Intercompany Profit Transactions -

Inventories

Patriani Wahyu Dewanti, S.E., M.Acc.

Accounting Department

Faculty of Economics

Yogyakarta State University

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

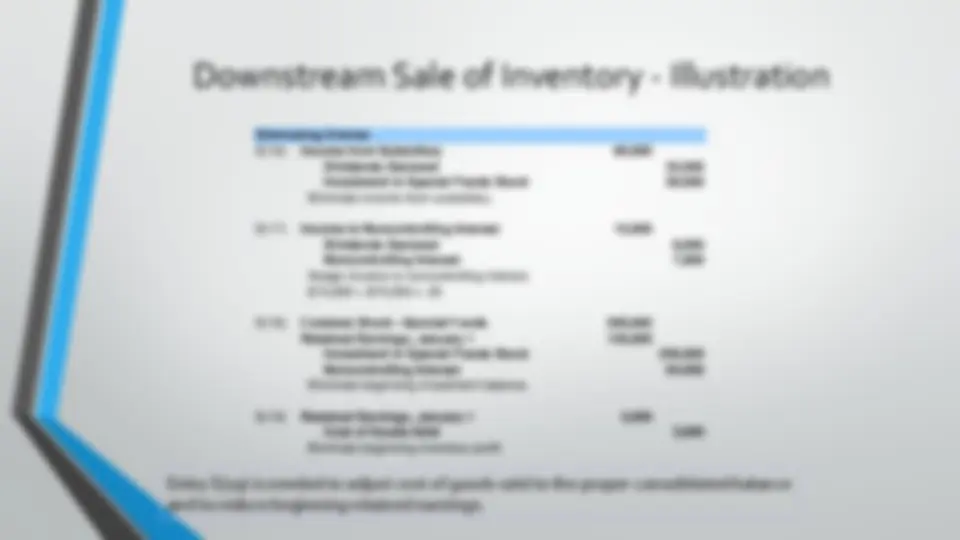

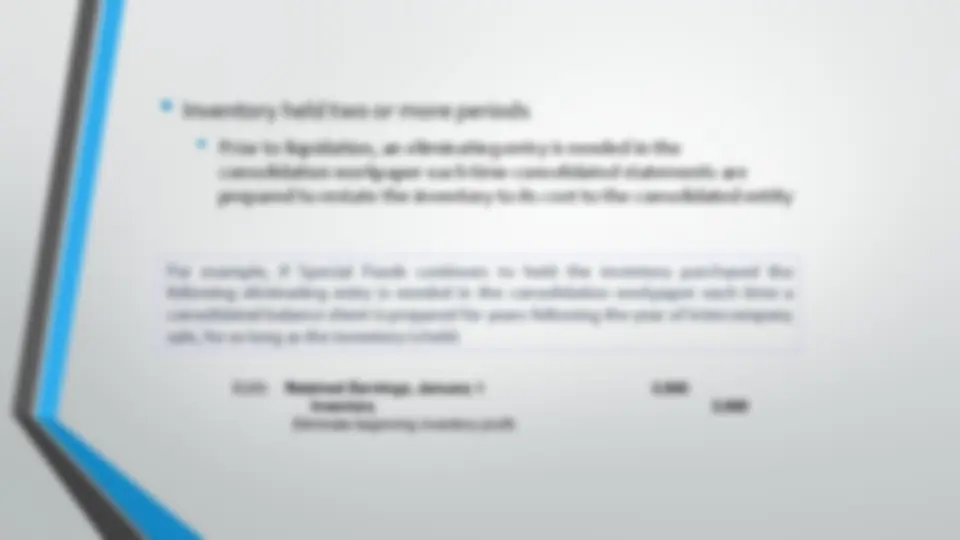

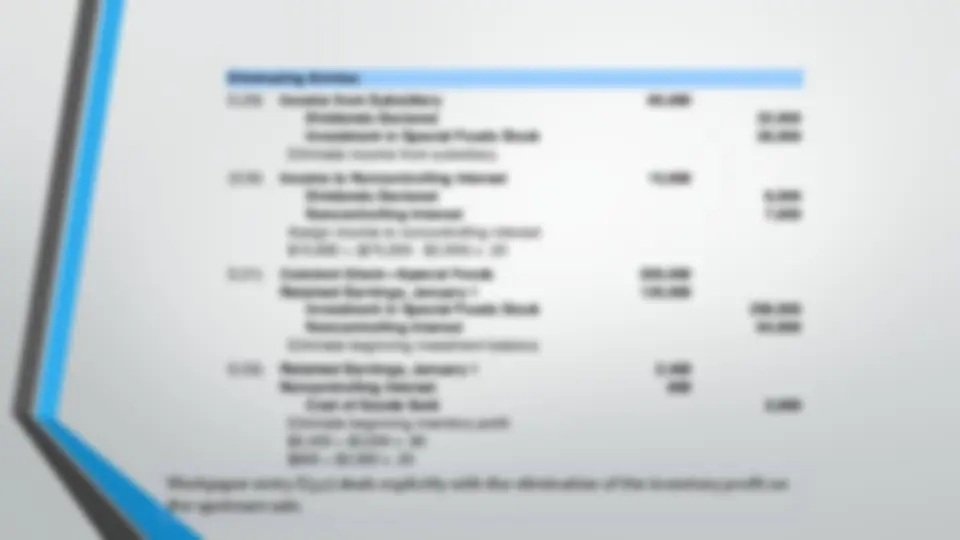

Entry E(19) is needed to adjust cost of goods sold to the proper consolidated balance and to reduce beginning retained earnings. Page 19. Downstream Sale of ...

Typology: Study notes

1 / 35

This page cannot be seen from the preview

Don't miss anything!

