Download macroeconomics class 20 and more Lecture notes Macroeconomics in PDF only on Docsity!

CHAPTER 22

Inflation, expectations and credibility

key questions

2

- (^) The definition and measurement of inflation

- (^) Causes and effects of inflation

- (^) The Quantity Theory

- (^) Interest rates and Inflation Fisher hypothesis

- (^) The Philips Curve - some explanations & cases

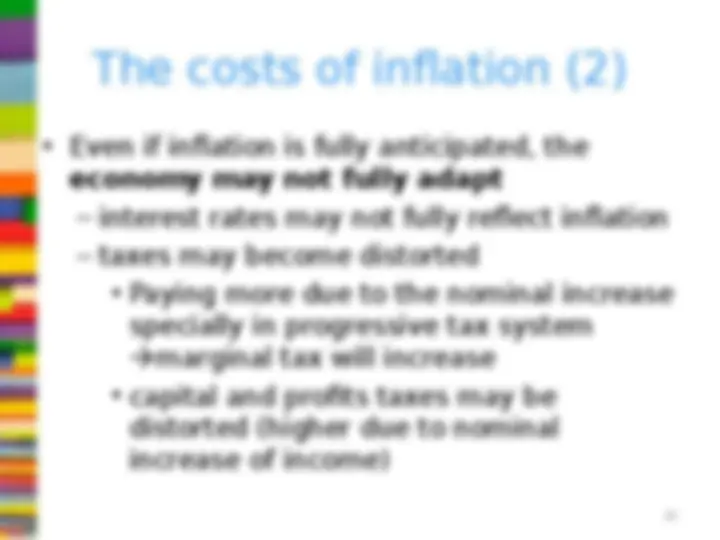

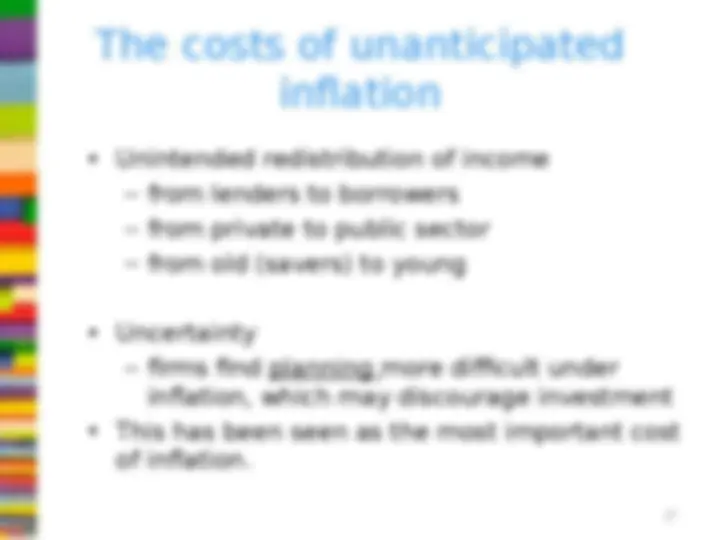

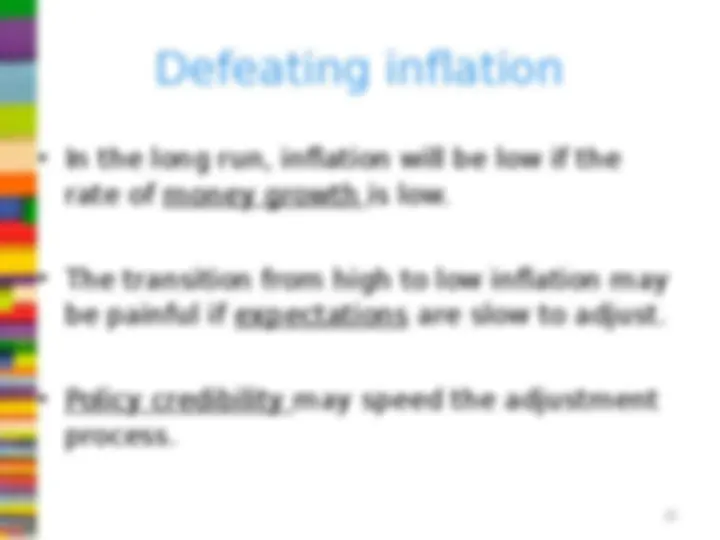

- (^) The Costs of inflation & how to defeat it

Some questions about inflation

- (^) The size of inflation in UK & Sweden

- (^) What are the causes of inflation?

