REMELYN L. ASAHID-CHENG

STATISTICAL ANALYSIS

WITH SOFTWARE APPLICATION

Introduction to Hypothesis Testing

MODULE 3-WEEK 9-TOPIC 19

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

a statistical method used to evaluate and test hypotheses or claims about a population using sample data. It involves formulating a null hypothesis and an alternative hypothesis, selecting a level of significance, and using statistical tests to either reject or fail to reject the null hypothesis.

Typology: Study notes

1 / 35

This page cannot be seen from the preview

Don't miss anything!

REMELYN L. ASAHID-CHENG

Introduction to Hypothesis Testing MODULE 3-WEEK 9-TOPIC 19

Introduction to Hypothesis Testing

Types of Hypotheses Three types of hypotheses will be explored here. ✓ Research hypotheses ✓ Statistical hypotheses ✓ Substantive hypotheses Although much of the focus will be on testing statistical hypotheses, it is also important for business decision makers to have an understanding of both research and substantive hypotheses..

Types of Hypotheses Research Hypotheses Virtually all inquisitive thinking businesspeople have similar research hypotheses concerning relationships, approaches, and techniques in business. Such hypotheses can lead decision makers to new and better ways to accomplish business goals. However, to formally test research hypotheses, it is generally best to state them as statistical hypotheses.

Types of Hypotheses Statistical Hypotheses In order to scientifically test research hypotheses, a more formal hypothesis structure needs to be set up using statistical hypotheses. A statistical hypothesis is a formal hypothesis structure set up with a null and an alternative hypothesis to scientifically test research hypotheses. Suppose business analysts want to “prove” the research hypothesis that older workers are more loyal to a company. The analysts either develop or obtain a “loyalty” survey instrument. If this instrument is administered to a sample of both older and younger workers, how much higher do older workers have to score (assuming higher scores indicate more loyal) than younger workers to prove the research hypothesis? What is the “proof threshold”? Instead of attempting to prove or disprove research hypotheses directly in this manner, business analysts convert their research hypotheses to statistical hypotheses and then test the statistical hypotheses using standard procedures. What are these procedures, and how is this done?