GENERAL OVERVIEW

Transfers at cost

Transfers at a profit or loss

Effect of type of inventory system

DOWNSTREAM SALE OF INVENTORY

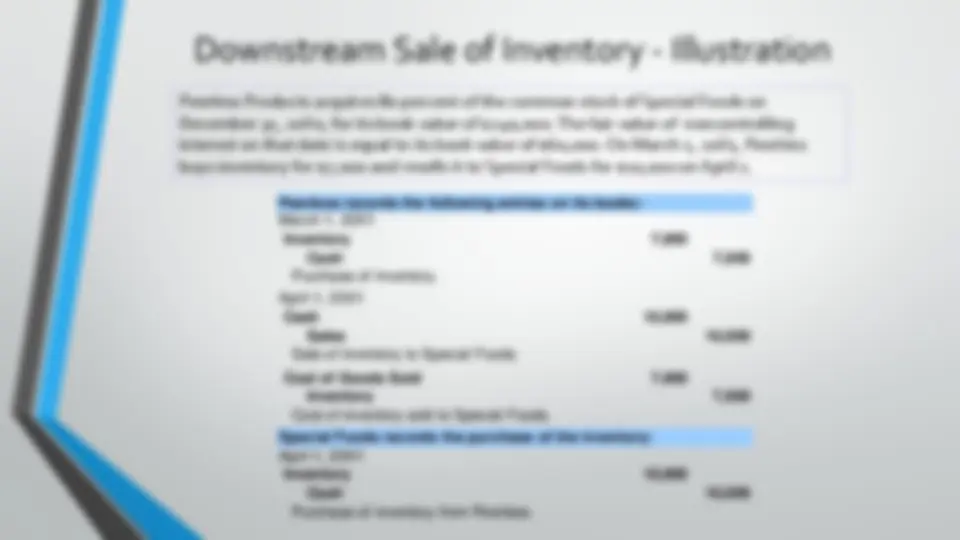

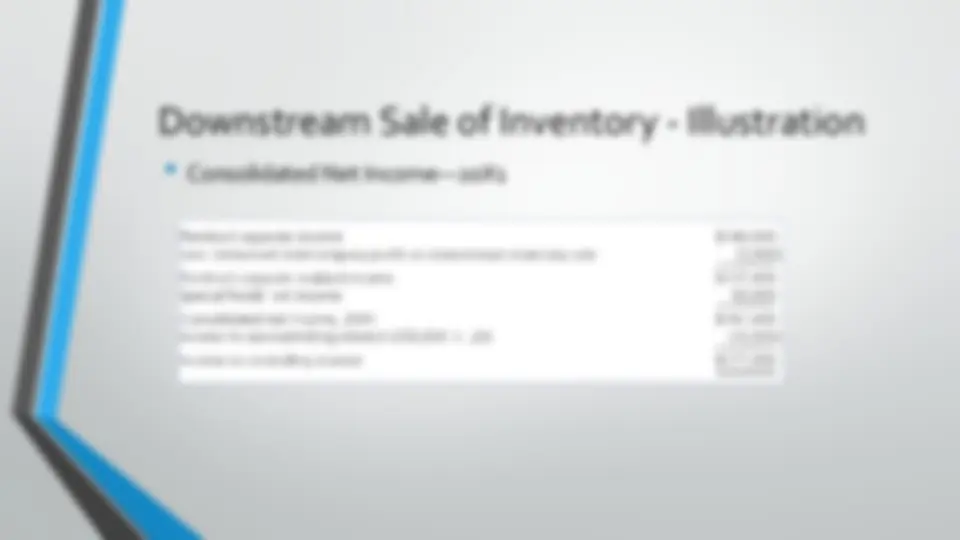

Downstream Sale of Inventory - Illustration

Downstream Sale of Inventory - Illustration

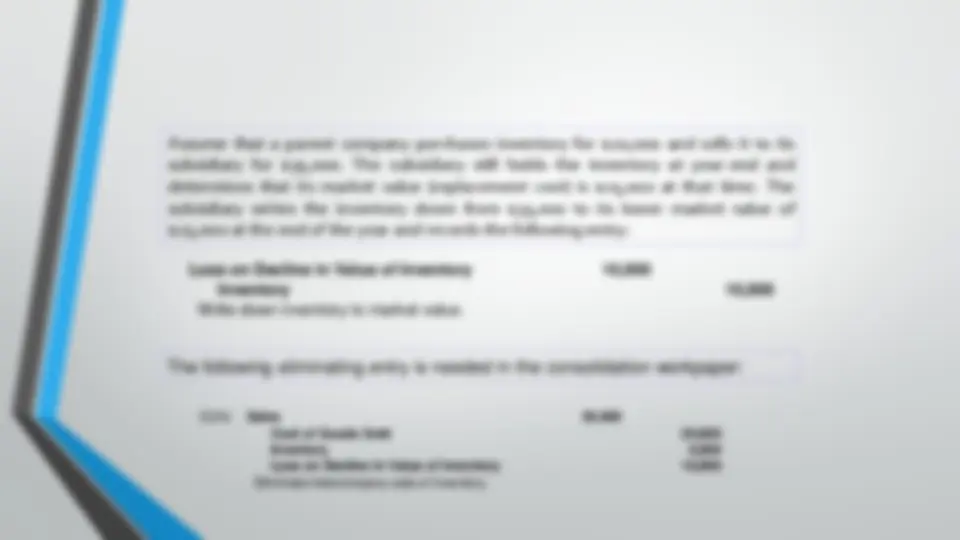

Special Foods records the sale: November 5, 20X Cash 15, Sales 15, Sale of inventory to Nonaffiliated. Cost of Goods Sold 10, Inventory 10, Cost of inventory sold to Nonaffiliated. Eliminating Entry: Sales 10, Cost of Goods Sold 10, Eliminate intercompany inventory sale.

