

816,

38.9%

697,

37.9%

Selling expenses

253,

12.0%

211,

11.5%

Administrative expenses

104,

5.0%

108,

5.9%

Total operating expenses

357,

17.0%

320,

17.4%

Income from operations

459,

21.9%

377,

20.5%

Other revenues and gains

Interest and dividends

9,

0.4%

11,

0.6%

Other expenses and losses

Interest expense

36,

1.7%

40,

2.2%

Income before income taxes

432,

20.6%

347,

18.9%

Income tax expense

168,

8.0%

139,

7.5%

Net income

$^

263,

12.6%

$^

208,

11.4%

VERTICAL ANALYSISOF BALANCE SHEET

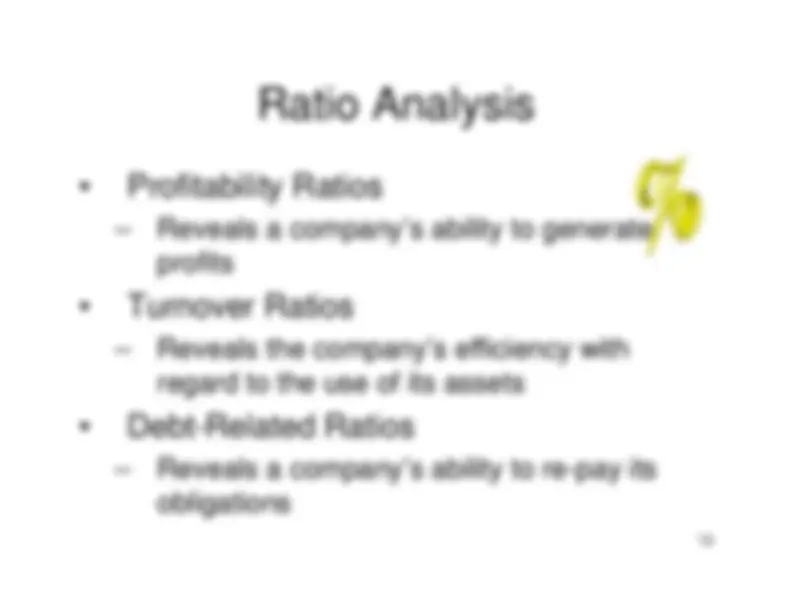

Ratio Analysis

