Project One

1 CONT ENT S

1.1 Question 1

Based on empirical data, the probability of winning $80 is 100% in experiment

one. The calculation for this probability is the count of episodes ending with a $80

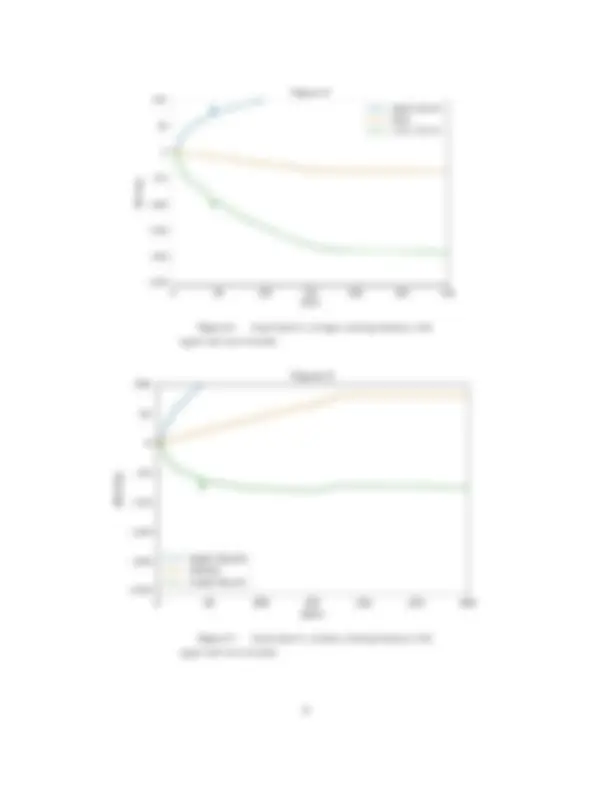

winning balance divided by the total episodes (1000). As shown in Figure 2, the

mean reaches $80 around 200.

1.2 Question 2

The expected value after 1000 spins for is 80. This value is the average winning

balance for all 1000 episodes held after 1000 spins. The expected value is

probability of each unique balance multiplied by the balance. Essentially this is a

weighted average of the winning balances based on the probability. As the

probability of each event is equal empirically, the expected value is merely a

simple average calculation across the episode results. The formula is as follows:

expected value =

∑

i=0

1000

Winning Balanc ei

1000

where i represents the spin.

1.3 Question 3

In experiment 1, the mean plus and minus standard deviation bands converge to

the mean after 200 spins. Convergence occurs due to the assumption of unlimited

bankroll and its implications on the standard deviation. As there is no loss limit,

there are large runs of continual losses creating a large amount of initial

variability as shown in Figure 6. However, the naïve code also assumes that there

are continuous funds to bet and eventually the strategy recovers from the

variability given enough spins to win. Therefore, the standard deviation

converges to zero as more and more episodes win which results in a convergence

of the upper and lower bands to the mean.

1.4 Question 4

In experiment 2, the probability of winning $80 after 1000 spins is 0.638. The

probability is calculated as the count of episodes where the 1000th spin held $80 as

the winning balance divided by the total episodes.

1