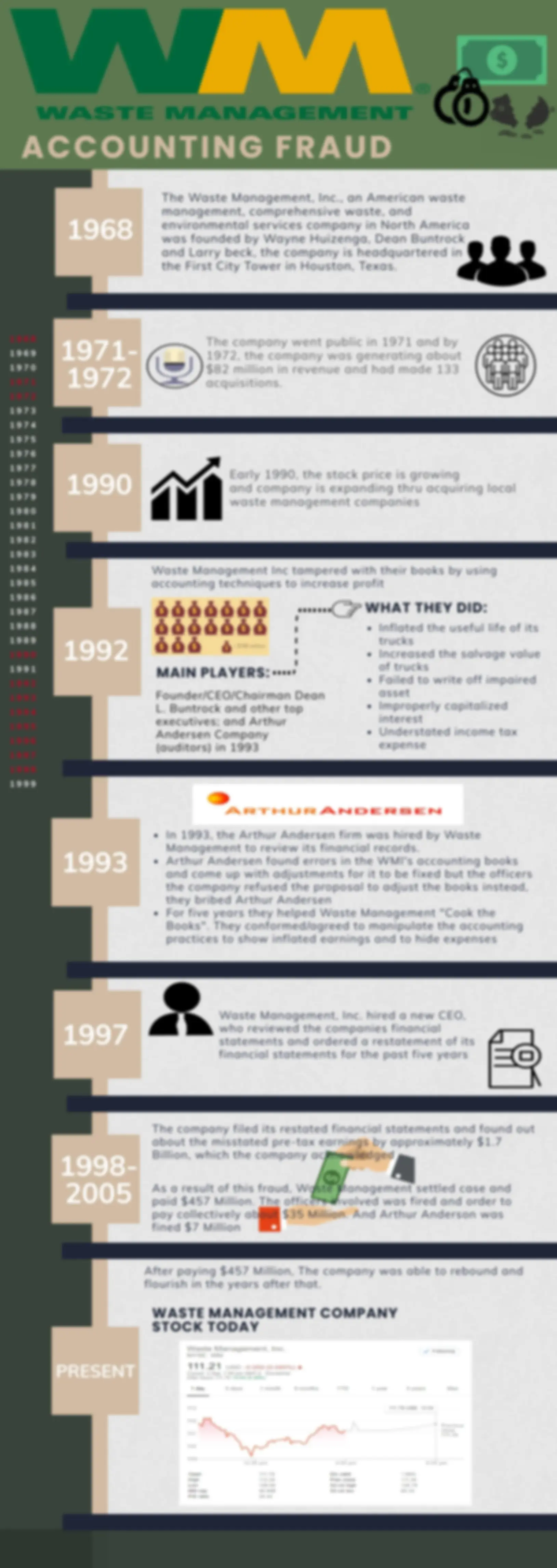

Download Fraud Cases in Accounting and more Assignments Accounting in PDF only on Docsity!

The SEC started an investigation to Enron and the partnerships headed by Andrew Fastow

Enron admits that there was an actual loss of $586M dating from 1997 after they have revised their financial statements

January 9

Andersen was fired by Enron because of destroying the company's documents

Enron scandal became a symbol of corruption for the whole Western economic system as 4, employees lost their jobs and their pension fund was abolished. During this period, citizen's trust in the economic system was destroyed and financial market suffered to the worst stock value loss in peaceful times

THE ENRON SCANDAL

Skilling suddenly resigns citing personal

reasons. Lay returns as CEO but analysts became weary of the

company's state and lower their ratings

on Enron stock. Enron's share drops to $39.95 per share, a 52-week low.

T H E F A L L O F A W A L L S T R E E T D A R L I N G

Enron was founded by Kenneth Lay in the merger of two natural gas transmission companies, Houston Natural Gas Corporation and InterNorth, Inc.

Jeff Skilling was hired by Lay and led the company's effort to focus on trading commodities in the deregulated markets

Andrew Fastow became the chief financial officer; He manage the creation of the company's partnerships that help hide Enron's losses

Arthur Andersen legal counsel instruct auditors to destroy Enron's files except the basic documents

$618M first quarterly loss was reported by Enron and disclosed a $12B reduction in shareholder's equity owing in part to Fastow's partnership

Arthur Andersen was convicted because of obstruction of justice 78 charges of conspiracy, fraud, money laundering and other counts was charged to Fastow

The SEC extended its investigation to Arthur Andersen

Enron's shares rose to an exceptional high of $90.56 per share

Jeffrey Skilling became CEO of Enron after Lay decided to retire

The Department of Justice started its criminal investigation to Enron

Economic Implications Fraudulent Energy Crisis

Enron defrauded California by creating imaginary shortages in energy supplies during the 2000-2001 California energy crisis that drive up prices and reap vast profits in the state's newly deregulated energy market.

