Managerial

Accounting

Dr. Zubair Ahmad

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Managerial accounting lectures notes

Typology: Lecture notes

1 / 24

This page cannot be seen from the preview

Don't miss anything!

2

Direct and Indirect (Overhead) costs: assigning costs to cost object Direct Material £ Steel Frame 10. Fabric 05. Foam 00. Indirect Material Screws 00. Glue 00. Direct Labour 10. Frame Cutting of fabric Assembly Manufacturing Overhead20. Supervision and management Depreciation img2.wfrcdn.com/lf/48/hash/27969/11185395/1/Chairmans-Rest-Kelsey-Tablet-Lecture-Chair.jpg accessed 2014-10-

Direct Costs: costs that can be easily and conveniently traced to the particular cost object under consideration. To be traced to a cost object, such as a product, the cost must be caused by the cost object. For example: If Reebook is assigning costs to its various regional and national sales offices, then the salary of the sales manager in its Tokyo office would be a direct cost of that office. Indirect Costs: is a cost that cannot easily and conveniently traced to the particular cost object under consideration. For example: A soup factory produce many different types of soup. The factory manger’s salary would be an indirect cost of a particular variety of soup i.e. chicken noodle soup. This salary is more a consequences of running the factory as such. So this cost is common to all products produced. Direct and Indirect (Overhead) costs: assigning (allocation) of costs to cost objects

Quiz (1) NB: Only ONE answer is correct Fixed costs are usually characterized by: a. Total costs that remain constant. b. Total costs that increase as activity decreases. c. Total costs that increase as activity increases. d. Unit costs that remain constant. 7

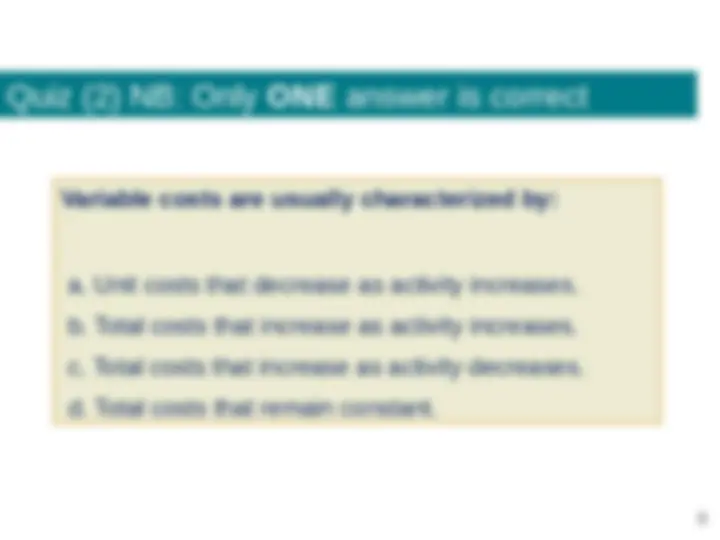

Quiz (2) NB: Only ONE answer is correct Variable costs are usually characterized by: a. Unit costs that decrease as activity increases. b. Total costs that increase as activity increases. c. Total costs that increase as activity decreases. d. Total costs that remain constant. 8

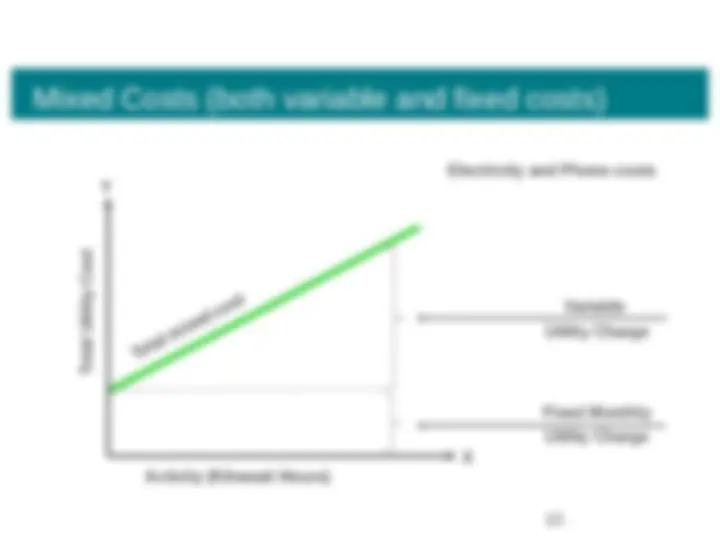

Mixed Costs (both variable and fixed costs) 10 Fixed Monthly Utility Charge Variable Utility Charge Activity (Kilowatt Hours) Total Utility Cost X Y Total mixed cost Electricity and Phone costs

