Download Impact of Share Repurchase Programs on Share Price: A Study of Listed Firms in the Benelux and more Schemes and Mind Maps Financial Management in PDF only on Docsity!

Master Thesis Financial Management

Do the announcements of share repurchase programs result in positive share price development? An event study by comparing different indices in the Benelux.

Name student: L.J. Erken

Admin. Number: s

Study program: Financial Management

Faculty: Faculty of Economics and Business Administration

Name supervisor: J.C. Rodriguez

Date of submission: 26FEB

Content

- Abstract …………………………………………………………………………………………………………………………….

- Introduction ………………………………………………………………………………………………………………….

- Share repurchase and its motivations …………………………………………………………………………..

- Literature review ………………………………………………………………………………………………………….

- Data ………………………………………………………………………………………………………………………………

- Methodology ………………………………………………………………………………………………………………..

- Empirical results …………………………………………………………………………………………………………..

- Conclusion ……………………………….……………………………………………………………………………………2

- Appendix ………………………………………………………………………………………………………………………….2

- References ……………………………………………………………………………………………………………………….

1. Introduction

In this extensive research, the share price effects as a result of announcing share repurchase programs in the Benelux are being examined. This gives us an apprehensive insight into the differences per country and relating indices. Although a lot of research has been done on share repurchase programs, there still is a lot uncovered for the Benelux. With this research, I hope to fill some blanks in the field of share repurchase in the Benelux.

1.1 The context of the paper Share repurchase is a popular tool for a company’s decision makers to led excessive cash flow back to its shareholders. This has been so in the U.S. for over 25 years, but also in the different countries in the Benelux this payout method is gaining popularity. The reasons why companies do so can be various. As discussed by Lee et al. (2010), two main issues rule the game. First of all, why do companies repurchase? In the extant literature on share repurchases, the most mentioned ones include; managerial intentions to signal to the market that the company’s shares are undervalued; warding off potential take-over attempts; avoiding dilution by using the repurchased shares to settle outstanding options and convertible securities; distribute excess cash when there is no investment opportunity and, within that line of thought; distribute cash by means of repurchase instead of dividends. Dittmar (2000) found that, while testing for all of these variables, most of them turned out to be valid reasons for share repurchase programs initiated by the specific companies (most of the reasons mentioned were also tested separately, for more details take a look at: Tarhan (1998) and Vermaelen (1984)).

The second issue addressed in the main repurchase studies is the reaction on the stock market to the announcement date of repurchase programs. “One common theme in these studies on repurchase is that the manager signals private information through the repurchase and the market positively values this private information”, Lee et al. (2010) says. The theory suggests that, when the stock is undervalued, a repurchase signals this information to the market. As a consequence, the market absorbs this information by an upward adjustment in the share price. At the same time, and within more negative boundaries to the companies’ perspective, an undervalued share price may lead to potential take-over initiatives. In an attempt to ward of these raiders, management may decide to repurchase shares (thereby, adjusting the share price to its correct level). The effect of signaling to the market however, only exists under the conditions of strong market monitoring circumstances. Without this present, managers are not under pressure of revealing any information and share prices may not respond to any management intentions of signaling.

This paper proceeds from this general conjecture and will focus on the Benelux indices by means of two objectives. Firstly, in order to see whether repurchase announcements in the Benelux lead to different results than in other countries, I measure the abnormal result around announcement date. This will be done by means of event study methodology. Secondly, I will test two hypotheses – the undervaluation hypothesis and the free cash flow hypothesis - on why managers actually decide to repurchase its own shares.

My main empirical finding is that, although my results are not statistically significant, the undervaluation hypothesis is pleaded for by my empirical evidence.

This research is already interesting because of its focus on the Benelux regarding a yet unidentified topic for this region. The sample used to get there however is even unique as the combination of the different indices leads to new insights with data that is hand-collected.

