Input - Output Models

Lê Xuân Trường

Lê Xuân Trường Input - Output Models 1/9

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An introduction to input-output models, a quantitative economic analysis tool used to represent interdependencies between different sectors of an economy. It covers topics such as input-output tables, leontief matrices, and the basic equation used to determine production levels to satisfy external demand.

Typology: Slides

1 / 9

This page cannot be seen from the preview

Don't miss anything!

Lê Xuân Trường

In economics, an input–output model is a quantitative economic model that represents the interdependencies between different sectors of a national economy or different regional economies. Wassily Leontief (1906–1999) is credited with developing this type of analysis and earned the Nobel Prize in Economics for his development of this model.

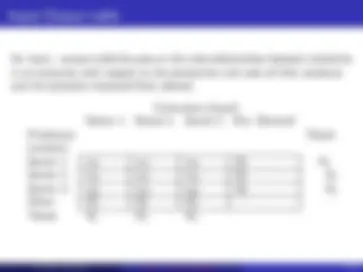

The other production factors row consists of costs to the respective sectors such as labor, profits, and so on

The external demand entry here could be consumption by exports and consumers

Each sector appears in a row and in a column The row of a sector shows the purchases of sector’s output by all sectors and by external demand. The entries represent the value of the products and might be in units of millions of dollars of product. The column of a sector gives the value of the sector’s purchaches for input from each sector (including itself) as well as what is spent for other cost.

An important assumption of input-output analysis is that the basic structure of the economy remains the same over reasonable intervals of time ⇓ We focus on the relative amounts of inputs that are used to produce a unit of output.

Let Aij be the number of units of sector i’s product needed to produce one unit of sector j’s product. It is said to be the unit input coefficient

Aij =

xij Xj

The matrix A = [Aij ] is called the Leontief matrix of the economy

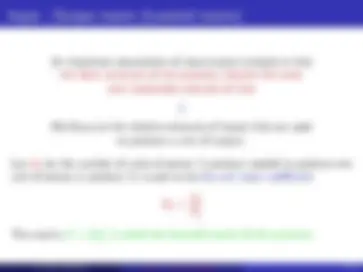

Assume that an economy has three interrelated sectors

Sector 1, Sector 2, Sector 3.

Let A be the Leontief matrix of the economy

We also assume that Di is the external demand from Sector i and put

Goal: Determine the levels of production for each Sector 1, 2, and 3 so that the external demand D can be satisfied.

Production = internal demand + external demand

Let Xi be the production required of Sector i to satisfy above equation. The production vector is

X =

From the definition of Leontief matrix A we have can obtain

X = AX + D or (I − A)X = D.

Since the matrix I − A is invertible it follows that

X = (I − A)−^1 D