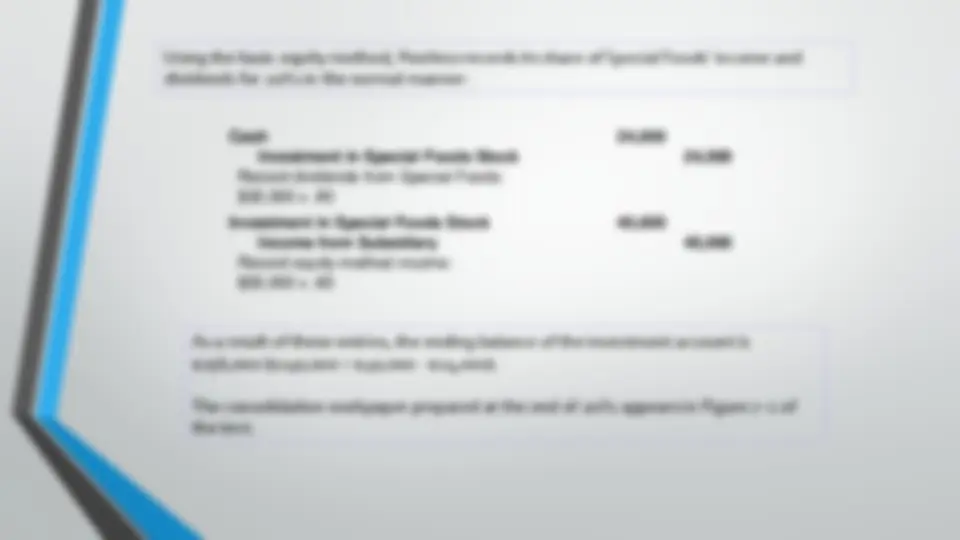

Cash 24, Investment in Special Foods Stock 24, Record dividends from Special Foods: $30,000 x. Investment in Special Foods Stock 40, Income from Subsidiary 40, Record equity-method income: $50,000 x. Using the basic equity method, Peerless records its share of Special Foods’ income and dividends for 20X1 in the normal manner: As a result of these entries, the ending balance of the investment account is $256,000 ($240,000 + $40,000 - $24,000). The consolidation workpaper prepared at the end of 20X1 appears in Figure 7–1 of the text.