1.2 The structure of the paper The rest of this paper is structured as follows: Section 2 discusses to a deeper extent the different motivations for share repurchase programs; Section 3 presents a literature review; Section 4 describes how the data is collected and structured; Section 5 explains the methodology used for this research; Section 6 presents the results of our analyses; and in Section 7 this paper concludes and also recommends on potential future research.

2. Share repurchase and its motivations

Companies that make a profit, in general, use this excess cash for two purposes: 1) paying dividends to its shareholders, and; 2) keep the remainder, stockholder’s equity, in the company. The latter one can be used for future investments; e.g. depending on an (minimum) expected net-present-value (NPV), the company will decide whether or not to invest in certain investment opportunities. However, when there are not enough investment opportunities available, some of the retained earnings remain. If that is the case, the leftover retained profits can also be used for share repurchases. When a company decides to repurchase its own shares, it reduces the number of shares held by the (public) shareholders.

According to Stephens and Weisbach (1998), there are three ways in which a company can repurchase its own equity, i.e.: 1) tender-offer repurchases, 2) Dutch auction repurchases, and 3) open-market repurchases, where the first two options are non-open-market share repurchases. In the case of a fixed-price tender offer, the company offer specifies in advance how many shares they are willing to repurchase, for what fixed price (which typically exceeds the market price) and what the duration of the repurchase period is. The alternative in a non-open-market repurchase, the Dutch auction, is similar to a fixed-price tender offer except that the offer specifies a price range for the to be repurchased shares. The shareholders themselves declare against what price they are willing to sell their shares. At the end, the repurchase price is the price that allows the firm to repurchase the amount of shares as announced in advance. This goes for all shareholders who tendered at, or below that price. The open-market repurchase is the most common method known. In this case, the firm will announce that it may or may not decide to repurchase its own shares against market prices for an upcoming given period of time. Whether the firm will actually decide to repurchase depends (mainly) on market conditions. In a comparison by Comment and Jarrell (1991), they find that a tender offer is used when a company has the intention to repurchase the largest number of shares.

So, either a company sticks to its words (which make the company ‘credible’) or it will incur costs in the form of reputational damage. In the latter case, the company might even be linked to overvaluation which comes with an even greater cost; an even more negative reaction on its share price.

2.1.2 Avoiding dilution Several companies use stock options incentive plans as part of the remuneration package offered to the (higher) executives. Once these options are exercised, stock dilution is created, i.e.: an increase in common shares can shift positions in ownership percentage, voting control, earnings per share, and, hence, the value of a share (or in other words: any event that reduces the investor’s share price below the initial purchase price). As Grullon et al. (2000) pointed out, several firms use share repurchase programs as a way to fine-tune their capital structure and, hence, prevent this kind of shareholder wealth diminishment.

2.1.3 Distributing excess cash Another argument in line with shareholders interest is when a firm aims to distribute excess cash to its shareholders by means of share repurchase programs. Intentionally, the presence of excess cash might lead to huge conflicts of interest between the shareholders and its company’s management. Self-interested managers could use the excess cash to fund negative net present value projects such as fringe benefit consumption or so-called ‘empire- building’ which would harm the company’s shareholders (Jensen ,1986). Another way in which agency difficulties could arise, is when the company’s management are not actually destroying value but simply run out of value-adding investment opportunities and retain the excess cash on the balance sheet (Hackethal et al., 2006).

Both types of agency conflicts are ameliorated when a firm’s management chooses to distribute the excess cash. This in preference to paying out dividends because, in case of excess cash, share repurchases are the safest way for a company to distribute it; there is no sign to the market of reoccurrence and the size can be adjusted any time. Paying out dividends will result in expectations for the next year and will have a negative impact on the share price in case the company cannot meet these expectations in the following years (Correia da Silva et. al, 2004)..

