FIN 254

Chapter 3

Financial Statement & Ratio

Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

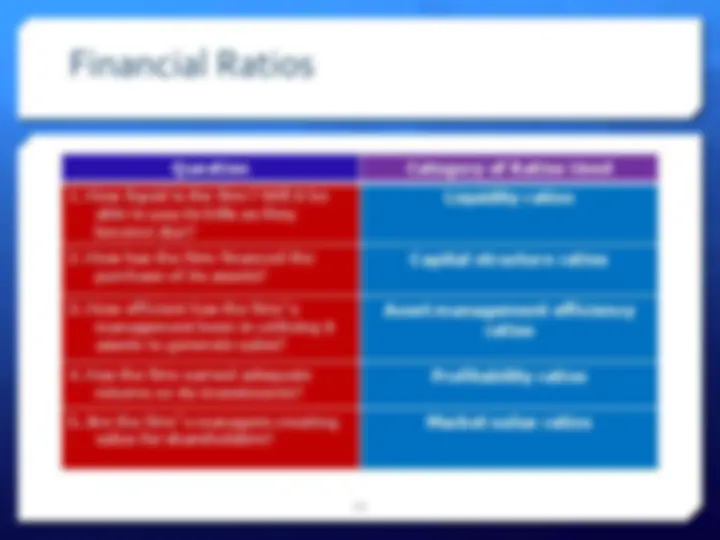

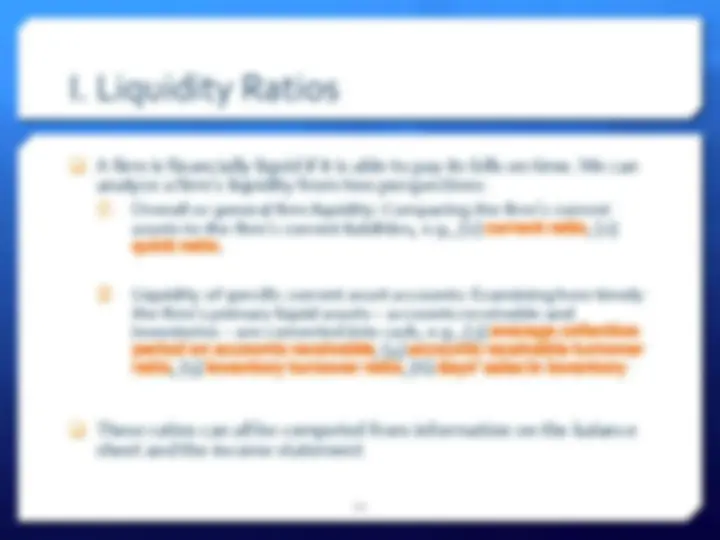

A comprehensive guide on calculating and using financial ratios to evaluate a company's performance. It covers various types of ratios such as liquidity ratios, capital structure ratios, asset management efficiency ratios, profitability ratios, and market value ratios. The document also discusses the limitations of financial ratio analysis and offers examples for better understanding.

Typology: Slides

1 / 76

This page cannot be seen from the preview

Don't miss anything!

An internal financial analysis might be done: To evaluate the performance of employees and determine their pay raises and bonuses. To compare the financial performance of the firm’s different divisions. To prepare financial projections, such as those associated with the launch of a new product. To evaluate the firm’s financial performance in light of its competitors and determine how the firm might improve its operations. A variety of firms and individuals that have an economic interest might also undertake an external financial analysis: Banks and other lenders deciding whether to loan money to the firm. Suppliers who are considering whether to grant credit to the firm. Credit-rating agencies trying to determine the firm’s creditworthiness. Professional analysts who work for investment companies considering investing in the firm or advising others about investing. Individual investors deciding whether to invest in the firm. 4

A report issued annually by a corporation to its stockholders. It contains basic financial statements as well as management’s analysis of the firm’s past operations and future prospects.

