AUDITING

1. SYSTEMATIC PROCESS OF F/S AUDIT

2. AUDIT PLANNING

3. AUDIT EVIDENCE

4. AUDIT DOCUMENTATION

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth exploration of the systematic process of financial auditing, focusing on audit planning, evidence gathering, documentation, and risk assessment. It covers topics such as pre-engagement activities, evaluating management integrity, materiality assessment, and the audit risk model.

Typology: Slides

1 / 28

This page cannot be seen from the preview

Don't miss anything!

_1. SYSTEMATIC PROCESS OF F/S AUDIT

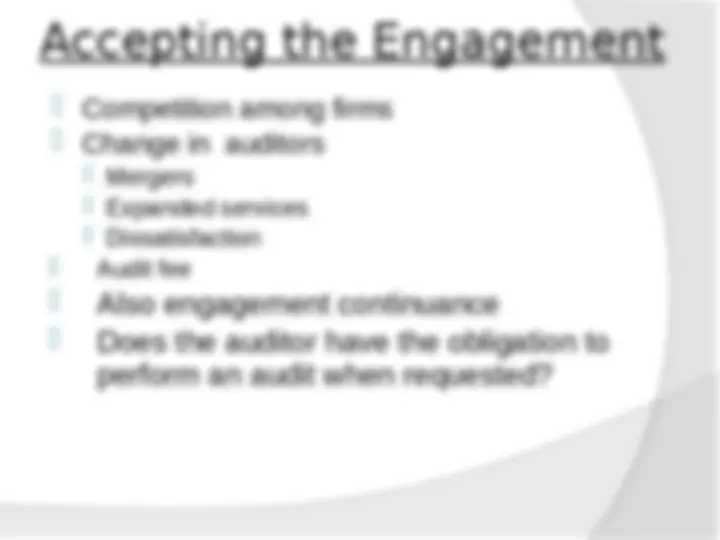

Accepting the Engagement (^) Competition among firms (^) Change in auditors (^) Mergers (^) Expanded services (^) Dissatisfaction (^) Audit fee

Evaluating the Integrity of Management (^) Trust in management (^) Management lacking in integrity? (^) Evaluation of Management Integrity a. Make inquiries of third parties

SYSTEMATIC PROCESS OF F/S AUDIT Pre-engagement and Audit Planning Audit Planning - developing a general strategy & a detailed approach for the expected nature, timing & extent of the audit. The auditor plans to perform the audit in an efficient & timely manner.

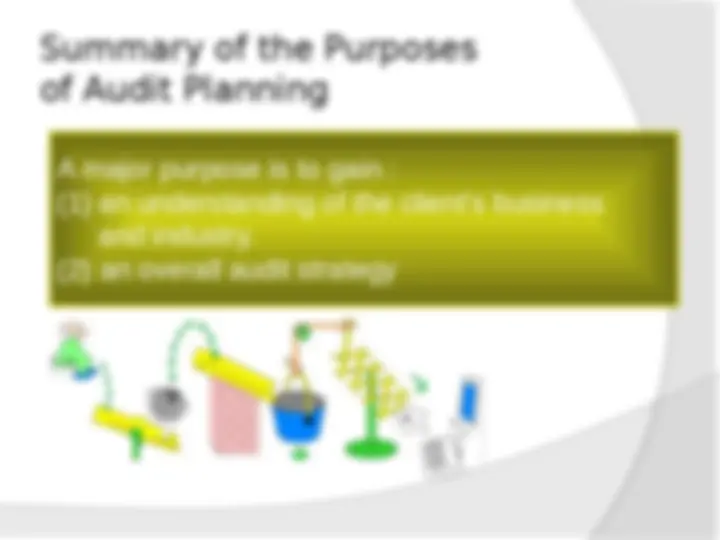

A major purpose is to gain : (1) an understanding of the client’s business and industry. (2) an overall audit strategy