- (^) What are the effects and hence costs of inflation?

- (^) What can be done about it?

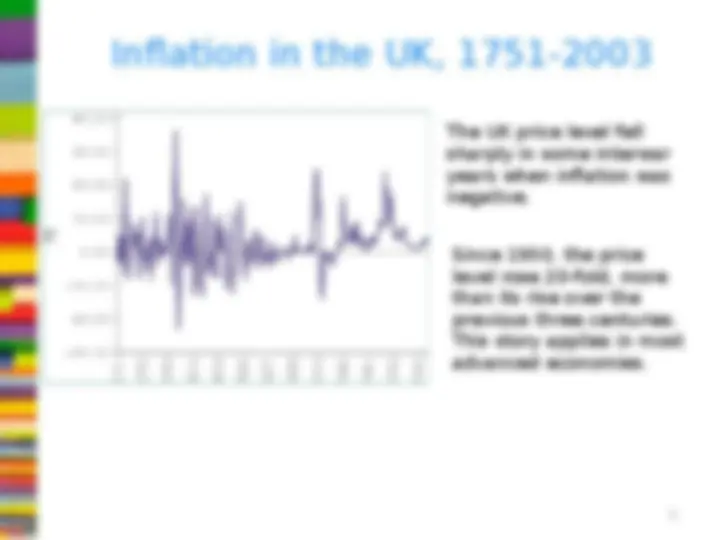

Inflation in the UK, 1751- The UK price level fell sharply in some interwar years when inflation was negative. Since 1950, the price level rose 20-fold, more than its rise over the previous three centuries. This story applies in most advanced economies.

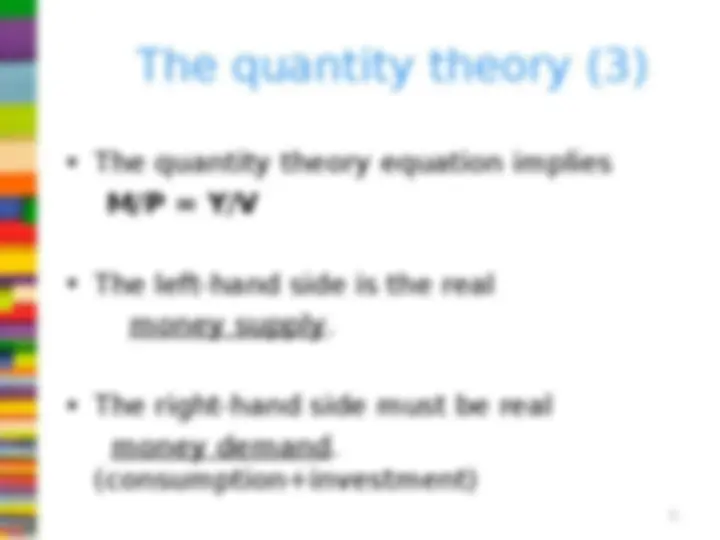

The quantity theory (1)

- (^) The quantity theory of money says:

