Types of Inventory

•Finished goods inventory

–Items ready and available for sale

–Permits prompt filling of orders

–Large production runs create economies of

scale

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Students of Communication, study E-Commerce as an auxiliary subject. these are the key points discussed in these Lecture Slides of E-Commerce : Finished Goods, Inventory, Prompt Filling, Large Production, Economies, Ordering Co, Carrying Costs, Stockout Costs, Rescheduling Production, Lost Sales

Typology: Slides

1 / 11

This page cannot be seen from the preview

Don't miss anything!

-^ Finished goods inventory^ –^ Items ready and available for sale^ –^ Permits prompt filling of orders^ –^ Large production runs create economies ofscale

:^ Cost of placing and receiving an order of goods • Carrying costs

:^ Cost of holding inventory

-^ Expressed as cost per unit per period –^ A percent of the inventory value per period • Stockout costs

: Incurred when a firm is unable to fill an order, resulting in:^ –^ Lost sales^ –^ Rescheduling production^ –^ Expediting special

orders

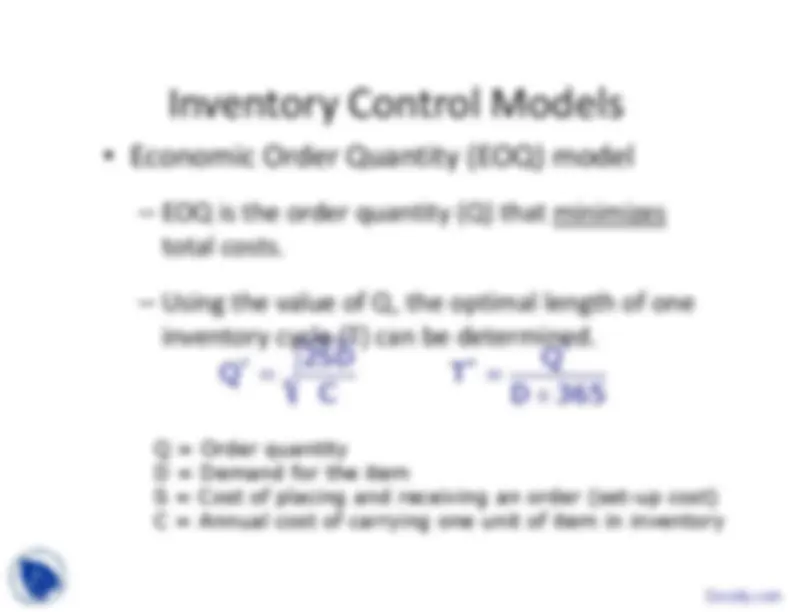

2SD Q C^

*Q * = (^) T ÷D 365

Q = Order quantityD = Demand for the itemS = Cost of placing and receiving an order (set-up cost)C = Annual cost of carrying one unit of item in inventory

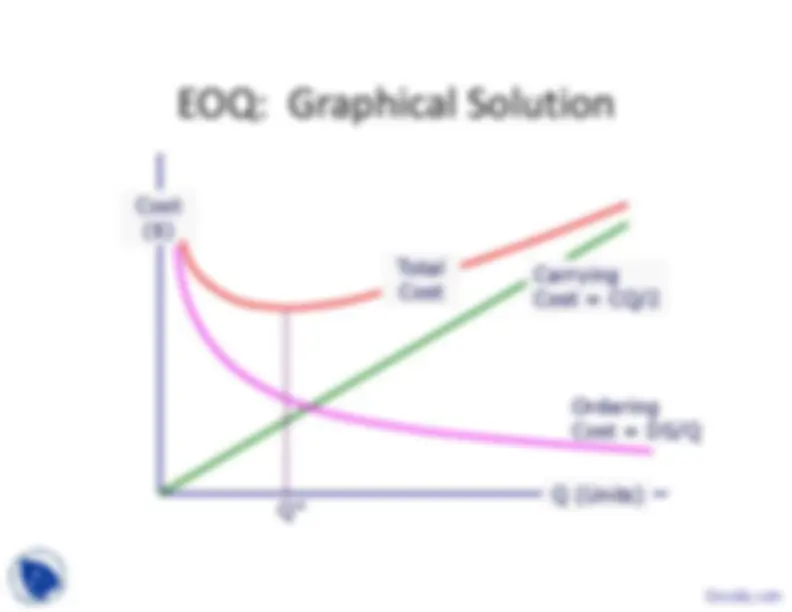

2SDQ* = C 2 $31.25= =

3, 600 $ 150 Conclusion: To minimize its inventory costs, Searsshould order 150 mattresses at a time.

Q (Units)

Cost($)

TotalCost Q*

CarryingCost = CQ/2OrderingCost = DS/Q

-^ Current assets represent a major investmentfor many firms but they are often don’treceive the management attention theydeserve. •^ The job of the financial manager is to find theappropriate balance between minimizing riskand maximizing return. •^ No one method is “right” for all firms. Themethod chosen will depend on firm size,complexity and the options currently^ available to it.