Internal Controls

Training

1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

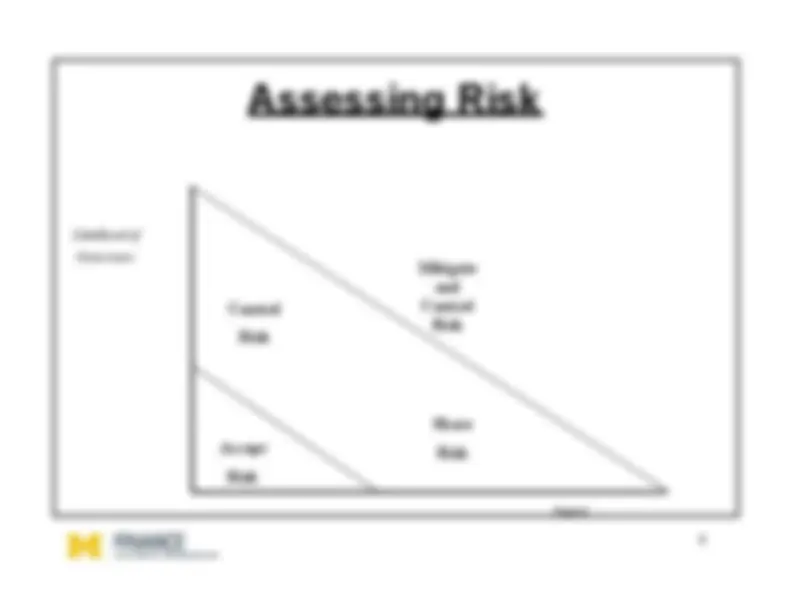

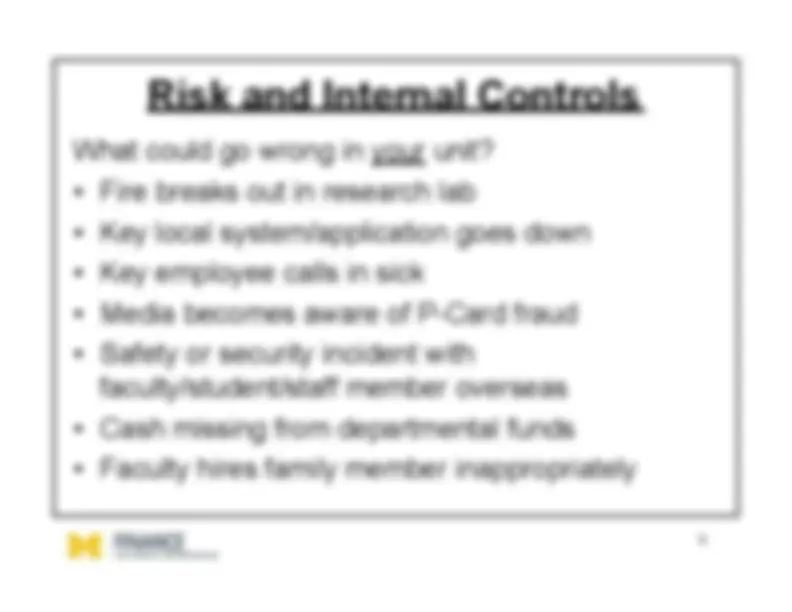

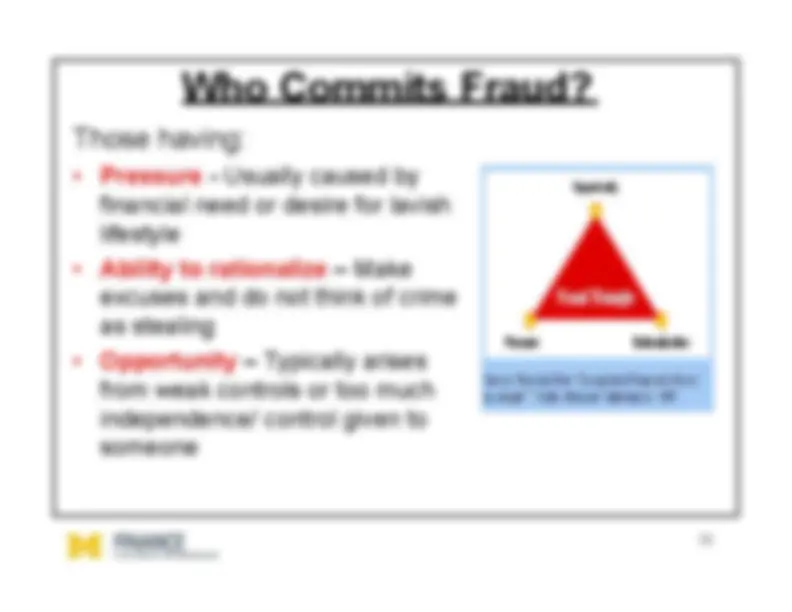

Risk and Internal Controls. Questions to ask yourself: • What can go wrong? • How could someone steal from us? • What policies are we most affected by?

