Globa Markets

Analy i Rep t

A M th P bli i f Gi

Mae’s Office of Capital Markets

– men

l

s s or

on ly u cat on o nnie

Global Markets

Analysis Report

A MONTHLY PUBLICATION OF GINNIE MAE’S

OFFICE OF CAPITAL MARKETS

FEBRU

ARY

2022

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An analysis of the US housing market, including home price trends, prepayment rates, and the role of Ginnie Mae in mortgage-backed securities (MBS). It includes data on the relative attractiveness of US fixed income and Ginnie Mae MBS, as well as the amount of MBS securitized into collateralized mortgage obligations (CMOs) by coupon and by single or multifamily properties. The document also includes a table showing the historical volume of mortgages by type, including GSE, GNMA, private MBS, agency CMO, private CMO, banks, and thrifts from 2000 to 2021.

Typology: Slides

1 / 35

This page cannot be seen from the preview

Don't miss anything!

Global Markets Analysis Report

Highlights Manager), an Environmental Protection Agency (EPA) online platform for owners to upload and report energy performance for properties. The system measures and tracks energy and water consumption and greenhouse gas emissions on a 1-100 index score.” 3 With these green property requirements, owners “are incentivized to implement measures that result in projects with greater energy and water efficiency, reduced operating costs, improved indoor air quality and resident comfort, and reduced overall impact on the environment. For properties that have already achieved a green building standard and that are refinancing with this lower MIP premium, proceeds may be used to complete further efficiency upgrades, and/or to retrofit to the next-level green certification standards.” 4 The new Green Status field in the Multifamily data disclosure file provides investors with additional transparency that allows for granular ESG investment decisions in the Ginnie Mae MBS market. The implementation timeline for the new data field began on February 1, 2022, with the addition of the Green Status field to the Multifamily Pool and Loan New Issuance Daily file. The Green Status field will be fully implemented into data disclosure files by March 1, 2022 when the data is aggregated into the Multifamily Pool and Loan New Issuance Monthly Disclosure. Within the file, investors will be able to identify pools with green properties by looking at the final entry in each row. The entry will contain one of five MIP indicators which are combinations of the four FHA mortgage categories: GRA (Green/Affordable); GRB (Green/Broadly Affordable); GRM (Green/Market); NGR (Not Green); or blank (Unknown). Table 2, shown below, describes the four categories of FHA mortgages (Green, Affordable, Broadly Affordable, and Market) in further detail.

Table 2. FHA MIP Indicators^5 With the new data disclosure field, Ginnie Mae presents information to investors on Multifamily pools within the Ginnie Mae MBS portfolio that are collateralized by green properties. So, how might Ginnie Mae Multifamily

Highlights MBS investors use this new ESG data disclosure field? According to the U.S. Department of Housing and Urban Development’s (HUD’s) office of Housing, “For investors in Ginnie Mae MBS, green building disclosure provides additional transparency of loan collateral quality. Further, such disclosure—along with HUD’s underwriting policies—provides investors with the facts needed to assess environmental, social, and governance (“ESG”) factors. ESG investing has grown in popularity in recent years, and this disclosure supports investment selection for buildings that are certified to be energy efficient during HUD’s loan underwriting process.” 2

Relative Attractiveness of US Fixed Income and Ginnie Mae MBS 1.2 Global 10‐Year Treasury Yields The US 10-year Treasury yield moved to 1.78% at month end January 2022, a MoM increase of 27 bps. At month end January 2022, US Treasury yields remain the highest of all the government treasury yields depicted in the figure below. The yield on the UK 10-year government notes increased to 1.30% in January, a MoM increase of 33 bps. The yield on the German 10-year note increased to 0.01% in January, a MoM increase of 19 bps. This is the first time since March 2019 that the German yield has crossed back into positive territory. The yield on the Italian 10-year note increased to 1.29% in January, a MoM increase of 12 bps. The yield on the Japanese 10-year government notes increased to 0.17% in January, a MoM increase of 11 bps. At the end of January 2021, the hedged yield for the 10-year Treasury JPY shifted to 2.56%, a decrease of 6 bps from the previous month. The hedged yield for the 10-year Treasury EUR shifted to 1.46%, a slight decrease of 4 bps from the previous month. Global 10‐Year Treasury Yields 7–10yr Total Return Hedged Index, JPY 7–10yr Total Return Hedged Index, EUR