This was passed by the congress in response to the scandal, to protect the interest of investors and further the public interest in the preparation of informative, accurate and independent audit reports

Sarbanes-Oxley Act

Skilling introduced the Mark-to-Market accounting technique—recognizing unrealized future gains, from some trading contracts into current income statement, presenting an illusion of higher profits. With its troubled assets, the company started to dump those in SPEs (Special Purpose Entities) to keep it off from ENRON’s book to make the losses look less severe than they really were. Because of MTM, the company boosted its stock price attracting more investors to the company.

Enron filled for chapter 11 bankruptcy

Skilling and Lay's trial began in

October 31 Houston,Texas

1985

(^1990 )

2000

2001

February 12

August 14

October 12 October 16

October 22

November 8

December 2 November 29

2002

January 17

June 15

2005

January 30

Creative Accounting

Brondo · Kallos · Petalio

OBJECTIVITY PRINCIPLE

The objectivity principle states

that accounting information and

financial reporting should be

independent and supported with

unbiased evidence. WORLDCOM violated

this principle by fabricating non-existent

revenues, without actual and valid

documents supporting the entries made.

MATCHING PRINCIPLE

Matching principle requires expenses to

be matched with revenues. WORLDCOM

violated this principle by capitalizing

period expenditures, overstating both

assets and equity. -Since expenses are

understated, cash flows and profit

inflated having no real matching of

revenues and expenses.

WorldCom's CFO fraudulently took

billions of dollars in operating expenses

and spread them out across so-called

property accounts—a type of capital

expense account. As a result, in 2001, the

company inflated revenue by roughly $

billion and reported a $1.4 billion profit

instead of a loss. Had the operating costs

been correctly reported, WorldCom

would have lost money for the 2001

fiscal year and first quarter of 2002. The

fraud was characterized mainly by the

improper reduction of line costs and

false adjustments to report revenue

growth.

Date of discovery : JUNE 2002

Person behind the discovery : Cynthia

Cooper , vice president of the

company’s internal audit unit

The fraud was uncovered through the

discovery of over $3.8 billion fraudulent

balance sheet entries. Eventually,

WORLDCOM was forced to admit that it

had overstated its assets by over $

billion.

This spate of corporate crime led to the

Sarbanes-Oxley Act in July 2002, which

strengthened disclosure requirements

and the penalties for fraudulent

accounting. In the aftermath,

WorldCom left a stain on the reputation

of accounting firms, investment banks,

and credit rating agencies that had

never quite been removed.

It is America's second-biggest long-

distance phone company, built up over

the years through a dizzying array of

mergers and acquisitions by its founder,

Bernard Ebbers. At the peak of the

telecoms boom, WorldCom was valued

at $180bn (£118bn) and employed

80,000 people. Mr Ebbers had a

personal fortune of $1.4bn.

WorldCom came into existence as a

result of a merger between an obscure

long-distance resale company, LDDS

(Long Distance Discount Service), and

two smaller firms, MFS

Communications and UUnet in the

early 1990s. The acquisition spree

culminated in the 1998 $37bn merger

with MCI, America's second-largest

long-distance phone company after

AT&T.

ACCOUNTING

PRINCIPLES VIOLATED

The meteoric rise and fall

of WorldCom has been

intimately linked to Wall

Street investment firms --

in particular Salomon

Smith Barney and its

parent company

Citigroup.

HOW DID WORLDCOM

BEGIN?

WHO WERE THE

PEOPLE INVOLVED?

From left to right - Bernard Ebbers (Chief

Executive Officer), Scott Sullivan (Chief

Financial Officer and Secretary), and

David Myers (Controller and Senior Vice

President)

WHEN WAS

WORLDCOM IN

TROUBLE?

HOW WAS THE FRAUD

DISCOVERED?

EFFECT OF THE FRAUD

IN THE FIELD OF

ACCOUNTING

WHAT IS WORLDCOM?

Tyco International Ltd. is a diversified manufacturing and service company, with four main operating

groups: healthcare and specialty products, fire and security services, flow control, and electrical and electronic components.

JUN 4, 2002

In early 2002, the Board of Directors of Tyco learned that one of its members Frank Walsh was paid $ 20 million commission (findets fee) for the role he played in aiding and securing the CIT merger, a payment that the rest of the board were unaware of. This prompted Tyco to carry an in depth internal investigation which uncovered many expense misemployments. In the same year, they observed the transfers of large sums of money from Tyco's accounts to Kozlowski's personal accounts. TYCO CANDAL The former executives were accused of giving themselves interest free or low interest loans for personal purchases of property, jewelry and other frivolities. According to SEC, these loans were never approved or repaid. Kozlowski, CEO, and Schwartz, CFO, were accused of issuing bonuses to themselves and other employees without the approval of Tyco's Board of Directors. It is alleged that bonuses were acted and used to buy the silence of those who suspected the former CEO and CFO of fraud. They are also indicted with charges for selling their company's stock without telling investors. Commingling of assets occured when Kozlowski considered the assets of Tyco as his own personal assets. He used Tyco's funds to pay for his personal expenses like his second wife's birthday party.

