Download Medicaid slide study guide and more Slides Health sciences in PDF only on Docsity!

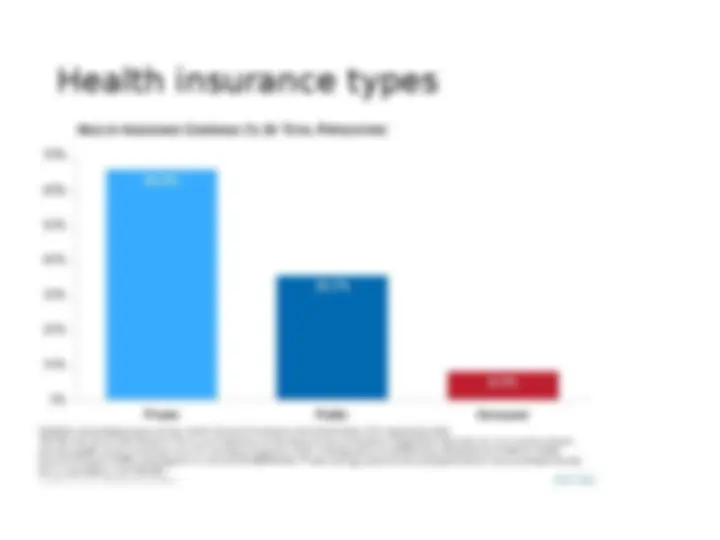

Private Health

Insurance

THE UNINSURED

- (^) In 2022, 8.4% or 27.6 million Americans of all ages did not have health insurance

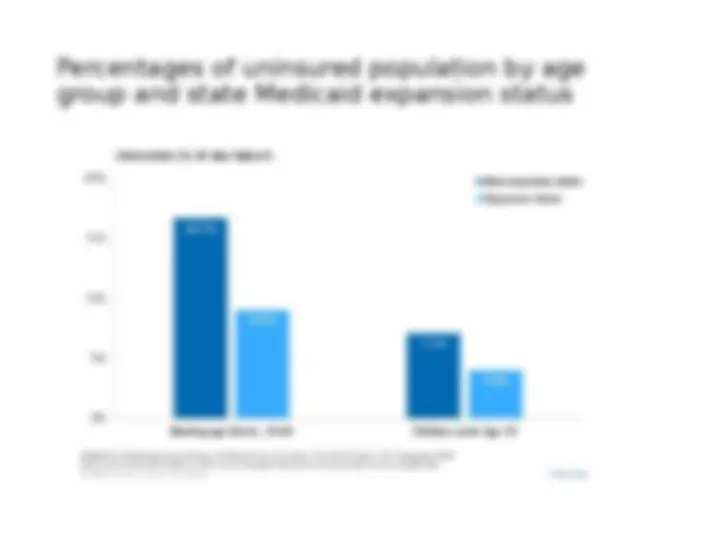

Percentages of uninsured population by age group and state Medicaid expansion status

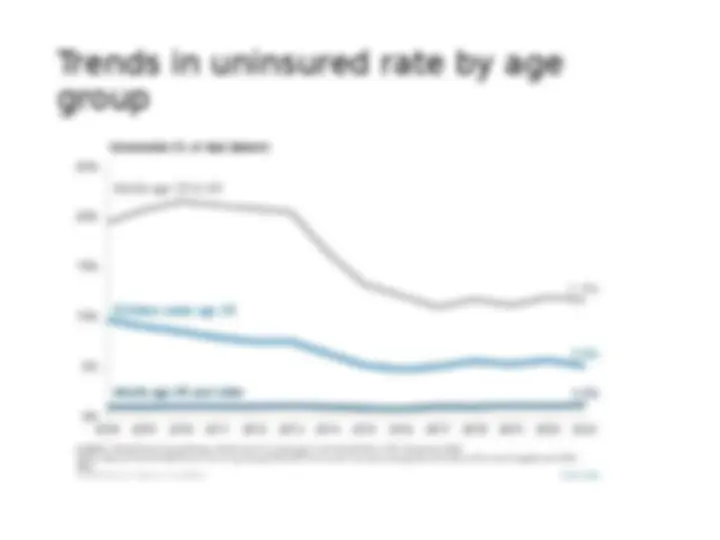

Trends in uninsured rate by age

group

Early health insurance

programs

- (^) Marine Hospital Service authorized in 1798.

- (^) Massachusetts Health Insurance Company of Boston incorporated in 1847.

