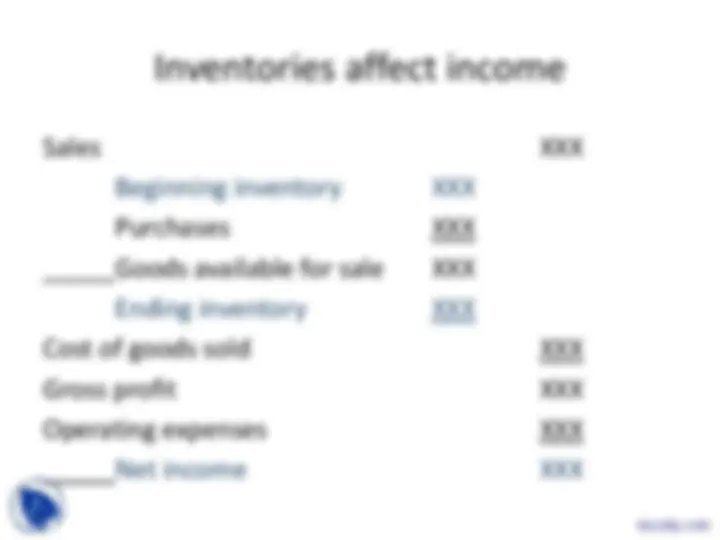

Learning Objectives

1. Explain the importance of inventory

for asset valuation and income

measurement

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth analysis of inventory valuation and its significance for asset valuation and income measurement. It covers the nature of inventory, types of inventory, inventory cost flow assumptions, and the impact of inventory valuation on liquidity and profitability. It also discusses various inventory valuation methods such as fifo, lifo, and average cost.

Typology: Slides

1 / 100

This page cannot be seen from the preview

Don't miss anything!

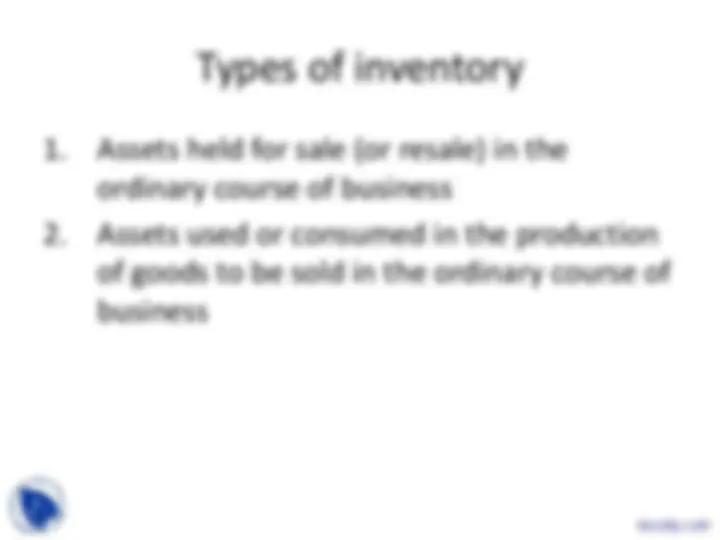

Items used in producing the product

Products started but not yet completed

Products completed but not yet sold

If you are in Los Angeles and your supplier is in New York City

You

Them

If you are in Los Angeles and your supplier is in New York City

You

Them

The F.O.B. designation determines who that “somebody” is

You

Them

You will pay the transportation cost and you will own the merchandise once it is turned over to the carrier in NYC

You

Them

These are noncancellable, long-term contracts to purchase goods at a set price

You might enter into such an agreement to buy a product if you thought its price was about to go up

If the price does go up, everything is cool and you will make lots of money

But if the price goes down, you have an economic problem and an accounting problem

On December 31, 19X1, gas is selling for $.

