Management Project

Bank Alfalah Limited

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

This is project report for Management Practices course submitted to Shankar Jamedar at Agra University. It includes: Management, Project, Products, Services, Hierarchy, Organiztional, Culture, Competitive, Job, Analysis

Typology: Study Guides, Projects, Research

1 / 26

This page cannot be seen from the preview

Don't miss anything!

Bank Alfalah Limited was incorporated in June 21st, 1997 as a public limited company under the Companies Ordinance 1984. Its banking operations commenced from November 1st ,1997. The bank is engaged in commercial banking and related services as defined in the Banking companies ordinance 1962. The Bank is currently operating through 350 branches in different cities, with the registered office at B.A.Building, I.I. Chandigarh, Karachi. Since, its inception as the new identity of H.C.E.B after the privatization in 1997, the management of the bank has implemented strategies and policies to carve a distinct position for the bank in the market place. Strengthened with the banking of the Abu Dhabi Group and driven by the strategic goals set out by its board of management, the Bank has invested in revolutionary technology to have an extensive range of products and services. This facilitates their commitment to a culture of innovation and seeks out synergies with clients and service providers to ensure uninterrupted services to its customers.

The bank perceived the requirements of customers and matches them with quality products and service solutions. During the past five years, bank has emerged as one of the foremost financial institution in the region endeavoring to meet the needs of tomorrow as well as today. To continually upgrade the quality of service to the customers, training of team members in all the integral aspects of banking, customer service and IT was specially focused. The portfolio concentrates on all aspects of conventional banking as well as the financial needs of corporate sector. Dynamic and high value product includes Car Financing, Home Financing, Rupee Travelers Cheques, Credits Cards, Debit Cards, On

line Banking, ATM and consumer Durables. In addition to this, Islamic Banking Division is a recent initiative, which operates as separate branch. It offers Shariah Compliant products through a network of five branches, which have been increased to 150 by the year 2010.The bank is committed to combine all it s energies and resources to bring high value, security and satisfaction to its customers, employees and shareholder. The Bank has invested in revolutionary technology to have an extensive range of products and services. This facilitates commitment to a culture of innovation and seeks out synergies with client and service providers to ensure uninterrupted services to it customers.

Board of directors

H.E. Sheikh Hamdan Bin Mubarak Al Nahayan Chairman

Mr. Mohammad Saleem Akhtar Chief Executive Officer Mr. Abdulla Nasser Hawalileel Al-Mansoori

Mr. Abdulla Khalil Al Mutawa Mr. Ikram Ul-Majeed Sehgal

Mr.Khalid Mana Saeed Al Otaiba Mr. Nadeem Iqbal Sheikh

(Ref: www.bankalfalah .com)

Products and services

With the mission to provide all-encompassing banking services to the customer bank Alfalah has uniquely defined menu of financial products ,currently it is one of the most comprehensive portfolios of personalized financial solutions that are custom tailor to serve the requirements not only foe conventional customers but also to fulfill the needs for corporate sector

Car financing Rupee traveler check Online banking Credit cards ATMs Home financing Islamic banking Corporate and structured financing

Car financing is one of the major renowned products of bank Alfalah and can be utilized in terms of financing of used vehicles, loan against car, balance transfer facility, refinancing facility only for Alfalah customers) and it is characterized in terms of

Lowest markup Lower insurance Quick processing Lower down payment

Major features of bank Alfalah home financing are the lowest markup, quick processing, multiple repayment options and free valuation. It has been bifurcated in terms of” home buyer, home construct, home improver, home balance transfer facility”

Financing limit : up to Rs 10,000,000/- Tenure : up to 20 years Equity participation: 30%borrowers/70%bank

Rupee travelers checks are as good as cash and are accepted at the major shops, travel agents, hotel business establishment and all over the country and abroad. This service is being offered to facilitate instant fund availability to travelers and business people who use to carry a large sum of money with them.

Bank Alfalah VISA card is everywhere and globally accepted and welcomed at location displaying it is accepted at nearly 30 million merchants 870,000 ATMs in more than 150 countries around the globe and over 10,000 establishments in Pakistan. Alfalah VISA pays for shopping, travel, entertainment, meals and much more.

Bank Alfalah limited presents Alfalah hilal card, the first VISA electron international debit card which gives unlimited access to current/saving accounts with a simple swipe at millions of retail shops and ATMs worldwide. The Alfalah hilal card come with the host of convenience and benefit combined with the combined with the wide reach of VISA network enabling it to be accepted at more than 840, ATMs and 13 million retail outlets, around the world making it the most acceptable debit card available in Pakistan.

To provide enhance and value added products to the customer bank is constantly starving for additional facility. Bank provide fully automate online full banking facility to customers enabling them to carry out banking transactions like balance inquiry, statement request, product information and exchange rate.

The bank offer 24 hours self service bank facility to its customers on country wide basis through development of automate teller machine. This system allows the banking facilities such as cash withdrawal, fund transferring, cash deposit, balance inquiry, account statement. Electronic cash dispensing facilities are available in major cities of Pakistan. All ATMs are linked through the state of the art satellite based communication system which offers 24 hour real time service.