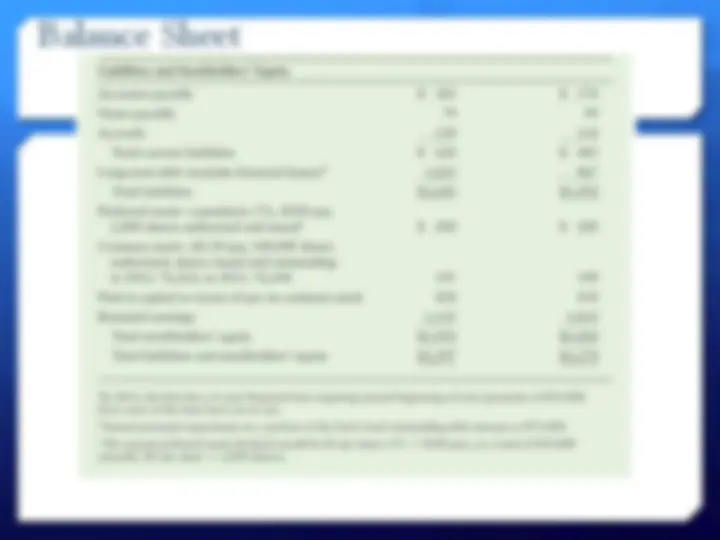

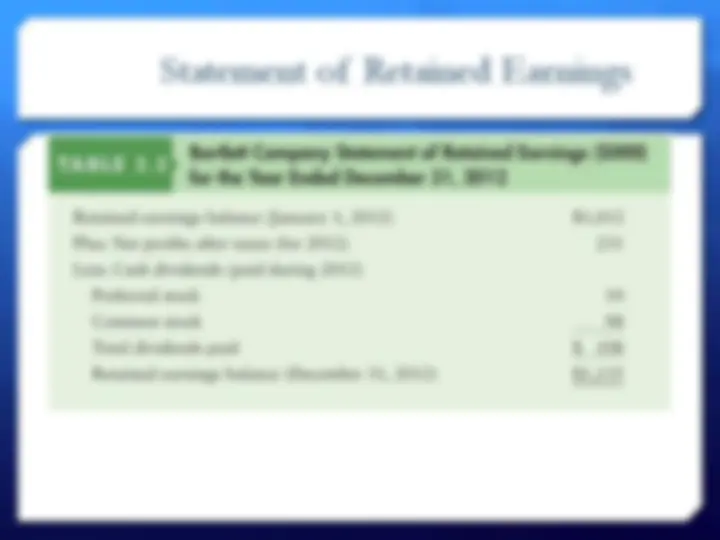

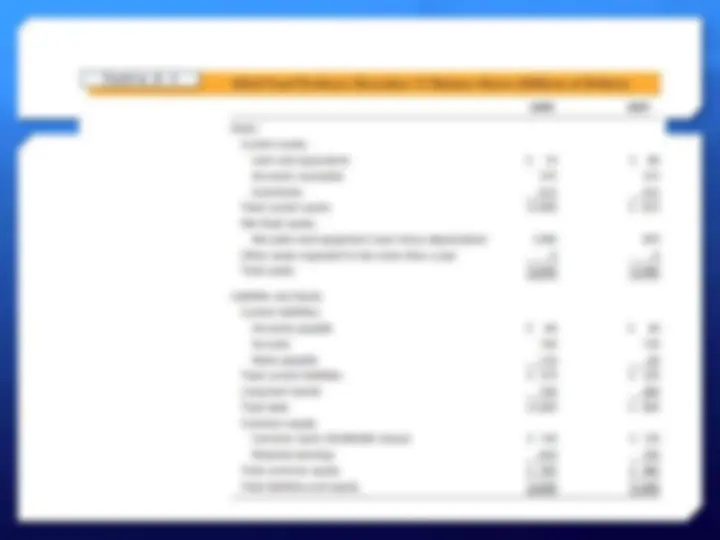

Balance Sheet Debt or Liabilities: ◦ Long-term debt – Interest bearing. E.g.: bonds, loans ◦ Current debt – Non-interest bearing. E.g.: payables, accruals Preferred Stock - Part of equity that is a hybrid of debt and common stock Common Stock – Portions of ownership of a company In the event of bankruptcy priority of payback are as follows: debt- preferred stocks-common stocks Paid in Capital Retained Earnings

