Linearization

(Lectures on Solution Methods for Economists V: Appendix)

Jes´us Fern´andez-Villaverde1and Pablo Guerr´on2

November 21, 2021

1University of Pennsylvania

2Boston College

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The concept of linearization in solving dynamic optimization problems in economics. It explains the difference between loglinearization and linearization, and provides a step-by-step guide on how to solve a system of equations using undetermined coefficients. The document also presents the general structure of a linearized system and policy functions. relevant for students of economics and related fields who are studying dynamic optimization problems.

Typology: Lecture notes

1 / 19

This page cannot be seen from the preview

Don't miss anything!

Jes´us Fern´andez-Villaverde^1 and Pablo Guerr´on^2 November 21, 2021 (^1) University of Pennsylvania

(^2) Boston College

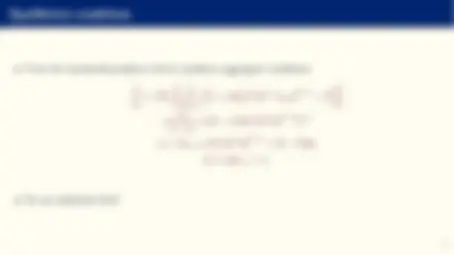

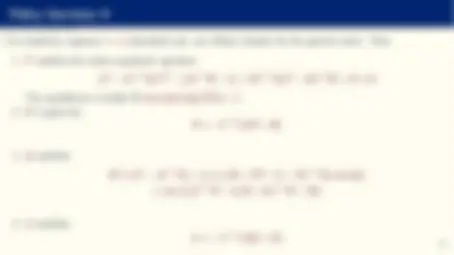

t=

βt^ {log ct + ψ log (1 − lt )}

ct + kt+1 = k tα (ezt^ lt )^1 −α^ + (1 − δ) kt , ∀ t > 0 zt = ρzt− 1 + εt , εt ∼ N (0, σ)

ct+

1 + αkα t+1−^1 l t^1 +1−α − δ

ψ ct 1 − lt = (1 − α) kα t l− tα

ct + kt+1 = k tα l t^1 −α+ (1 − δ) kt

1 + αkα−^1 l^1 −α^ − δ

ψ c 1 − l = (1 − α) kαl−α

c + δk = kαl^1 −α

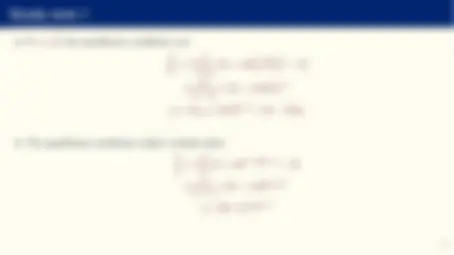

Solution:

k = μ Ω + ϕμ l = ϕk c = Ωk y = kαl^1 −α

where ϕ =

1 α

1 β −^ 1 +^ δ

)) (^1) −^1 α , Ω = ϕ^1 −α^ − δ, and μ = (^) ψ^1 (1 − α) ϕ−α.

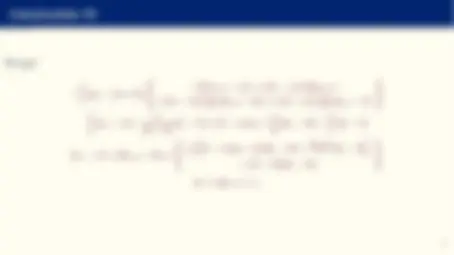

We linearize:

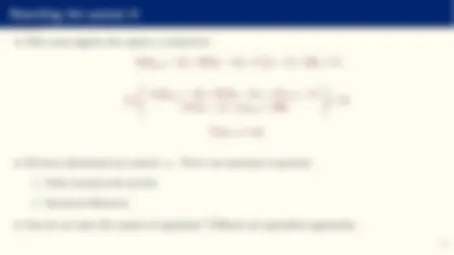

1 ct^ =^ βEt

ct+

1 + αkα t+1−^1 (ezt+1^ lt+1)^1 −α^ − δ

ψ ct 1 − lt = (1 − α) k tα (ezt^ lt )^1 −α^ l t−^1

ct + kt+1 = k tα (ezt^ lt )^1 −α^ + (1 − δ) kt zt = ρzt− 1 + εt

around l, k, and c with a First-order Taylor Expansion.