Typology: Exams

1 / 30

This page cannot be seen from the preview

Don't miss anything!

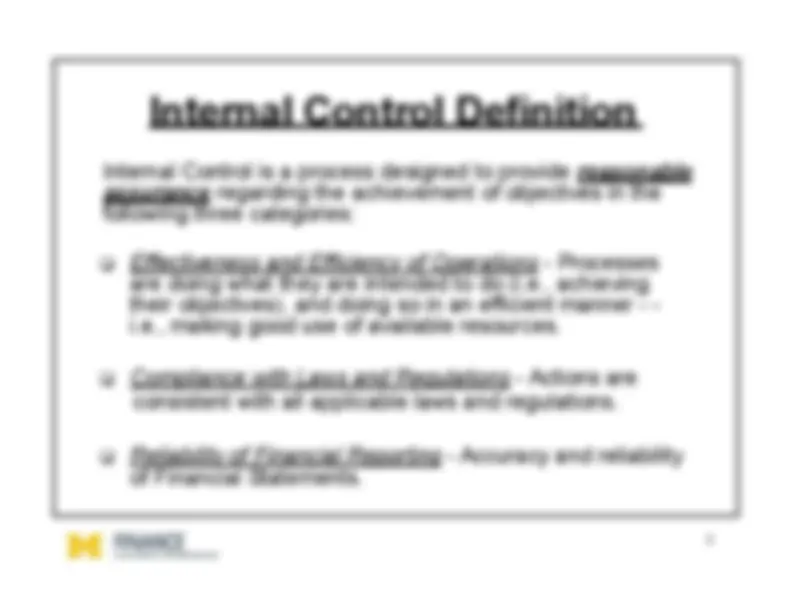

Internal Controls?