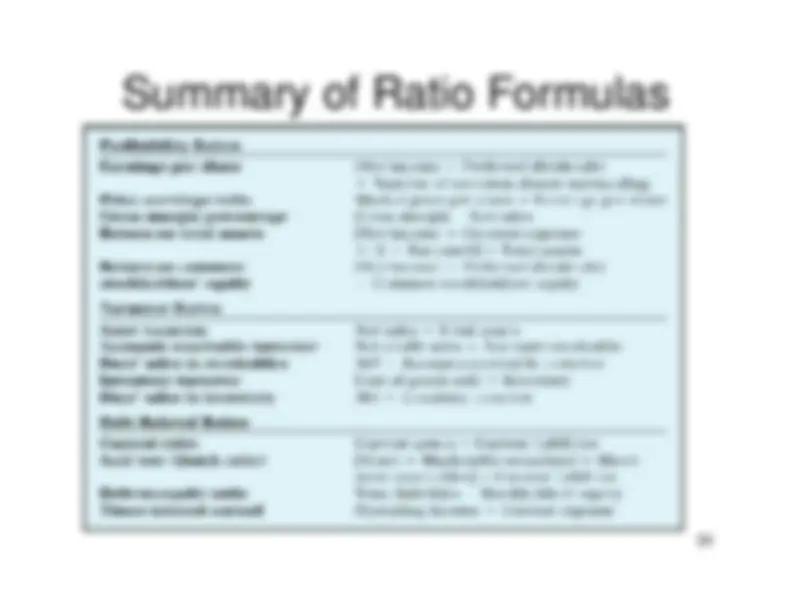

Profitability Ratios

Reveals a company’s ability to generateprofits

Turnover Ratios

Reveals the company’s efficiency withregard to the use of its assets

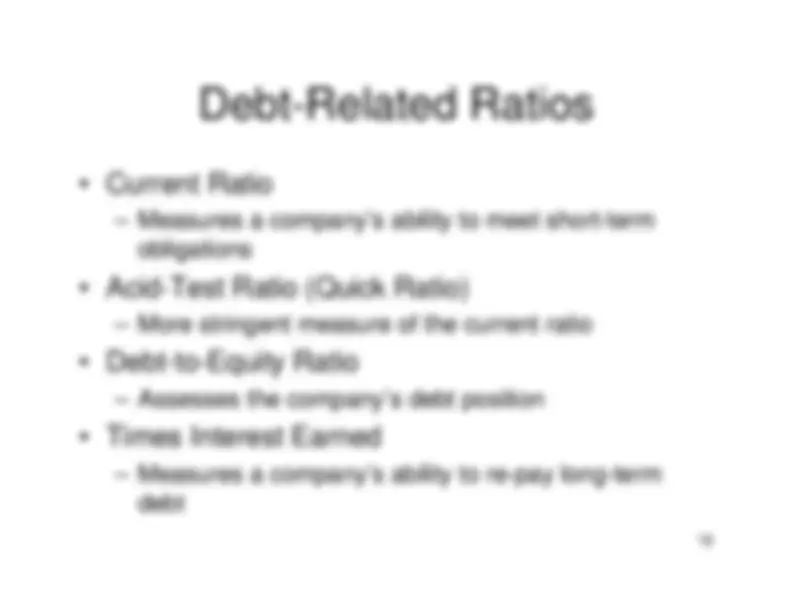

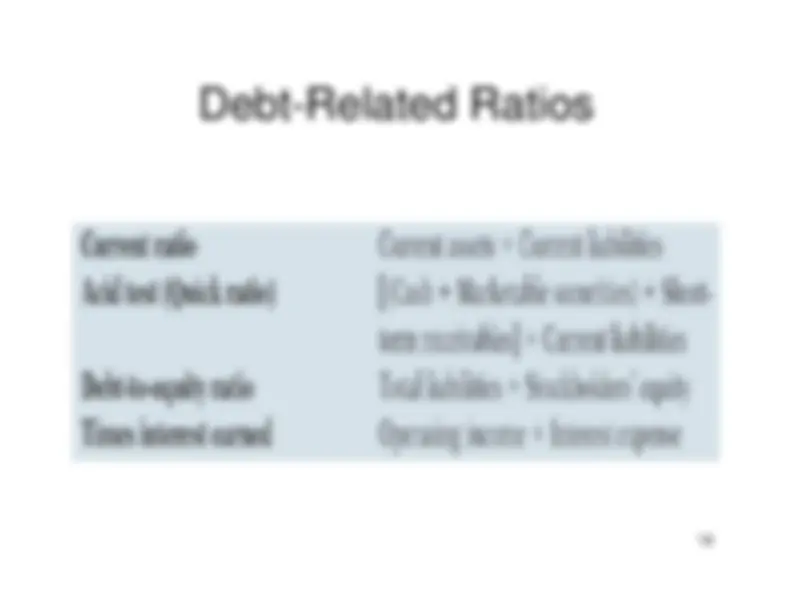

Debt-Related Ratios

Reveals a company’s ability to re-pay itsobligations

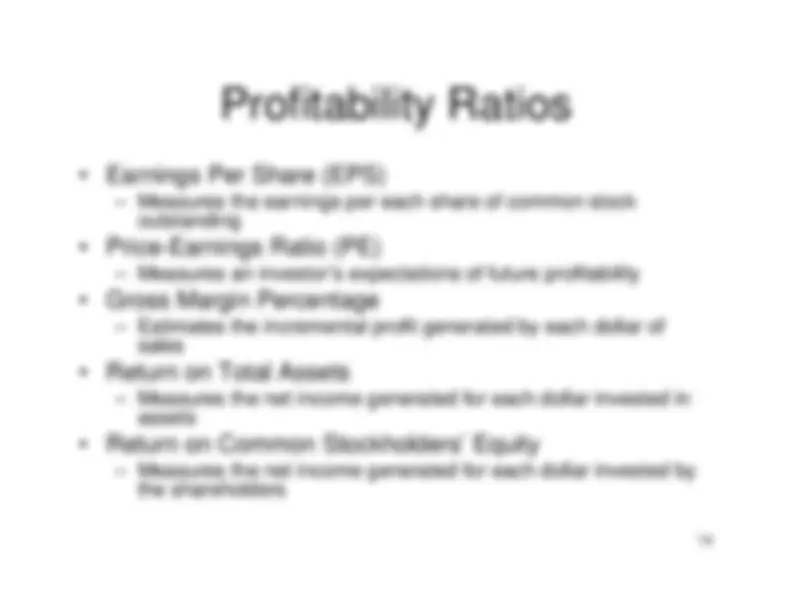

Profitability Ratios

outstanding

sales

assets

the shareholders

Turnover Ratios

collected

credit sales

inventory

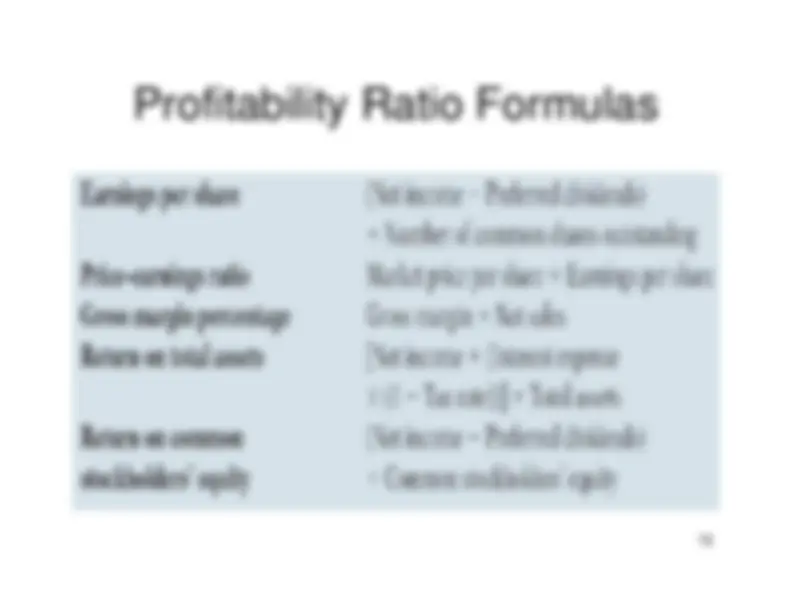

Turnover Ratio Formulas

Debt-Related Ratios

Summary of Ratio Formulas