Download Greater Exeter Economic Development Needs Assessment and more Exams Business in PDF only on Docsity!

Greater Exeter Economic

Development Needs Assessment

Final Report

Prepared for Greater Exeter Strategic Plan authorities

Devon County Council

East Devon District Council

Exeter City Council

Mid Devon District Council

Teignbridge District Council

and for

Dartmoor National Park Authority

March 2017

Contents

- 1 Introduction...................................................................................................................................... Executive Summary.................................................................................................................................. i

- 2 The Functional Economic Market Area

- 3 Socio-Economic Baseline

- 4 Economic Growth Plans and Aspirations

- 5 Employment Land Supply

- 6 Future Employment Growth Scenarios

- 7 Future Sites and Premises Requirements

- 8 High Level Property Market Trends

- 9 Conclusions.....................................................................................................................................

- Glossary

- Job Number:

- Version Number: 3.

- Date: 9 March Approved by: Gareth Jones

ii

concentrated in Exeter, and Financial & Insurance employment is also lower than the national average (LQ = 0.79)^2.

0.3.3 Mid Devon is a mainly rural district with a number of market towns. Tiverton, Cullompton and Crediton are the largest towns. Mid Devon includes a very small section of the Dartmoor National Park. Manufacturing and Wholesale & Retail are strong in Mid Devon, and Construction is also an important sector. The district has lesser employment concentrations in Information & Communications, and Finance & Insurance.

0.3.4 East Devon is characterised by a number of market towns, a large rural area, and large coastal areas. The District has seen strategic investment and growth in housing and employment on its western edges close the City of Exeter. The largest towns in East Devon are Honiton, Axminster, Sidmouth, and Exmouth. Wholesale & Retail, Transport & Storage, and Accommodation & Food Services show high employment concentrations. Construction is also an important sector in East Devon. The district has less employment concentrations in Manufacturing, Information & Communications, and Finance & Insurance.

0.3.5 Teignbridge includes part of the south west edge of Exeter, and is characterised by rural market towns and coastal areas. Newton Abbott is the biggest town in Teignbridge, with Kingsteignton and Teignmouth being the other main settlements. Teignbridge includes a large section of the Dartmoor National Park. Manufacturing, Wholesale & Retail Trade, Accommodation & Food Services, and Real Estate all display high employment concentrations. Construction is also an important sector in Teignbridge. The district has lower employment concentrations in Information & Communications and Finance & Insurance.

0.3.6 Dartmoor National Park covers parts of Mid Devon, South Hams, Teignbridge, and West Devon District Councils. It is a semi-natural upland area, characterised by small, dispersed settlements. Ashburton and Buckfastleigh are the largest of these settlements, with populations of around 3,500. Dartmoor has a high concentration of employment in Mining & Quarrying, Construction, Accommodation & Food, and Real Estate. Manufacturing, Wholesale & Retail, and Finance & Insurance are less concentrated in Dartmoor.

0.4 Economic growth plans and aspirations

0.4.1 There is already an established area-wide approach to developing a new economic strategy for Greater Exeter, through the partnership for Exeter and the Heart of Devon. The Economic Development Strategy for this area seeks to deliver growth in the economy through both productivity growth and growth in the size of the business base and employment. Productivity growth may drive the need for new, modern premises that are fit-for-purpose for high value, high productivity activities, and growth in the business base and employment is likely to generate demand for new employment land and premises.

(^2) See Section 3.11 for more information on sector concentrations.

iii

0.4.2 Historically Exeter has been the driver of economic growth in the Greater Exeter area. This is the main office location in Greater Exeter, and has many higher value employers including those associated with the Met Office and University. Whilst the regeneration of brownfield sites and conversion of buildings will continue to deliver economic growth, the city has a limited supply of employment land for future development, and recent and future growth is taking place to the east of the city, close to Junction 29 of the M5. Establishment of an Enterprise Zone in East Devon is intended to increase economic growth in this area. Much of Greater Exeter’s planned future growth in high-value research, innovation and office-based employment will take place to the east of the city, along with manufacturing and distribution that is attracted by the accessibility of the location. There will be additional development of sites for manufacturing and distribution, which are likely to be in close proximity to Exeter and the M5/A38/A380 corridor where market demand is greatest, but not exclusively.