Income at different stages Depreciation : The charge to reflect the cost of assets used up in the production process. Depreciation is not a cash outflow. Amortization : A noncash charge similar to depreciation except that it is used to write off the costs of intangible assets. Since these are non-cash so Earnings Before Interest Tax Depreciation and Amortization (EBITDA) is also an important indicator of firm performance

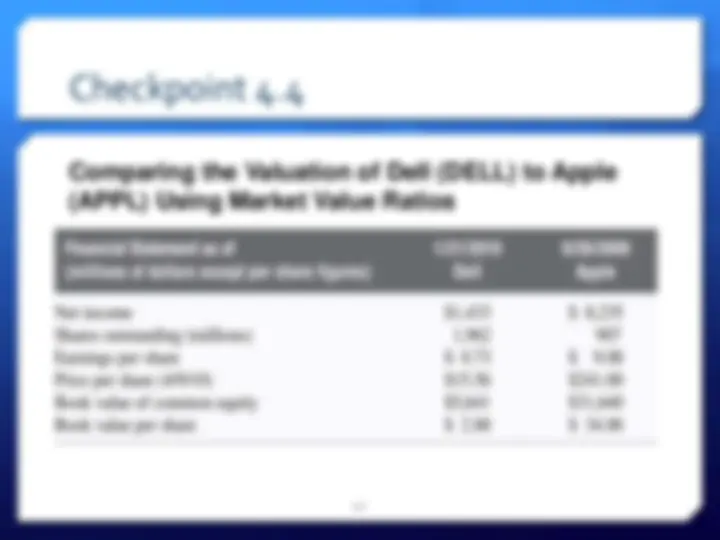

Market Value VS Book Value Book Values are the values of assets calculated using methods of GAAP and put in the balance sheet. Market Values are the current price of an asset in the market if it were to put up for sale.

Operating Activities : Deals with items that occur as part of normal ongoing operation. Investing Activities : Activities involving long-term assets. Financing Activities : Activities involving long-term debt or equity financing.

