LIT EM AP 2.0

(CHAPTER 1)

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth analysis of the conceptual framework for financial reporting, which serves as the theoretical foundation for accounting standards. It explains the purpose, relevance, materiality, understandability, financial statements, reporting entity, measurement, presentation and disclosure, and qualitative characteristics of useful financial information. The document also discusses the international accounting standards (ias) issued by the international accounting standards committee (iasc), and the international financial reporting standards (ifrs) issued by the international accounting standards board (iasb).

Typology: Slides

1 / 43

This page cannot be seen from the preview

Don't miss anything!

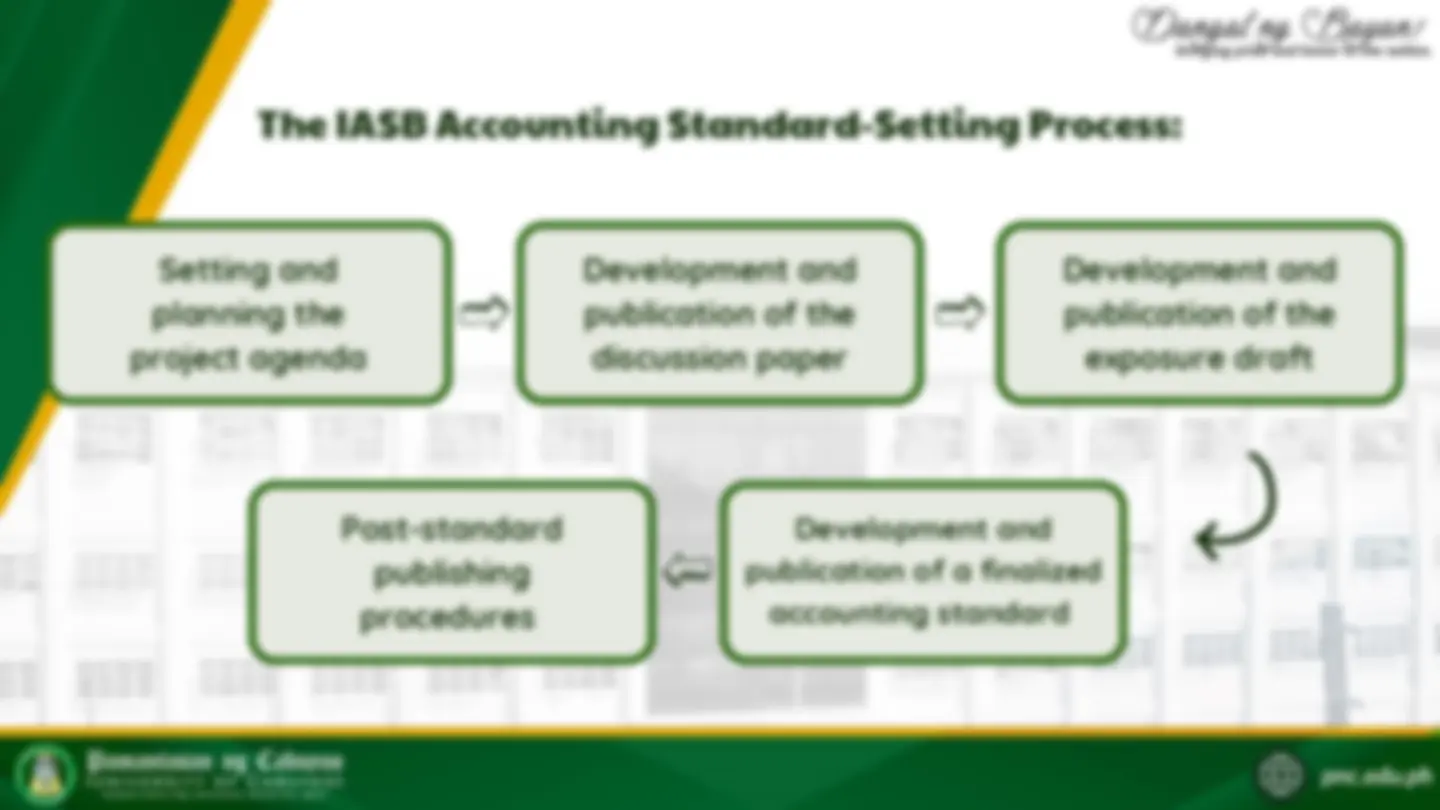

The IASB Accounting Standard-Setting Process:

planning the^ Setting and project agenda

Development and publication of the discussion paper

Development and publication of the exposure draft

publication of a finalized^ Development and accounting standard

Post-standard publishing procedures

it is the interpretative body of the IASB. It is formerly called as the International Financial Reporting Interpretations Committee (IFRIC). This committee develops authoritative interpretations of existing IAS and IFRS and provides guidance on financial reporting issues not specifically addressed by IAS and IFRS. An IFRIC Interpretation becomes part of IFRS once they are approved by the IASB.