A separate division is initiated which operates as separate branch. it offers Shariah complaint products through a network of 5 branches .Islamic banking has launched following products with the perception that these are in the accordance with the Shariah principle.

a. Alfalah Musharik homes b. Murabaha finance c. Alfalah car ijrah

The portfolio concentrate on all the aspects of conventional banking as well as the financial need of corporate sector including dynamic and higher value product

Loaning against securities Letter of credit Letter of guarantee Demand finance Cash finance

(Ref; www.bankalfalah.com)

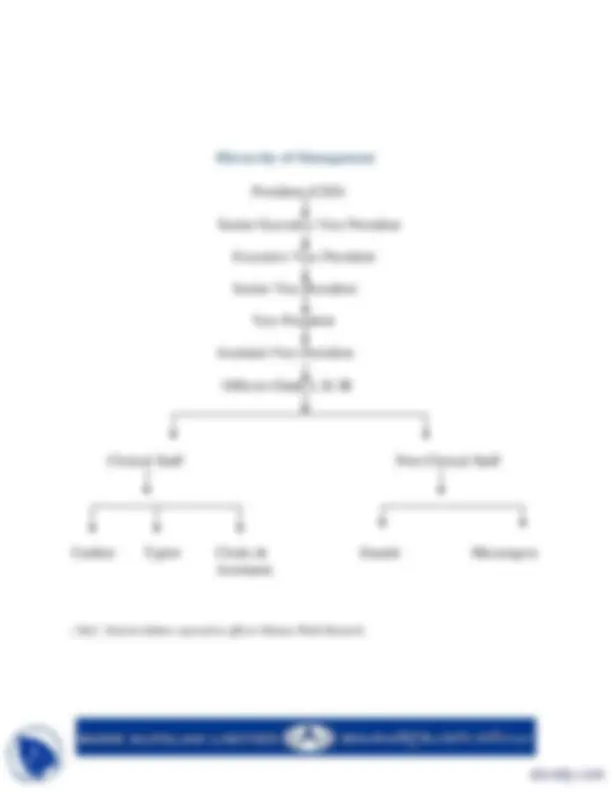

Posts and structure within a Branch

Branch manager

Operations staff

Clearing dpt remittance dpt accounts dpt cash dpt accounts IT accounts opening dpt closing

dpt dpt

Clearing remittance accountants chief cashier operations IT operations officer officer & auditors cash officers officer officer officer cash sorters opening closing

(Reference : Naeem Akhtar operation officer Khana pul branch.)

Clearing departments: This department clears the cheques of other banks that have been deposited in Bank Alfalah or the cheques of bank Alfalah deposited in other banks.

Remittance department: This department deals with every type of remittances.

Accounts department: This department deals with accounts section i.e. book and record keeping.

Cash department:

The most attractive department of the bank. This deals with the cash receiving cash payments and sorting and saving of cash like matters.

Accounts opening department: This department deals with all the new opening accounts. Here all the documentation and other required steps for the opening of accounts are performed.

Accounts closing department: This deal with the closing of accounts affairs.

IT department : This department is considered as the most needed department now a days because it provides and take care of all the computer systems of the bank.

(Ref: Naeem Akhtar operation officer Khana pul Branch)

FAYOL’s principles of management and Bank Alfalah

Division of work: At bank Alfalah there is a proper division of work. They have hired different people with different work specializations and they have separate departments for separate types of tasks, like accounts dpt, cash dpt, IT dpt and many more like these.

Authority : in bank Alfalah the authority is with is with the top level managers, with in the branch it is the characteristic of a branch manager and in the specific department of the branch it is with the in charge of the department.

Discipline : The employees and managers of bank Alfalah are very disciplined because they honor and respect the rules and regulations.

Unity of command: This principle is seen in bank Alfalah because the employees receive orders from the branch manager and he in turn gets it from the regional manager.

Unity of direction: This principal is applied because the employees have only one direction i.e. profit maximization through increased customer orientation. Subordination of individual interests to the general interest: The employees do subordinate their personal interests to the general interest that is they follow and obey all the rules and do all the jobs they don’t want to or they are less willing to do that.

Remuneration:

E-business and Bank Alfalah

As the world of banking is changing and a new trend of computer based banking has emerged and accepted worldwide so has done the bank of Alfalah .it has accepted this change and have benefited itself from it a lot. The bank of Alfalah is using computer and information technology in the following fields.

Data storage: The data that was previously stored in the big registers, folders and files now are stored in the computer. The accessing data time from registers have been decreased to in a great deal. Now any manger or operation officer can access the account information of a client within the fraction of minutes.

Online banking: The greatest advantage of e-business is e-banking that is any client or customer can withdraw and add amount to his account from different cities of the country previously we could do these from the branches with in a city.

Online information: Any customer can access his account status any time online.

Social responsibility and bank Alfalah:

Classical view: While interviewing the operation officer of bank Alfalah Khana pul branch we came to know that bank Alfalah acts under the classical view which says that managements only social

responsibility is the profit maximization. Besides he told us that the bank abbeys the rules and regulation regarding the social benefits so we can say that this bank is at the social obligation level because it has proper disposing channel for disposing the wastes and rough supplies. Besides he told us that bank Alfalah contributes his share in different natural disasters like the earthquake of October, 8, 2005 and it banned the usage of SUGAR in Branches during the sugar crisis in the country so we can say that it is socially responsive also.