2.1.4 Tax burden Firms that actually act in the best interest of the shareholders, as every company is supposed to, have another motivation in case of a tax burden. In some countries, the tax burden on an investor’s income is on average higher for dividend income than for capital gains. In order to maximize after-tax gains for the company’s shareholders, share repurchase programs are the way to go. Share price effects can be neglected however; companies already known for acting in the best interest of the shareholder are expected to distribute excess cash by means of share repurchase programs. The market will anticipate on these expectations so these developments are already absorbed in the market value of the firm.

2.1.5 Merger and acquisition The last motivation within the first category is also a tax-related one, this time in reference to merger and acquisition (M&A) activity. In many legal systems, an exchange of shares is more tax-efficient than receiving money from the perspective of the target firm’s shareholders. Therefore, it might be a smart tactic for an acquiring company to repurchase its own shares before it will start bidding on a target firm. Tax advantages for the target firm may then result in a lower acquisition price and, hence, this will benefit the shareholders of the bidding firm. Hackethal et al (2006) concludes: “If the characteristics of the acquisition deal are known ex ante, the repurchase announcement will, however, not create new market information and should therefore leave the acquirer’s market value unchanged”.

2.2 Shareholders harm Arguments belonging to the second category are supposed to contravene with the shareholders interest. These merely include; 1) warding off a potential take-over; 2) only inside shareholders are informed; 3) dilution.

2.2.1 Warding off a potential take-over Another reason why companies might decide upon a share repurchase program in preference to paying dividends is to ward off the threat of a potential take-over (Simon, 1986). Bidder companies (or ‘raiders’) are looking for undervalued companies so that once they control the firm, they can profit from the expected synergies (by releasing private information or improving efficiency). As discussed by Dittmar (2000): “Brown and Ryngaert (1991), Bagwell (1992), and Hodrick (1996) document the existence of shareholder heterogeneity and the upward slope of the supply curve”. Within that presence of an increasing demand for the shares of the target company, a potential target can increase its selling price by repurchasing its own stock, i.e.; by means of share repurchases, the acquisition price of the target company rises as the shareholders who sold their interest in the company during the share repurchase are the ones with the lowest reservation value. On the contrary, working with a cash dividend does not change the distribution of the reservation values. The share repurchase will lead to a selling of the shares by the shareholders with the lowest reservation prices, leaving those behind who are only willing to sell their shares at a premium above the tendered price. This premium makes the target company more expensive and might even entirely filter out the synergies that would apply to the bidder company. Hackethal et al. (2006) contributes to this discussion by saying that the amount of outstanding shares available to the bidding firm has declined and cash reserves are used up. As a result of the above mentioned arguments; a potential take-over is warded off. As concluded by Shoven and Simon (1987): “We therefore would predict an increase in restructurings, especially repurchase, in response to the threat of takeover”.

2.2.2 Only inside shareholders are informed Sometimes, only inside shareholders are informed about an upcoming share repurchase program by the company.

Table 1: Related research on open market share repurchases in several countries world-wide. All show positive CAR

3.1 Empirical work done on the US Undervaluation hypothesis Signaling effects are expected to be stronger when the potential for actual undervaluation increases. This is confirmed by the research done by Stephens and Weisbach (1998), Comment and Jarrel (1991) and Ikenberry et al. (1995). They found that abnormal returns are larger for firms whose share prices underperformed in the market during the days prior to the date of announcement. Ikenberry et al. (1995) also observed “a strong negative relationship between the market-to-book ratio prior to the buy-back announcement and the magnitude of positive abnormal returns thereafter” (Hackethal and Zdantchouk, 2006). With his research, Vermaelen (1981) shows that the signal’s strength is at the same time the function of its credibility; abnormal returns increases at the day of announcement based on the amount of shares repurchased as well as in the amount of shares held by the firm’s management. It is assumed that the credibility of the signal increases when wealth of the management (manager) is at risk.

