Managing Transaction ExposureManaging Transaction Exposure

1111

ChapterChapter

111.J. Gaspar: Adapted from Jeff Madura, International Financial Management

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

When transaction exposure exists, the firm faces three major tasks: ➀ Identify its degree of transaction exposure. ➁ Decide whether to hedge this exposure ...

Typology: Lecture notes

1 / 31

This page cannot be seen from the preview

Don't miss anything!

ChapterChapter 11. J. Gaspar: Adapted from Jeff Madura, International Financial Management

Whether all transactions exposure should behedged, or

Whether transactions exposure should be hedgedselectively, or

None of the transactions exposure should behedged at all. 11.

Transaction Exposure

Transaction exposure exists when short-termfuture cash transactions of a firm are affected byexchange rate fluctuations.

When transaction exposure exists, the firm facesthree major tasks: Identify its degree of transaction exposure. Decide whether to hedge this exposure. Choose a hedging technique if it decides to hedge partor all of the exposure. 11.

Transaction Exposure

To identify net transaction exposure, a centralizedgroup consolidates all subsidiary reports tocompute the expected net positions in eachforeign currency for the entire MNC.

Note that sometimes, a firm may be able to reduceits transaction exposure by pricing its exports inthe same currency that it will use to pay for itsimports. 11.

Futures and Forward Hedges

A futures hedge uses currency futures, while aforward hedge uses forward contracts, to lock inthe future exchange rate.

Recall that forward contracts are commonlynegotiated for large transactions, while thestandardized futures contracts tend to be used forsmaller amounts. 11.

Futures and Forward Hedges

To hedge future payables (receivables), a firmmay purchase (sell) currency futures, or negotiatea forward contract to purchase (sell) the currencyforward.

The hedge-versus-no-hedge decision can bemade by comparing the known result of hedging tothe possible results of remaining unhedged, andtaking into consideration the firm’s degree of riskaversion. 11.

Futures and Forward Hedges

If the real cost of hedging is negative, thenhedging is more favorable than not hedging.

To compute the expected value of the real cost ofhedging, first develop a probability distribution forthe future spot rate. Then use it to develop aprobability distribution for the real cost of hedging. 11.

Nominal Cost Nominal Cost Real Cost Probability With Hedging Without Hedging of Hedging 5 % $1. $1. $0. 10 $1. $1. $0. 15 $1. $1. $0. 20 $1. $1. $0. 20 $1. $1. $0. 15 $1. $1. $0. 10 $1. $1.

- $0. 5 $1. $1. - $0.

For each £ in payables, expected RCH = P i RCH i^ = $0. 11.

Futures and Forward Hedges

If the forward rate is an accurate predictor of thefuture spot rate, the real cost of hedging will bezero.

If the forward rate is an unbiased predictor of thefuture spot rate, the real cost of hedging will bezero on average. 11.

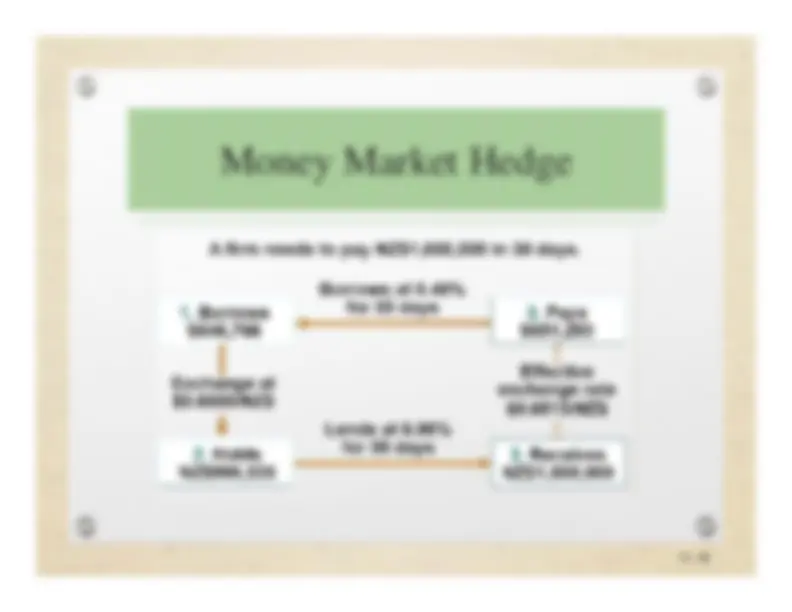

Money Market Hedge

A money market hedge involves taking a moneymarket position to cover a future payables orreceivables position.

For payables: Borrow in the home currency (optional) Convert proceeds to foreign currency at the spot rate andinvest in the foreign currency to pay off AP at maturity

For receivables: Borrow in the foreign currency Convert amount to local currency at the spot rate andinvest at home. At maturity pay off loan with foreigncurrency AR. 11.

Money Market Hedge 11.

Money Market Hedge

If interest rate parity (IRP) holds, and transactioncosts do not exist, a money market hedge willyield the same results as a forward hedge.

