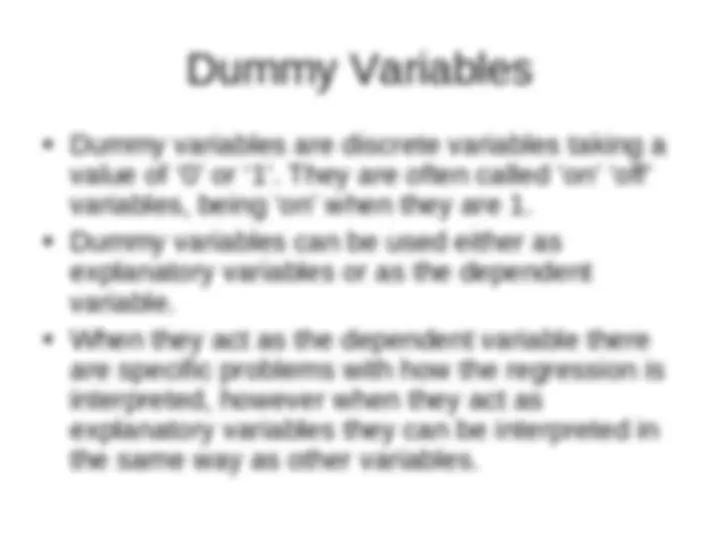

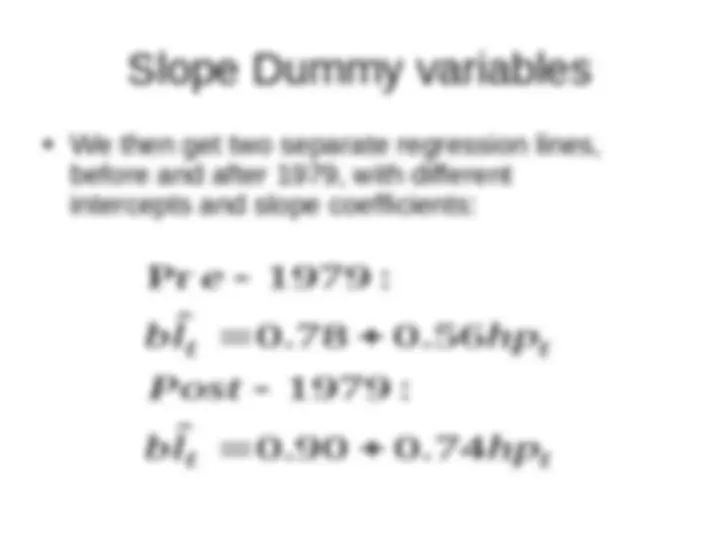

Dummy Variables

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Introduction to dummy variable

Typology: Summaries

1 / 25

This page cannot be seen from the preview

Don't miss anything!

coefficients of skewness and excess kurtosis

being jointly equal to 0

numberof observatio ns

coefficient of excess kurtosis

coefficient of skewness

]

24

( 3 )

6

[

2

1

2

2

2

1

T

b

b

b b

W T

with 2 degrees of freedom.

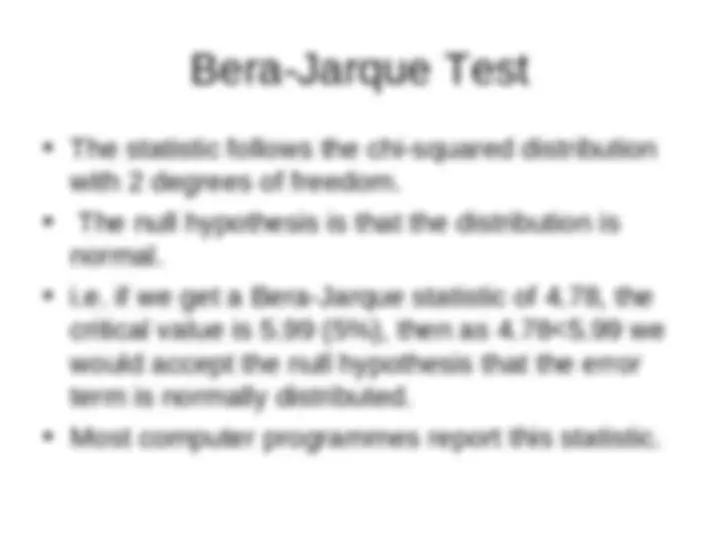

normal.

critical value is 5.99 (5%), then as 4.78<5.99 we

would accept the null hypothesis that the error

term is normally distributed.

Dummy Variable for Single Outlier

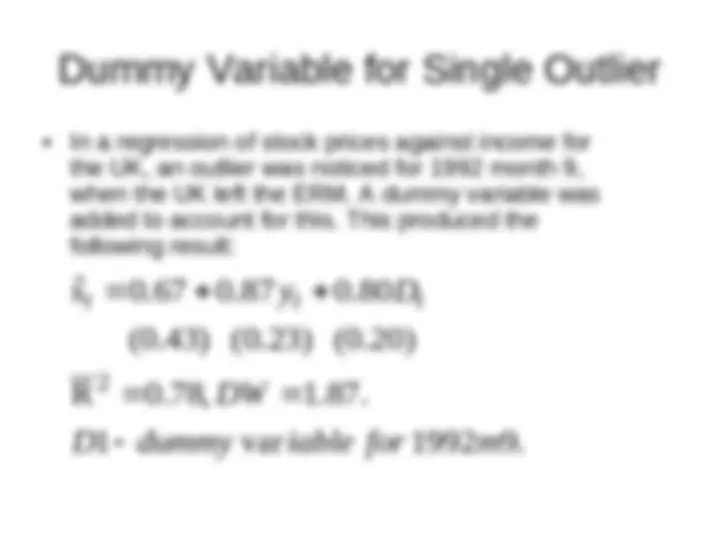

the UK, an outlier was noticed for 1992 month 9,

when the UK left the ERM. A dummy variable was

added to account for this. This produced the

following result:

2

t t t

value of ‘0’ or ‘1’. They are often called ‘on’ ‘off’

variables, being ‘on’ when they are 1.

explanatory variables or as the dependent

variable.

are specific problems with how the regression is

interpreted, however when they act as

explanatory variables they can be interpreted in

the same way as other variables.