(Ref: Nida Javed and Abdul Basit Ali operation officer and BDO respectively in Khana pul branch and satellite town branch)

Organizational culture

Outcome orientation:

The culture of bank Alfalah is more outcome oriented. One of the operations officer said that it is

more profit oriented rather than other things. He said that it is because that in banking profit is

the sign of life and it can keep you going. That’s why the main focus of bank Alfalah is on profit maximizing.

People orientation:

While talking about the people orientation the officer told us that we have to deal with two

groups of people first are the employees and second are the customers.

Employees:

Bank Alfalah is has specified strong rules and regulations for its employees. Employees have to

follow them and have to produce maximum output irrespective of how hard they have to work

for it. Once the targets have been aimed then employees have to achieve that.

Customers:

Bank Alfalah is very much customer oriented .said the branch manger that customers are our

keys to maximized profit and keep going. Bank Alfalah cares a lot about its customers it wants to

satisfy the customers either by producing value added products or packages ,or superior services.

Bostan consulting group (BCG- matrix )

The businesses whose growth rate as well as market shares are very higher and those who are the leader of markets.

The businesses having big market share but low growth rate, and they earned a lot amount of

cash due to their reputation.

Businesses growing highly but having low market share than star’s businesses.

According to Mr. Basit Ali (BDO) and the following website Bank Alfalah lies under the

category of STAR in the BCG MATRIX, as there growth rate and market share is very high.

( Ref:

http://www.scribd.com/search?cat=redesign&q=bcg+matrix+of+bank+alfalah&x=0&y=0 and

Abdul Basit Ali Business development officer Satellite Town Branch.)

SWOT analysis of an organization helps find out about the strengths and weaknesses the organization has internally and the opportunities and threats it faces from the external environment. This analysis leads to a clear positioning of the organization’s management and its position in the market along with evaluation of the overall performance of the bank.

The following are the strengths, weaknesses, opportunities and threats of Bank Alfalah limited

If we say, today the rates of challenges are too high but simultaneously the rate of opportunities is also high. It is mandatory to try to make progress with consistency as well as to adapt changes with the needs of time, in order to cope up with both conditions. In the prevailing scenario, Bank Alfalah could penetrate further and could capture various corporate customers in addition to the retail customers by expanding their network.

In addition to the excellent routine banking, it has earned a good name by offering special products like car financing, home financing and credit card. So, the penetration of these products could enhance the market share.

In the rapidly growing industry of Pakistan, launching of another SBU, Alwarid Mobile will be an excellent addition towards the credibility as well as enhancement of Bank Alfalah’s market share.

Bank Alfalah has launched another division known as Islamic Banking. This new aspect will also attract a large number of people, who don’t want to deal with interest bearing banking. Hence, it’s a new opportunity where competitors are limited.

THREATS

While doing business, threats are part of the game. Especially, in this era, most of the financial institutions are working as Private Limited Company and facing or have a fear of threat from their competitor as well as new entrants.

In order to maintain as well as to enhance the market share, banks always try to introduce new schemes / packages. Hence, the environment is very much innovative and adaptive to the needs of customers.

Though Bank Alfalah has a strong footing and maintain a good number of loyal customer, still bank has threats in various sectors:

a) In Car Financing MCB & UBL are threats however, the expected car financing of ABN Ambro could also be a threat for Bank Alfalah.

b) In Home Financing Union Bank or to some extent NBP are threats.

( Ref:

http://www.scribd.com/search?cat=redesign&q=bcg+matrix+of+bank+alfalah&x=0&y=0 and

Nida Javed and Abdul Basit Ali Business development officer Satellite Town Branch.)

Competitive analysis

The sole purpose of competitive analysis is to determine the organization’s or company’s

position when compared with its competitors in the industry environment.

PORTER discussed five competitive forces in the competitive analysis of the company. Here is

Bank Alfalah’s competitive analysis with respect to porter’s five competitive forces.

It’s a threat of having the new entrants in the same industry. For bank Alfalah this threat is high

as more new banks are being launched in the country. Its negative for bank Alfalah as they have

now to think more about their products and services. The latest entrances in this industry are of

BARCLAYS, RBS, SILKBANK and many more.

Customers are influenced by the brand name of bank Alfalah “the caring bank”. The bank sets its own prices not influenced by the customer, due to the low bargaining power bank Alfalah gets

high profit and has positive effect on company.

Bargaining power of supplier for bank Alfalah is low. The suppliers of any particular bank are

their customers, investors, and stakeholders. Bank Alfalah has many customers and stakeholders

because its parent company is in Abu-Dhabi

Threats in which customers move from your organization to another organization bearing

switching cost is called threat of substitutes. Threat of substitute for bank Alfalah is high and it

creates negative effect on the company because the switching cost for the customer is very low.

Because it doesn’t cost much to open an account in another bank. And now a day an individual