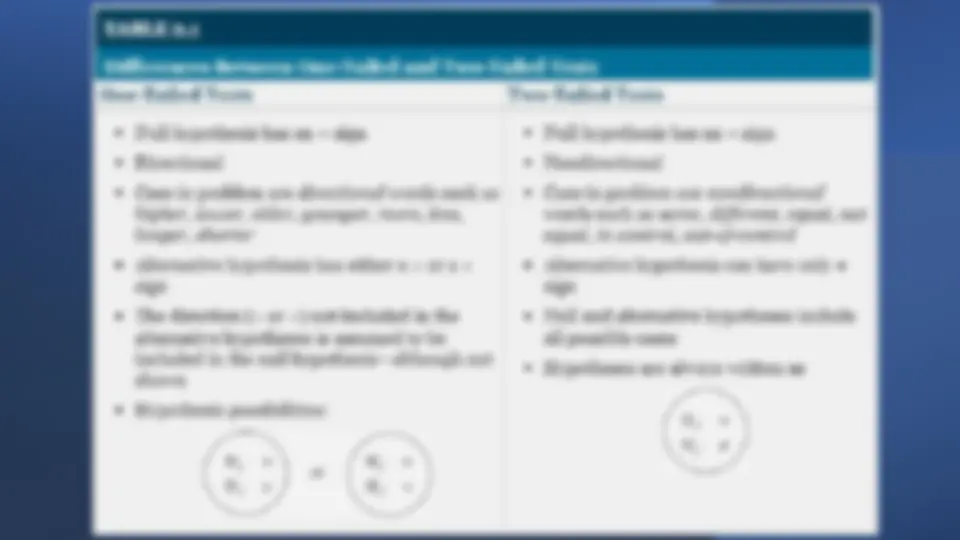

Types of Hypotheses Statistical Hypotheses It is common symbolism to represent the null hypothesis as Ho and the alternative hypothesis as Ha. The null and alternative hypotheses for the flour example can be restated using these symbols and μ for the population mean as Note that the alternative hypothesis is the “complement” of the null hypothesis and contains everything that is not in the null hypothesis. Thus, between the null and alternative hypotheses all possibilities are being considered. Statistical hypotheses are written so that they will produce either a one-tailed or a two-tailed test. The hypotheses shown here for the flour packaging manufacturing study are two-tailed because there is no presumption that analysts believe that the packages are overfilled or that they are underfilled. That is, there is no “directional” hypothesis. By conducting a two-tailed test such as this, analysts allow for the possibility that either μ > 80 oz. or μ < 80 oz. could occur.

Types of Hypotheses Statistical Hypotheses A two-tailed test is a statistical test wherein the business analyst is interested in testing both sides of the distribution. Two-tailed tests always use = and ≠ in the statistical hypotheses and are directionless in that the alternative hypothesis allows either the greater than (>) or the less than (<) possibility. As an example of a one-tailed test, suppose a company has held an 18 % share of the market. However, because of an increased marketing effort, company officials believe the company’s market share is now greater than 18 %, and the officials would like to prove it. The null hypothesis is that the market share is still 18 %. Converting the 18 % to a proportion and using p to represent the population proportion results in the following null hypothesis. The alternative hypothesis is that the population proportion is now greater than. 18. Note that the “new idea” or “new theory” that company officials want to “prove” is stated in the alternative hypothesis. The null hypothesis states that the old market share of 18 % is still true.

Types of Hypotheses Substantive Hypotheses In testing a statistical hypothesis, a business analyst reaches a conclusion based on the data obtained in the study. If the null hypothesis is rejected and therefore the alternative hypothesis is accepted, it is common to say that a statistically significant result has been obtained. For example, in the market share problem, if the null hypothesis is rejected, the result is that the market share is “significantly greater” than 18 %. The word significant to statisticians and business analysts merely means that the result of the experiment is unlikely due to chance and a decision has been made to reject the null hypothesis. However, in everyday business life, the word significant is more likely to connote “important” or “a large amount.” One problem that can arise in testing statistical hypotheses is that particular characteristics of the data can result in a statistically significant outcome that is not a significant business outcome.

Types of Hypotheses Substantive Hypotheses In addition to understanding a statistically significant result, business decision makers need to determine what, to them, is a substantive result. A substantive result occurs when the outcome of a statistical study produces statistically significant results that are also important to the decision maker. The importance to the analyst will vary from study to study. As an example, in a recent year, one healthcare administrator was excited because patient satisfaction had significantly increased (statistically) from one year to the next. However, an examination of the data revealed that on a five-point scale, their satisfaction ratings had gone up from 3. 61 to only 3. 63. Is going from a 3. 61 rating to a 3. 63 rating in one year really a substantive increase? On the other hand, increasing the average purchase at a large, high- volume store from $ 55. 45 to $ 55. 50 might be substantive as well as significant if volume is large enough to drive profits higher. Both business analysts and decision makers should be aware that statistically significant results are not always substantive results.

