CHAPTER 7

DEMAND FOR INSURANCE

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

VIDEO TRANSCRIPTS AND LECTURE SLIDES

Typology: Lecture notes

1 / 90

This page cannot be seen from the preview

Don't miss anything!

Demand for insurance driven by the fear of the unknown Hedge against risk -- the possibility of bad outcomes Purchasing insurance means forfeiting income in good times to get money in bad times If bad times avoided, then money lost Ex: The individual who buys health insurance but never visits the hospital might have been better off spending that income elsewhere.

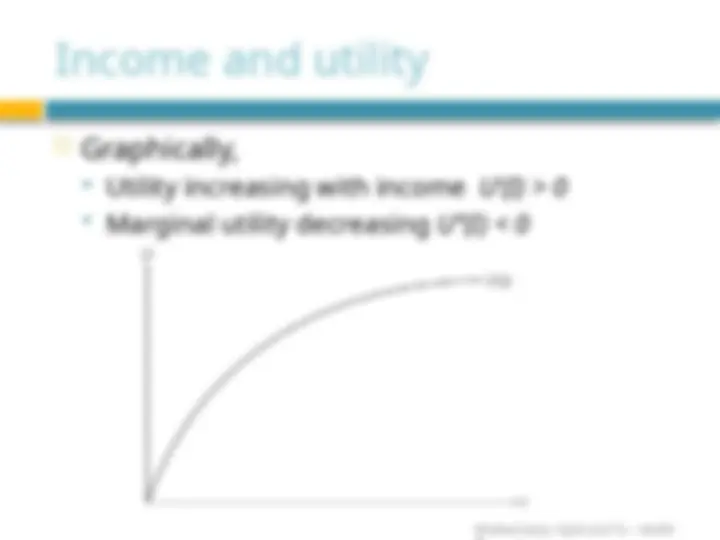

Utility increasing with income U’(I) > 0 Marginal utility decreasing U’’(I) < 0

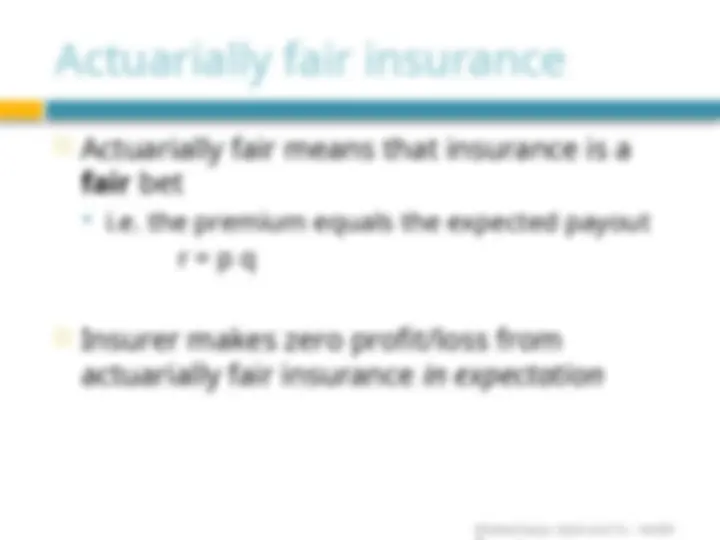

An individual does not know whether she will become sick, but she knows the probability of sickness is p between 0 and 1 Probability of sickness is p Probability of staying healthy is 1 - p If she gets sick, medical bills and missed work will reduce her income (^) I S = income if she does get sick (^) I H > IS = income if she remains healthy

Suppose we offer a starving graduate student a choice between two possible options, a lottery and a certain payout: A: a lottery that awards $500 with probability 0.5 and $ with probability 0.5. B: a check for $250 with probability 1. The expected value of both the lottery and the certain payout is $250: E[I] = p IS + (1- p) IH E[A] = .5(500) + .5(0) = $ E[B] = 1(250) = $

The student’s preference for option B over option A implies that his expected utility from B, is greater than his expected utility from A: E[U(B)] ≥ E[U(A)] U($250) ≥0.5 U($500) + 0.5 U($0) In this case, even though the expected values of both options are equal, the student prefers the certain payout over the less certain one. (^) This student is acting in a risk-averse manner over the choices available.