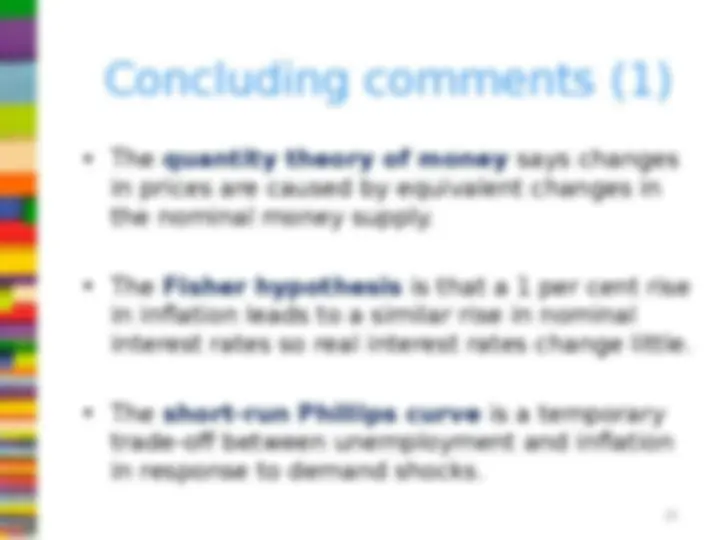

- (^) “Changes in the nominal money supply lead to equivalent changes in the price level (and money wages) but do not have effects on output & employment.”

- (^) PY = MV

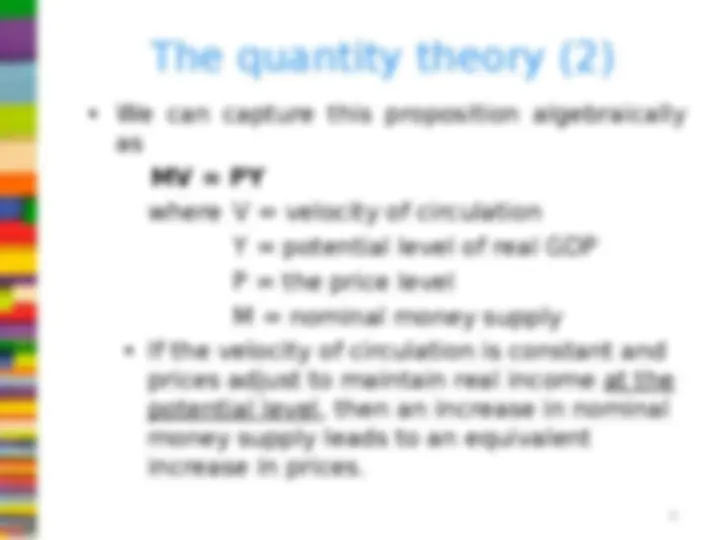

The quantity theory (2)

- (^) We can capture this proposition algebraically as MV = PY where V = velocity of circulation Y = potential level of real GDP P = the price level M = nominal money supply

- (^) If the velocity of circulation is constant and prices adjust to maintain real income at the potential level, then an increase in nominal money supply leads to an equivalent increase in prices.

Some implications of the quantity theory

- (^) monetary policy can try and fix P over time, in which case P M

- (^) The equation says prices and money are correlated, but is agnostic on which causes which.

- (^) With an intermediate target for nominal money, the causation flows from money to prices.

- (^) With a target for prices or inflation, the causation flows the other way.

The short run

- (^) Also, in the short run, the link between money and prices may be broken if: - (^) the velocity of circulation is variable - (^) prices are sluggish

- (^) For all the above reasons, we must therefore interpret the quantity theory with care.