- (^) Plans offered for “Gold Rush” workers in

- (^) Early plans were more disability insurance covering specific diseases.

- (^) Later, they were expanded to cover other diseases, but only reimbursed patients for out-of-pocket costs (income protection).

Hospital insurance

- (^) In 1929, Baylor University Hospital (Dallas, TX) offered hospital care (“Blue Cross”) to a group of teachers on a prepaid basis ($6/year/person). http://www.bls.gov/data/inflation_calculator.htm

- (^) As insurance decreased financial barriers to hospital care, demand for care (and hospital beds) increased.

- (^) During “The Great Depression,” hospitals with empty beds and declining revenues were financially stabilized by such insurance plans.

THE HEALTH INSURANCE INDUSTRY

Structure

- (^) The term “third-party payer” may suggest that there are only 3 parties (patients; provider; insurance) involved, but the structure of the insurance industry is far more complicated.

Principles of risk

management

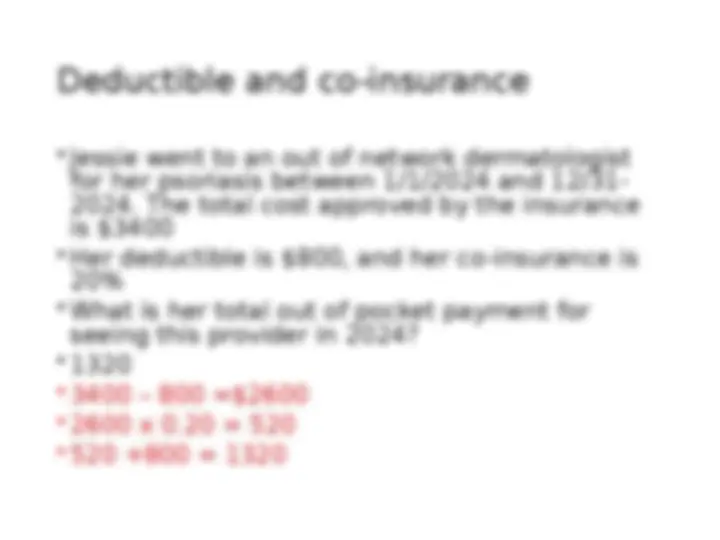

- (^) Purchasing insurance requires a known small loss - a premium - for protection against a large unknown loss (i.e. trading certainty for uncertainty).

- (^) Insurance does not remove the risk of loss, but transfers part of the risk to the insurer.

- (^) 1) your risk of getting a stroke in 2023 is 1/100, but if you get it and do not have insurance, you will have to pay out of pocket 2 millions

- (^) 2) you enrolled in an insurance and pay $ as an annual premium. In case if you got stroke your cost will be totally covered

Pure vs. Speculative risks

- (^) Kidney transplant (covered)

- (^) Breast enhancement surgery

- (^) After Mastectomy (usually covered)

- (^) Healthy individuals (not covered)

BASIC PRINCIPLES AND

STRATEGIES OF HEALTH

INSURANCE

BASIC PRINCIPLES AND

STRATEGIES OF HEALTH

Prescription coverage:^ INSURANCE

- (^) If prescription coverage provides relatively small benefit at a high administrative cost and is inconsistent with some of the basic principles of insurance (substantial loss, accidental), why are they covered by health plans?

- (^) Because they are critically important in preventing unpredictable, severe complications of the underlying disease - (^) Myocardial infarction because of uncontrolled BP - (^) Stroke because of uncontrolled LDL

- (^) Drug therapy is can be preventive, and mitigate and/or delay the expense of other more costly therapies.

- (^) However, the potential benefits are not always realized.

Why antihypertensive drugs/chronic

disease medications are largely

insurable?

- (^) Taking antihypertensives is a regular event

- (^) It is predicable, not accidental

- (^) These seem to be inconsistent with insurance theories.

- (^) Why they are insurable?