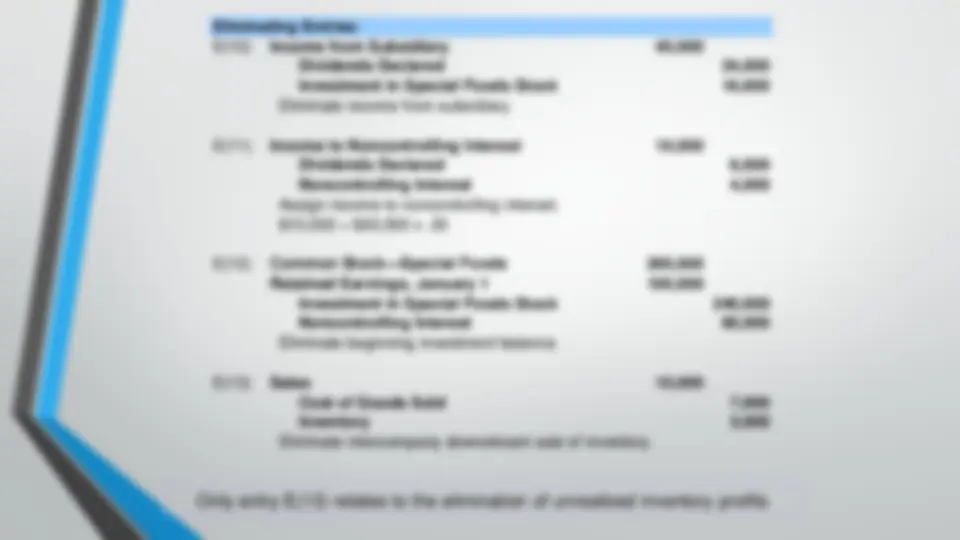

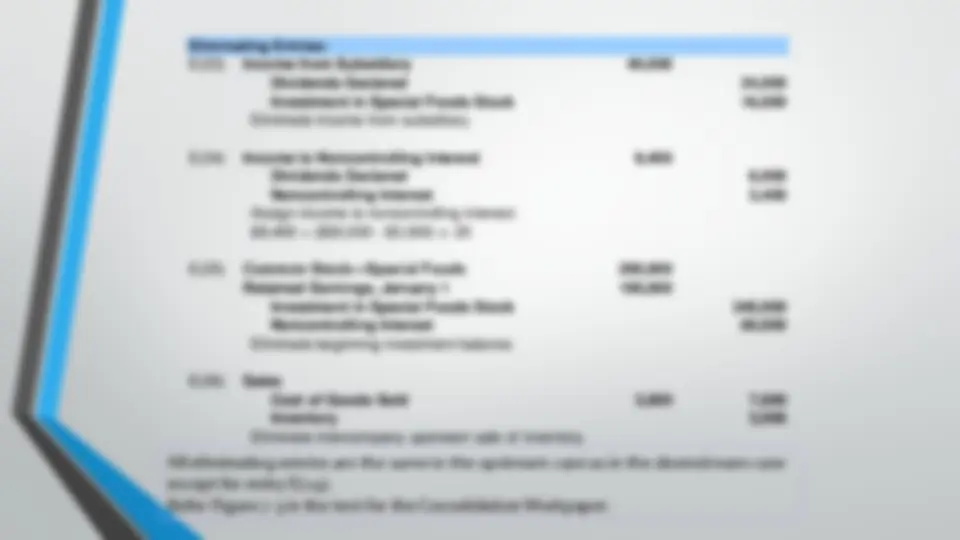

Eliminating Entries: E(10) Income from Subsidiary 40, Dividends Declared 24, Investment in Special Foods Stock 16, Eliminate income from subsidiary. E(11) Income to Noncontrolling Interest 10, Dividends Declared 6, Noncontrolling Interest 4, Assign income to noncontrolling interest. $10,000 = $50,000 x. E(12) Common Stock—Special Foods 200, Retained Earnings, January 1 100, Investment in Special Foods Stock 240, Noncontrolling Interest 60, Eliminate beginning investment balance. E(13) Sales 10, Cost of Goods Sold 7, Inventory 3, Eliminate intercompany downstream sale of inventory. Only entry E(13) relates to the elimination of unrealized inventory profits