We get:

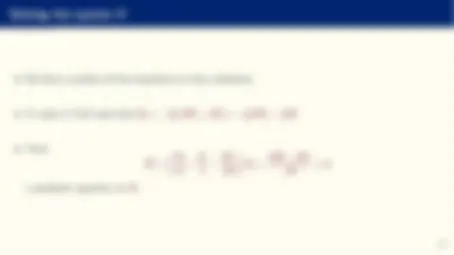

c (ct^ −^ c) =^ Et

− (^1) c (ct+1 − c) + α (1 − α) β yk zt+1+ α (α − 1) β (^) ky 2 (kt+1 − k) + α (1 − α) β (^) kly (lt+1 − l)

c (ct − c) + 1 (1 − l) (lt − l) = (1 − α) zt + α k (kt − k) − α l (lt − l)

(ct − c) + (kt+1 − k) =

y

(1 − α) zt + α k (kt − k) + (1− l α)(lt − l)

zt = ρzt− 1 + εt

Et

G (kt+1 − k) + H (kt − k) + J (lt+1 − l) +K (lt − l) + Lzt+1 + Mzt

Et zt+1 = ρzt

G (P 1 (kt − k) + P 2 zt ) + H (kt − k) + J (R 1 (P 1 (kt − k) + P 2 zt ) + R 2 Nzt )

+K (R 1 (kt − k) + R 2 zt ) + (LN + M) zt = 0

a quadratic equation on P 1.

one stable and another unstable.

P 2 =

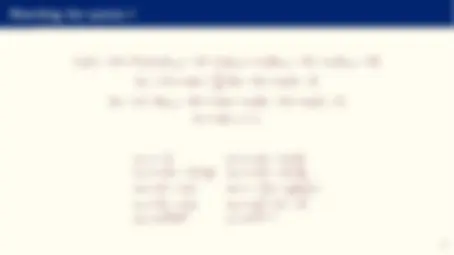

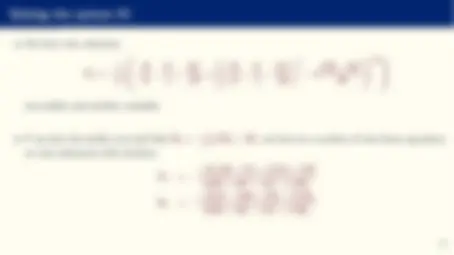

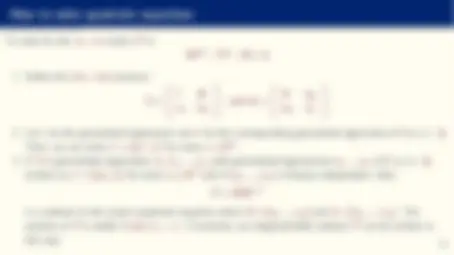

Given m states st , n controls yt , and k exogenous stochastic processes zt+1, we have:

Ast + Bst− 1 + Cyt + Dzt = 0 Et (Fst+1 + Gst + Hst− 1 + Jyt+1 + Kyt + Lzt+1 + Mzt ) = 0 Et zt+1 = Nzt

where C is of size l × n, l ≥ n and of rank n, F is of size (m + n − l) × n, and that N has only stable eigenvalues.

We guess policy functions of the form:

st = Pst− 1 + Qzt yt = Rst− 1 + Uzt

where P, Q, R, and U are matrices such that the computed equilibrium is stable.

To solve for the m × m matrix P in ΨP^2 − ΓP − Θ = 0

Ξ =

Im 0 m

, and ∆ =

Ψ (^0) m (^0) m Im