Download Macroeconomics Notes ECON1002 and more Lecture notes Macroeconomics in PDF only on Docsity!

MACRO-ECONOMICS LECTURE NOTES

Week 1– Unit 1

Learning Outcomes:

- Define Macroeconomics and distinguish between Macroeconomics and Microeconomics.

- Define the concepts of Gross Domestic Product, Gross National Product, Value Added, Nominal vs Real Income.

- Explain the circular flow of income.

- Identify measurement issues related to GDP as an indicator. Review- Microeconomics is the study of the choices of individuals, the study of decisions made by enterprises such as businesses firms and the interaction of those choices and decisions in social frameworks such as markets. Macroeconomics is the study of the national economy and the global economy. The study of the determination of economic aggregates and averages. It describes the behaviour of all households, firms, and the government in determining. Macroeconomics looks at the economy, dealing with such aggregate phenomena as growth in total output and living standards, commonly called ‘economic growth’, business cycles, inflation, unemployment, and the balance of payments. It also asks how government can use their monetary and fiscal policy instrument to help stabilize the economy. Macroeconomic concerns:

- Employment

- Inflation

- Economic Growth- Gross Domestic Product

- Income Distribution

- Trade Balance Examples of Microeconomic and Macroeconomic Concerns

Microeconomics Production Production/Output in Individual Industries and Businesses How much steel? How many offices? How many cares? Prices Price of Individual Goods and Services Price of medical care Price of gasoline Apartment rents Income Distribution of Income and Wealth Wages in the auto industry Minimum wages Employment Employment by Individual businesses & industries. Jobs in the steel industry Number of employees in a firm Macroeconomics Production National Production/ Output Total Industrial Output Gross Domestic Product (GDP) Growth of Output Prices Aggregate Price Level Consumer Prices Producer Prices Rate of Inflation Income National Income Total Wages and Salaries Producer Prices Rate of Inflation Employment Employment & Unemployment in the Economy Total number of jobs Unemployment rate

- Exports : Sales of goods and services to foreign residents. Payments received for exports constitute another injection into the circular flow. - Withdrawals : are variables in an economy that leak out of the circular flow of income and reduce the size of national income. Withdrawals include savings, taxation, and imports. Elements: Injections and Leakages Leakages = S (savings) + T (taxes) + M (imports) Injections = I (injections) + G (government spending) + M (imports) Income in an economy therefore arises from: Imports = C (c onsumption expenditure or spending) + I (injections or investments) + G (government spending) – M (imports) Consumer Expenditure = Y (income) – S (savings) – T (taxes) Circular Flow of Government

Calculation of National Accountants Total Product / National Product Total/ National Income Total/ National Expenditure --- describe essentially the same flow. Therefore, National Product = National Income= National Expenditure so long as leakages = Injections. Three methods used in calculating national accounts: Output Method, Income Method and Expenditure Method. GDP, GNI AND GNP

- Gross Domestic Product (GDP) -This can be calculated in three different ways: a. as the sum of values added by all producers of both intermediate and final goods. b. as the income claims generated by the total production of goods and services c. as the expenditure needed to purchase all final goods and services produced during the period. Output Method: Factor incomes arise from the sale of goods and services produced in the economy; one such way of calculating income is therefore to add up the value of all output created in the relevant period mainly for sale in the market. The value is measure by the supply price of output i.e., the price a firm receives for its product.

- The determination of GDP in the short run depends on the behaviour of the key components of aggregate expenditure.

- Consumption spending depends on disposable income and wealth.

- Investment spending depends on interest rates and business confidence.

- A necessary condition for GDP to be in equilibrium is that desired domestic spending equals actual output.

- There are two approaches to showing equilibrium national income: - a. The income expenditure approach b. The injections withdrawals approach Theory of GDP Determination The national accounts measure actual spending in each of the four categories C + I + G + NX (net exports (exports – imports) The theory of GDP determination deals with desired spending in each of these four categories: Spending can be:

- AUTONOMOUS – independent of income changes

- INDUED - dependent on income changes Simple Keynesian Model- Consumption C= Private Consumption Disposable income (income after taxes) can be spent and saved therefore: The consumption function determines the level of C and relates the total desired consumer spending of the personal sector to the variables that affect it. CONSUMPTION FUNCTION

C= A+ b(Yd) Disposable income

‘C’ represents total consumption

‘A’ represents autonomous consumption ‘b (Yd)’ represents induced consumption. Yd (disposable income) = Y-T (income-taxes) EXAMPLE: What does this mean? If Y = 1000 T- = 10% Yd= 1000- 10% (1000) = 900 A=200 b(Yd)= 0.75 (yd) C = 200+ 0.75(Yd) =200+ 0.75(900) =200+ = MPC, APC vs MPS, APS Because disposable income is either spent or saved then: APC + APS = 1 MPC + MPS = 1

- APC is the total consumption spending divided by total disposable income (C/Yd).