(^) She gains a high income I H if healthy, and low income I S if sick.

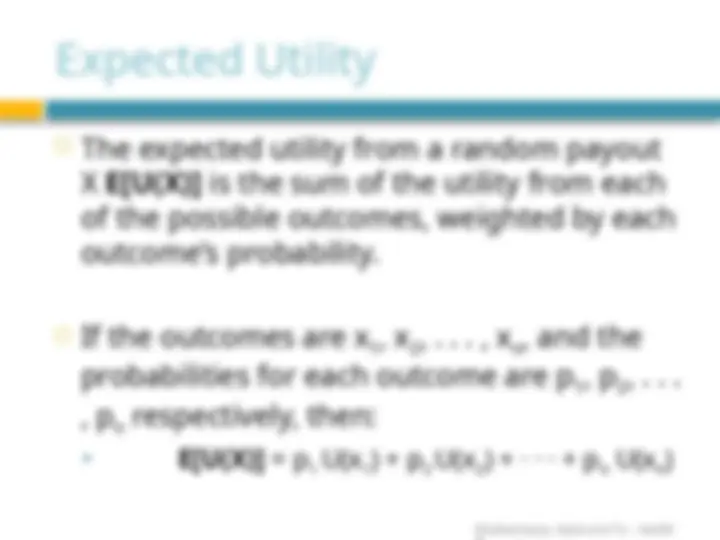

Expected utility E[U(I)] is: E[U(I)] = p U(I S ) + (1- p) U(I H

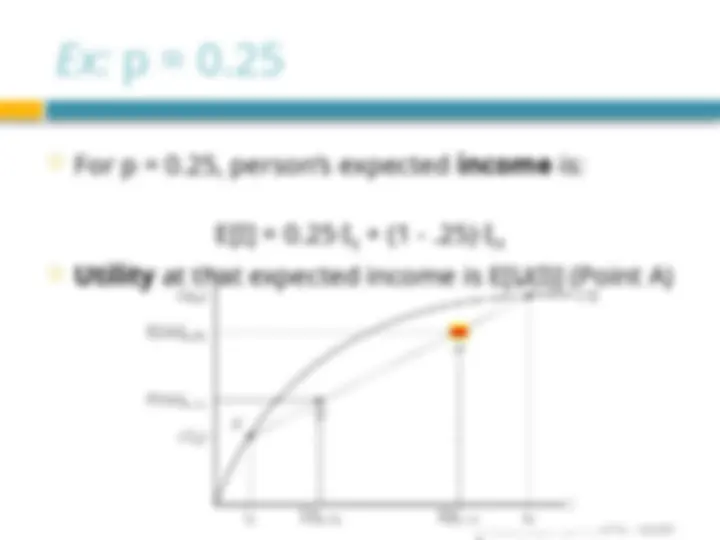

For p = 0.25, person’s expected income is: E[I] = 0.25·I S

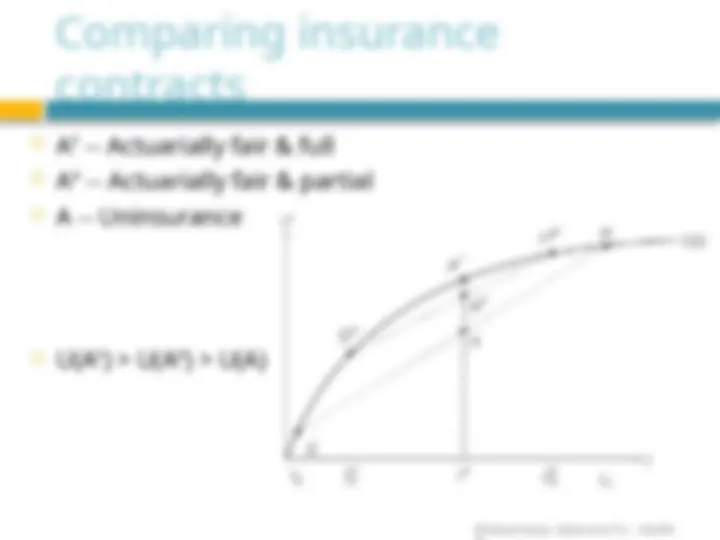

H Utility at that expected income is E[U(I)] (Point A)