Before December 2001, the IASB’s interpretative body is called the Standards Interpretations Committee (SIC). On reconstituted as December 2001, IFRIC SIC was. IFRIC issues IFRIC IC.

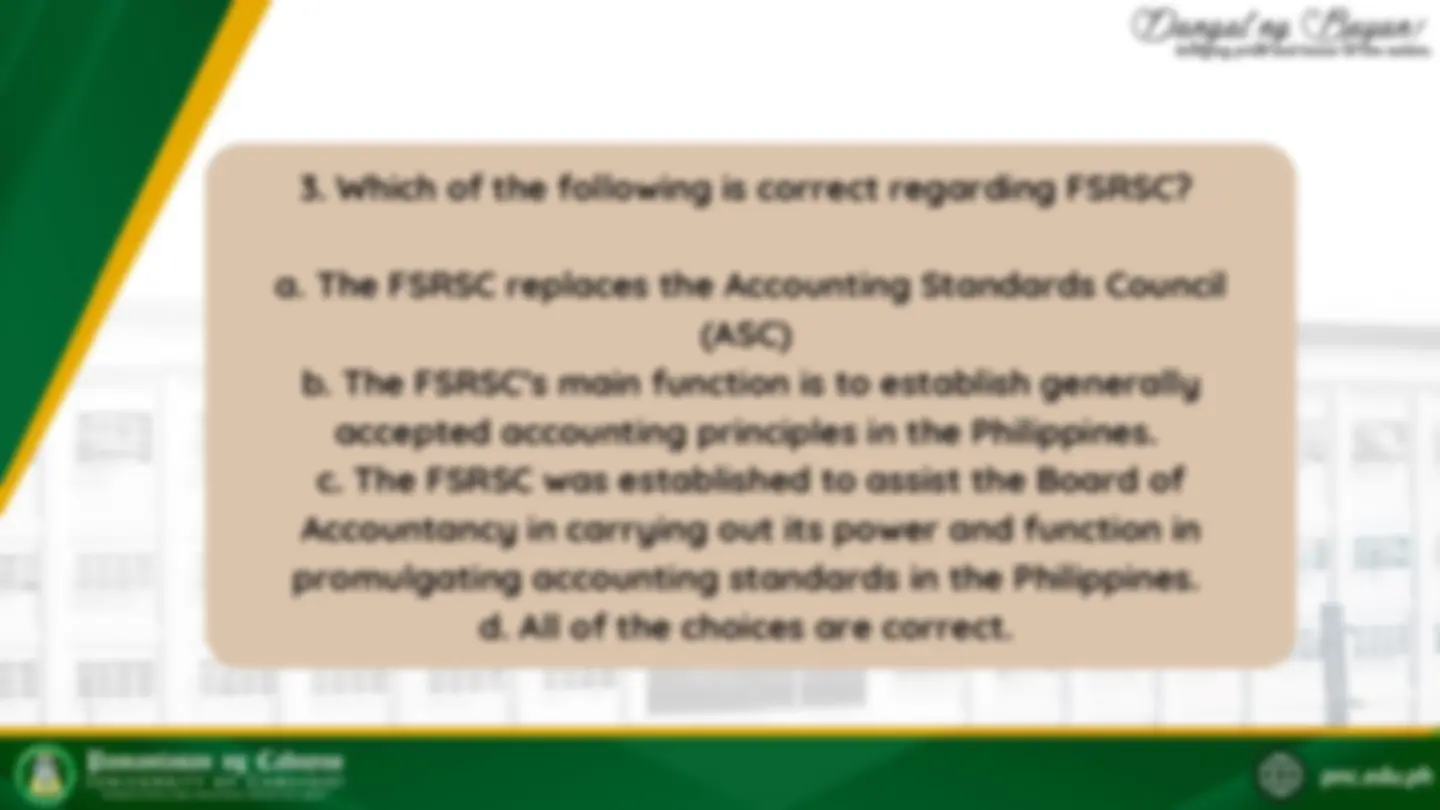

*In September 2022, the Professional Regulatory Board of Accountancy (BOA) issued Board Resolution No.44 (s.2022) which contains the approval of renaming the FRSC to FSRSC.