Relative Attractiveness of US Fixed Income and Ginnie Mae MBS 1.3 Ginnie Mae Yields– USD Ginnie Mae fixed rate MBS yields increased MoM in January 2022. Ginnie Mae II yields were at 2.33% on January 31, 2022, up by 45 bps from the prior month. Ginnie Mae I yields were at 2.45%, up by 36 bps from the prior month. On January 31, Ginnie Mae II SF yields were 55 bps higher than the US 10-year Treasury yield, representing an increase in spread of 36 bps since December 31, 2021. The yields on the Ginnie Mae I SF were 67 bps higher than the US 10-year Treasury yield on January 31, 2022, representing an increase in spread of 9 bps since December 31, 2021. Ginnie Mae II SF Yield, USD Ginnie Mae I SF Yield, USD

% Yield

Relative Attractiveness of US Fixed Income and Ginnie Mae MBS 1.5 Global Treasury Yield Per Duration GNMA MBS continue to offer higher yields in comparison to other government fixed income securities of various tenors with similar or longer duration. Prepayment risk is a feature of MBS. In January, the GNMA II 2.5% securities duration and yield increased MoM by 0.51 units and 38 bps, respectively. In January, the GNMA II 3% securities duration and yield increased MoM by 0.41 units and increased by 38 bps, respectively. Yield vs. Duration

Security Duration Yield

Relative Attractiveness of US Fixed Income and Ginnie Mae MBS 1.6 Monthly CMO Demand for Ginnie Mae MBS In January 2022, $15.7 billion of Ginnie Mae MBS were securitized into Collateralized Mortgage Obligations (CMOs) as underlying collateral, a 20% MoM increase. Of that, approximately $4 billion were Multifamily MBS, all having coupons between 2% and 3%. $11.2 billion were Single-Family MBS with over 90-percent of the Single- Family MBS having coupons between 2% and 3.5%. Through the first four months of Fiscal Year 2022 approximately $60 billion of Ginnie Mae Single-Family and Multifamily MBS were securitized into Ginnie Mae CMO transactions. This represents a roughly 8% decrease over the same period in Fiscal Year 2021. January 2022 CMO Collateral Coupon Distribution

State of the US Housing Market Nationally, home prices exceed their pre-crisis peak on a nominal basis by 48.6% through September 2021. As shown in both the tables above and below, the extent of HPI increases since the trough has varied from region to region and state to state. Nationally, home prices exceed the trough by 88.4%. As shown in the regional HPI table above, much of this asset appreciation has taken place during the pandemic.

State 2000 to Peak Peak to Trough Trough to Current YOY Current HPI % Above Peak National 59.6% -21.1% 88.4% 12.7% 48.6% AK 66.9% -5.2% 40.3% 9.0% 33.0% AL 41.6% -15.0% 64.7% 13.1% 40.0% AR 39.8% -11.0% 56.3% 13.1% 39.1% AZ 110.2% -49.5% 178.2% 20.8% 40.5% CA 144.8% -47.0% 137.5% 16.6% 25.8% CO 32.3% -10.3% 140.3% 16.1% 115.6% CT 72.9% -19.6% 36.9% 15.6% 10.0% DC 162.5% -11.7% 115.1% 10.8% 90.0% DE 88.5% -23.5% 52.0% 13.4% 16.3% FL 130.0% -46.5% 144.6% 17.2% 30.8% GA 35.9% -27.1% 112.7% 14.7% 55.1% HI 139.0% -27.0% 96.0% 11.9% 43.0% IA 27.8% -5.4% 54.2% 9.9% 45.8% ID 73.3% -32.2% 201.0% 28.4% 104.0% IL 49.9% -23.8% 46.4% 10.7% 11.6% IN 19.1% -8.7% 76.9% 13.3% 61.6% KS 31.0% -7.8% 66.2% 12.6% 53.2% KY 28.9% -5.4% 64.3% 12.6% 55.4% LA 51.6% -6.7% 45.0% 8.3% 35.2% MA 69.8% -18.2% 76.7% 14.4% 44.5% MD 126.4% -26.5% 51.8% 11.5% 11.6% ME 72.0% -12.4% 76.8% 18.3% 54.8% MI 18.4% -31.5% 110.8% 13.7% 44.3% MN 52.5% -23.0% 83.7% 12.0% 41.5% MO 39.2% -15.0% 74.2% 13.4% 48.1% MS 38.9% -12.8% 43.6% 9.9% 25.3% MT 79.3% -13.6% 98.1% 19.3% 71.2% NC 39.7% -14.1% 83.9% 16.2% 57.9% ND 51.7% -0.9% 69.8% 7.9% 68.3% NE 24.3% -5.9% 77.3% 13.0% 66.7% NH 72.7% -21.9% 81.1% 17.4% 41.4% NJ 102.2% -22.7% 50.2% 14.6% 16.2% NM 66.6% -17.9% 55.7% 12.8% 27.8% NV 117.4% -59.3% 203.6% 17.1% 23.6% NY 75.7% -10.5% 56.5% 13.5% 40.1% OH 19.6% -16.6% 77.4% 13.1% 48.0% OK 36.8% -4.6% 60.2% 11.9% 52.7% OR 85.6% -28.6% 129.9% 16.3% 64.1% PA 68.9% -10.9% 57.3% 12.6% 40.1% RI 108.1% -28.0% 79.2% 17.0% 29.0% SC 40.6% -16.0% 84.6% 14.3% 55.1% SD 40.2% -2.4% 72.9% 15.1% 68.7% TN 38.4% -12.6% 100.0% 17.2% 74.7% TX 35.8% -3.0% 96.9% 14.4% 91.0% UT 65.1% -26.1% 152.8% 23.1% 86.9% VA 95.1% -18.8% 59.7% 12.7% 29.8% VT 78.1% -10.3% 55.3% 16.8% 39.3% WA 83.4% -27.3% 144.1% 17.3% 77.5% WI 38.6% -14.2% 69.8% 12.6% 45.6% WV 39.2% -5.7% 40.8% 11.6% 32.8% WY 84.7% -9.7% 52.8% 10.7% 38.1%