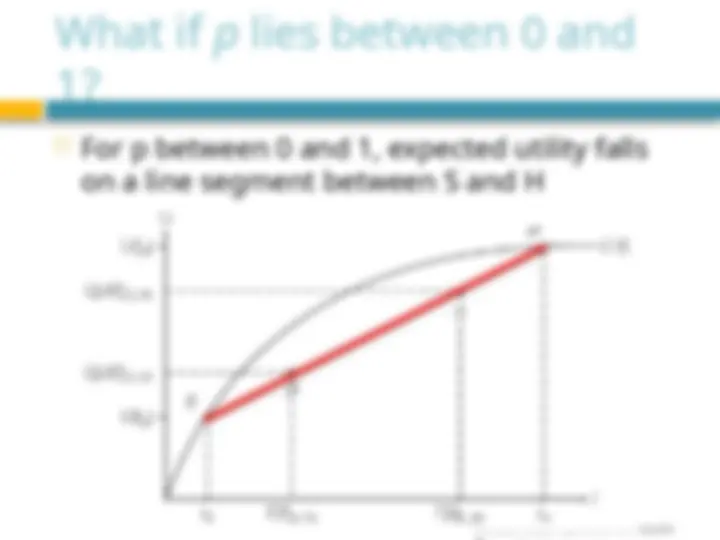

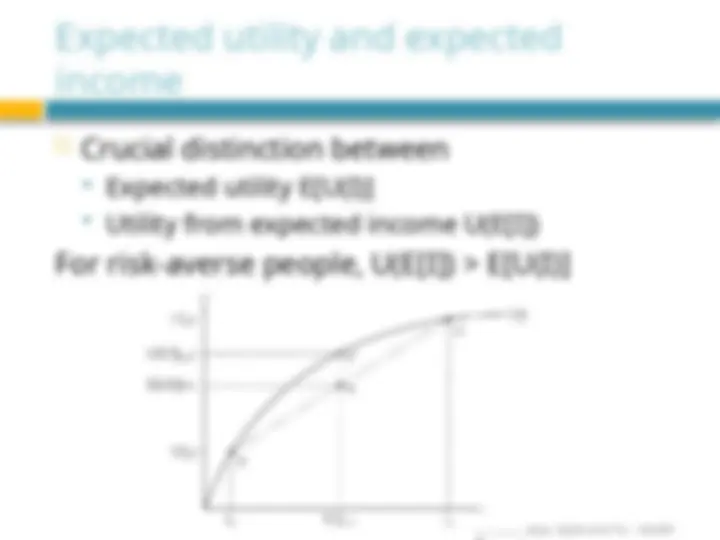

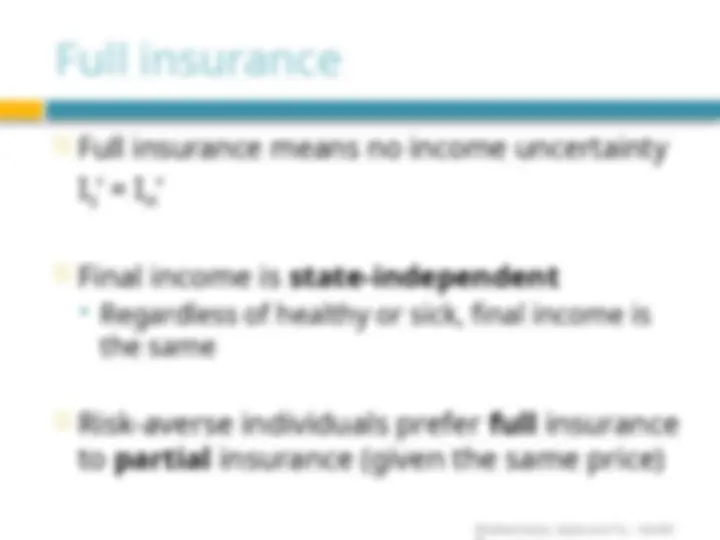

Synonymous definitions of risk-aversion: Prefer certain outcomes to uncertain ones with the same expected income. Prefers the utility from expected income to the expected utility from uncertain income U(E[I]) > E[U(I)]