- MPC (or what was represented as b) is the percentage of each dollar change in income that is consumed. The MPC is therefore the slope of the consumption function (ΔC / ΔY)ΔC / ΔY)C / ΔC / ΔY)Y).

Worked Example ...

If the consumption function is C= 100 + 0.8 Yd Marginal Propensity to Consume, Average Propensity to Consume vs Marginal Propensity to Save, Average Propensity to Save 100+0.8(1000) = 900 1000-900= 100 MPC= 0. MPS= 0. Autonomous Consumption= 100

Completing the Simple Keynesian Model The simple Keynesian model is expressed in terms of Consumption (C) and Investment (I). Recall C is determined by the consumption function. Introducing Investment (I). Desired Investment Spending It is the most volatile component of GDP. Planned investment spending by firms is likely to be affected by a range of factors. The 2 most important are:

- Interest Rate

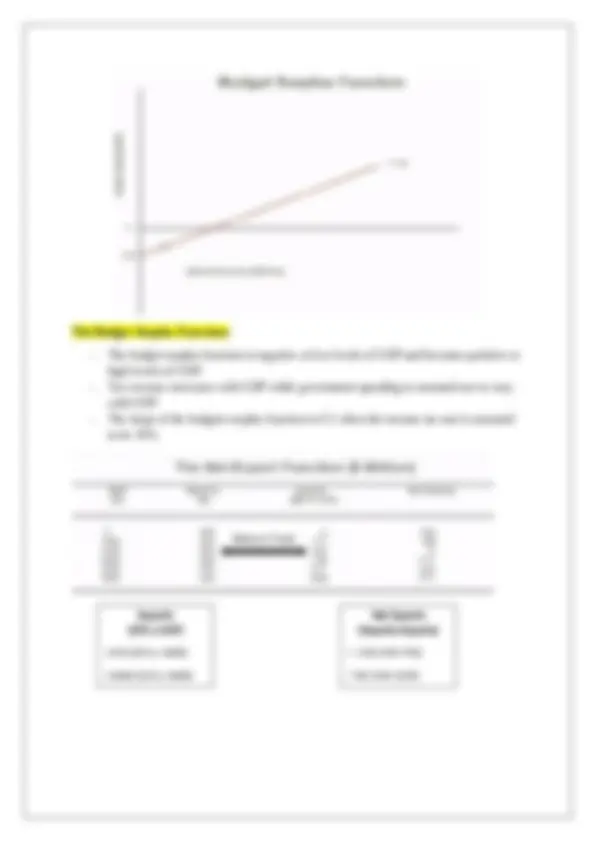

- Level of Business Profits The Keynesian Model treats investment as autonomous because Keynes saw that expectations were dominant in determining the level of investment and not so much current income. The Aggregate Expenditure Function in a Closed Economy with No Government ($ Million)

Simple Keynesian Model: EQUILIBRIUM INCOME The Equilibrium level of GDP occurs where aggregates desired spending equals total output. By combining C and I the simple Keynesian aggregate demand function is determined. In this simple model equilibrium can also be shown where leakage = injection, i.e., savings = investment. At any level of GDP at which aggregate desired spending is greater than output, there will be a pressure for GDP to rise. At any level of GDP for which aggregate desired spending is less than output there will be a pressure for GDP to fall. 2750 1150 670 2500 1500 500

Equilibrium in an Open Economy with Government G-Government Spending

- Government consumption contributes to aggregate spending in the same way as any other component of autonomous spending (such as investment). - Taxes affect private consumption via their effect on disposable income. - The Budget balance is the difference between total government revenue and total government spending i.e., Taxes – Government Spending. - T > G = Budget Surplus - T < G = Budget deficit Government Surplus (T-G) =130 (300-170) Net Taxes (10% of GDP) =175 (10% x 1750) =400 (10% x 4000) Consumption = Autonomous AND Induced Investment = Autonomous Government Spending = Autonomous Taxation = Induced Exports = Autonomous Imports = Induced *Autonomous - Not changing *Induced - Changing All the components of the aggregate expenditure function

The Budget Surplus Functions

- The budget surplus function is negative at low levels of GDP and becomes positive at high levels of GDP. - Tax revenue increases with GDP while government spending is assumed not to vary with GDP. - The slope of the budgets surplus function is 0.1 when the income tax rate is assumed to be 10%. Balance Trade Net Exports (Exports-Imports) = -210 (540-750) -710 (540-1250) Imports (25% x GDP) =250 (25% x 1000) =1000 (25% x 4000)