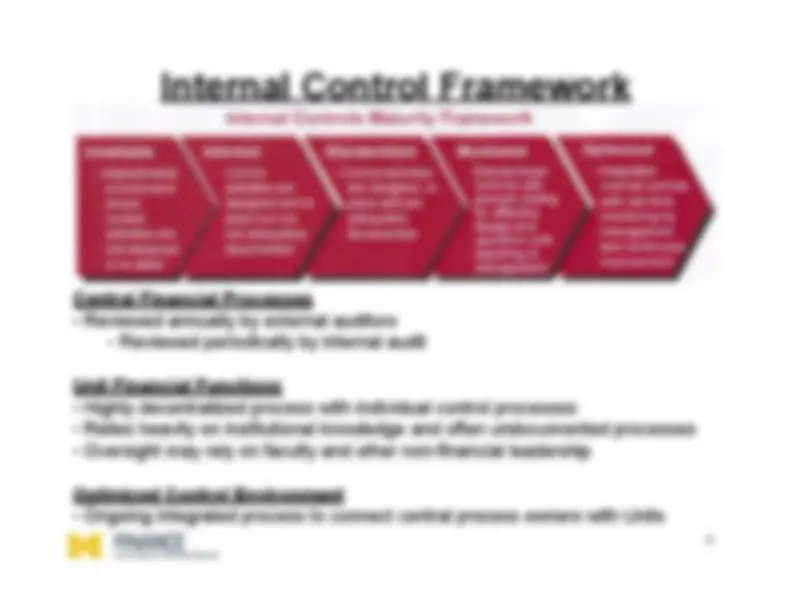

Internal Control Framework

Central Financial Processes • Reviewed annually by external auditors

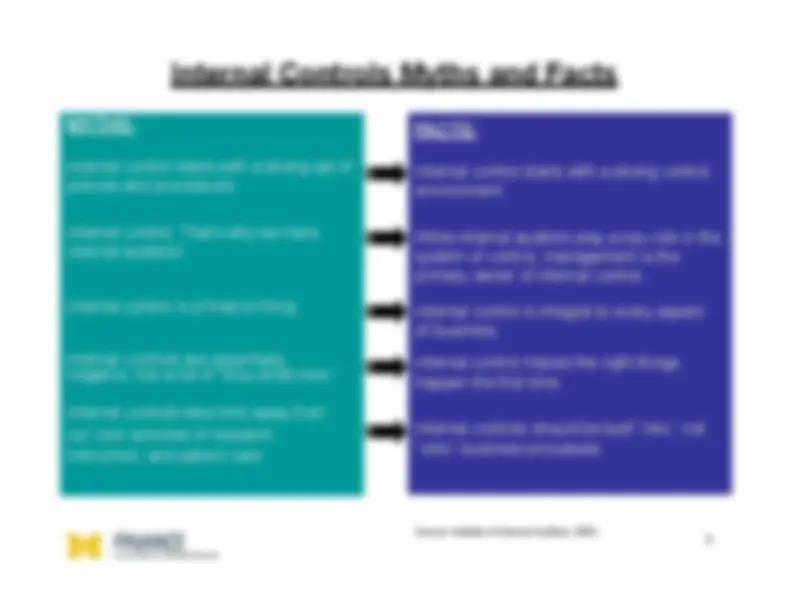

Internal Controls Myths and Facts

MYTHS:Internal control starts with a strong set ofpolicies and procedures.Internal control: That’s why we haveinternal auditors!Internal control is a finance thing.Internal controls are essentiallynegative, like a list of “thou-shalt-nots.”Internal controls take time away fromour core activities of research,instruction, and patient care.

FACTS:Internal control starts with a strong controlenvironment.While internal auditors play a key role in thesystem of control, management is theprimary owner of internal control.Internal control is integral to every aspectof business.Internal control makes the right thingshappen the first time.Internal controls should be built “into,” not“onto” business processes.Source: Institute of Internal Auditors, 2003

Questions to ask yourself:•^

What can go wrong?

-^

How could someone steal from us?

-^

What policies are we most affected by?

-^

What types of transactions in our area providethe greatest risk?

-^

How can someone bypass the internal controls?

-^

What potential risk areas could cause adversepublicity?

Likelihood ofOccurrence

Impact

AcceptRisk

Mitigate

and ControlRisk

ControlRisk

ShareRisk

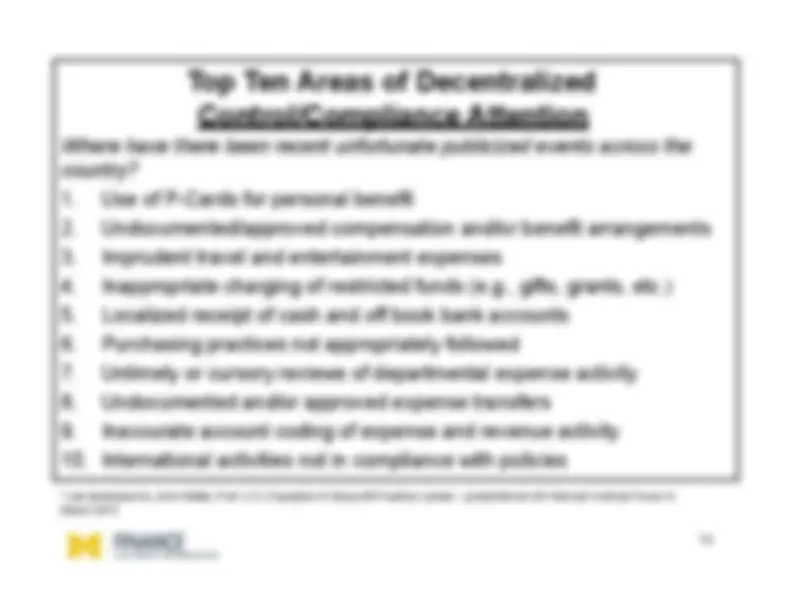

Top Ten Areas of DecentralizedControl/Compliance Attention

Where have there been recent unfortunate publicized events across thecountry? 1.

Use of P-Cards for personal benefit

Undocumented/approved compensation and/or benefit arrangements

Imprudent travel and entertainment expenses

Inappropriate charging of restricted funds (e.g., gifts, grants, etc.)