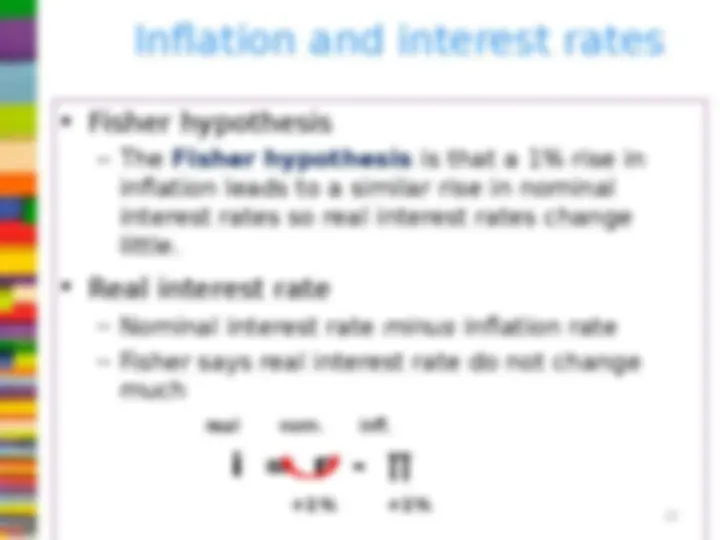

Inflation and interest rates

- (^) Fisher hypothesis

- (^) The Fisher hypothesis is that a 1% rise in inflation leads to a similar rise in nominal interest rates so real interest rates change little.

- (^) Real interest rate

- (^) Nominal interest rate minus inflation rate

- (^) Fisher says real interest rate do not change much real nom. infl. i = r - ∏ +1% +1%

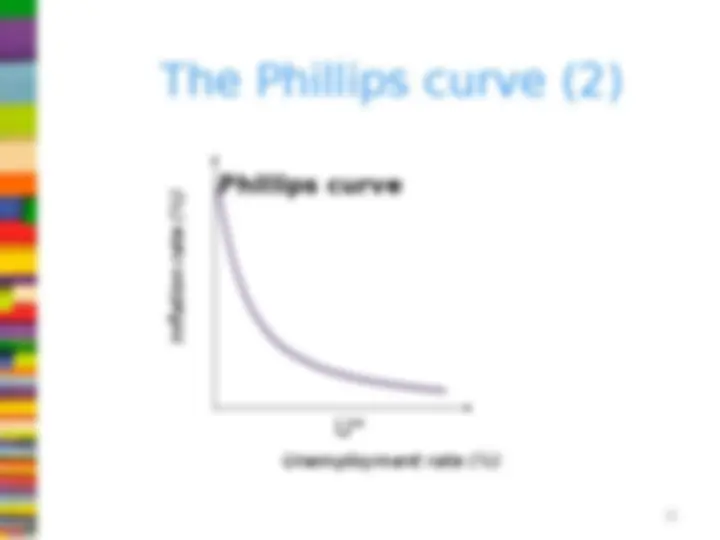

- (^) In 1958, Prof. A W Phillips demonstrated a statistical relationship between annual inflation and unemployment in the UK.

- (^) The Phillips curve relates higher unemployment to lower inflation.

- (^) It implies we can trade-off higher inflation for lower unemployment and vice versa.

The Phillips curve (1)

The Phillips curve (3)

Y1 Y Yf (Unemployment rate DUE TO Yf -Yi) O 45

AD

Y

ADAD 11 AD 2 If A Demand curve AD Increases between Y1 and Y Prices increases as Unemployment decreases

The long-run Phillips curve (1)

- (^) The classics

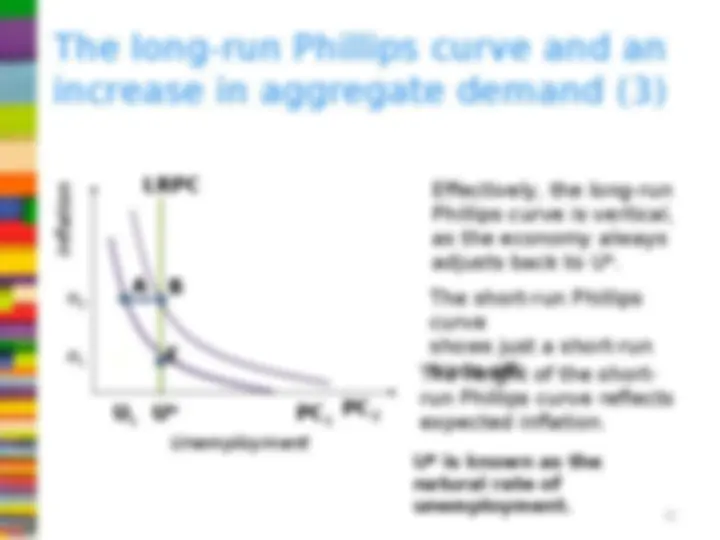

- (^) The vertical long-run Phillips curve implies that sooner or later, the economy will return to U*, whatever the inflation rate.