Long-term Country of research Authors CAR Dataset U.S. Ikenberry et al. (1995) [3 years ]: 8.7% 1,239 OMR (1980-1990) Cha n et a l. (2004) [2 years ]: 11.0% 5,382 OMR (1980-1996) Canada Ikenberry et al. (2000) [2 years ]: 14.9% 1,060 OMR (1989-1997) Short-term Country of research Authors CAR Dataset U.S. McNa lly (1999) [-1; +1]: 2.5% 702 OMR (1984-1988) Stephens a nd Weis bach (1998) [-1; +1]: 2.7% 591 OMR (1981-1990) Verma elen (1981) [-1; +1]: 3.7% 243 OMR (1970-1978) Mitchell a nd Netter (1989) [-1; +1]: 3.5% 337 OMR (Oktober 1987) Comment a nd Ja rrell (1991) [-1; +1]: 2.3% 1,197 OMR (1985-1988) Va fea s a nd Joy (1995) [-1; +1]: 3.2% 162 OMR (1985-1991) Ikenberry et al. (1995) [-1; +1]: 3.5% 1,239 OMR (1980-1990) Ka hle (2002) [-1; +1]: 1.5% 712 OMR (1993-1996) Ga s pa r et a l. (2005) [-1; +1]: 2.9% 3,989 OMR (1984-2000) Grullon a nd Micha ely (2002) [-1; +1]: 2.7% 4,443 OMR (1980-1997) Peyer a nd Verma elen (2005) [-1; +1]: 2.4% 6,470 OMR (1984-2001) Lie (2005) [-1; +1]: 3.0% 4,729 OMR (1981-2000) Aus tra lia La mba a nd Rams a y (2000) [-1; +1]: 3.3% 103 OMR (1989-1998) Canada Li a nd McNa lly (1999) [-2; +2]: 3.6% 183 OMR (1989-1992) Ikenberry et al. (2000) [-15; +15]: 0.9 % 1,060 OMR (1989-1997) France Ginglinger and L'Her (2006) [0; +1]: 0.6% 363 OMR (1998-1999) Germa ny Seifert a nd Stehle (2003) [-1; +1]: 5.9% 192 OMR (1998-2003) Ha cketha l and Zda ntchouk (2006) [-1; +1]: 6.0% 224 OMR (1998-2003) Ja pa n Zha ng (2002) [-1; +2]: 6.0% 39 OMR (1995-1999) UK Ra u a nd Verma elen (2002) [-2; +2]: 1.1% 126 OMR (1985-1998) Os wa ld a nd Young (2002) [-1; +1]: 1.4% 266 OMR (1995-2000) Rees (1996) [-2; +2]: 0.3% 882 OMR (1981-1990)

Also, it seems that the magnitude of the information asymmetry between a firm’s management and its shareholders has its bearing on announcement effects, as found by Ikenberry et al. (1995): stock- price effects on date of announcement are inversely related to firm size. The logic behind this reasoning is that smaller firms disclose less information to the capital markets and are less researched by business analysts. Next to that, as added by Vermaelen (1981), there is lower institutional ownership at smaller firms and are (therefore) more likely to be undervalued. As a result, the extent of information asymmetry should, more or less, decrease with firm size. This is confirmed by Stephens and Weisbach (1998) who find a negative correlation between the size of the firm and its CAR around announcement day as well as a by research done by Chan et al. (2004). Overall, share repurchase programs seem to serve as a credible way of signalling to the market that a firm is undervalued which is also confirmed by qualitative research; Brav et al. (2005) questioned 384 CFO’s and Lane et al. (1989) also talked with several managers of listed firms. Both found that perceived undervaluation is indeed one of the most mentioned motivations by managers to repurchase its own shares (for more information see also Baker et al. (1981)).