Localized receipt of cash and off book bank accounts

Purchasing practices not appropriately followed

Untimely or cursory reviews of departmental expense activity

Undocumented and/or approved expense transfers

Inaccurate account coding of expense and revenue activity

International activities not in compliance with policies

matching PO before paying an invoice

-^

statement

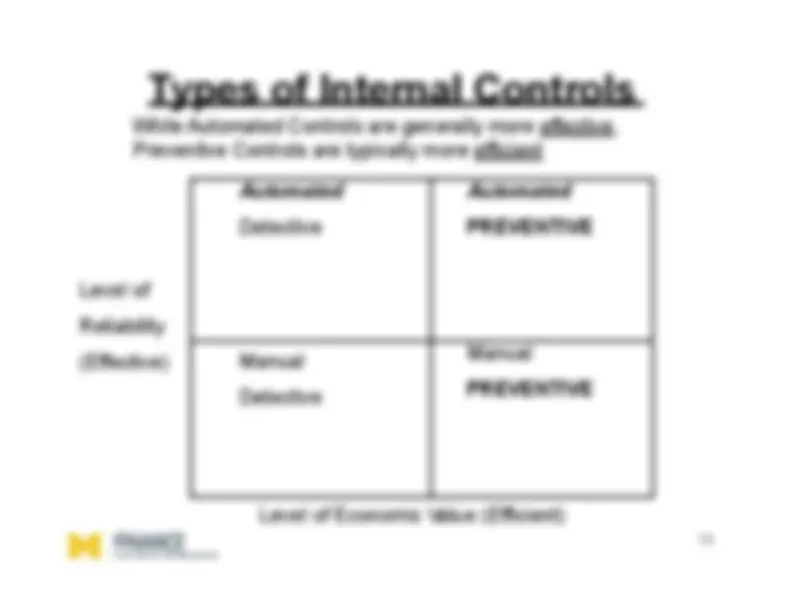

Level ofReliability(Effective)

Level of Economic Value (Efficient)

While Automated Controls are generally more effective,Preventive Controls are typically more efficient

Automated Detective

Automated PREVENTIVE

ManualDetective

Manual PREVENTIVE

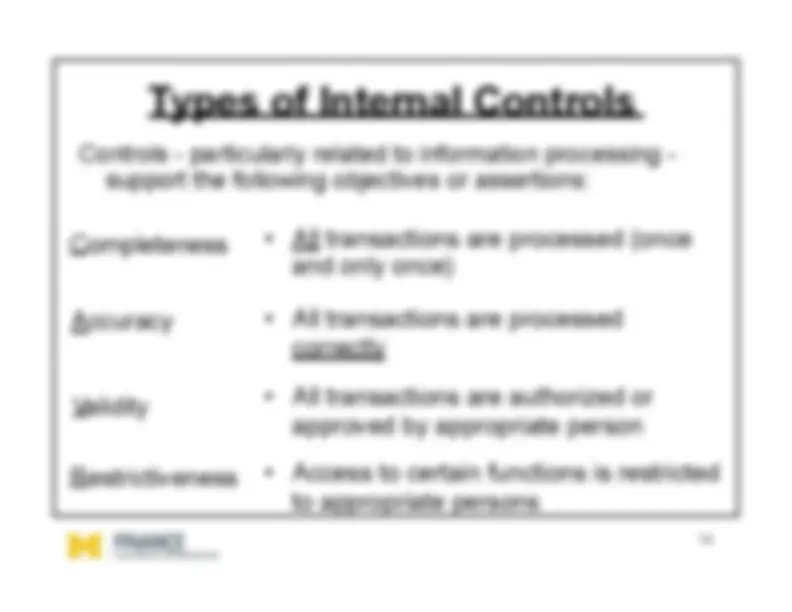

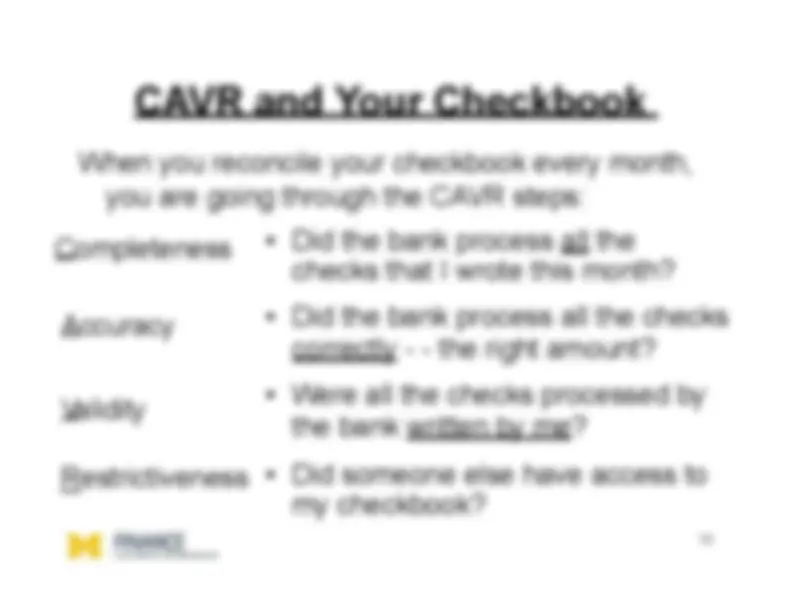

Controls - particularly related to information processing -

support the following objectives or assertions: Completeness

-^

All transactions are processed (onceand only once)