Philippines called the^ The FRSC issued the accounting standards in the Philippines Accounting Standards (PFRS)^ (PAS) which serves as the highest hierarchy of GAAP inand P hilippine Financial Reporting Standards the Philippines. Moreover, it is the international counterpart of IASB.

Accounting Standards Council (ASC) which^ The former setting body was called the was created by the Certified Public Accountants (PICPA). Philippine Institute of

interpretations of the existing PAS and PFRS and provide^ It was established by the FRSC to develop authoritative guidance on financial reporting issues not specifically addressed in PAS and PFRS. It is the international counterpart of IFRS IC.

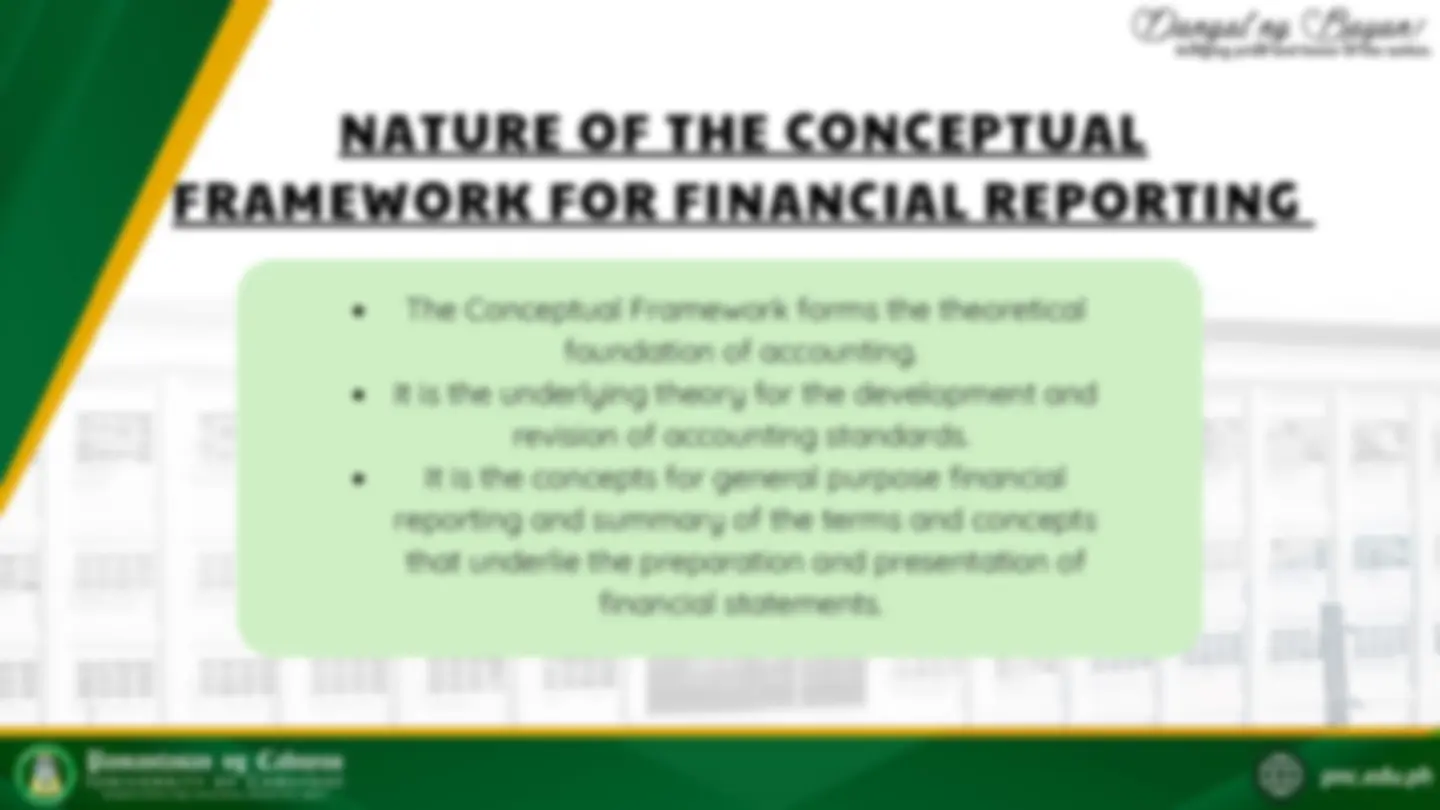

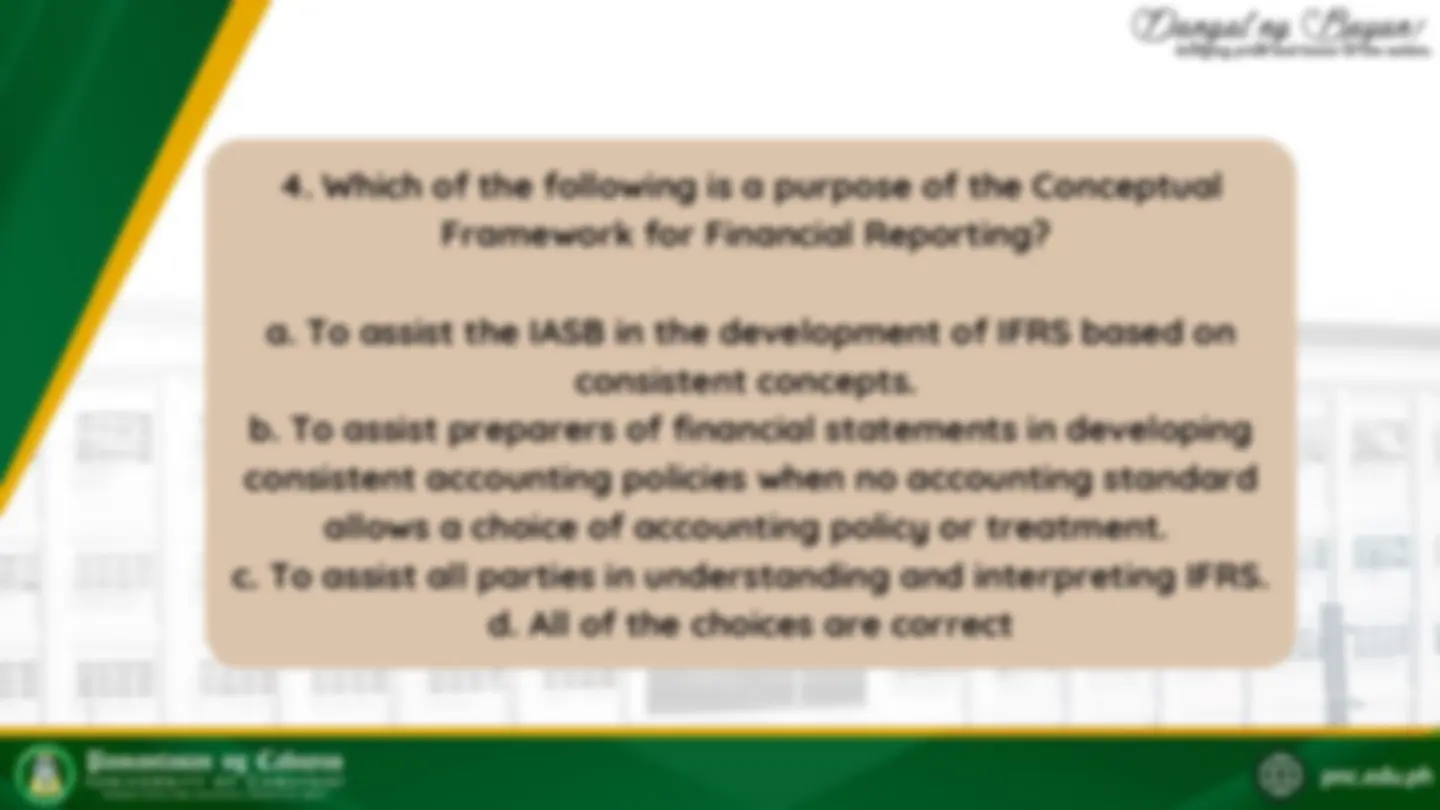

The Conceptual Framework forms the theoretical foundation of accounting. It is the underlying theory for the development and revision of accounting standards. reporting and summary of the terms and concepts^ It is the concepts for general purpose financial that underlie the preparation and presentation of financial statements.