Free cash flow hypothesis The validity of the free cash flow hypothesis is, amongst others, tested for by Bagwell and Shoven (1988), Evans et al. (2000), and Li and McNally (1999). They found a positive relation between abnormal returns and the available excess cash at a company. It is suggested that share repurchase programs are an excellent way to signal to the market that a firm’s management does not use excess funds for private-benefits or low NPV projects. Moreover, as observed by Stephens and Weisbach (1998), firms with on average more excess cash tend to repurchase greater amount of shares, which indicates that it is indeed a method used by management to reduce a firm’s excess cash.

Concluding: for the research on share repurchase programs done for the US, there are several motivations that contribute to management acting. However, the most prominent one is the ‘signalling undervaluation’ one. Research done on other countries that the US, give us the same idea.

3.2 Empirical work on countries outside the US Cumulative abnormal returns at, or around, the day of announcement are (for both US and non-US companies) are strictly positive (table 1). The most mentioned motivation in these empirical papers is also the ‘undervaluation signalling hypothesis’ as a motivation for repurchasing a firm’s own shares. This goes for all but one: the UK. Rau and Vermaelen (2002) suggest that, as a consequence of legal restrictions imposed by the UK government, repurchase announcements are moderately used as a way to signal perceived undervaluation. This is so because of, amongst other, the rule that UK firms are not allowed to repurchase shares when directors possess price-sensitive information about the firm that is not disclosed. The empirical work done by Rau and Vermaelen (2002) also indicates that share repurchases in the UK are mainly motivated by tax consequences for institutional shareholders (e.g. investment banks and pension funds).

The number of repurchase announcements for the 4 stock indices in the Benelux – AEX, AMX, BEL20 and LuxX) can be seen in figure 1 below (for a comparable image per index of this research, please go to Appendix 2). For the 43 companies in this research that actually announced a share repurchase during the last 6 years, a total of 121 share repurchase announcements have been identified.

Figure 1. This graph shows the quarterly distribution of share repurchase announcements over the last 6 years for the Benelux.

If we would look at these figures, we notice an interesting development; after the default of Lehman Brothers in autumn 2008, a major decrease in share repurchase activity can be observed. In the quarters after that default, a small but inarticulate rise in repurchase announcement seems to pop up again. The activity as before the financial crisis of 2008 was not reached again however.

In total 4 indices are incorporated in this research. See table 2 below for the number of repurchase announcements per index as identified in the sample.

Table 2. This table shows the repurchase announcements per index as included in this research.

5 3

5 4

9

6

13

10

11

4

5

1

2

4

5

2

5 5

1

4

8

3

5

1 0

2

4

6

8

10

12

14

Index Country # of repurchase announcements AEX Netherlands 58 AMX Netherlands 19 BEL20 Belgium 27 LuxX Luxembourg 17

5. Methodology

In this paper, the stock-price effect of open-market share repurchase announcements in the Benelux are considered. Although there are numerous other interesting aspects to examine, the focus in here is only on the share price.

5.1 Methodology In this research, the effects of an ‘economic event’ on the value of different firms are examined. When this is the case, event study methodology is the right approach to solve the trick. “Event studies focus on the impact of particular types of firm-specific events on the prices of the affected firms’ securities” as stated by Brown and Warner (1980).The logic behind this technique is that, in general, the effects of an event are directly reflected in a firms’ market value (i.e. share price) and it is a legitimate way of measuring success as acting in the interest of the shareholders is the most common goal for all companies. As suggested by the pioneers of event study methodology (Fama, Fisher, Jensen and Roll (1969)), this method shows if share prices generate a different result surrounding an event as opposed to the absence of an event. The share price returns in the event window (period of research conducted) are compared with the normal expected returns (to be defined by a model based on an estimation window prior to the event) if there had been no economic or firm-related event taken place. The residual between the two is called ‘abnormal return’. In order to perform a successful event study, I will perform three steps, namely; 1) defining the event of interest and the period of the event in which the share prices are examined; 2) describe the selection criteria for including a certain firm in the study (MacKinlay, 1997), and; 3) determining a benchmark-model as a basis on which the comparison between the share price return and the normal expected return can be made as well as calculate and analyze the abnormal returns around the event date. In this section, the setup for the regression analyses will also described. In the next section, the results of both ways of empirical testing will be described.