Accuracy

-^

All transactions are processedcorrectly

Validity

-^

All transactions are authorized orapproved by appropriate person

-^

Access to certain functions is restrictedto appropriate persons

Restrictiveness

CAVR and the Gross Pay Register

Completeness

All employees that should be in aunit, are in the unit

-^

The pay for a new hire starting inthe middle of a month is correct

-^

Additional pay was approved byappropriate personPerson processing changes in payis not reconciling GPR

AccuracyValidityRestrictiveness •

ManualControls

Preventive

Detective

Preventive

Detective

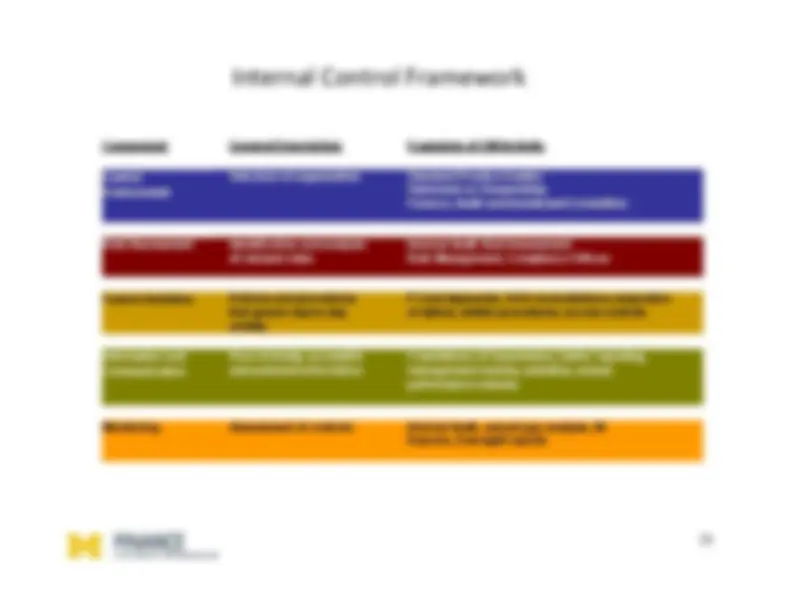

The Five Components of a Strong

Internal Control Framework

Control Activities

^ Policies/procedures that ensuremanagement directives arecarried out. ^ Range of activities includingapprovals, authorizations,verifications, recommendations,performance reviews, assetsecurity and segregation ofduties.

Monitoring

^ Assessment of a control system’sperformance over time. ^ Combination of ongoing andseparate evaluation. ^ Management and supervisoryactivities. ^ Internal audit activities.

Control Environment ^ Sets tone of organization-influencing control consciousnessof its people. ^ Factors include integrity, ethicalvalues, competence, authority,responsibility. ^ Foundation for all othercomponents of control.

Information and Communication ^ Pertinent information identified,captured and communicated in atimely manner. ^ Access to internal and externallygenerated information. ^ Flow of information that allows forsuccessful control actions frominstructions on responsibilities tosummary of findings formanagement action.

Risk Assessment

^ Risk assessment is theidentification and analysis ofrelevant risks to achieving theentity’s objectives-forming thebasis for determining controlactivities.

All five components must be in place for internal control to be effective.

Component

General Description

Examples of UM Activity

ControlEnvironment

Sets tone of organization

Standard Practice GuidesStatement on StewardshipFinance, Audit and Investment Committee

Risk Assessment

Identification and analysisof relevant risks

Internal Audit Risk AssessmentRisk Management, Compliance Offices

Control Activities

Policies and proceduresthat govern day-to-dayactivity

P-Card Approvals, SOA reconciliations, separationof duties, written procedures, access controls

Information andCommunication

Flow of timely, accessibleand pertinent information

Foundations of Supervision, metric reporting,management reviews, websites, annualperformance reviews

Monitoring

Assessment of controls

Internal Audit, annual gap analysis, M-Reports, Oversight reports

Internal

Control Framework