logo

Stat 709: Mathematical Statistics

Lecture 9

Jun Shao

Department of Statistics

University of Wisconsin

Madison, WI 53706, USA

Jun Shao (UW-Madison) Stat 709 Lecture 9 September 23, 2009 1 / 12

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Material Type: Notes; Professor: Shao; Class: Mathematical Statistics; Subject: STATISTICS; University: University of Wisconsin - Madison; Term: Fall 2009;

Typology: Study notes

1 / 19

This page cannot be seen from the preview

Don't miss anything!

logo

Jun Shao

Department of Statistics University of Wisconsin Madison, WI 53706, USA

logo

Let (Ω, F , P ) be a probability space. (i) Let C be a collection of subsets in F. Events in C are said to be independent iff for any positive integer n and distinct events A 1 ,..., An in C ,

P ( A 1 ∩ A 2 ∩ · · · ∩ An ) = P ( A 1 ) P ( A 2 ) · · · P ( An ).

(ii) Collections C i ⊂ F , i ∈ I (an index set that can be uncountable), are said to be independent iff events in any collection of the form { Ai ∈ C i : i ∈ I } are independent. (iii) Random elements Xi , i ∈ I , are said to be independent iff σ ( Xi ), i ∈ I , are independent.

logo

Let C i , i ∈ I , be independent collections of events. If each C i is a π-system ( A ∈ C i and B ∈ C i implies A ∩ B ∈ C i ), then σ (C i ), i ∈ I , are independent.

Random variables Xi , i = 1 , ..., k , are independent according to Definition 1.7 iff

F ( X 1 ,..., Xk )( x 1 , ..., xk ) = FX 1 ( x 1 ) · · · FXk ( xk ), ( x 1 , ..., xk ) ∈ R k

Take C i = {( a , b ] : a ∈ R, b ∈ R}, i = 1 , ..., k If X and Y are independent random vectors, then so are g ( X ) and h ( Y ) for Borel functions g and h. Two events A and B are independent iff P ( B | A ) = P ( B ), which means that A provides no information about the probability of the occurrence of B.

logo

Let X be a random variable with E | X | < ∞ and let Yi be random ki -vectors, i = 1 , 2. Suppose that ( X , Y 1 ) and Y 2 are independent. Then E [ X |( Y 1 , Y 2 )] = E ( X | Y 1 ) a.s.

First, E ( X | Y 1 ) is Borel on (Ω, σ ( Y 1 , Y 2 )), since σ ( Y 1 ) ⊂ σ ( Y 1 , Y 2 ). Next, we need to show that for any Borel set B ∈ B k^1 + k^2 , ∫

( Y 1 , Y 2 )−^1 ( B )

XdP =

∫

( Y 1 , Y 2 )−^1 ( B )

E ( X | Y 1 ) dP.

If B = B 1 × B 2 , where Bi ∈ B ki^ , then

( Y 1 , Y 2 )−^1 ( B ) = Y (^) 1 − 1 ( B 1 ) ∩ Y (^) 2 − 1 ( B 2 )

logo

and ∫

Y (^) 1 − 1 ( B 1 )∩ Y (^) 2 − 1 ( B 2 )

E ( X | Y 1 ) dP =

∫ IY − 1 1 ( B^1 )

2 ( B^2 ) E ( X | Y 1 ) dP

∫ IY − 1 1 ( B^1 ) E ( X | Y 1 ) dP

∫ IY − 1 2 ( B^2 ) dP

=

∫ IY (^) 1 − 1 ( B 1 ) XdP

∫ IY (^) 2 − 1 ( B 2 ) dP

=

∫ IY (^) 1 − 1 ( B 1 ) IY (^) 2 − 1 ( B 2 ) XdP

=

∫

Y (^) 1 − 1 ( B 1 )∩ Y (^) 2 − 1 ( B 2 )

XdP ,

where the second and the next to last equalities follow the independence of ( X , Y 1 ) and Y 2 , and the third equality follows from the fact that E ( X | Y 1 ) is the conditional expectation of X given Y 1. This shows that the result for B = B 1 × B 2. Note that B k^1 × B k^2 is a π-system.

logo

We can show that the following collection is a λ -system:

H =

B ⊂ R k^1 + k^2 :

∫

( Y 1 , Y 2 )−^1 ( B )

XdP =

∫

( Y 1 , Y 2 )−^1 ( B )

E ( X | Y 1 ) dP

Since we have already shown that B k^1 × B k^2 ⊂ H , B k^1 + k^2 = σ (B k^1 × B k^2 ) ⊂ H and thus the result follows.

The result in Proposition 1.11 still holds if X is replaced by h ( X ) for any Borel h and, hence, P ( A | Y 1 , Y 2 ) = P ( A | Y 1 ) a.s. for any A ∈ σ ( X ), (1) if ( X , Y 1 ) and Y 2 are independent. We say that given Y 1 , X and Y 2 are conditionally independent iff (1) holds. Proposition 1.11 can be stated as: if Y 2 and ( X , Y 1 ) are independent, then given Y 1 , X and Y 2 are conditionally independent.

logo

For random vectors X and Y , is P [ X −^1 ( B )| Y = y ] a probability measure for given y? Problem: P [ X −^1 ( B )| Y = y ] is defined a.s.

Let X be a random n -vector on a probability space (Ω, F , P ) and A be a sub-σ -field of F. Then there exists a function P ( B , ω) on B n^ × Ω such that

(a) P ( B , ω) = P [ X −^1 ( B )|A ] a.s. for any fixed B ∈ B n , and (b) P (·, ω) is a probability measure on (R n , B n ) for any fixed ω ∈ Ω.