- (^) The position of the short-run Phillips curve depends on expected inflation.

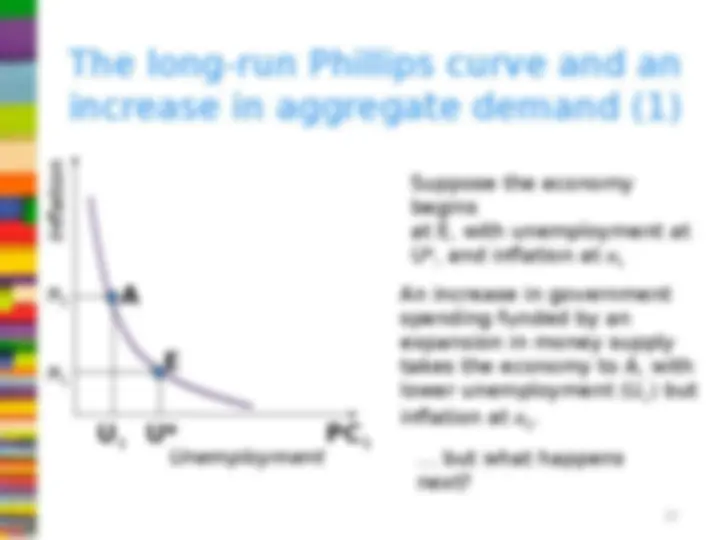

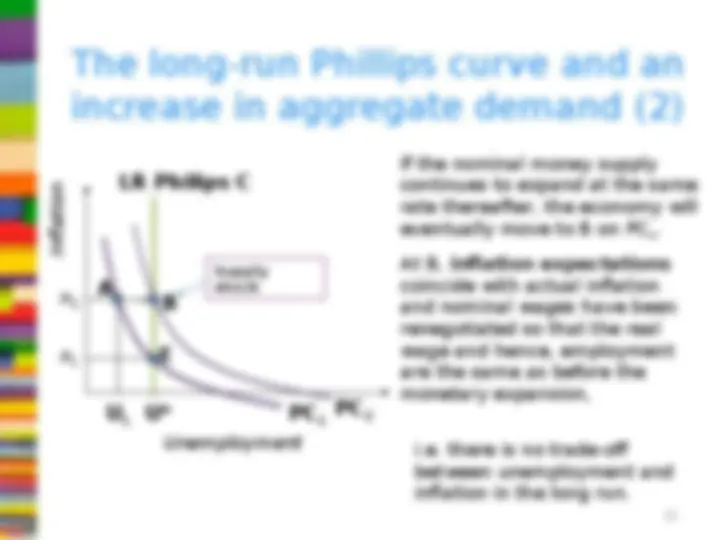

U* The long-run Phillips curve and an increase in aggregate demand (1) … but what happens next? Unemployment Inflation PC 1 Suppose the economy begins at E, with unemployment at U*, and inflation at 1 E 1 U 1 An increase in government spending funded by an expansion in money supply takes the economy to A, with lower unemployment (U 1 ) but inflation at 2. 2 A

A 2 If the nominal money supply continues to expand at the same rate thereafter, the economy will eventually move to B on PC 2. At B, inflation expectations coincide with actual inflation and nominal wages have been renegotiated so that the real wage and hence, employment are the same as before the monetary expansion, i.e. there is no trade-off between unemployment and inflation in the long run. LR Philips C Unemployment Inflation U PC 1* 1 E U 1 PC 2 B The long-run Phillips curve and an increase in aggregate demand (2) Supply shock