Types of Explanatory Dummy

Variable

health.

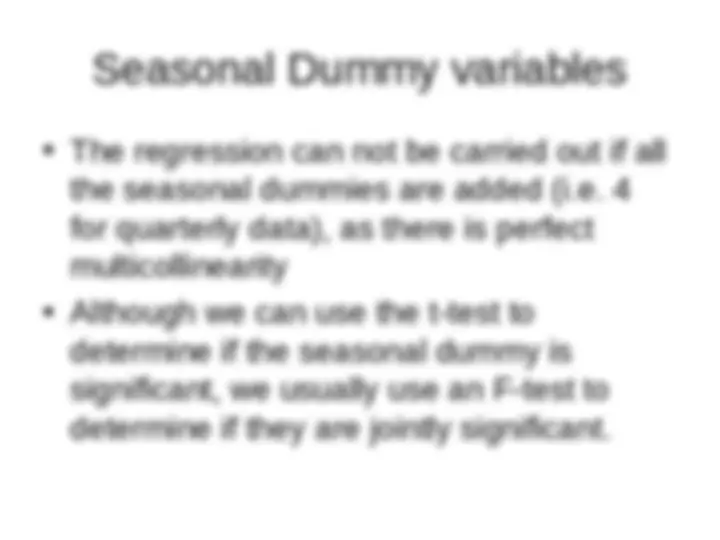

nature of the data, so quarterly data requires

three dummy variables etc.

policy:

the intercept of the regression

slope of the regression

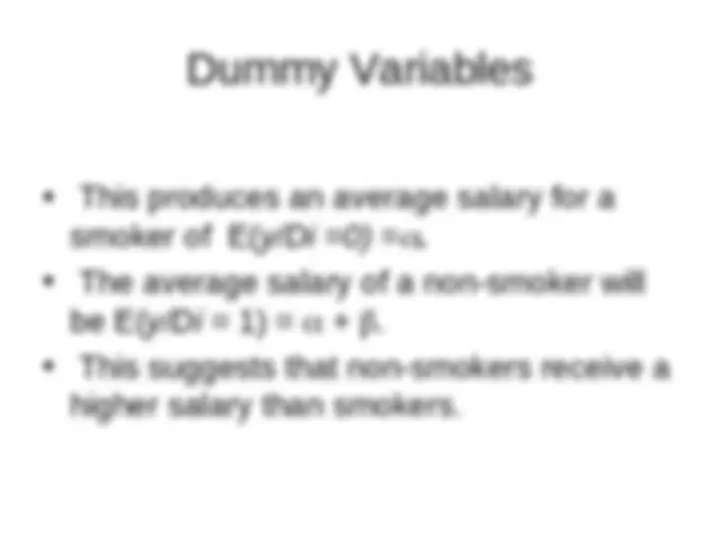

smoker of E( y/Di =0) = .

variable in a model with other explanatory

variables. In addition to the dummy variable

we could also add years of experience ( x) ,

to give:

finance due to the ‘day of the week’ effect on asset

prices.

i.e. a January dummy variable would consist of 0, except

every observation in January which has the value of 1.

quarterly data 3 etc. i.e. we have as many dummies as

months, quarters etc minus 1.

all the other dummies refer to differences between

themselves and this reference month.

gas and electricity firm, where the share price is

regressed against 3 dummy variables. (Using

quarterly data)

t t

t t

t t

t

t t

Q s y y

Q s y y

Q s y y

Q s y

s D D D y

2 3 4

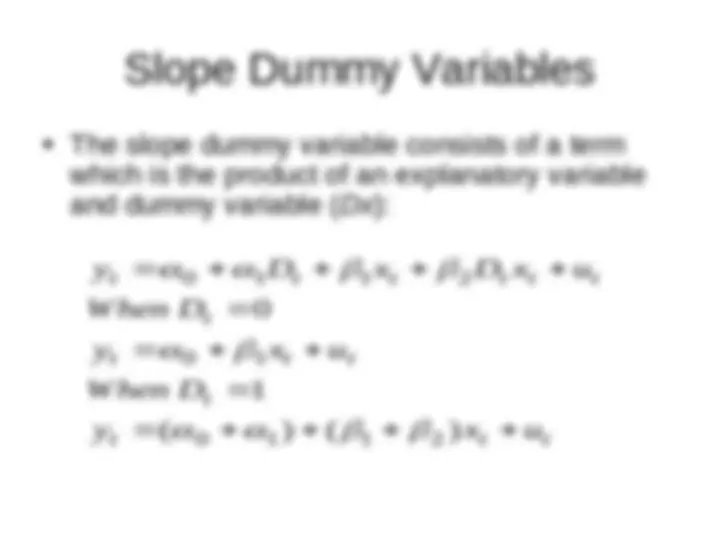

the intercept dummy variable, we could also use

dummy variables to model changes in the slope

of the regression line, these are known as slope

or interaction dummy variables.

or more commonly both types in a regression, to

account for changes in the intercept and slope of

the regression line.

which is the product of an explanatory variable

and dummy variable ( Dx ):

t t t

t

t t t

t

t t t t t t

y x u

When D

y x u

When D

y D x D x u

( ) ( )

1

0

0 1 1 2

0 1

0 1 1 2