FINANCIAL

STATEMENTS:

Tools for decision making

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

study your financial statement with this powerpoint. I hope it helps

Typology: Study notes

1 / 19

This page cannot be seen from the preview

Don't miss anything!

(^) Appreciate the importance of financial analysis as analytical process. (^) Discuss the three basic decision areas dealt with by managers and the items involved in these decisions. (^) Explain the steps in analyzing financial statements. (^) Differentiate horizontal analysis from vertical analysis and appreciate their importance in business decision-making. (^) Demonstrate how to prepare a common-size balance and income statement and analyze the changes therein. (^) Explain the different profitability ratios and their importance in decision-making and solve problems using them. (^) Discuss the limitations of financial statements and financial statement analysis.

BASIC DECISION AREAS OPERATION FINANCE INVESTMENT

(^) Refers to deciding what assets to acquire, be they current assets as marketable securities or non-current assets as property, plant or equipment and long-term investments in stocks and bonds. (^) It includes the decisions relative to projects to undertake or business to enter to. (^) Current available resources and new founding obtained can be utilize to fund: a) Working capital – working capital budget for operating expenses and payment for current liabilities. b) Property plant and equipment- capital budgeting- capital expenditure intended for long-term assets and projects. c) Major spending programs- e.g. research and development, product or service development, promotional and advertising programs or long-term investment alternatives for excess funds so that cash can be converted into an earning asset.

(^) Refers to decision that involves funding investments and operations over the long run. (^) Includes decisions that relate to the companies capital structure, debt-equity mix, funding sources, dividend policies, cost of capital, among others.

STEPS IN ANALYZING THE FINANCIAL STATEMENTS (^) Understanding the information provided in the financial statements- any reader of the financial statements, especially the manager, who is to make decisions to benefit the enterprise, needs to have a basic knowledge of finance in its contextual meaning to avoid confusion and misleading or wrong decisions, which are sometimes, fatal to the business. (^) Drawing logical conclusion based on the data presented- i.e., financial statements for two or more periods are necessary before one can make a decision on how the business is performing or how the condition of the company is changing. Comparative analysis of sales or revenue and expenses can help the manager decide on where the company needs improvement-sales, manufacturing or expenses. (^) Making the appropriate decision on the course of action to take- After drawing logical conclusion, the manager or user of the financial statements is now able to determine the course of action to take to correct what needs correction and the steps necessary to redirect company efforts towards the goals that the company has set.

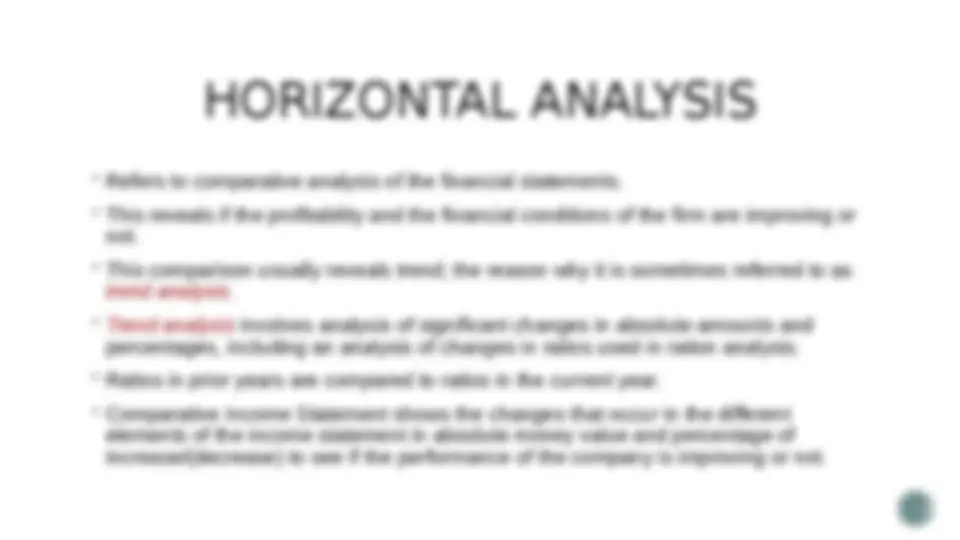

(^) Refers to the type of analysis where one number is compared to another to identify significant relationships. TWO TYPES OF VERTICAL ANALYSIS:

(^) Return on Owners’ Investment (ROI)- Sometimes referred to as ROE. It relates income or profit after income tax to the total stockholders’ equity. The average is computed by adding the beginning and the ending balances and dividing it by two. (^) Profit margin- also known as return on sales, (ROS) is the ratio of income to net sales. (^) Return on Assets- Is a measure of asset utilization.

(^) Debt ratio- relates total liabilities to total assets. (^) Stockholders’ ratio- relates total stockholders’ equity to total assets. (^) Debt-equity ratio- relates the total liabilities to total stockholders’ equity. (^) Interest coverage ratio- indicates the company’s ability to pay its interest on its obligation.