Analysis of mixed costs: Some methods (1)

1. Inspection of Accounts i. Classify each ‘cost object’ as ‘variable’ or ‘fixed’ cost. ii. Aggregate the costs in each cost type. iii. Divide the sum of costs of the ‘variable cost’ type by the total activity. This gives an estimate of variable cost per unit 2. High-Low Method iv. Identify the highest and lowest levels of activity in a series of activity level measures, and the total costs associated with each. v. Divide the difference between the costs at each level by the difference between the activity levels. This gives a simple estimate of variable cost per unit of activity.

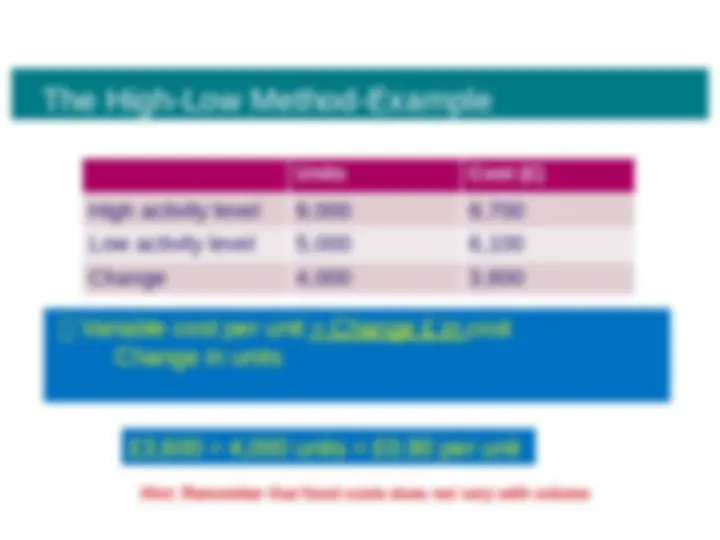

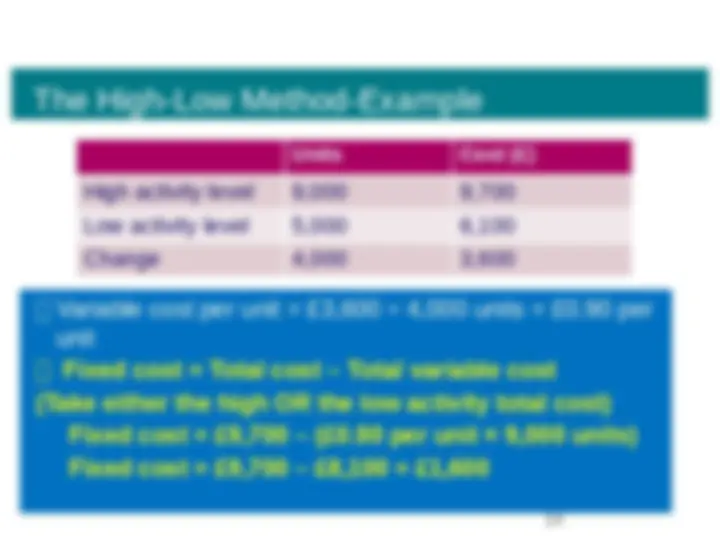

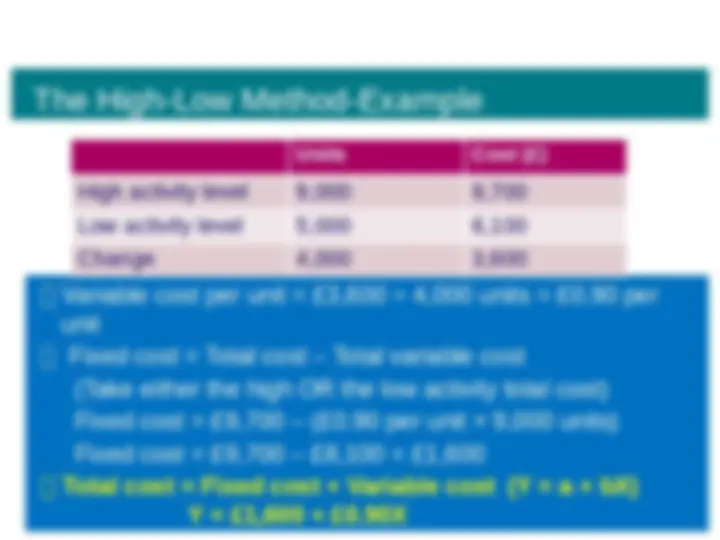

The High-Low Method-Example Variable cost per unit = Change £ in cost Change in units Units Cost (£) High activity level 9,000 9, Low activity level 5,000 6, Change 4,000 3, £3,600 ÷ 4,000 units = £0.90 per unit Hint: Remember that fixed costs does not vary with volume

The High-Low Method-Example 14 Variable cost per unit = £3,600 ÷ 4,000 units = £0.90 per unit Fixed cost = Total cost – Total variable cost (Take either the high OR the low activity total cost) Fixed cost = £9,700 – (£0.90 per unit × 9,000 units) Fixed cost = £9,700 – £8,100 = £1, Units Cost (£) High activity level 9,000 9, Low activity level 5,000 6, Change 4,000 3,