5.1.1 Defining event of interest The event is share repurchase announcements by listed firms in the Benelux in the period 1-1- till 31-12-2011, i.e.; 6 years. The event window for each announcement consists of 61 days. That is, 30 days prior to the announcement, the day of announcement itself, and 30 days after the announcement date. Realistically speaking; the most interesting days to the research is the day of announcement itself and the 2 days straight after. However, we should take into account that the market may already adopt some information about the upcoming event and we will capture these potential effects of rumors and/or insider trading by increasing our event window, both prior and after the day of announcement.

5.1.2 Selection criteria The conducted research considers listed firms in the Benelux. To be more specific; Dutch firms listed on the AEX and AMX; Belgian firms listed on the BEL20; Luxembourg firms listed on the LuxX. For all these indices, it concerns the time period January 2006 – December 2011.

To calculate the impact of the event, abnormal returns are required. Abnormal returns are defined as the difference between the ex-post return of the share price over the event window and the normal return over the event window.

AR it = Rit – Rit* for t = -30,-29,…,+29,+3 0 (3)

As discussed by MacKinlay (1997), it is necessary to use the concept of Cumulative Abnormal Return (CAR) in order to accommodate a multiple period event window. As a result, we can examine our results from the event study on basis of different time series (to be discussed in section six).

The CAR for a selected time window is calculated as follows:

CARi (t1, t2)= ∑(t2, t=1) ARit (4)

Once the returns (CAR) are known, the cross-sectional average can be calculated by means of the Cumulative Average Abnormal Return (CAAR):

CAAR = (1/N)N ∑i=1 CARi (5)

It is useful to know whether the results are significantly different from zero. This will be done according to the null hypothesis:

H0 : E ( CARit ) = 0 (6)

The t statistics in equations (5) and (6) are used to test the null hypothesis - as presented in equation (6) - that abnormal returns on a particular day and CAR for a given period [ t; t+n ] are not different from zero.

T = ARit / σ ( ARi ) (7) with σ ( ARi ) equal to the standard error of the estimate from (1)

T = CAR(t+n, i) /((√n) σ(ARi) (8) with CAR(t+n,i) = ∑(t+n, j=t)ARi,j

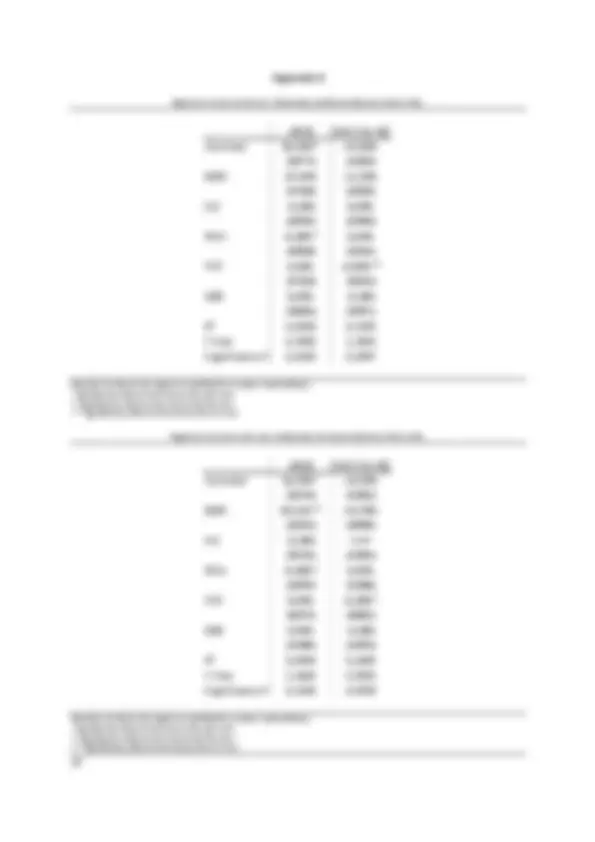

5.2 Regression In order to compare this study with previous studies, I conduct a regression analysis for the abnormal returns from repurchase announcements. In the following, the variables are defined which are then used as covariates. In table 3 below, the corresponding descriptive statistics can be found.