0.4.3 The four Districts together create a diverse and resilient economy, forming a collaborative environment that supports investment. Each District has their own economic growth aspirations which look to contribute to the economic growth of the whole area: East Devon : the western part of East Devon will be a focal point for development, which will accommodate wider growth aspirations including employment growth attracted by and associated with the success and role of Exeter, including a new Exeter Science Park associated with the University of Exeter. Exeter : the Innovation Exeter Programme is setting a long term framework for the future growth of Exeter’s economy in terms of transformational changes towards a knowledge economy, based around its strengths as recognised by the Government’s Science and Innovation Audit (namely: applied environmental science, digital innovation, data analytics, and high performance computing). Exeter City Futures is also part of this overarching framework. Mid Devon : the economic focus is on attracting higher skilled employment, and this will be achieved by up-skilling the workforce. In particular the Council wants to support and encourage technical and scientific businesses. Teignbridge : economic growth aspirations focus on successful, growing local businesses providing a good range of jobs. The Council is particularly keen to encourage growth in smaller businesses because of the greater resilience that a diverse business base has in any future economic downturn. There is also a focus on providing viable and attractive town centres, as well as delivering sustainable transport.

- Dartmoor National Park : economic aspirations are centred on supporting appropriate economic growth rooted in the quality of landscape and place, increasing productivity through the development of the National Park productivity network and rural enterprise zone, increasing international tourism, and further developing a strong food and drink offer.

0.4.4 There are aspirations to invest in the market towns that surround Exeter. Much of this investment will facilitate leisure, residential and some employment development. The surrounding town centres are unlikely to grow into more significant employment locations.

0.4.5 The existing local plans for each of the Greater Exeter districts identify a significant amount of land to accommodate future economic growth. These include:

v

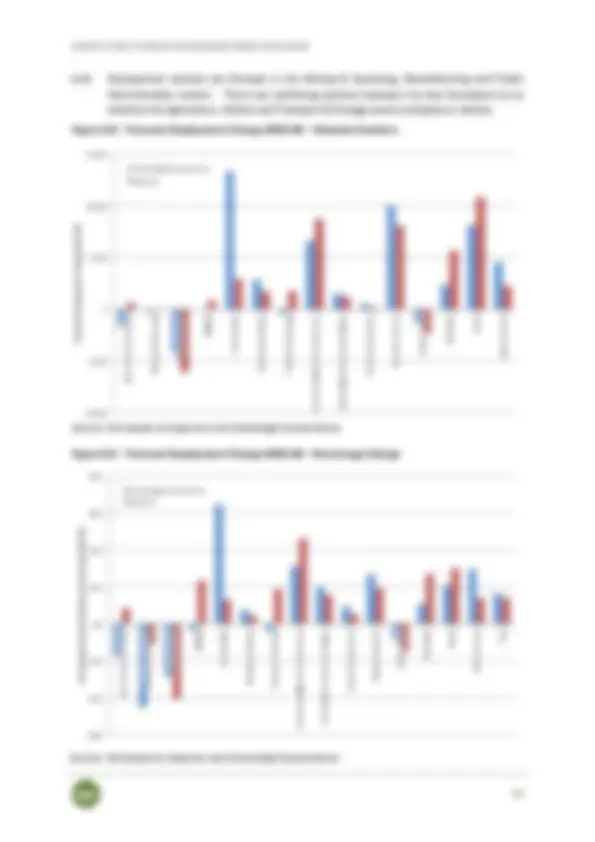

0.6.2 The two forecasters’ baseline assessments are for employment growth of between 1, and 1,700 new jobs per year over the period from 2015 to 2040. The hybrid and alternative scenarios push this rate up to between 1,600 and 2,000 new jobs per year. The main sectors experiencing the highest levels of absolute growth under the baselines and alternative scenarios are: Construction Accommodation & Food Services Business Services

0.6.3 Manufacturing and Public Administration in particular are expected to see a decline in employment over the period to 2040.