Analysis of Mixed costs: Further methods (2)

3. Scattergraph Method i. All costs at different activity levels are plotted in a graph (cost on the vertical axis and activity level on the horizontal). ii. A ‘line of best fit’ is drawn through the scatter of data points (typically with 50% of points above and 50% below the line) iii. This is a ‘visual inspection’ based ‘regression line’ indicating the average mix of fixed and variable costs across activity levels. 4. Least-Square Regression Method Uses equations to minimize the sum of ‘squared errors’ and so give a more precise regression line, potentially indicating the mix of fixed and variable costs more accurately.

The Scattergraph Method Slope = Change in cost Change in units Horizontal distance is the change in activity. 0 1 2 3 4

Total Cost in 1,000’s of pounds

Activity, 1,000’s of Units Produced

Vertical distance is the change in cost.

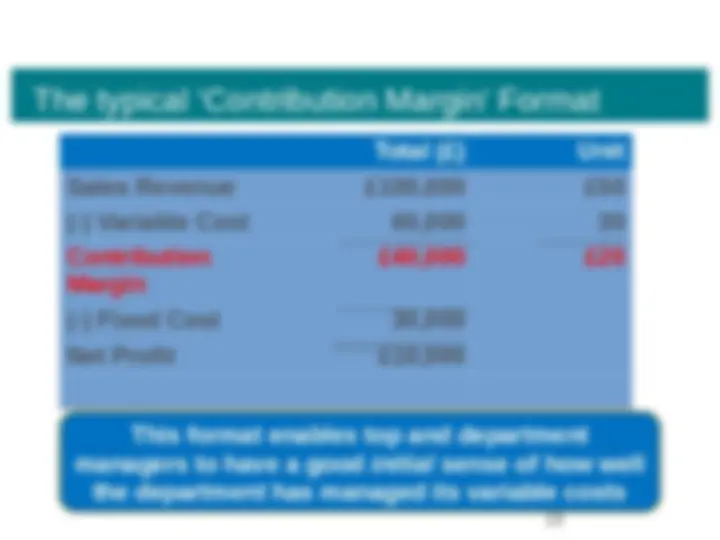

The typical ‘Contribution Margin’ Format 19 Total (£) Unit Sales Revenue £100,000 £ (-) Variable Cost 60,000 30 Contribution Margin

(-) Fixed Cost 30, Net Profit £10, This format enables top and department managers to have a good initial sense of how well the department has managed its variable costs

A comparison Needed for external reporting More useful for managing