(^) U’(I) > 0 (^) U’’(I) < 0

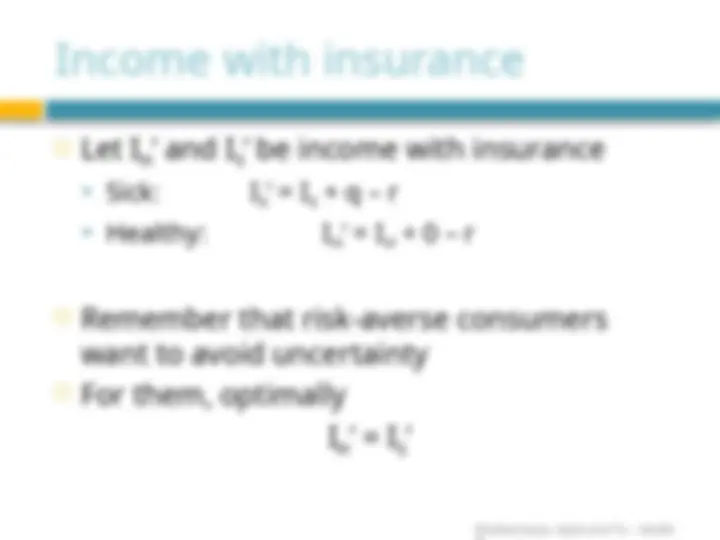

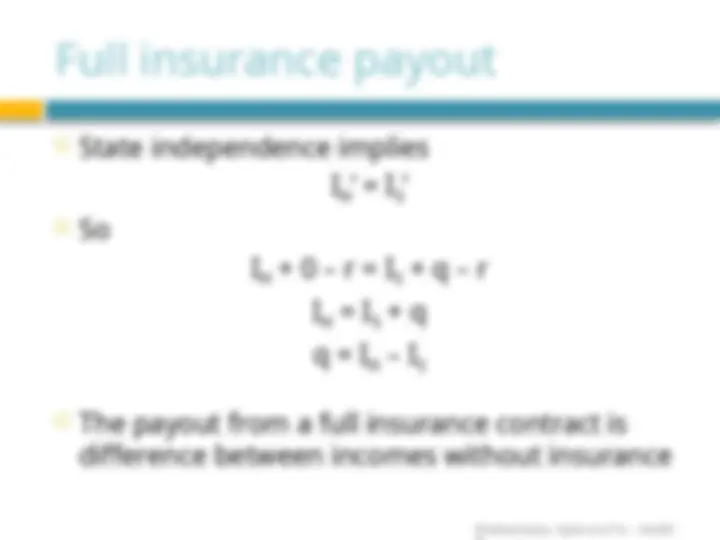

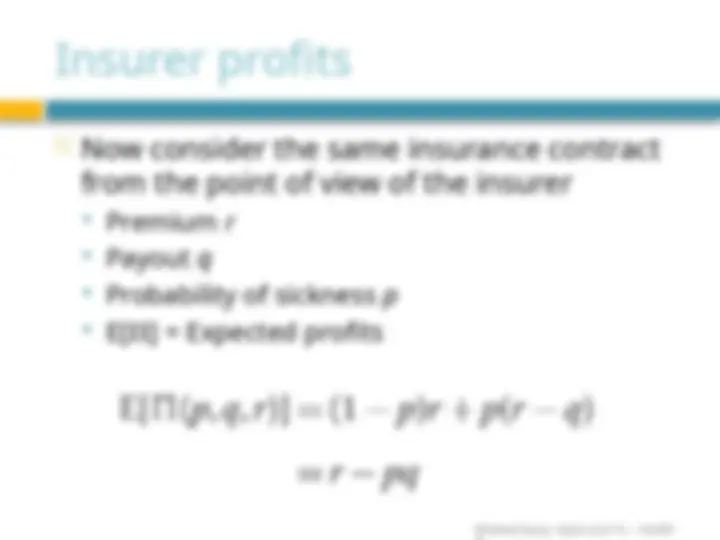