Cash 32, Investment in Special Foods Stock 32, Record dividends from Special Foods: $40,000 x. Investment in Special Foods Stock 60, Income from Subsidiary 60, Record equity-method income: $75,000 x. During 20X2, Special Foods receives $15,000 when it sells to Nonaffiliated Corporation the inventory that it had purchased for $10,000 from Peerless in 20X1. Also, Peerless records its pro rata portion of Special Foods’ net income and dividends for 20X2 with the normal basic equity-method entries: The consolidation workpaper prepared at the end of 20X2 is shown in Figure 7–2 in the text. Four elimination entries are needed:

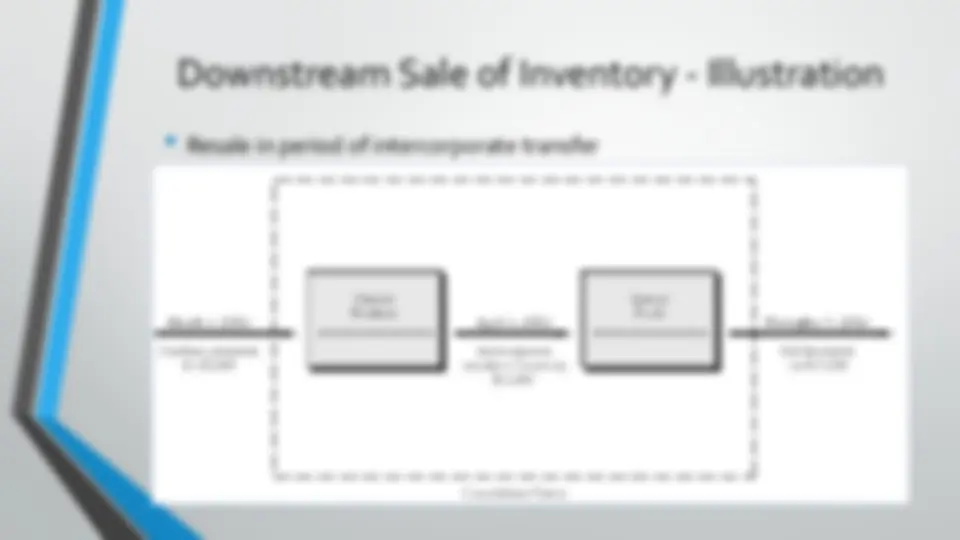

Downstream Sale of Inventory - Illustration

Downstream Sale of Inventory - Illustration