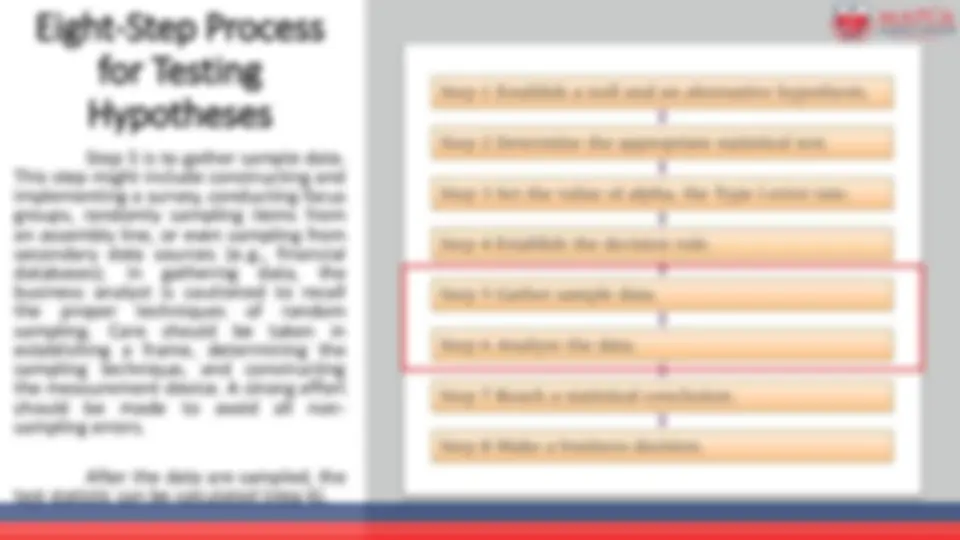

Eight-Step Process for Testing Hypotheses

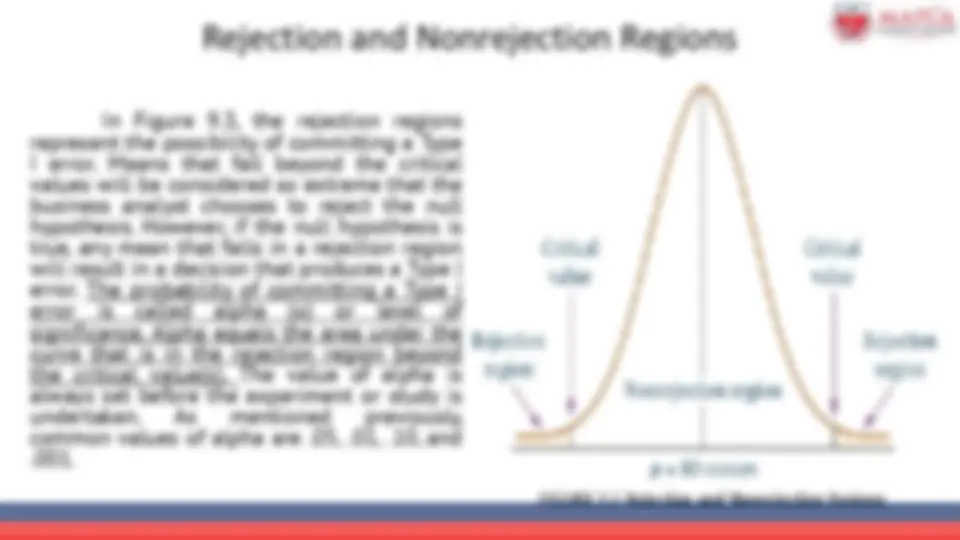

Eight-Step Process for Testing Hypotheses Step 2 is to select the most appropriate statistical test to use for the analysis. In selecting such a test, the business analyst needs to consider the type, number, and level of data being used in the study along with the statistic used in the analysis (mean, proportion, etc.). In addition, business analysts should consider the assumptions underlying certain statistical tests and determine whether they can be met in the study before using such tests. At step 3 , the value of alpha is set. Alpha is the probability of committing a Type I error and will be discussed later. Common values of alpha include. 05 ,. 01 ,. 10 , and. 001.