Table 3. Descriptive statistics for the entire sample in the Benelux (N=121).

Note: BMR is the firms’ book-to-market ratio and defined as net asset value per share divided by the share price. SIZ is the natural logarithm of total assets. ROA is return-on-assets and computed as net income over total assets. FCF is free cash-flow and defined as all liquid assets divided by book value of equity. DEB is long term debt divided by total assets.

Book-to-Market (BMR) : One of the most mentioned arguments in favor of share repurchases is the presumed undervaluation of the outstanding shares (Ikenberry et al., 2000; Kahle, 2002). Investors’ expectations with respect to a firm creating economic value will increase as the BMR ratio decreases. As a result, firms with high BMR values are also called ‘value firms’. On the contrary, firms with low BMR values are referred to as ‘growth firms’ (Hackethal et al., 2006). Value firms are therefore more likely to signal undervaluation by means of a share repurchase announcement. Hence, I expect a positive correlation between the AR’s and BMR-ratio. The BMR ratio is defined as a firm’s net asset value per share divided by its share price. Net assets per share is defined as net tangible assets (i.e. shareholders equity minus intangibles) divided by year-end number of shares.

Size (SIZ): Information asymmetry may be another important driver to a firm’s undervaluation. By this I mean the discrepancy between the information available to the managers and the information available to the public. Larger companies have more coverage by investors and analysts than small ones. Therefore, I expect that managers of smaller companies are more likely to send stronger signals to the market than managers of larger companies. Firm size is defined as the natural logarithm of the firm’s total assets.

Return-on-Assets (ROA): Obtained from specific market characteristics, the stock-price effect will only show positive signs in the case the firm has a strong balance sheet and track record (as determinants of profitability). Managers have the intention to show the world their company is doing just fine, because if a firm can use excess cash to repurchase shares it is considered as a healthy and strong signal. Apparently, in this case, the company has the freedom to choose to use its cash to repurchase shares (and by that disturb the financial flexibility of the company) without negative consequences. This is partly, because it shows the public that the company is not overinvesting and its managers are not too devoted to empire-building and such. If, however, the firm has not showed participation in profitable investment opportunities in the period prior to the announcement, a negative stock-price effect is expected. On the other hand, it is expected that a positive stock-price effect will materialize if the announcement follows a flourish and profitable period. Hence, the ROA-ratio is used.

AR CAR BMR SIZ ROA FCF DEB [0] [+2;+30] % % Min. -5,34 -6,50 0,02 3,42 -0,05 0,02 -0, Max. 7,62 17,66 0,89 14,13 0,61 0,31 0, Average 0,85 2,00 0,47 8,27 0,15 0,13 0, Median 0,77 2,34 0,51 7,93 0,09 0,11 0, Stdev. 2,60 5,01 0,17 2,10 0,11 0,05 0,

Dependent variables Independent variables

6. Empirical results

In this section, the main results will be presented. In the first part we will review the abnormal returns for the investigated fields. In the second part, we will evaluate the regression analysis.

