Customer Profitability

Analysis and Loan Pricing

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Details for loan pricing in banking sector

Typology: Lecture notes

1 / 46

This page cannot be seen from the preview

Don't miss anything!

(^) When deciding what rate to charge, loan officers attempt to forecast default losses over the life of the loan Strong competition for loans tends to increase the banks under-pricing of loans (^) The appropriate procedure is to identify expected and unexpected losses and incorporate both in determining the appropriate risk charge. (^) Credit risk, in turn, can be divided into expected losses and unexpected losses. (^) Expected losses might be reasonably based on mean historical loss rates. (^) In contrast, unexpected losses should be measured by computing the deviation of realized losses from the historical mean.

(^) Floating-rate loans: (^) increase the rate sensitivity of bank assets, increase the GAP (^) reduce potential net interest losses from rising interest rates (^) Because most banks operate with negative funding GAPs through one-year maturities, floating-rate loans normally reduce a bank’s interest rate risk. (^) Given equivalent rates, most borrowers prefer fixed-rate loans in which the bank assumes all interest rate risk. (^) Banks frequently offer two types of inducements to encourage floating-rate pricing:

Index rate (i.e., prime rate) plus a markup of one or more percentage points. Cost of funds (i.e., 90-day CD rate) plus a markup. These methods are simple but may not properly account for loan risk, cost of funds, and operating expenses.

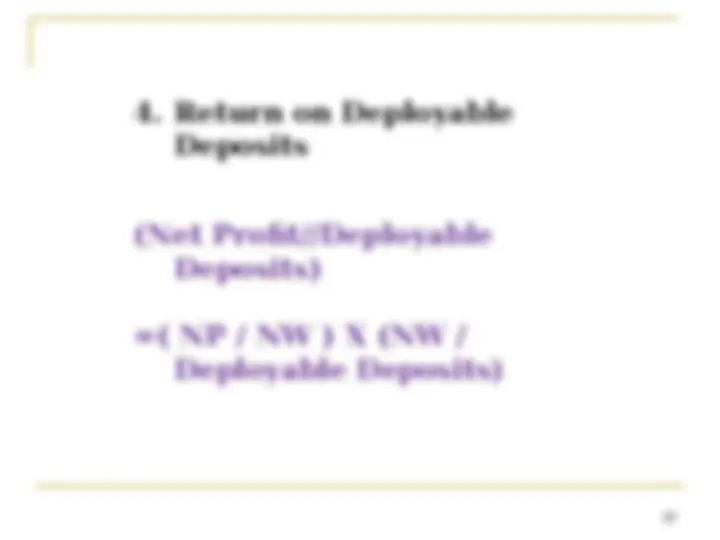

Return on net funds employed: Marginal cost of capital (funds) + Profit goal = (Loan income - Loan expense)/Net bank funds employed Here the required rate of return is marginal cost of capital (funds) + Profit goal.