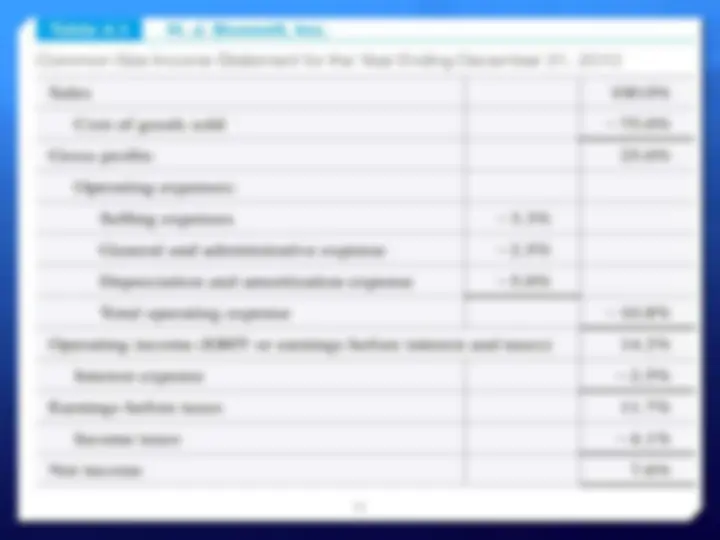

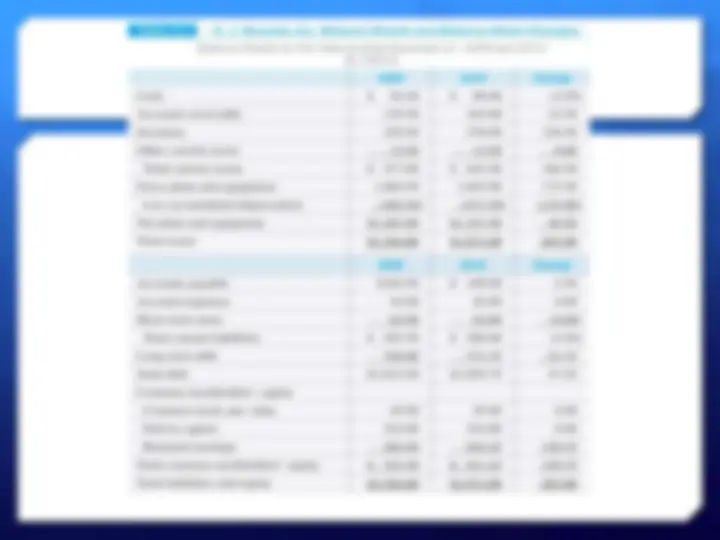

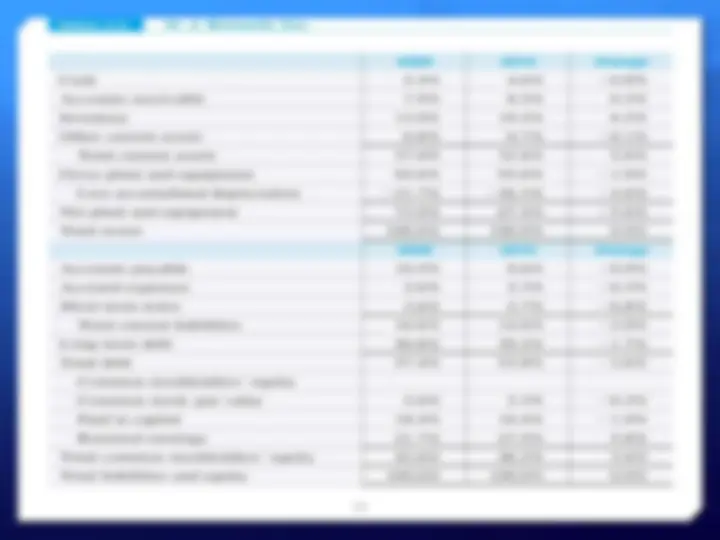

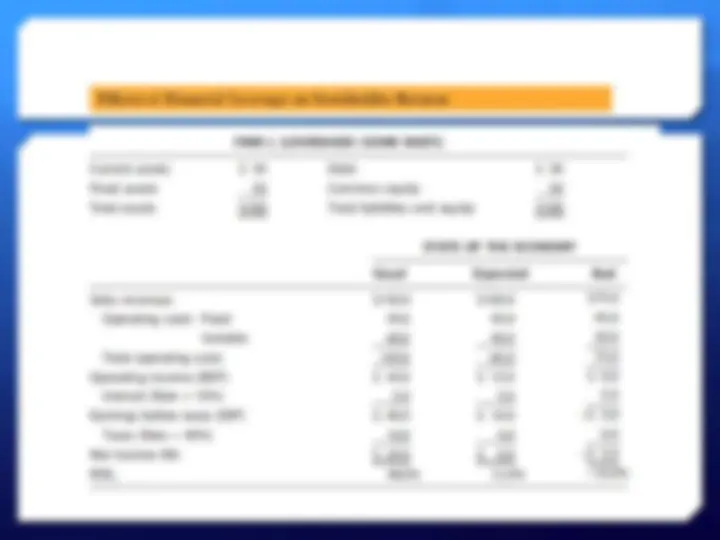

Common Size Statements

For a common size income statement, divide each entry in the income statement by the company’s sales. For a common size balance sheet, divide each entry in the balance sheet by the firm’s total assets. 20