State of the US Housing Market

Size of the US Residential Mortgage Market 2.2 Size and Value of the US Housing Market The total value of the single-family housing market reached $36.8 trillion in Q3 2021. The value of household equity has continued to trend upward into Q3 2021. As mentioned in Section 2.1 above, the unprecedented pace of asset appreciation during the pandemic is driving much of the increase in the overall value of real estate as an asset class, as debt remains relatively flat. The total value of the US housing market is up 93.4% from its trough in 2011. Conversely, mortgage debt outstanding has increasing slightly from $11.3 trillion in Q2 2021 to $11.5 trillion in Q3 2021. Agency MBS account for a growing percentage of the total mortgage debt outstanding, up to 67% of total mortgage debt. Value of the US Housing Market

Debt Household equity Total Value

Private Label Securities Home Equity loans Agency MBS Unsecuritized first liens

State of the US Housing Market 2.4 Characteristics of Ginnie Mae Loans in Forbearance 157,070 Ginnie Mae loans were in forbearance as of the end of December 2021. This represents 6% decrease MoM, lower than the 11% MoM pace observed in October and November. 8,292 of loans in forbearance were removed from MBS pools and 148,778 still actively remain in pools. Most liquidated loans (5,986) were FHA and within that subset, 3,482 of those loans were originated by nonbanks. Approximately 96% of the loans that were in forbearance at the end of December were due to COVID-19 circumstances.

State of the US Housing Market

Number of Loans Removed from Pools: Nonbank The current share of Ginnie Mae loans in forbearance stands at 1.47% as of the end of December, down approximately a tenth of a percent MoM from 1.57% at the end of November. This approximately 10 bps decline is roughly half the decrease observed in each of the prior two months, during which the total forbearance percentage dropped approximately 20 bps each month. The forbearance rate remains significantly higher than the forbearance rate prevailing in the period prior to the pandemic between Jan 2019 and February 2020 (approximately 0.1%), and, as stated above, the rate of convergence to pre-pandemic rates has slowed in December.

Share of Ginnie Mae Loans in Forbearance

Mortgagor Payoff Repurchase of Delinquent Loan Loss Mitigation

Mortgagor Payoff Repurchase of Delinquent Loan Loss Mitigation

State of the US Housing Market 2.5 Ginnie Mae Agency Issuance and Agency Outstanding by State Ginnie Mae MBS represent approximately 24% of new Agency issuance over the past year. The share of Ginnie Mae collateral outstanding varies across states, with the highest Ginnie Mae share in Alaska (47%) and the lowest in the District of Columbia (12%). The difference between Ginnie Mae share of Agency Issuance (24%) over the past year and Ginnie Mae’s share of overall outstanding Agency MBS (26%) is reflective of ebbs and flows in FHA and VA first lien origination market share, discussed in Section 2.8 below.