0.6.4 When these sectors are allocated to Planning Use Classes^4 , the largest growth in employment is seen in jobs which do not require any employment property provision (i.e. those people that work from home, are peripatetic, or who work in service roles in others’ premises). Use Classes A and C are next largest, closely followed by Use Class D. Jobs in Use Class B only account for between 4 % and 12% of total employment growth (based on the hybrid and three alternative scenarios), although this is heavily influenced by the decline in employment in Manufacturing.

Greater Exeter Strategic Plan (GESP) area

0.6.5 The two forecasters’ baseline assessments are for employment growth of between around 1,400 and 1,600 new jobs per year over the period from 2015 to 2040. The hybrid and alternative scenarios push this rate up to between 1,500 and 1,900 new jobs per year. The main sectors experiencing the highest levels of absolute growth under the baselines and alternative scenarios are the same as the wider HMA.

0.6.6 When these sectors are allocated to Planning Use Classes, the profile is very similar to the wider HMA.

Dartmoor National Park

0.6.7 In Dartmoor, the hybrid scenario forecasts growth of 1,710 net additional jobs over the 25- year period. This equates to approximately 70 jobs per annum. This equates to around 17% growth over the entire period.

0.7 Labour market dynamics

0.7.1 Economic activity rates across East Devon, Mid Devon and Teignbridge are forecast to rise. In Exeter overall economic activity rates are forecast to decline. The rising student population which is forecast appears to be the primary driver of these falling rates.

0.7.2 Occupational and skills data shows a move towards a higher skilled workforce.

(^4) A useful guide to Use Classes can be found here: http://nlpplanning.com/uploads/ffiles/2015/08/776168.pdf

vi

0.7.3 The Experian model shows a rising trend towards commuting into Exeter and out from the other three districts. However, in reality this will be influenced by the location of new employment accommodation.

0.8 Forecast employment land requirement

HMA

0.8.1 Focusing on future employment land requirements in Use Class B, it is important to note that future requirements are driven by more factors than just future employment growth. These are: Replacement of employment space as it becomes outdated and no longer fit-for-purpose. This is an important factor in the Manufacturing sector, where employment is declining, but there is still a healthy demand for new workspace Some replacement of employment developments will take place on existing sites which are re-used, but other development will need to take place on new employment sites

- An allowance for choice and flexibility must be made, ensuring that businesses have a choice of possible properties to meet their needs, and that there is sufficient flexibility in the employment property stock to allow businesses to upgrade or downgrade their requirement dependent on their particular circumstances