To assist the IASB in the development of existing and future accounting standards based on consistent concepts. To assist financial statements preparers in the development of consistent accounting policies when no accounting standard accounting standard allows a choice of accounting policy or^ applies to a particular transaction or event, or when an To assist all parties in understanding and interpreting the^ treatment. accounting standards.

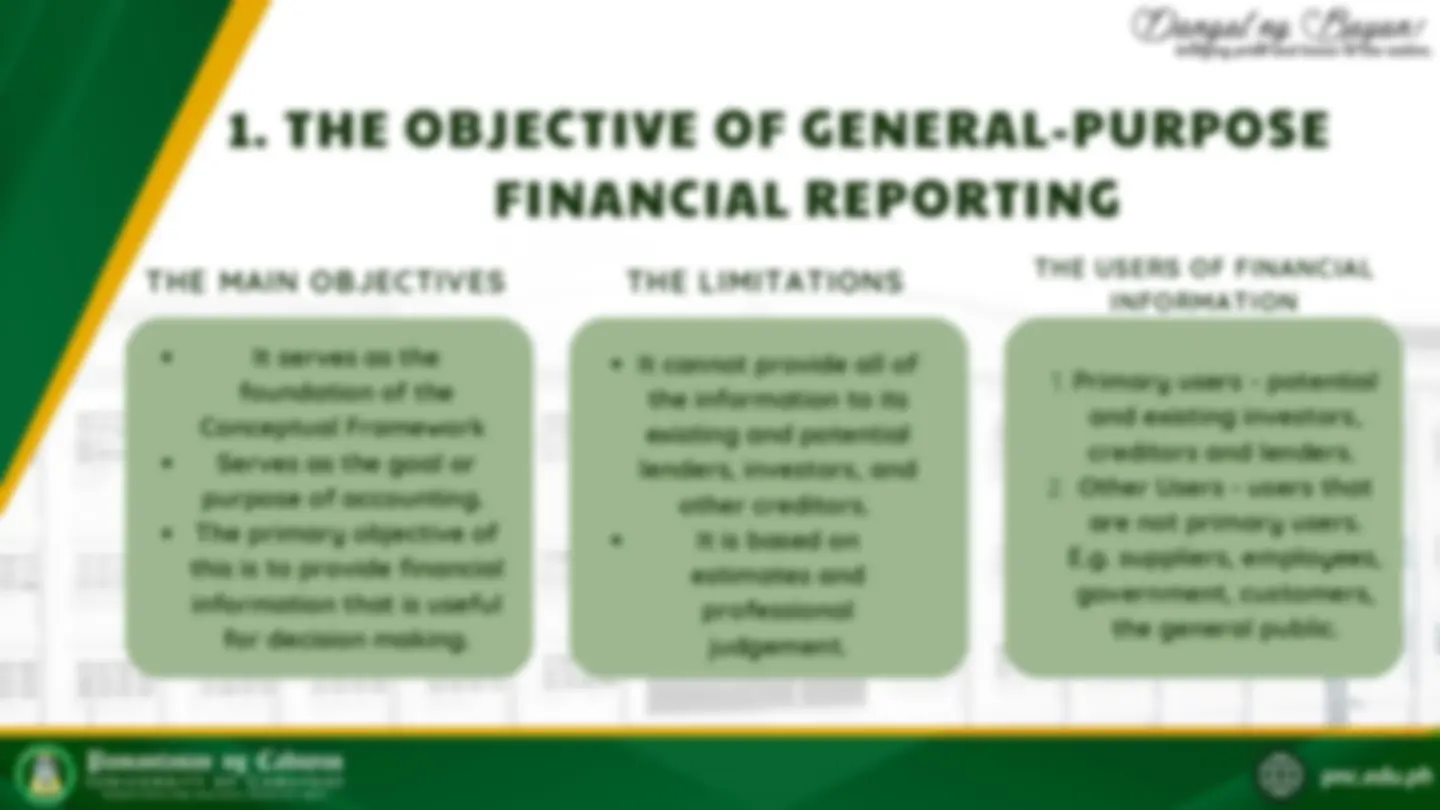

foundation of the^ It serves as the Conceptual Framework Serves as the goal or The primary objective of^ purpose of accounting. this is to provide financial information that is useful for decision making.

It cannot provide all of the information to its lenders, investors, and^ existing and potential other creditors. It is based on estimates and professional judgement.

Primary users - potential and existing investors, Other Users - users that^ creditors and lenders. E.g. suppliers, employees,^ are not primary users. government, customers, the general public.