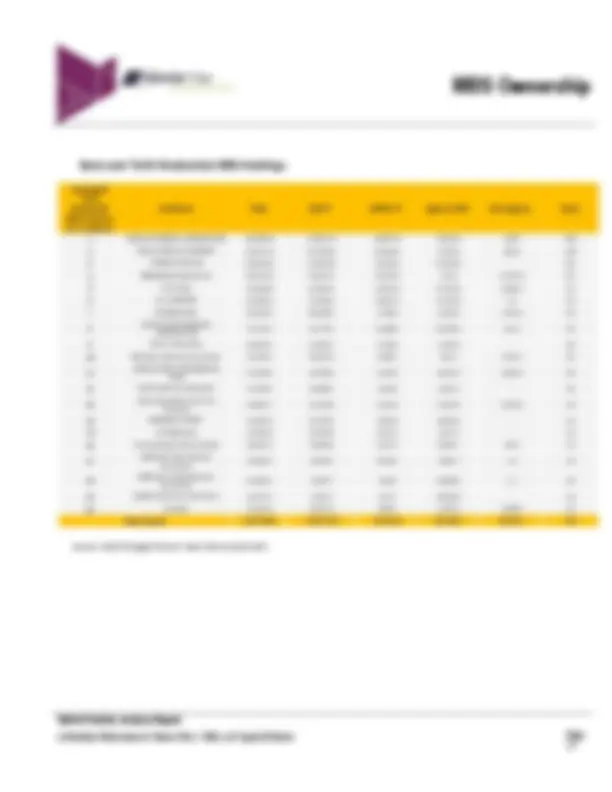

Agency Issuance (past 1 year) Agency Outstanding National GNMA Share GNMA Loan Count GNMA Avg. Loan Size (000) GSE Avg. Loan Size (000) GNMA Share by UPB^ GNMA Loan Count GNMA Avg. Loan Size (000) GSE Avg. Loan Size (000) 24% 2,957,558 273.57 293.21 26% 10,611,120 186.89 217. AK 49% 10,581 304.93 288.76 47% 36,948 254.48 218. AL 37% 58,761 215.19 227.73 40% 231,762 147.38 172. AR 35% 31,244 183.82 206.35 39% 135,562 125.05 155. AZ 23% 95,711 279.21 281.77 25% 273,817 201.58 215. CA 16% 240,876 426.71 415.08 16% 670,676 311.59 316. CO 24% 79,248 363.20 344.07 23% 213,609 273.28 268. CT 23% 26,272 262.09 276.87 25% 103,430 195.30 207. DC 12% 2,653 470.08 456.22 12% 8,577 365.06 350. DE 29% 14,188 261.93 268.76 32% 50,192 196.72 206. FL 30% 252,363 270.26 267.45 32% 831,131 197.58 200. GA 31% 135,038 239.74 264.51 34% 489,860 167.46 198. HI 36% 12,779 588.53 465.86 31% 32,769 452.75 352. IA 18% 17,967 171.32 196.98 22% 81,793 128.14 148. ID 22% 19,636 295.77 285.57 23% 64,726 198.58 213. IL 19% 86,619 214.89 241.16 21% 350,953 154.22 177. IN 26% 65,546 185.95 196.86 30% 277,063 126.10 146. KS 26% 22,722 197.64 217.06 29% 96,432 133.95 160. KY 30% 40,245 193.66 204.55 34% 161,456 136.18 152. LA 38% 46,502 209.49 231.53 39% 190,130 152.10 174. MA 15% 34,521 364.38 355.92 15% 110,997 271.52 267. MD 32% 87,510 347.15 323.67 33% 282,749 256.95 247. ME 23% 10,310 230.56 250.45 26% 37,641 169.40 187. MI 17% 64,712 186.46 208.28 20% 273,508 127.06 154. MN 16% 38,379 249.33 256.88 18% 159,445 175.46 195. MO 25% 57,599 195.77 211.05 29% 243,545 134.99 158. MS 43% 26,214 199.33 209.62 47% 117,872 135.93 157. MT 20% 9,479 237.48 280.44 24% 33,070 197.55 208. NC 26% 114,594 236.22 261.21 29% 412,659 164.70 194. ND 20% 4,886 190.94 237.66 23% 16,629 188.11 184. NE 23% 14,283 214.57 208.25 27% 65,419 141.40 157. NH 20% 10,955 293.28 280.99 23% 38,729 216.76 210. NJ 19% 61,968 314.00 331.84 21% 224,915 229.92 251. NM 34% 22,387 231.39 234.97 38% 94,187 158.29 173. NV 30% 45,507 314.08 293.92 31% 130,545 232.75 225. NY 17% 55,458 314.65 342.18 20% 302,033 199.26 243. OH 24% 92,657 180.99 200.43 29% 417,815 124.29 146. OK 38% 40,091 197.41 210.24 43% 187,850 134.02 157. OR 19% 36,852 323.14 323.49 19% 110,671 240.20 245. PA 21% 80,724 206.74 243.51 26% 385,055 144.68 178. RI 28% 10,204 299.99 274.47 29% 34,639 220.79 209. SC 32% 68,060 235.20 245.64 34% 227,632 172.07 185. SD 27% 7,433 228.88 225.90 29% 29,144 164.48 174. TN 28% 71,206 241.75 258.18 32% 273,153 163.41 195. TX 29% 267,675 251.89 273.81 32% 1,062,415 171.15 202. UT 18% 33,551 331.03 323.09 19% 97,285 239.54 252. VA 35% 137,389 339.68 325.23 36% 435,485 247.57 248. VT 18% 3,029 236.69 249.07 19% 12,101 176.44 177. WA 21% 78,933 370.73 370.52 22% 234,175 269.10 282. WI 15% 32,874 205.06 217.46 17% 122,651 150.15 161. WV 40% 13,879 195.86 196.26 43% 57,036 138.50 142. WY 34% 7,714 258.02 252.48 35% 24,980 198.91 197.