BASIC PRINCIPLES AND

STRATEGIES OF HEALTH

INSURANCE

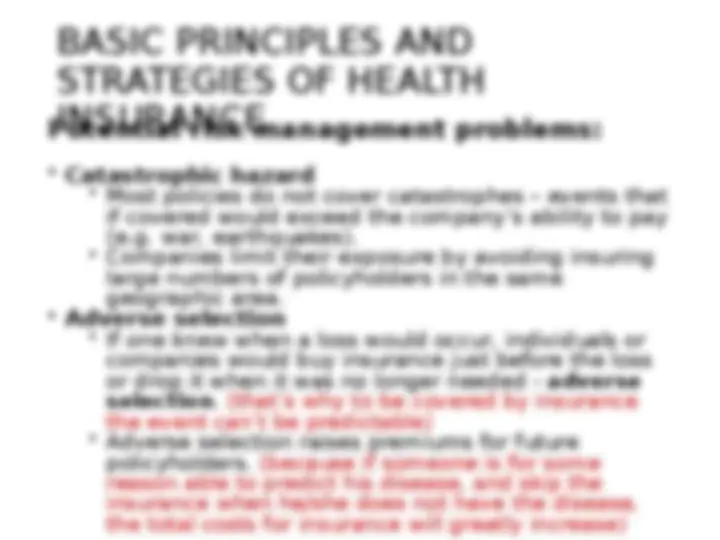

Potential risk management problems:

- (^) Incentives to create losses - a policyholder actually gains from a loss (e.g. insuring a car for more than it is worth), which incentivizes the loss.

- (^) Supplier-induced demand - a person paid for a service determines how often the service is provided - conflict of interest (e.g. physicians).

- (^) Moral hazard

- (^) Decreasing the out-of-pocket loss increases the likelihood that the peril will occur.

- (^) Having health insurance encourages patients to consume health care services of low value that they would not otherwise use.

- (^) Overconsumption increases premiums for all.

BASIC PRINCIPLES AND

STRATEGIES OF HEALTH

INSURANCE

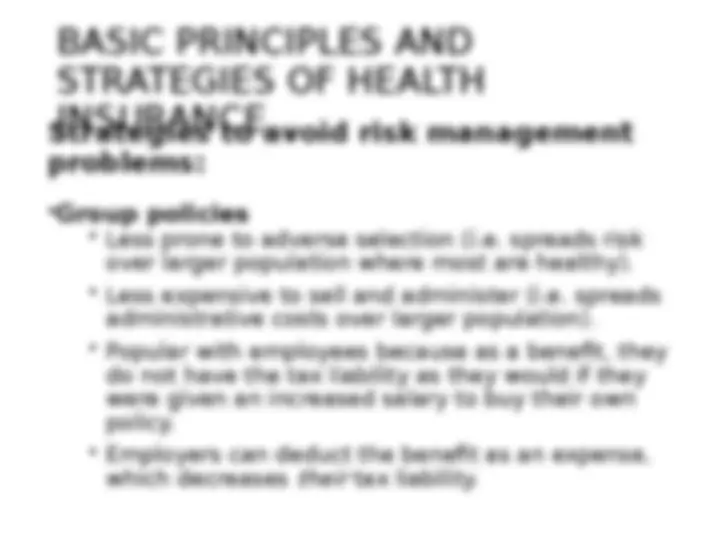

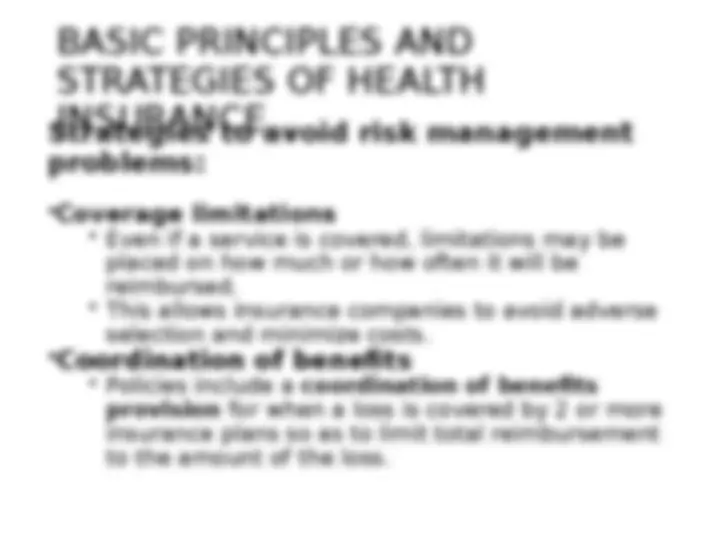

Strategies to avoid risk management problems:

- Group policies

- (^) Less prone to adverse selection (i.e. spreads risk over larger population where most are healthy).

- (^) Less expensive to sell and administer (i.e. spreads administrative costs over larger population).

- (^) Popular with employees because as a benefit, they do not have the tax liability as they would if they were given an increased salary to buy their own policy.

- (^) Employers can deduct the benefit as an expense, which decreases their tax liability.