THE MAIN OBJECTIVES THE LIMITATIONS THE USERS OF FINANCIAL INFORMATION

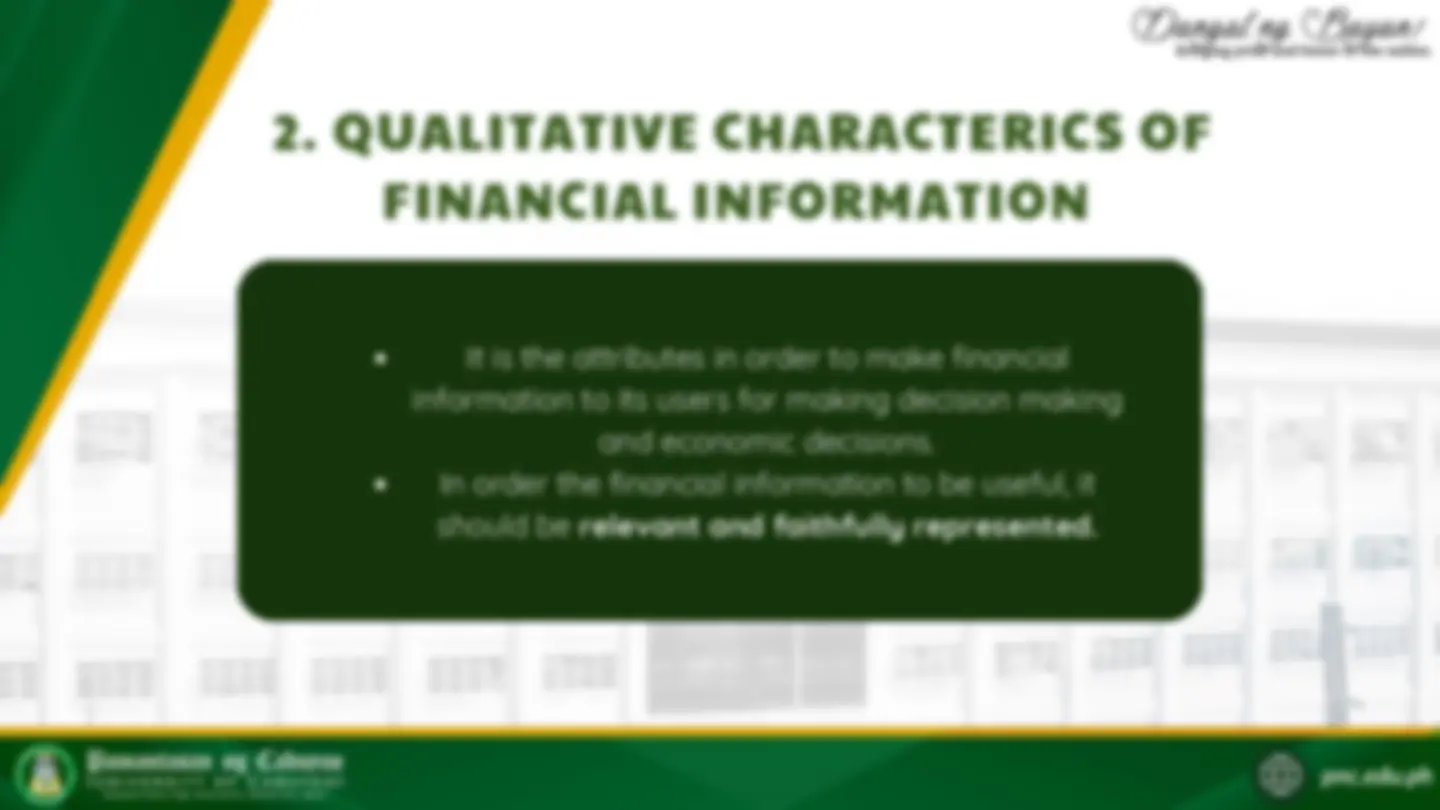

information to its users for making decision making^ It is the attributes in order to make financial In order the financial information to be useful, it^ and economic decisions. should be relevant and faithfully represented.

