Download Hypothesis Testing in the Multiple regression model and more Schemes and Mind Maps Statistics in PDF only on Docsity!

Hypothesis Testing in the Multiple regression

model

Testing that individual coefficients take a specific value such aszero or some other value is done in exactly the same way aswith the simple two variable regression model.

Now suppose we wish to test that a number of coefficients orcombinations of coefficients take some particular value.

In this case we will use the so called “F-test”

Suppose for example we estimate a model of the form

We may wish to test hypotheses of the form {H0:

b

=0 and

b2=0 against the alternative that one or more are wrong} or{H0:

b

=1 and

b

b

=0 against the alternative that one or more

are wrong} or {H0:

b

b

=1 and

a

=0 against the alternative that

one or more are wrong}

This lecture is inference in this more general set up.

We will not outline the underlying statistical theory for this. Wewill just describe the testing procedure.

i i i i i i i

u X b X b X b X b X b a Y

5 5 4 4 3 3 2 2 1 1

Example 1

Suppose we want to test that :

H0:

b

=0 and b2=

against the

alternative that one or more are wrong in:

The above is the

unrestricted model

The

Restricted Model would be

i i i i i i i

u X b X b X b X b X b a Y

5 5 4 4 3 3 2 2 1 1

i

i

i

i

i

u X b X b X b a Y

5 5 4 4 3 3

Example 2

Suppose we want to test that :

H

b

=1 and

b

b

against the

alternative that one or more are wrong :

The above is the

unrestricted model

The

Restricted Model would be

Rearranging we get a model that uses new variables as functionsof the old ones:

i i i i i i i

u X b X b X b X b X b a Y

5 5 4 4 3 3 2 2 1 1

i i i i i i i

u X b X b X b X b X a Y

5 5 4 4 3 2 2 2 1

i i i i i i i

u X b X b X X b a X Y

5 5 4 4 3 2 2 1

)

(

)

(

Further Definitions

Define the

U

nrestricted R

esidual R

esidual S

um of S

quares (URSS)

as the residual sum of squares obtained from estimating theunrestricted model.

Define the

R

estricted R

esidual R

esidual S

um of S

quares (RRSS)

as

the residual sum of squares obtained from estimating the restrictedmodel.

Note that according to our argument above

Define the

degrees of freedom

as

N-k

where

N

is the sample size and

k

is the number of parameters estimated in the unrestricted model (I.e

under the alternative hypothesis)

Define by

q

the number of restrictions imposed (in both our examples

there were two restrictions imposed

URSS

RRSS

≥

The F-Statistic

The Statistic for testing the hypothesis we discussed is

The test statistic is always positive. We would like this to be“small”. The smaller the

F

-statistic the less the loss of fit due to

the restrictions

Defining “small” and using the statistic for inference we need toknow its distribution.

)

/(

/

)

(

K

N

URSS

q

URSS

RRSS

F

−

−

=

Since the smaller the test statistic the better and since the teststatistic is always positive we only have one critical value.

For a test at the

level of significance we choose a critical

value of

If the test statistic is below the critical value we accept the nullhypothesis.

Otherwise we reject.

α

k

N

q

F

α

Examples

Examples of Critical values for 5% tests in a regression modelwith 6 regressors under the alternative

- Sample size 18. One restriction to be tested: Degrees of

freedom 1, 12:

- Sample size 24. Two restrictions to be tested: degrees of

freedom 2, 18:

- Sample size 21. Three restrictions to be tested: degrees of

freedom 3, 15:

75

.

4

)

12 ,

1 ( ,

05 .

0

1

=

−

F

55

.

3

=

F

)

15 ,

3 ( ,

05 .

0

1

−

F

Examples

Examples of Critical values for 5% tests in a regression modelwith 6 regressors under the alternative. Inference based on large samples:

- One restriction to be tested: Degrees of freedom 1. :– Two restrictions to be tested: degrees of freedom 2:– Three restrictions to be tested: degrees of freedom 3:

84

.

3

=

χ

99

.

5

=

χ

81

.

7

=

χ

.

regr lbp lpbr lpsmr lryae ltba lrma

Source |

SS

df

MS

Number of obs =

F( 5,

Model |.

Prob > F

Residual |.

R-squared

Adj R-squared = 0.

Total |.

Root MSE

log butter purchases

lbp |

Coef.

Std. Err.

t

P>|t|

[95% Conf. Interval]

-------------+----------------------------------------------------------------log price of butter

lpbr | -.

log price of margarine

lpsmr |

log real income

lryae |

log butter advertising

ltba | -.

log margarine advertising

lrma | -.