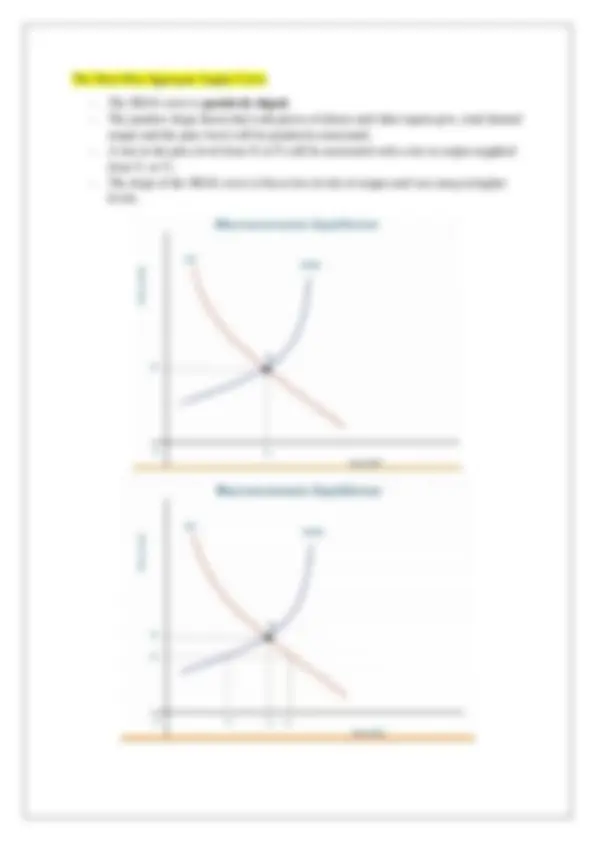

Equilibrium GDP = 2000 AE=Y Equilibrium GDP

- GDP is in equilibrium where aggregate desired expenditure (AE) equals national output - In the figure, equilibrium GDP occurs at E 0 where AE intersects the 45^0 degree line. - If GDP is below Y 0 desired AE will exceed national output and production will rise. 415

- If GDP is above Y 0 desired AE will be less than national output and production will fall. - When saving is the only withdrawal and investment is the only injection, the equilibrium level of GDP is also that were saving equals investment or where leakages= injections. Changing Equilibrium GDP National Equilibrium Income can be changed by chances to the injections. For example , If government spending increases…

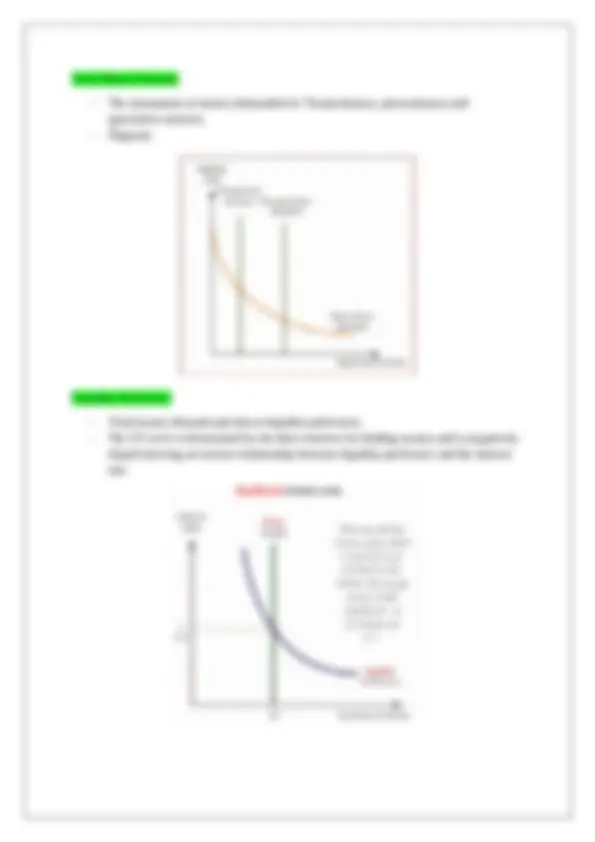

The Simple Multiplier

- An increase in the autonomous component of desired aggregate expenditure increases equilibrium GDP by a multiple of the initial increase. - The initial equilibrium is at E 0 where AE0 intersects the 45^0 line. Here desired expenditure equals national output. - An increase in autonomous expenditure of A then shifts the AE function up to AE 1 - Because desired spending is now greater than output, production and GDP will rise. - Equilibrium occurs when GDP rises to Y 1 - Here desired expenditure E 1 equals output Y 1

Multiplier -The simple multiplier is the multiplier when the price level is constant.

- It is equal to 1/ (1-z) where Z is the marginal propensity to spend out of national income.

- Thus, the larger z is the larger multiplier. It is a basic prediction of macro-economic that the simple multiplier relating $1 worth of increased spending on domestic output to the resulting increase in GDP is greater than unity. Notes on the Multiplier: Changes in Aggregate Expenditure K = 1/ (1-0.8 [1-0.1] + 0.2) = 1/ (1-0.8 [0.9] + 0.2) = 1/ (1-0.72 + 0.2) = 1/ 0. = 2.08 (Multiplier)

(K)

c= 0. t= 0. m= 0. 10 – Exports 0.20- Imports C = MPC (Marginal Propensity to Consume) T = MPT (Marginal Propensity to Tax) M = MPM (Marginal Propensity to Import)