This is so because the forward premium/discounton a forward rate reflects the interest ratedifferential between the two currencies. 11.

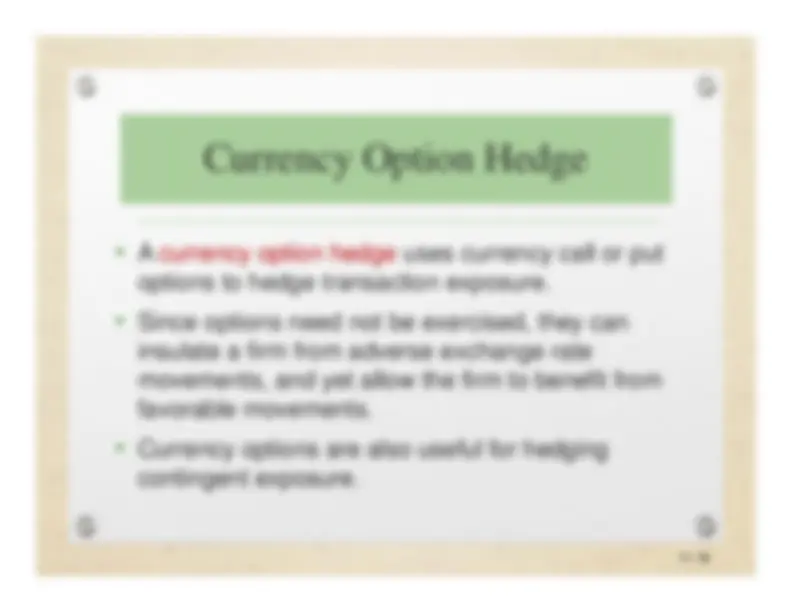

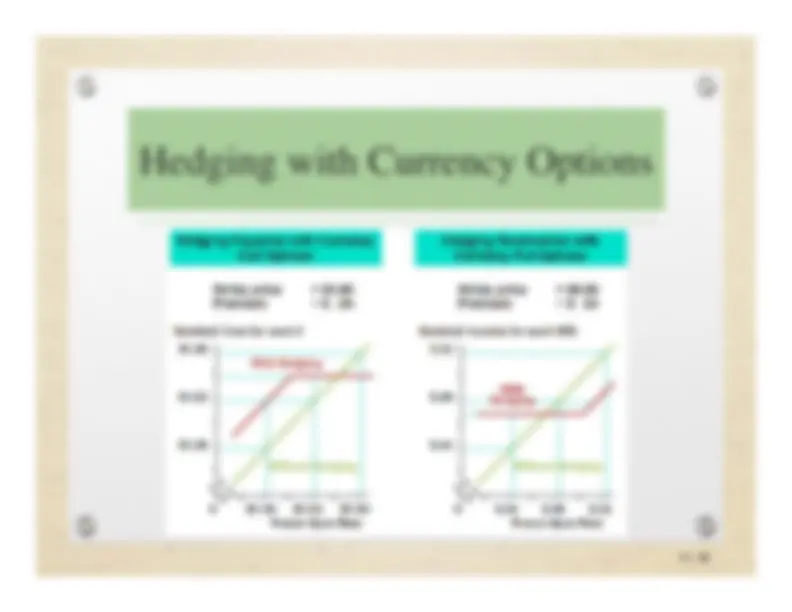

Hedging with Currency Options 11.

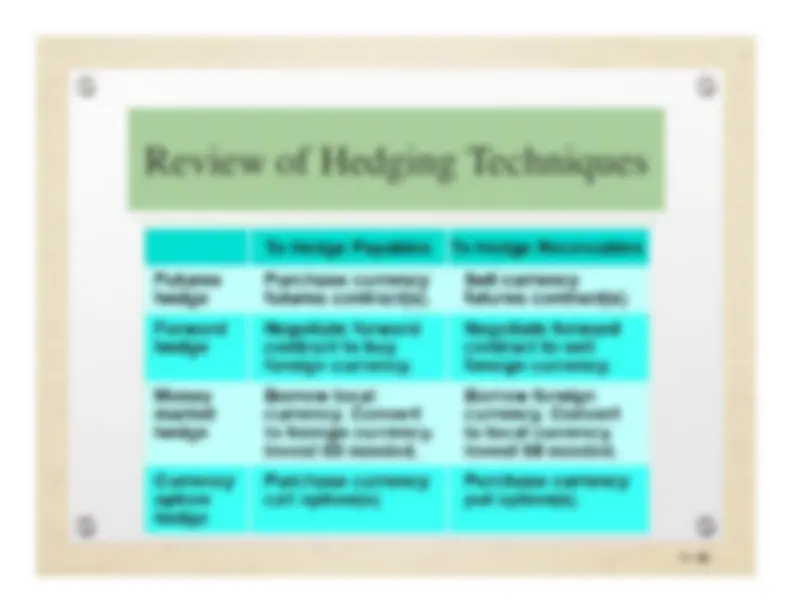

Review of Hedging Techniques 11.