Loan

Receivable

and

Impairmen

t

MSG- G SC

AY 2020-2021

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

This is about intermediate accounting.

Typology: Exercises

1 / 13

This page cannot be seen from the preview

Don't miss anything!

MSG- GSC AY 2020-

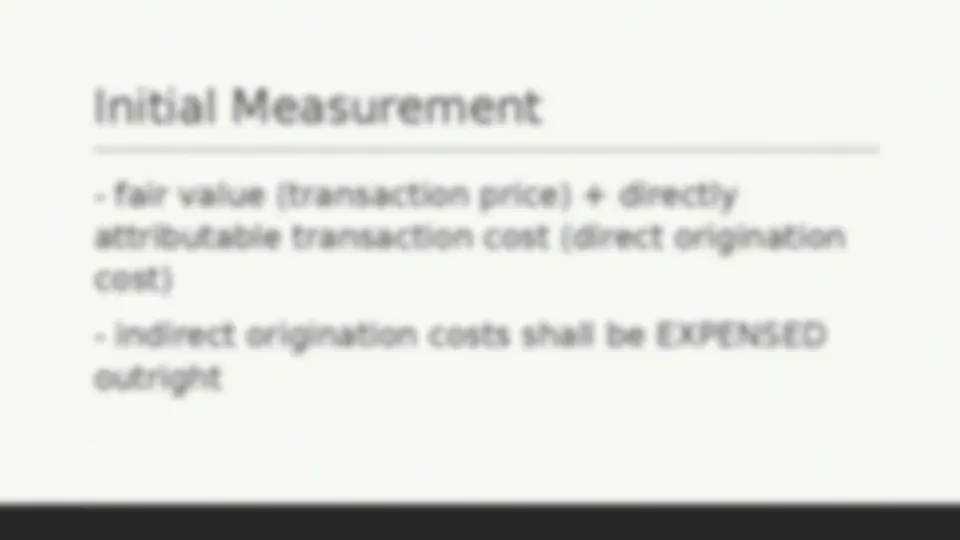

Origination Fees

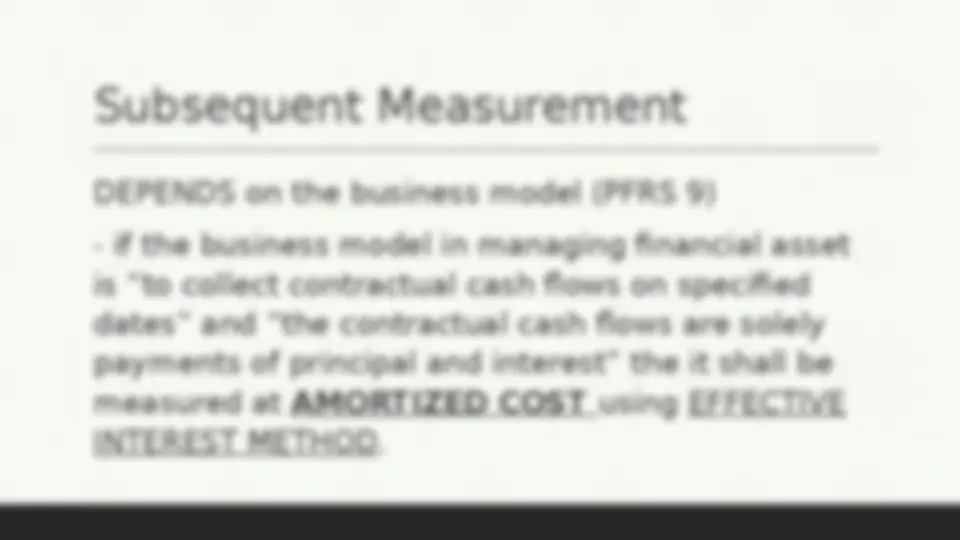

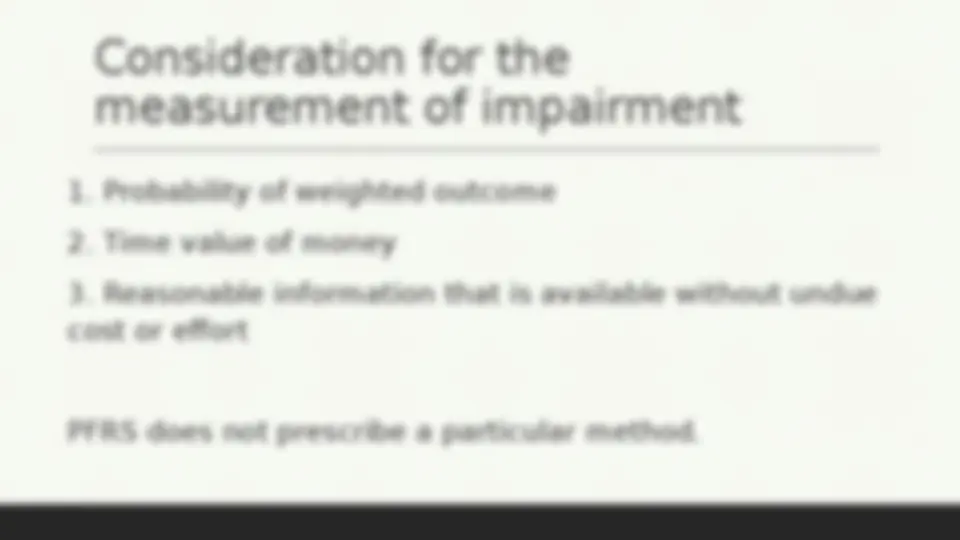

PFRS 9 provides that an entity shall recognize a loss allowance for expected credit losses on financial asset measured at amortized cost. The entity shall measure the loss allowance for a financial instrument at an amount equal to the lifetime expected credit losses if there is a significant increase since initial recognition. Credit loss are the present value of all cash shortfalls.