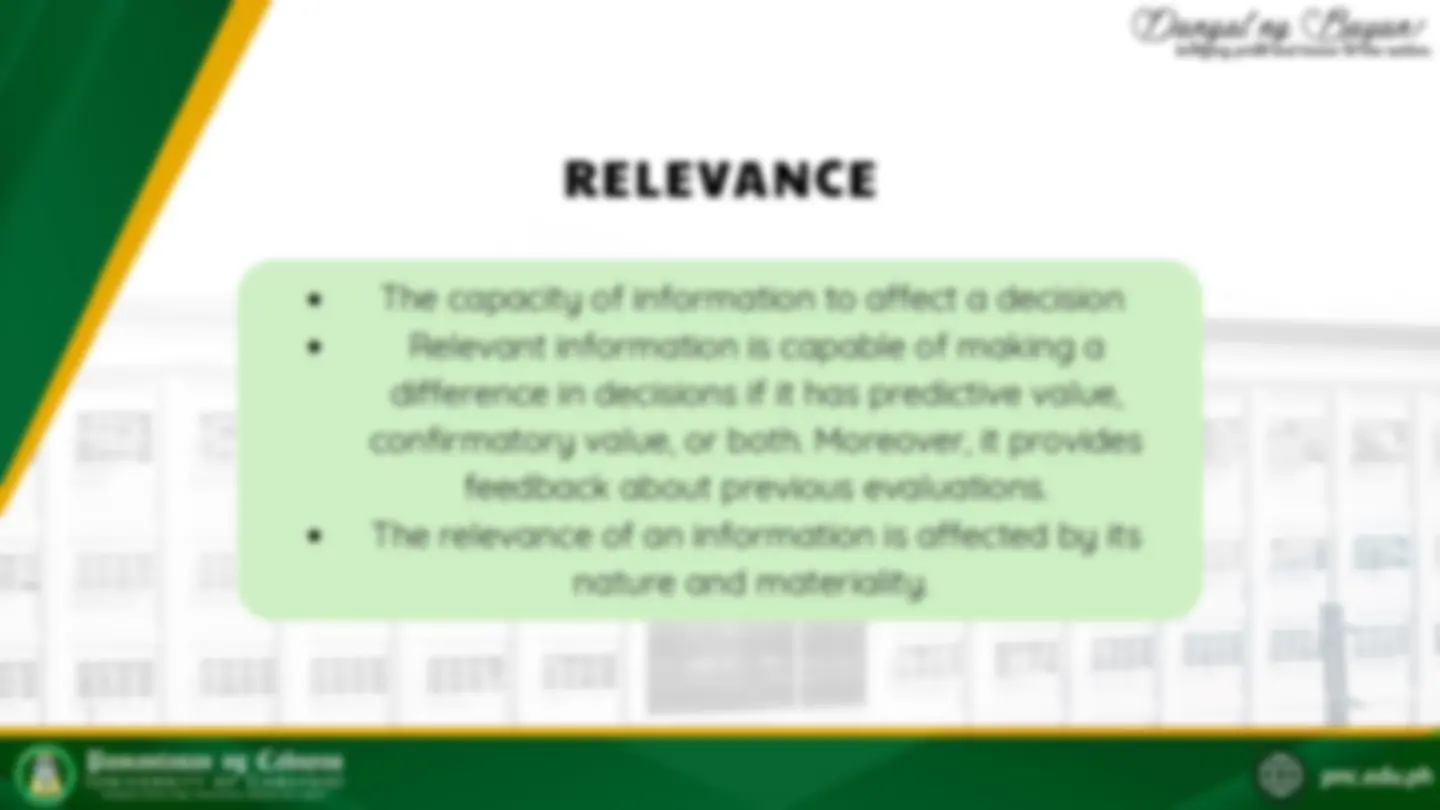

It dictates that strict adherence to accounting standards is not required when the items are not significant enough to affect the decision of a primary user and the fairness of the materiality is just a “quantitative threshold”^ financial statements. In simply terms,

The descriptions and figures presented in the financial reports should match what really existed. In faithful representation, there are three (3) characteristics

All information that are necessary for a user to phenomenon being^ understand the depicted must be included and clearly stated in the reports.

The information contained in the financial reports should be free from bias. The reports should be in favor of one party to another party.

There should be no errors or omissions in the descriptions based on the^ transactions and notes.

COMPLETENESS NEUTRALITY^ FREE FROM ERROR

represented towards the transactions and other^ The financial information should be faithfully transactions and other events are accounted for in^ events to be represented. It is necessary that the accordance with their economic substance and not their legal form. If there is a conflict between economic substance and legal form when it comes to reporting, the economic substance form. will prevail over the legal

INCREASING THE QUALITATIVE CHARACTERISTICS