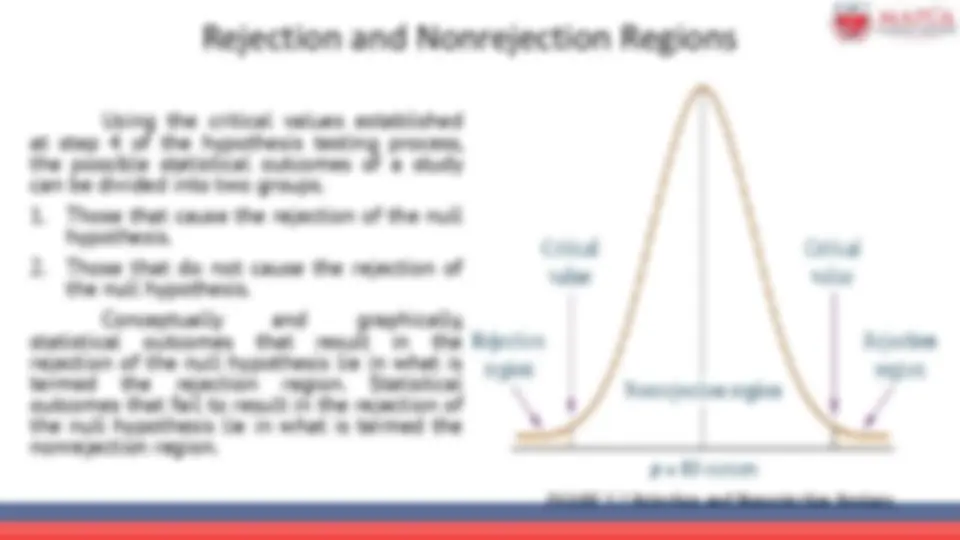

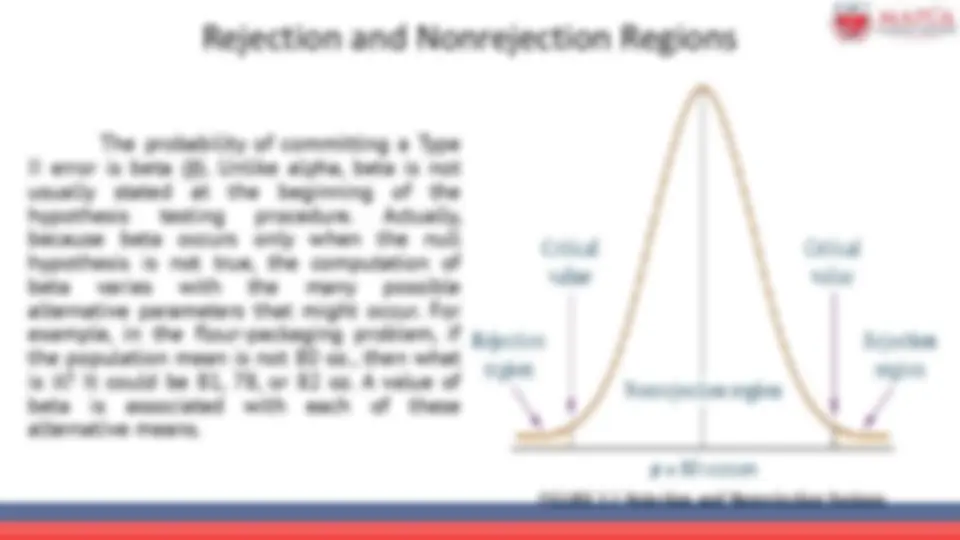

Eight-Step Process for Testing Hypotheses Step 4 is to establish the decision rule, which should be done before the study is undertaken. Using alpha and the test statistic, critical values can be determined. These critical values are used at the decision step (step 7 ) to determine whether the null hypothesis is rejected or not. If the p-value method (discussed later) is utilized, the value of alpha is used as a critical probability value. The process begins by assuming that the null hypothesis is true. Data are gathered and statistics computed. If the evidence is away from the null hypothesis, the business analyst begins to doubt that the null hypothesis is really true. If the evidence is far enough away from the null hypothesis that the critical value is surpassed, the business analyst will reject the null hypothesis and declare that a statistically significant result has been attained. The first four steps in testing hypotheses should always be completed before the study is undertaken. It is not sound research to gather data first and then try to determine what to do with them.