0.8.2 The main employment space requirements in the B Use Classes over the period 2040 are:

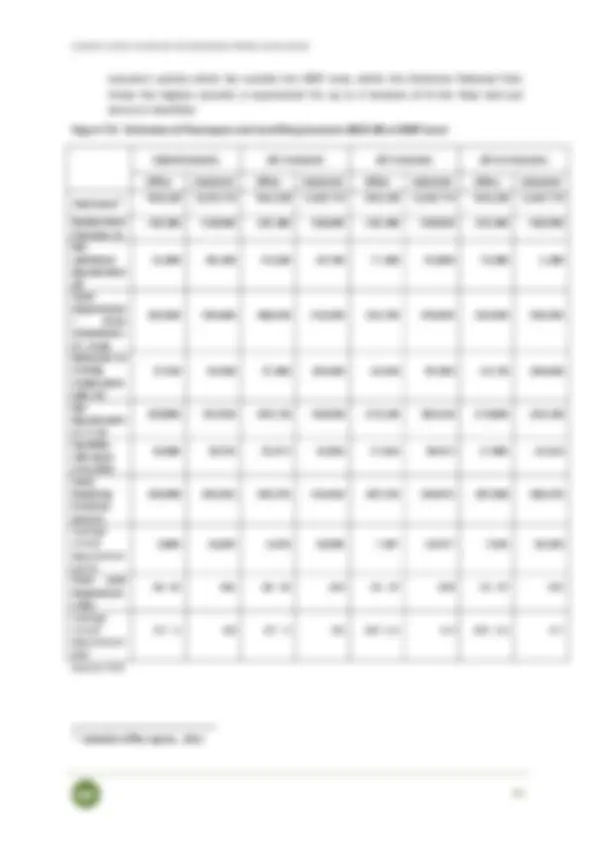

Between 190,000 sq m and 220,000 sq m of gross additional office space depending on which scenario is considered

- Between 465,000 sq m and 540,000 sq m of industrial space (covering both manufacturing and distribution), depending on which scenario is considered

0.8.3 When allowances for delivery on allocated sites, flexibility and choice are included, the B Use Class requirements become: Between 165,000 sq m and 190,000 sq m of offices – equivalent to 6,700 sq m to 7,600 sq m per year

- Between 410,000 sq m and 475,000 sq m of industrial – equivalent to 16,500 sq m to 19, sq m per year

0.8.4 In terms of sites, this means:

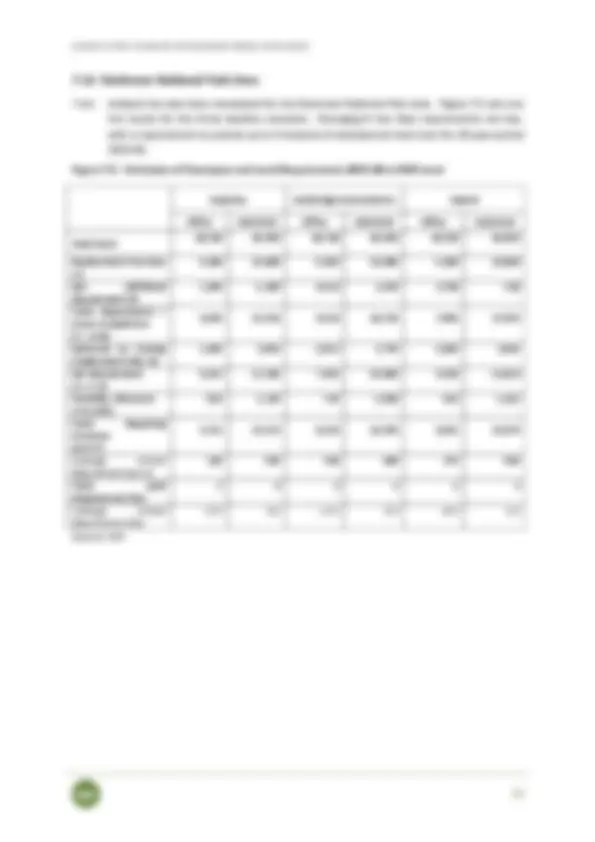

Between 19 ha and 27ha for offices over the period to 2040 – depending on the scenario considered and the density at which the offices are developed (i.e. in-town or out-of-town). This equates to between 0.8 ha and 1.1 ha per year across the HMA

- Between 103 ha and 119 ha for industrial over the period to 2040 – depending on which scenario is considered. This equates to between 4.1 ha and 4.7 ha per year across the HMA

0.8.5 It appears that there is a significant amount of allocated land in the current Local Plans for the Greater Exeter districts. However, East Devon District Council officers have raised questions about the deliverability of some of this land, due both to site-specific barriers and constraints, and also the difficulty of delivering viable development. Delivering employment

viii

0.10 Location of future development

0.10.1 Exeter is a very strong office location. Market sentiment is towards sites in the city centre and close to the motorway junctions, in particular sites close to key transport networks. Office-based, R&D, industrial and distribution businesses are all interested in being located in this area. This fits well with the Growth Point status and Enterprise Zone status which are helping to progress and deliver sites here. Market signals suggest that industrial and, to a slightly lesser extent, distribution businesses are also interested in sites close to motorway junctions within Greater Exeter.