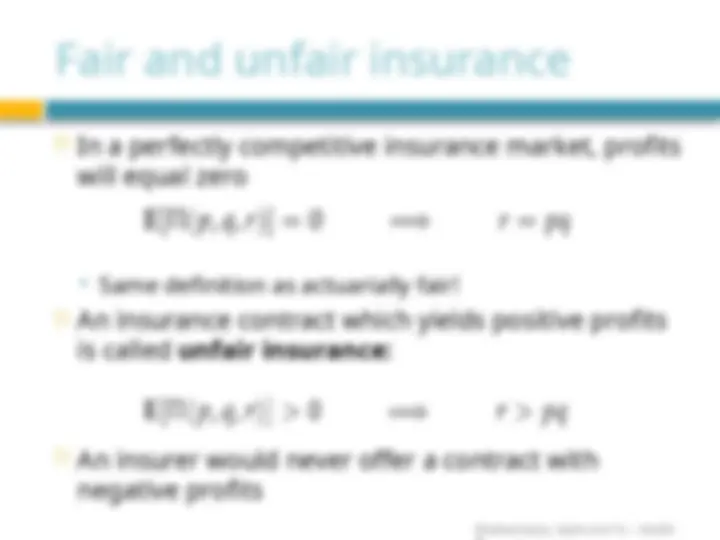

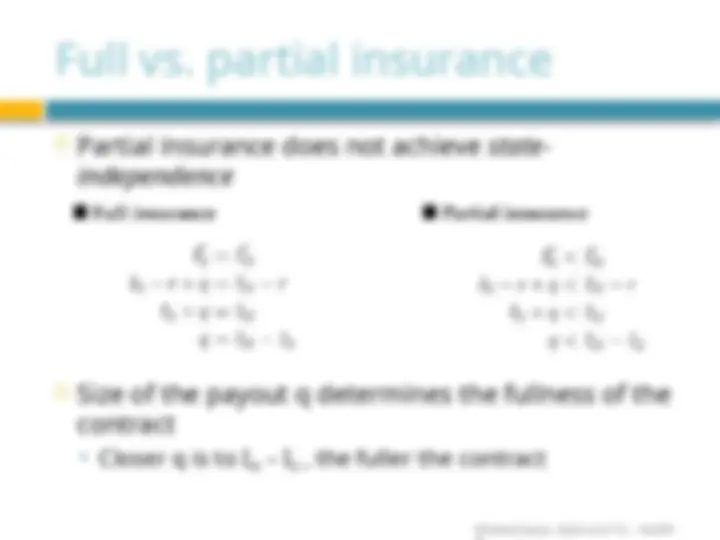

(^) Payment r is known as the insurance premium

(^) Sick: I S

S

H

H

S

H

S

H

S

H