JUL 20, 2002

Kowlowski and Swartz accused of enterprise corruption for stealing $170 million from Tyco and taking $430 by fraud in the sale of company shares. Kzlowski splits Tyco into four publicly traded companies which causes the price of Tyco shares to fall. Edward Breen reaplces Kozlowski and immediately starts to revise accounting processes. Kozlowski and Swartz found guilty for stealing $150 million from Tyco and sentenced up to 25 years in prison.

ABOUT THE COMPANY

JAN 30, 2002

Kozlowski and Swartz Lie About Selling Stock (^) JUN 3, 2002 As Kozlowki resigns he is said to be under a sales tax evasion investigation. Kozlowski is accused of conspiring to avoid $1 million in sales tax on art purchases.

WHO WERE INVOLVED?

DENNIS KOZLOWSKI MARK SWARTZ FRANK WALSH MARK BELNICK

TIMELINE 1960

Tyco is founded as a research laboratory.

FEB 11, 1992

Dennis Kozlowski Hired as CEO 1997 The company merges with Bermuda-based security-systems- provider ADT.

MAR 13, 2001

Tyco spends $9.2 in cash and stock to acquire CIT group through Frank Walsh. JAN 22, 2002

SEP 12, 2002

JUL 20, 2002

Frank Walsh pleads guilty to trying to hide $20 million in fees from the CIT Group deal.

OCT 7, 2003

Trial of Kozlowski MAR 17, 2004 and Swartz Begins Mistrial Declared Second Trial for Kozlowski and Swartz Begins

JAN 26, 2005

MAR 17, 2005

Kozlowski, Swartz, Benick, and Walsh, the four major stakeholders are found guilty.

HOW DID THE FRAUD HAPPEN?

HOW WAS IT DISCOVERED?

JUN 17, 2005

WHAT HAPPENED...

WIRECARD, WHICH OFFERED ELECTRONIC PAYMENT TRANSACTION SERVICES, RISK

MANAGEMENT AS WELL AS PHYSICAL AND VIRTUAL CARDS, COLLAPSED ON JUNE 25, OWING

CREDITORS ALMOST $4 BILLION AFTER DISCLOSING A GAPING HOLE IN ITS BOOKS THAT ITS

AUDITOR EY SAID WAS THE RESULT OF A SOPHISTICATED GLOBAL FRAUD. $2 BILLION OF THE

REVENUE WAS BOOKED FROM A CLIENT NAMED LONG SHOT SHADY INC. THE COMPANY

DISCLOSED THE FOLLOWING INFORMATION REGARDING THIS:

WIRECARD FRAUD:

THIS IS AN AGREEMENT WITH A CREDIT CARD PROCESSOR IN

THE PHILIPPINES THAT WIRECARD USED TO PROCESS CREDIT

CARD TRANSACTIONS, WHERE THEY ACTUALLY DON'T HAVE

LISCENCE TO OPERATE IN THE JURISDICTION, THEY JUST SEND

THE TRANSACTIONS TO THEIR WAY AND THEY GIVE WIRECARD A

COMMISSION OUT OF IT.

THE REVENUES ARE BEING DIRECTED TO ESCROW ACCOUNTS

IN TWO OFFSHORE BANKS IN THE PHILIPPINES--BDO UNIBANK &

BANK OF THE PHILIPPINE ISLANDS

WIRECARD FRAUD

CASE ANALYSIS NO. 8

FINANCIAL REPORTING, FRAUDS AND ETHICS

THE AUDITOR SHOULD HAVE RESORTED TO TESTING THE CASH RECEIPTS OF BANK ACCOUNTS WHERE CASH WAS RECEIVED

FOR THESE REVENUES.

THE AUDITOR REQUESTED AND SET OUT BANK CONFIRMATIONS TO THE OFFSHORE BANKS IN THE PHILIPPINES REGARDING THE ESCROW ACCOUNTS; ANY OF THEM HAVE NOT RESPONDENT.

COPIES OF THOSE BANK ACCOUNTS; ANY OF THEM HAVE NOT RESPONDED

THE AUDITOR RELIED ON THESE STATEMENTS INSTEAD OF INSISTING TO GET BANK CONFIRMATIONS.

WHAT SHOULD HAVE HAPPENED...

THE AUDITOR SHOULD HAVE ASKED FOR A CONTRACT PERSON AT THE CLIENT'S SIDE TOT INDEPENDENTLY VERIFY THE INVOICE BALANCES.

STEVE ROGERS NO RESPONSE FOR A WEEK...

WHAT HAPPENED...

ESCROW ACCOUNTS (PHILIPPINES)

THESES ARE THE SAME ONES THAT THE AUDITORS SENT OUT THE CONFIRMATION LETTERS TO GET INDEPENDENT CONFIRMATION, BUT WERE NOT ABLE TO GET ANY ANSWERS.

THE AUDIT TEAM DID NOT RECEIVE ANY RESPONSE FROM ANY OF THESE BECAUSE THESE ACCOUNTS ACTUALLY DID NOT EXIST.

THE AUDIT TEAM DECIDED THAT THEY WON'T BE ABLE TO

ISSUE AN AUDIT REPORT WITHOUT THESE BANK

CONFIRMATIONS