0.10.2 Viability is strongest and therefore deliverability of employment sites is easiest close to Exeter and sites with strong transport links. It is more difficult further away from here. Delivery models such as public intervention or mixed-use with residential should be considered for harder to deliver sites.

0.10.3 Sustainable access to new employment developments needs to be given significant consideration in the process of allocating any further employment sites, and in broader economic development strategy.

1 Introduction

1.1 Background

1.1.1 The Local Authorities in the Greater Exeter area are starting work on aligned planning policy and development strategy. As part of this there are moves towards preparing a joint Strategic Plan for the area. The Joint Strategic Plan will cover: East Devon Exeter Mid Devon

1.1.2 The parts of Teignbridge and Mid Devon that fall inside the Dartmoor National Park boundary are not included in the Joint Strategic Plan area.

1.1.3 Dartmoor National Park is preparing its own Local Plan, and analysis from this EDNA report will be used to inform that plan. Therefore analysis for the whole of DNP is included in this report.

1.1.4 Devon County Council is also a partner in this joint planning work. Dartmoor National Park Authority likewise has a number of interests, both as an adjoining planning authority, and as an authority within the Exeter Housing Market Area.

1.1.5 In this context these partners have commissioned an Economic Development Needs Assessment (EDNA) for the Exeter Housing Market Area (HMA) and Dartmoor National Park including areas of West Devon and South Hams, which looks ahead to 2040. This will provide a key piece of evidence for informing the future development and direction of the joint Greater Exeter Strategic Plan and the Dartmoor Local Plan, and will provide the economic element of a Housing and Economic Development Needs Assessment as referred to in National Planning Practice Guidance.

1.1.6 The Exeter HMA is defined by the Strategic Housing Market Assessment (SHMA) as the geographic area covered by East Devon District Council, Exeter City Council, Mid Devon District Council, Teignbridge District Council and the part of Dartmoor National Park falling within Teignbridge and Mid Devon Districts. The Dartmoor National Park falls within 2 HMA’s, Exeter and Plymouth.

1.1.7 The different spatial scales under consideration in this report are shown in Figure 1.1 below.

The Joint Strategic Plan area (i.e. the HMA less that part of it covered by Dartmoor National Park)

- Dartmoor National Park area separately

1.2.2 This economic development needs assessment will help to identify the future scale and location of employment land needed to enable the four Greater Exeter local authorities and the Dartmoor National Park Authority to reach their economic growth aspirations and potential. This assessment is based on quantitative analysis including economic growth forecasts, and also on qualitative evidence from consultations with the local authorities, the business community and other important local stakeholders. The approach is compliant with the National Planning Policy Framework, Planning Practice Guidance, other relevant guidance and current best practice.

1.2.3 The report includes:

A definition of the Functional Economic Market Area A review of the local economy and recent trends A set of future growth scenarios which are informed by ‘baseline’ future growth projections from Cambridge Econometrics and Experian. These have been developed in consultation with the client steering group, and draw on qualitative evidence from consultations as well as quantitative evidence The scenarios include future employment projections and estimates of economic activity rates, commuting ratios and unemployment An assessment of the scale and location of future economic growth and therefore employment land

- Coverage of the three main geographical areas of interest: the Greater Exeter HMA, the Joint Strategic Plan area and Dartmoor National Park.

