1

HETEROSCEDASTICITY

The assumption of equal variance

Var(ui) = σ2, for all i, is called

homoscedasticity, which means

“equal scatter” (of the error terms

ui around their mean 0)

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Heteroscedasticity is a topic from Econometrics

Typology: Slides

1 / 29

This page cannot be seen from the preview

Don't miss anything!

The assumption of equal variance

Var(u i

) = σ

2 , for all i, is called

homoscedasticity, which means

“equal scatter” (of the error terms

u i

around their mean 0)

Consequences of ignoring

heteroscedasticity during the OLS

procedure

The estimates and forecasts based on

them will still be unbiased and

consistent

However, the OLS estimates are no

longer the best (B in BLUE) and thus

will be inefficient. Forecasts will also

be inefficient

i

i

i

2

j

i

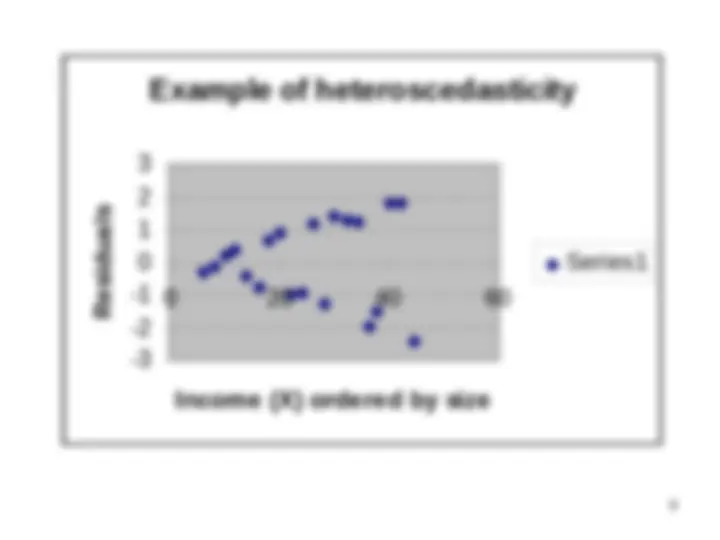

Example of heteroscedasticity

0

1

2

3

0 20 40 60

Income (X) ordered by size

Residuals

Series

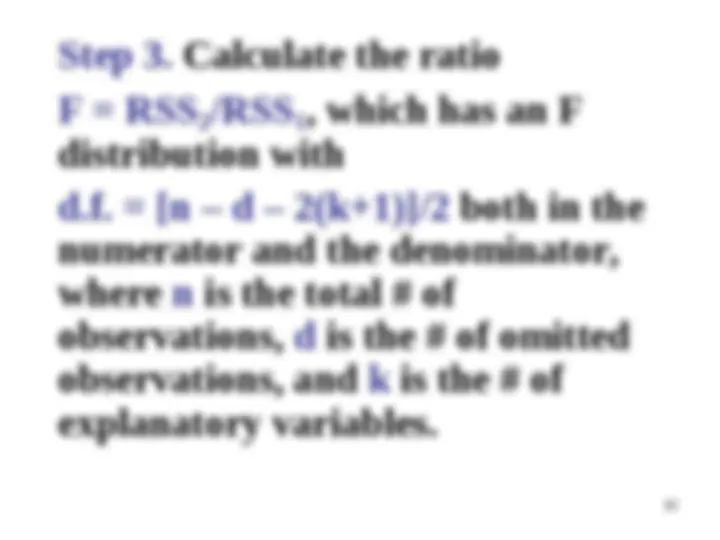

Step 3. Calculate the ratio

2

1

, which has an F

distribution with

d.f. = [n – d – 2(k+1)]/2 both in the

numerator and the denominator,

where n is the total # of

observations, d is the # of omitted

observations, and k is the # of

explanatory variables.

: All the variances

σ i

2 are equal (i.e., homoscedastic) if

cr

, where F cr

is found in the

table of the F distribution for

[n-d-2(k+1)]/2 d.f. and for a

predetermined level of significance

α, typically 5%.

(for large n>30)

The Breusch-Pagan test

Step 1. Run the regression of û i

2

on all the explanatory variables. In

our example (CN p. 37), there is

only one explanatory variable, X 1

,

therefore the model for the OLS

estimation has the form:

û i

2 = α 0

X 1i

Step 2. Keep the R

2 from this

regression. Let’s call it R û

2

Calculate either

(a) F = (R û

2 /k)/[(1-R û

2 )/(n-(k+1)],

where k is the # of explanatory

variables; the F statistic has an F

distribution with d.f. = [k, n-(k+1)]

Reject H 0

: All the variances σ i

2 are

equal (i.e., homoscedastic) if F >F cr

Drawbacks of the Breusch-

Pagan test

It has been shown to be

sensitive to any violation of the

normality assumption

Three other popular LM tests: the

Glejser test; the Harvey-Godfrey

test, and the Park test, are also

sensitive to such violations (won’t

be covered in this course)

Step 2. Compute the statistic

χ

2 = nR û

2 , where n is the sample size

and R û

2 is the unadjusted R-squared

from the OLS regression in Step 1. The

statistic χ

2 = nR û

2 , has an asymptotic

chi-square (χ

2 ) distrib. with d.f. = k,

where k is the # of ALL explanatory

variables in the AUXILIARY model.

Reject H 0

: All the variances σ i

2 are

equal (i.e., homoscedastic) if χ

2

χ cr

2

Estimation Procedures when H 0

is

rejected

proportional factor

If it can be assumed that the error variance is

proportional to the square of the indep. variable

X j

2 , we can correct for heteroscedasticity by

dividing every term of the regression by X 1i

and

then reestimating the model using the transformed

variables. In the two-variable case, we will have to

reestimate the following model (CN, p. 39):

Y i

/X 1i

= β 0

/X 1i

β 1

u i

/X 1i