Let Y be measurable from (Ω, F , P ) to (Λ, G ). Then there exists PX | Y ( B | y ) such that

(a) PX | Y ( B | y ) = P [ X −^1 ( B )| Y = y ] a.s. PY for any fixed B ∈ B n , and (b) PX | Y (·| y ) is a probability measure on (R n , B n ) for any fixed y ∈ Λ.

Furthermore, if E | g ( X , Y )| < ∞ with a Borel function g , then

E [ g ( X , Y )| Y = y ] = E [ g ( X , y )| Y = y ] =

∫

R n

g ( x , y ) dPX | Y ( x | y ) a.s. PY.

logo

For random vectors X and Y , is P [ X −^1 ( B )| Y = y ] a probability measure for given y? Problem: P [ X −^1 ( B )| Y = y ] is defined a.s.

Let X be a random n -vector on a probability space (Ω, F , P ) and A be a sub-σ -field of F. Then there exists a function P ( B , ω) on B n^ × Ω such that

(a) P ( B , ω) = P [ X −^1 ( B )|A ] a.s. for any fixed B ∈ B n , and (b) P (·, ω) is a probability measure on (R n , B n ) for any fixed ω ∈ Ω.

Let Y be measurable from (Ω, F , P ) to (Λ, G ). Then there exists PX | Y ( B | y ) such that

(a) PX | Y ( B | y ) = P [ X −^1 ( B )| Y = y ] a.s. PY for any fixed B ∈ B n , and (b) PX | Y (·| y ) is a probability measure on (R n , B n ) for any fixed y ∈ Λ.

Furthermore, if E | g ( X , Y )| < ∞ with a Borel function g , then

E [ g ( X , Y )| Y = y ] = E [ g ( X , y )| Y = y ] =

∫

R n

g ( x , y ) dPX | Y ( x | y ) a.s. PY.

logo

For a fixed y , PX | Y = y = PX | Y (·| y ) is called the conditional distribution of X given Y = y.

If Y ∈ R m^ is selected in stage 1 of an experiment according to its marginal distribution PY = P 1 , and X is chosen afterward according to a distribution P 2 (·, y ), then the combined two-stage experiment produces a jointly distributed pair ( X , Y ) with distribution P ( X , Y ) given by (2) and PX | Y = y = P 2 (·, y ). This provides a way of generating dependent random variables.

A market survey is conducted to study whether a new product is preferred over the product currently available in the market (old product).

logo

For a fixed y , PX | Y = y = PX | Y (·| y ) is called the conditional distribution of X given Y = y.

If Y ∈ R m^ is selected in stage 1 of an experiment according to its marginal distribution PY = P 1 , and X is chosen afterward according to a distribution P 2 (·, y ), then the combined two-stage experiment produces a jointly distributed pair ( X , Y ) with distribution P ( X , Y ) given by (2) and PX | Y = y = P 2 (·, y ). This provides a way of generating dependent random variables.

A market survey is conducted to study whether a new product is preferred over the product currently available in the market (old product).

logo

The survey is conducted by mail. Questionnaires are sent along with the sample products (both new and old) to N customers randomly selected from a population, where N is a positive integer. Each customer is asked to fill out the questionnaire and return it. Responses from customers are either 1 (new is better than old) or 0 (otherwise). Some customers, however, do not return the questionnaires. Let X be the number of ones in the returned questionnaires. What is the distribution of X?

If every customer returns the questionnaire, then (from elementary probability) X has the binomial distribution Bi ( p , N ) in Table 1. (assuming that the population is large enough so that customers respond independently), where p ∈ ( 0 , 1 ) is the overall rate of customers who prefer the new product.

logo

The survey is conducted by mail. Questionnaires are sent along with the sample products (both new and old) to N customers randomly selected from a population, where N is a positive integer. Each customer is asked to fill out the questionnaire and return it. Responses from customers are either 1 (new is better than old) or 0 (otherwise). Some customers, however, do not return the questionnaires. Let X be the number of ones in the returned questionnaires. What is the distribution of X?

If every customer returns the questionnaire, then (from elementary probability) X has the binomial distribution Bi ( p , N ) in Table 1. (assuming that the population is large enough so that customers respond independently), where p ∈ ( 0 , 1 ) is the overall rate of customers who prefer the new product.

logo

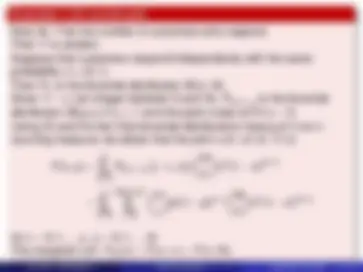

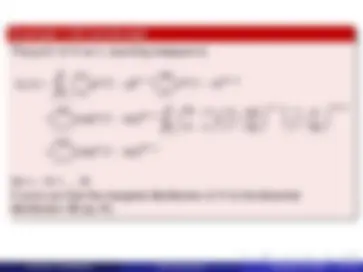

The p.d.f. of X w.r.t. counting measure is

fX ( x ) =

N

k = x

k x

px^ ( 1 − p ) k − x

k

π k^ ( 1 − π) N − k

x

( π p ) x^ ( 1 − π p ) N − x^

N

k = x

N − x k − x

π − π p 1 − π p

) k − x ( 1 − π 1 − π p

) N − k

x

( π p ) x^ ( 1 − π p ) N − x

for x = 0 , 1 , ..., N. It turns out that the marginal distribution of X is the binomial distribution Bi ( π p , N ).