State of the US Housing Market

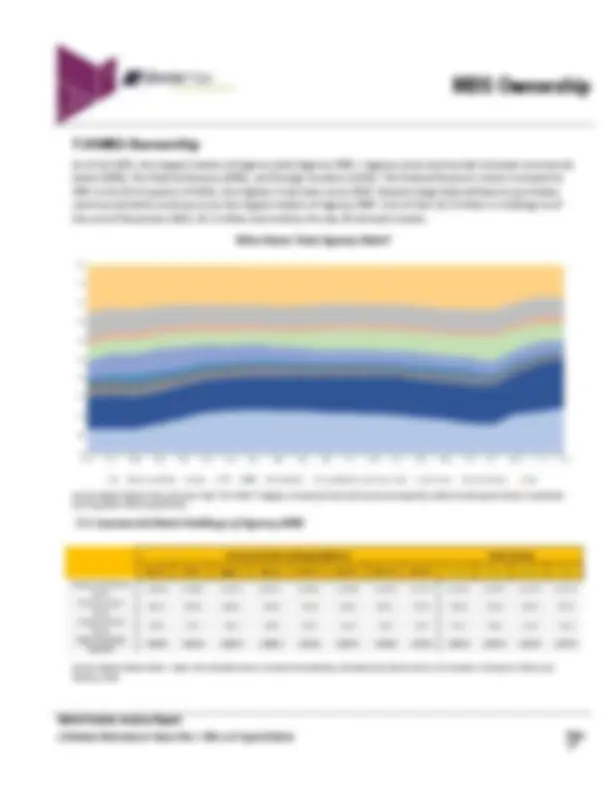

2.6 Outstanding Single‐Family Agency MBS As of December 2021, outstanding single-family securities in the Agency market totaled $7.79 trillion: 40.2% Fannie Mae, 34.0% Freddie Mac, and 25.8% Ginnie Mae MBS. Over the past twelve months, Freddie Mac’s total outstanding issuance has increased by approximately 17%, while Fannie and Ginnie have decreased outstanding issuance by 2% and 3% respectively. Despite this, Fannie outstanding remains larger than either Freddie or Ginnie by approximately $0.5 trillion and $1.1 trillion, respectively. Ginnie Mae MBS collateral composition has changed dramatically over the past ten years. In December 2011, 76% of Ginnie Mae outstanding collateral was FHA and 19.5% was VA. In December 2021, FHA collateral comprised 53% of Ginnie Mae MBS outstanding and VA collateral comprised 42% of Ginnie Mae MBS outstanding. Outstanding Agency Mortgage‐Backed Securities

Composition of Outstanding Ginnie Mae Mortgage‐Backed Securities