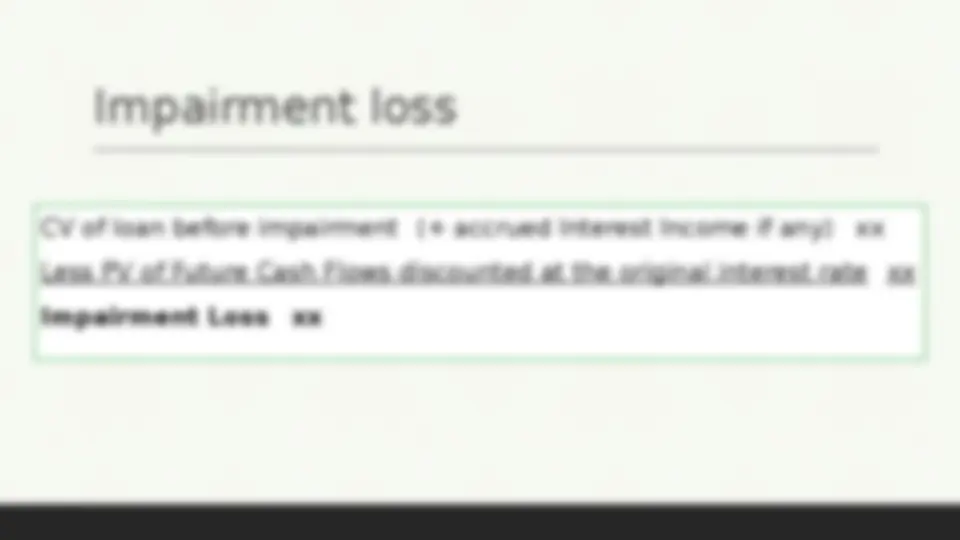

CV of loan before impairment (+ accrued Interest Income if any) xx Less PV of Future Cash Flows discounted at the original interest rate xx Impairment Loss xx

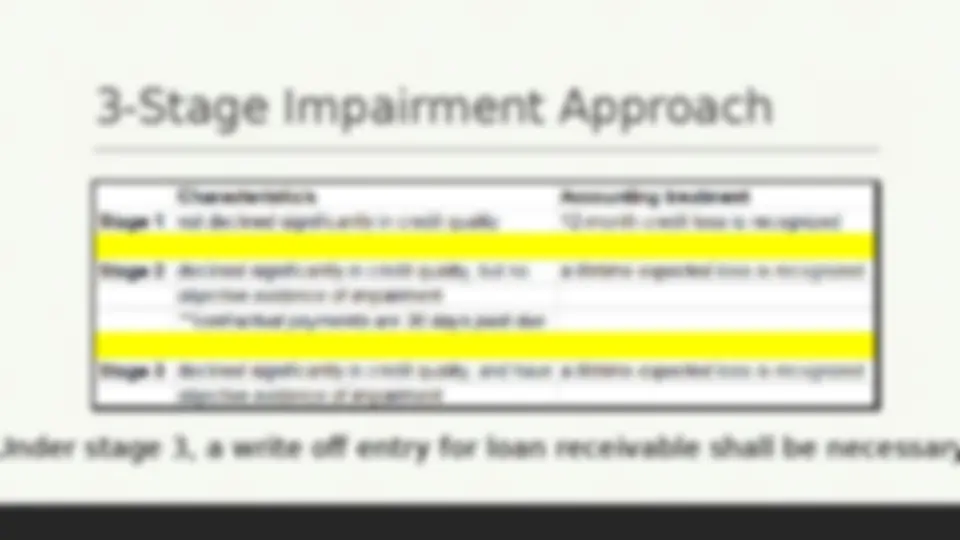

Under stage 3, a write off entry for loan receivable shall be necessary

Interest Income Under Each Stage Characteristic/s Accounting treatment Interest Income is recognized based on Stage 1 not declined significantly in credit quality 12-month credit loss is recognized GROSS CV (GCV) or FACE AMOUNT (FA) Stage 2 declined significantly in credit quality, but no objective evidence of impairment **contractual payments are 30 days past due a lifetime expected loss is recognized GROSS CV (GCV) or FACE AMOUNT (FA) Stage 3 declined significantly in credit quality, and have objective evidence of impairment a lifetime expected loss is recognized NET Carrying Amount (GCV or FA minus Allow. For Credit Loss)