1.3 Structure of the report

1.3.1 The rest of this report comprises the following chapters:

Chapter 2 set out the consideration and definition of the Functional Economic Market Area for Greater Exeter

Chapter 3 sets out the socio-economic baseline for the Greater Exeter area

Chapter 4 considers the economic growth aspirations for the area

Chapter 5 considers the current supply of employment land in the Greater Exeter area, and the historic rate of employment land take-up

Chapter 6 sets out the future economic growth prospects for the Greater Exeter area, including the baseline economic growth forecasts and scenarios

Chapter 7 converts the economic growth prospects into a demand for employment land over the period to 2040

Chapter 8 sets out high-level trends in the property market which may influence future demand in Greater Exeter

Chapter 9 sets out the conclusions to the study

1.3.2 There are also a number of appendices to this report:

- Overview of the methodology

- Consideration of the Functional Economic Market Area in support of Chapter 2

- Baseline socio-economic analysis in support of Chapter 3

- Current employment land supply and recent take-up in support of Chapter 5

- Appendix to Chapter 6 on future employment growth

- Appendix to Chapter 7 on future sites and premises requirements

- High level property market trends in support of Chapter 8

- Dartmoor National Park data and analysis

- Greater Exeter Strategic Plan area data and analysis

- Property industry workshop notes

- Growth scenario setting workshop notes

Figure 2.1 – HoSW LEP area extent

Source: Heart of the South West Growth Hub

Travel to Work Areas (TTWA)

2.3.6 The local transport network converges on Exeter, with the M5 motorway, primary roads and rail network all coming into the city. Figure 7 in Appendix 2 shows that Exeter is the centre of the transport network. The transport network does not help with the determination of the boundary of the FEMA.

2.3.7 Consultations undertaken to inform this report, including with property industry professionals and District Council officers, discussed the newly opened South Devon Link Road which increases accessibility between Exeter, the southern part of Teignbridge and Torbay. Consultees suggest that this is more likely to draw commuters from Torbay into Exeter than it is to attract commuters from Greater Exeter into Torbay.

2.3.8 Latest ONS^6 TTWAs are based on 2011 Census data. In 2011 there is an Exeter TTWA which covers a large area and a Sidmouth TTWA that covers part of the study area. The two TTWAs cover a larger area than the proposed HMA. However, FEMAs can overlap and official TTWAs don’t allow this. To investigate this further, we have looked at the travel to work data from the 2011 Census to understand the patterns that underlie the TTWA definitions.

(^6) Further information on TTWAs can be accessed here:

http://webarchive.nationalarchives.gov.uk/20160105160709/http://www.ons.gov.uk/ons/guide- method/geography/beginner-s-guide/other/travel-to-work-areas/index.html

2.3.9 Travel to Work Areas (TTWAs) are defined to approximate self-contained local labour market areas, where the majority of an area’s resident workforce work, and where the majority of the workforce live. The criteria used for defining TTWAs is that generally at least 75% of an area's resident workforce work in the area and at least 75% of the people who work in the area also live in the area. The area must also have a working population of at least 3,500. However, for areas with a working population in excess of 25,000, self-containment rates as low as 66.7% are accepted. Figure 2.2 – The Exeter TTWA

Source: ONS

2.3.10 In general, the commuting patterns in Greater Exeter, seen in Figure 2.3 below, show that the City of Exeter is at the heart of the functional economic market area, and the broad boundaries align well with the District boundaries, particularly in East Devon and Mid Devon. Teignbridge to the south shows a strong flow into Exeter, but there are also strong net flows of commuters between the south of Teignbridge and Torbay. With the exception of Torbay the four Districts all show a strong coalescence around Exeter and not their neighbours further out.

2.3.11 Exeter City Council has commissioned research into commuting patterns into the city, and this has concluded that commuting patterns are unlikely to change significantly in the foreseeable future. Any significant future changes are likely to be driven by two factors: Exeter’s shortage of employment land and its tightly drawn boundaries is pushing new development out of the city

- The development of new employment sites in the Growth Point in East Devon, some of which is providing new employment space for Exeter

Property market area

2.3.12 The housing market area has been defined as part of the strategic housing market assessment^7 (there is also a new SHMA currently being produced). This report describes how a housing market area is determined, primarily using data on household migration and travel-to-work patterns. The report concludes that there is sufficient self-containment within the four Districts of East Devon, Exeter, Mid Devon and Teignbridge to form a housing market area.