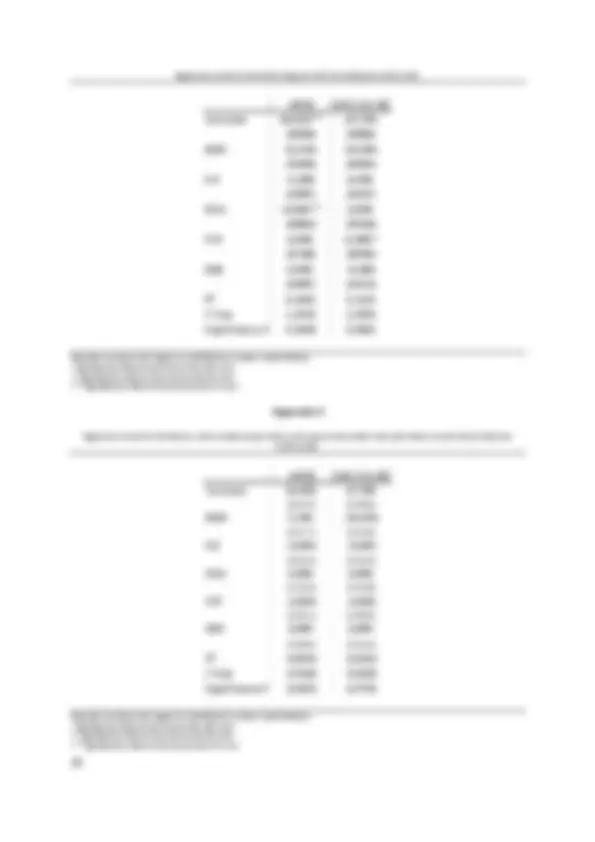

6.1 Abnormal returns In table 4 below, the cumulative average abnormal returns are presented for the Benelux entirely. This includes the 121 repurchase announcements from companies listed on the AEX, AMX (Netherlands), BEL20 (Belgium) and the Luxx (Luxemburg) as defined in our sample. See appendix 3 for the CAAR per index.

While the average price effect on the announcement date itself is only a modest 0.9%, the cumulative return reaches 4.7% over the entire event window [-30; +30]. In the days surrounding the event date – time frame [-1; +1] – the CAR is 1.0% which is considerably lower compared to other research (see section 3 of this paper). In the period following the event date CAR[+2;+30], a price return of 2% can be noticed suggesting to support the signaling hypothesis. All returns are significantly different from the 1% level.

Table 4. Cumulative Average Abnormal Returns of the open-market share repurchase announcements in the Benelux (N=121).

Interesting to notify is the positive CAAR of 1.7% prior to the day of announcement, i.e. [-30;-2]. This result is incongruent with the theory that corporate managers are able to time their repurchase announcement as suggested by Ikenberry et al. (1995) and Comment and Jarrell (1992). However, as suggested by Hackethal and Zdantchouk (2006), there are two mutually non-exclusive reasons for positive abnormal returns prior to the event date. Although I have performed an extensive research (as explained in section 4), it is possible that I have missed some items of public information that has been disclosed to the markets in advance of the

BENELUX

(N=121) t-statistic [0] 0,9% 3, [-1;+1] 1,0% 3, [-2;+2] 1,0% 4, [-5;+5] 1,7% 4, [-10;+10] 2,3% 4, [-30;+30] 4,7% 3, CAAR [-30;-2] 1,7% 3, [-10;-2] 0,2% 4, [-5;-2] 0,2% 3, [+2;+5] 0,5% 3, [+2;+10] 1,1% 4, [+2;+30] 2,0% 4,

event date as taken in this research. Moreover, positive returns prior to the event date does not necessary have to be a result of firm specific information being available prior to the firm’s statement; it might also be a result of insider trading where people closely related to/involved with the firm act upon their privately required information. In figure 3 below, the effect to the share price on the announcement date is clearly visible in an upward reaction as described above. This is, at the same time, the only abnormal return that is significantly different from 0 (at a 1% level) for our entire sample when looking at abnormal returns only.

Figure 3. Average abnormal return of open-market share repurchase announcements in the Benelux (N=121).

This is different however when we have a look at the CAAR. In figure 4, the upward trend is clearly showed, reflecting our entire event window. The price effect on announcement date is in here clearly visible as well.

Figure 4. Cumulative average abnormal return of open-market share repurchase announcements in the Benelux (N=121).

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%