Week 10

Cong / Shirley

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

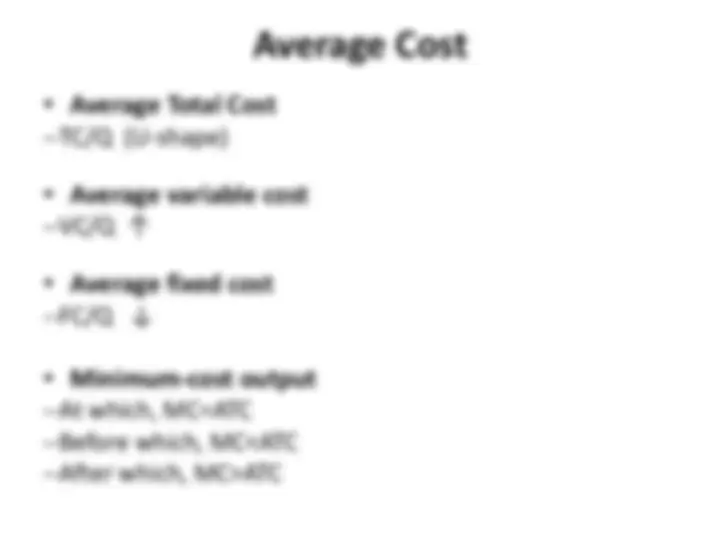

An overview of various cost concepts, including fixed and variable costs, total cost, marginal cost, average cost, and minimum-cost output. It also covers the concepts of economic profit, marginal revenue, and optimal output level. Several questions to test understanding of these concepts.

Typology: Study notes

1 / 11

This page cannot be seen from the preview

Don't miss anything!

Cong / Shirley

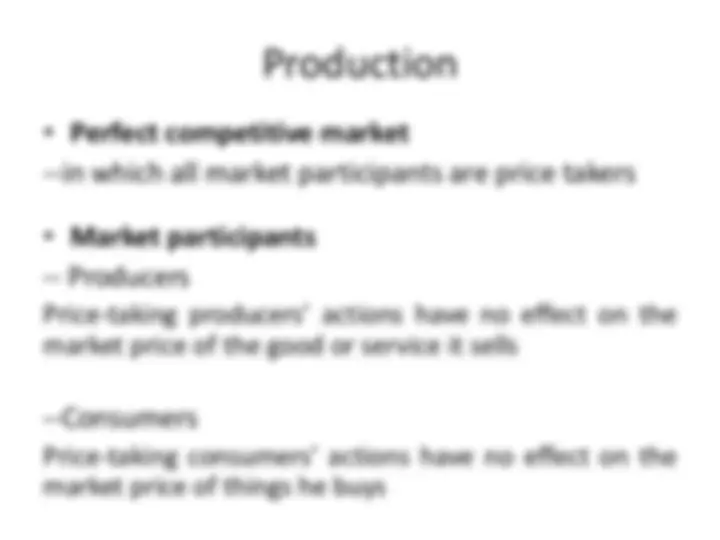

--in which all market participants are price takers

-- Producers Price-taking producers’ actions have no effect on the market price of the good or service it sells

--Consumers Price-taking consumers’ actions have no effect on the market price of things he buys

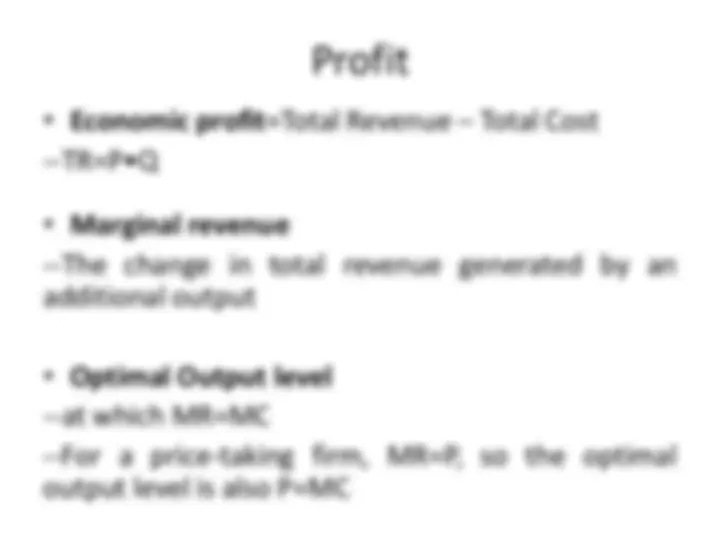

--TR=P•Q

--The change in total revenue generated by an additional output

--For a price-taking firm, MR=P, so the optimal output level is also P=MC

Q1. If Jacob knows the marginal cost of the first sports jersey is $21, the marginal cost of the second sports jersey is $40, and the marginal cost of the third jersey is $17, what is the total variable cost of producing three jerseys?

a) $

b) $

c) $

d) $

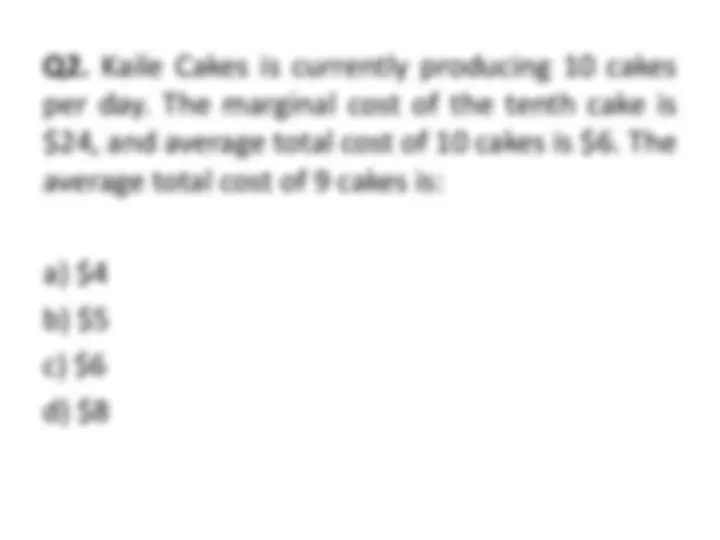

Q2. Kaile Cakes is currently producing 10 cakes per day. The marginal cost of the tenth cake is $24, and average total cost of 10 cakes is $6. The average total cost of 9 cakes is:

a) $

b) $

c) $

d) $

Q4. If a business is operating in a competitive market in the short run, what is fixed?

a) market price and total costs

b) marginal costs and average total costs

c) market price and fixed costs

d) profits

Q5. In a competitive market the price is $8. A typical firm in the market has ATC = $6, AVC = $5, and MC = $8. How much economic profit is the firm earning in the short run?

a) $0 per unit

b) $1 per unit

c) $2 per unit

d) $3 per unit