2.3.13 When considering employment sites and premises, local property professionals have stated during a consultation workshop held in November 2016^8 that the Greater Exeter region is a reasonable approximation of a property market area. However, they do note that Torbay is a separate area of search to Exeter, although Newton Abbot might be included in a property search in Torbay.

Flow of goods, services and information, and service market for consumers

2.3.14 No quantitative data is easily available, but we have gathered qualitative information through stakeholder consultations. In consultation it has been suggested that Teignbridge residents use the retail facilities on Torquay’s edge-of-town retail parks, but there is little travel into the Torbay town centres. Higher-order flows are towards Exeter. The most recent adopted work on retail catchment was carried out in 2008^9 , but there is also an updated retail study currently underway. A retail catchment is the area drawn upon by a retail centre i.e. where consumers travel from to do their shopping. The summary map of the retail catchment area for Exeter, in Appendix 2, shows a catchment area that is larger than the Greater Exeter area. This is a function of the largely rural nature of surrounding areas and the lack of nearby competitor retail centres.

2.3.15 VenueScore is an annual survey compiled by Javelin Group, which ranks the UK’s top circa 3,500 retail venues including town centres, stand-alone malls, retail warehouse parks and factory outlet centres. VenueScore rankings are based on a scoring system which seeks to measure the overall attraction of each venue compared to other venues across the country. On this basis, Exeter city centre is by far the highest ranking retail centre in the Greater Exeter area. It is actually one of the highest ranking retail centres in the whole of the UK, ranking 22nd^ overall for 2016/17. Newton Abbott and Exmouth are also strong performers,

(^7) DCA (2014) Exeter Housing Market Area: Strategic Housing Market Assessment 2014/ (^8) Full notes found in Appendix 10 (^9) DTZ (2008) Exeter Retail Study

ranking in the first quartile. St Thomas district centre, Sidmouth, Honiton, and Seaton all rank in the second quartile of national retail centres.

Administrative area

2.3.16 The HMA has already been defined using the boundaries of four local authorities, so these are established as a baseline area for this study. During consultation to inform this study, Mid Devon District Council officers^10 stated that it has considered its functional linkages with North Devon, but has concluded that its most functional relationship is with Exeter. Mid Devon does not have a strong link northwards to Taunton, and sees Exeter as its hub for higher level services. Exeter City Council officers also stated that it cannot accommodate much further economic growth within the city boundaries, so is reliant on working with its neighbouring authorities to accommodate the future growth of the city.

2.3.17 In the final draft of the Regional Spatial Strategy (2008), 21 places were identified as Strategically Significant Cities and Towns (SSCTs) i.e. places which play a critical strategic role regionally or sub-regionally. They were chosen because they are a focal point for economic activity. In the area being considered, Exeter, Newton Abbot and Torquay are identified as SSCTs. This is helpful in emphasising the distinctive difference between Newton Abbott and Torquay. On balance, Newton Abbott is more Exeter-facing than it is Torbay-facing.

Catchment area for cultural and social facilities

2.3.18 There is limited information available on these factors. Most of the higher order cultural and social facilities are concentrated in Exeter: Exeter Phoenix Spacex Northcott Theatre Bike Shed Theatre Exeter Cathedral Exeter Quayside Royal Albert Memorial Museum

2.3.19 There is some data on the circulation areas of local newspapers (published by DC media) in the local area. The local titles are: The Express & Echo. The circulation area is centred around Exeter and covers as far as Tiverton, Exmouth, Honiton and villages in East Devon The Mid Devon Gazette series includes four newspapers covering Tiverton, Crediton, Culm Valley, Bampton, Dulverton and surrounding villages

- The Herald Express is centred on Torquay, and the circulation area includes Paignton, Newton Abbot, Brixham and other towns and villages in South Devon

(^10) Please note that these are the views of officers and not necessarily of elected members