**Loan Interest Rate = Marginal Cost of Raising Loanable Funds to Lend to Borrower

Nonfund Bank Operating Costs

Estimated Margin to Compensate Bank for Default Risk

Bank's Desired Profit Margin**

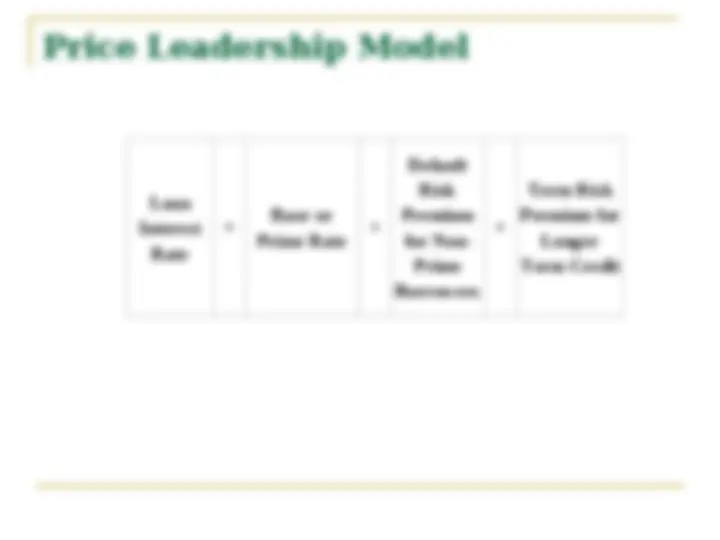

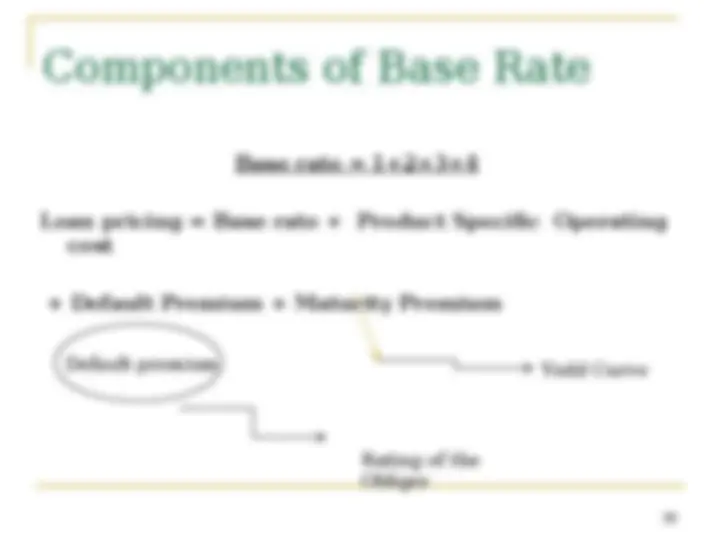

**Loan Interest Rate = Base or Prime Rate

Default Risk Premium for Non- Prime Borrowers

Term Risk Premium for Longer Term Credit**

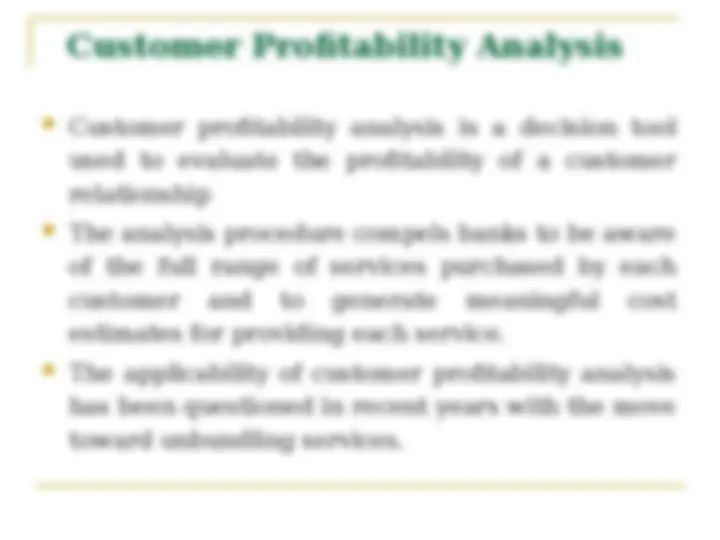

(^) Customer profitability analysis is a decision tool used to evaluate the profitability of a customer relationship The analysis procedure compels banks to be aware of the full range of services purchased by each customer and to generate meaningful cost estimates for providing each service. The applicability of customer profitability analysis has been questioned in recent years with the move toward unbundling services.

Estimate Total Revenues From Loans and Other Services Estimate Total Expenses From Providing Net Loanable Funds Estimate Net Loanable Funds Estimate Before Tax Rate of Return By Dividing Revenues Less Expenses By Net Loanable Funds

(^) These costs include the interest cost of financing the loan, loan administration costs, and risk expense associated with potential default.

…the cost of funds estimate may be a bank’s weighted marginal cost of pooled debt or its weighted marginal cost of capital at the time the loan was made.

…loan administration expense is the cost of a loan’s credit analysis and execution.

…the actual risk expense measure equals the historical default percentage for loans in that risk class times the outstanding loan balance.

Aggregate cost estimates for noncredit services are obtained by multiplying the unit cost of each service by the corresponding activity level. Example: (^) it costs Rs 7 to facilitate a wire transfer and the customer authorizes eight such transfers, the total periodic wire transfer expense to the bank is Rs56 for that account.

In many commercial credit relationships, borrowers must maintain compensating deposit balances with the bank as part of the loan agreement. (^) Ledger balances are those listed on the bank’s books Collected balances equal ledger balances minus float associated with the account Investable balances are collected balances minus required reserves

(^) Facility fee …the fee applies regardless of actual borrowings because it is a charge for making funds available. (^) The most common fee selected is a facility fee, which ranges from 1/8 of 1 percent to 1/2 of 1 percent of the total credit available Commitment fee …serves the same purpose as a facility fee but is imposed against the unused portion of the line and represents a penalty charge for not borrowing Conversion fee …a fee applied to loan commitments that convert to a term loan after a specified period (^) Equals as much as 1/2 of 1 percent of the loan principal converted to term loan and is paid at the time of conversion

Loanamount

The target profit is then based on a minimum required return to shareholders per account.