Constant

_cons |

Unrestricted Model

Example: The Demand for butter:

Hypothesis to be tested

: Butter and margarine advertising do not change

demand and income elasticity of butter is one:

Three restrictions

The Test

The value of the test statistic is

The critical value for a 5% test wit (3,45) degrees of freedom is2.

We accept the null hypothesis

since 0.71<2.81.

F

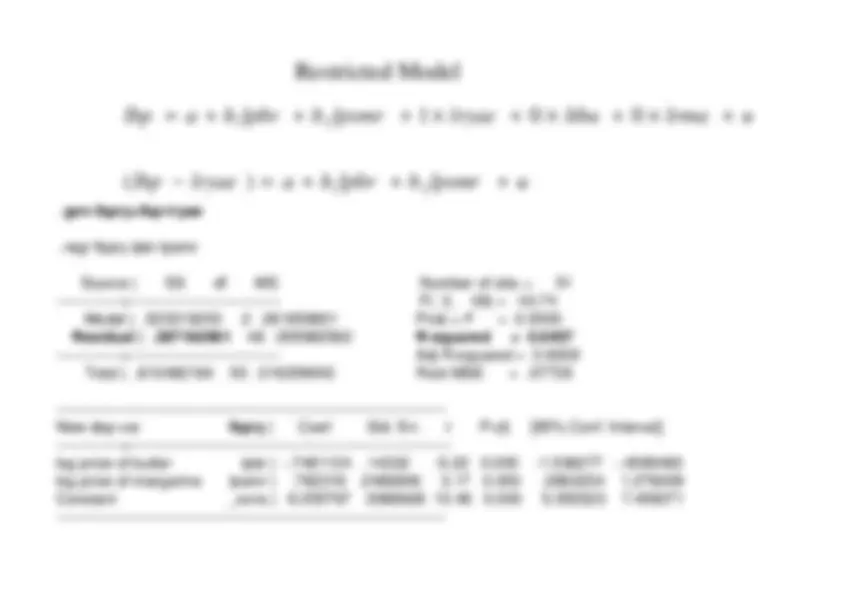

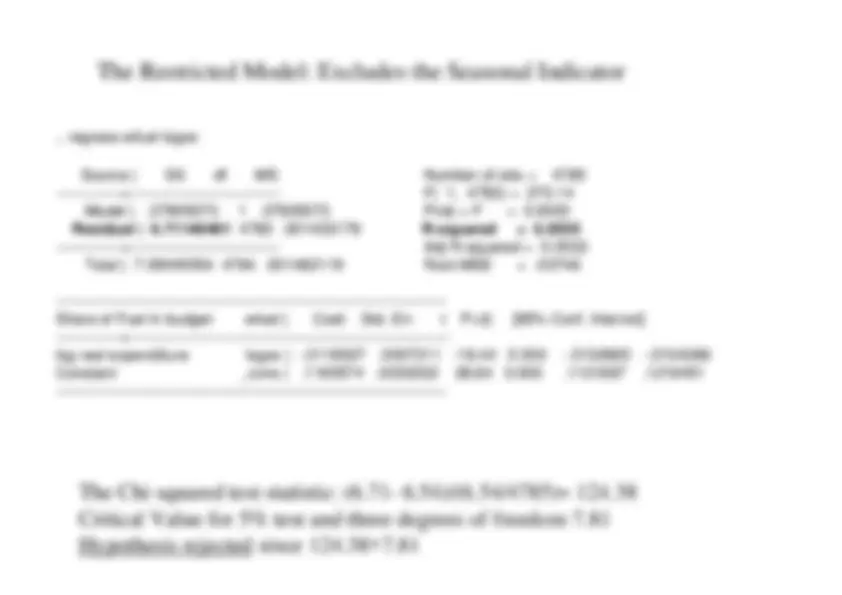

A Large sample example: Testing for seasonality in

fuel expenditure

Alternative form of the F-statistic using the R

squared

So long as the Total sum of squares is kept the same betweenmodels we can also write the F-statistic as

where U refers to the unrestricted model and R to the restrictedmodel

This will not work if we compute the R squared with differentdependent variables in each case (e.g. because oftransformations.

k

N

R

q

R

R

F

U

R

U

Heteroskedasticity

Heteroskedasticity means that the variance of the errors is notconstant across observations.

In particular the variance of the errors may be a function ofexplanatory variables.

Think of food expenditure for example. It may well be that the“diversity of taste” for food is greater for wealthier people thanfor poor people. So you may find a greater variance ofexpenditures at high income levels than at low income levels.