Since Peck has agreed to pay $1.00 per gallon, accounting conservatism mandates:

December 31, 19X

Est. Loss on Purch. Commit. 6,

Est. Liab. on Contract 6,

This reduces Peck’s income and increases his liabilities

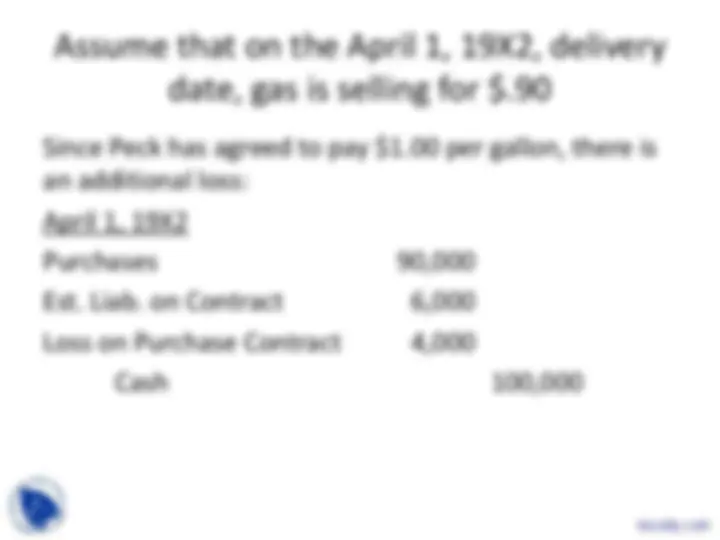

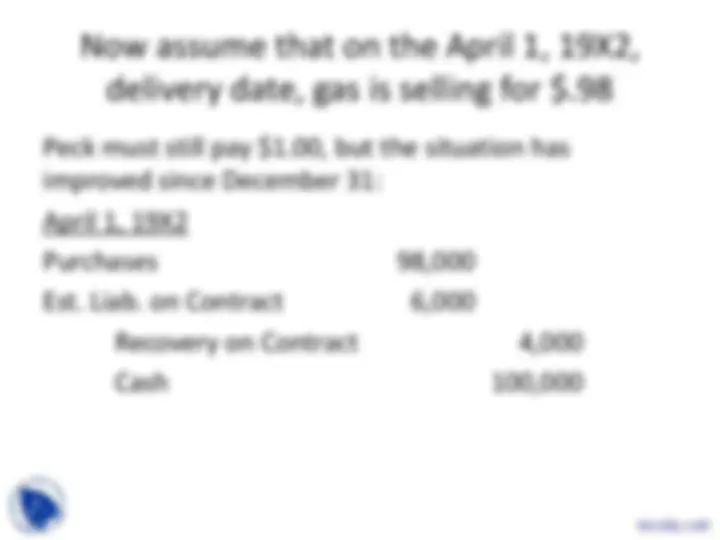

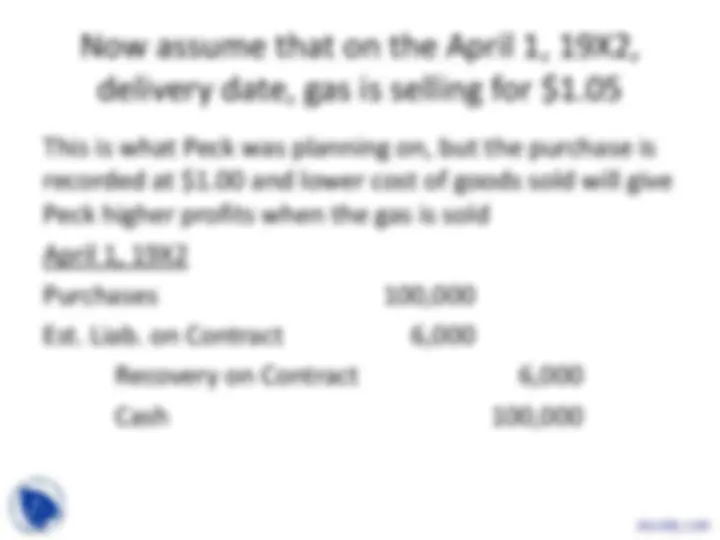

Assume that on the April 1, 19X2, delivery date, gas is selling for $.

Since Peck has agreed to pay $1.00 per gallon, there is an additional loss:

April 1, 19X

Purchases 90,

Est. Liab. on Contract 6,

Loss on Purchase Contract 4,

Cash 100,