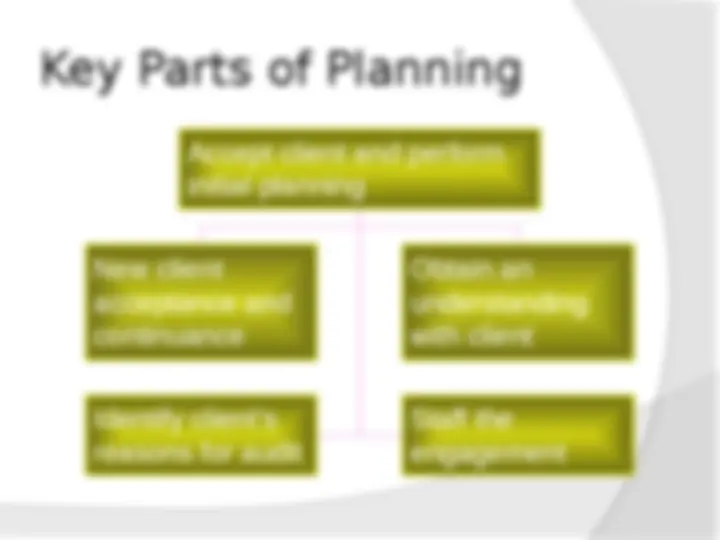

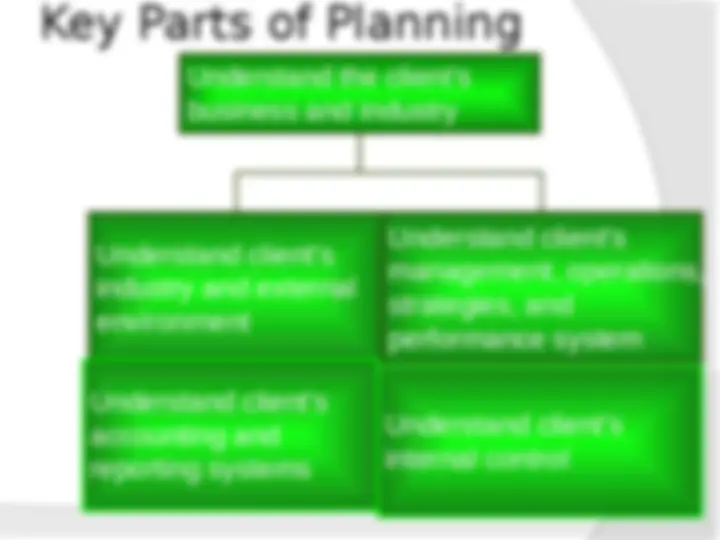

Key Parts of Planning Understand the client’s business and industry Understand client’s industry and external environment Understand client’s management, operations, strategies, and performance system Understand client’s accounting and reporting systems Understand client’s internal control

What are some reasons for obtaining an understanding of the client’s industry and external environment?

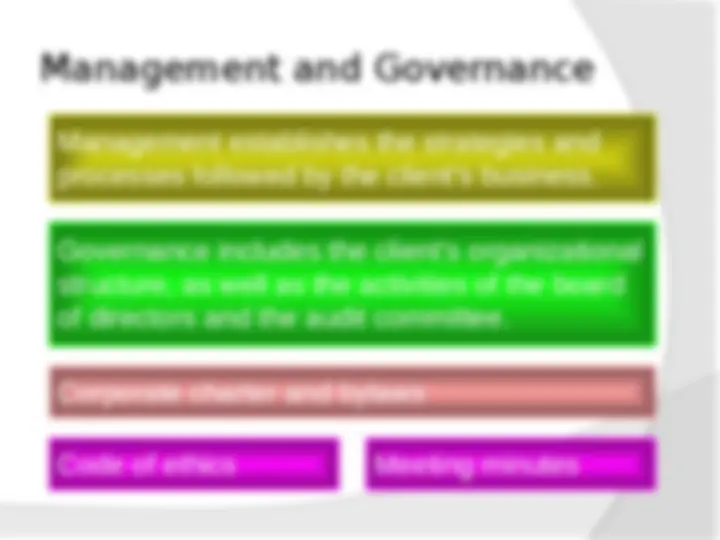

Management and Governance Management establishes the strategies and processes followed by the client’s business. Governance includes the client’s organizational structure, as well as the activities of the board of directors and the audit committee. Corporate charter and bylaws Code of ethics Meeting minutes

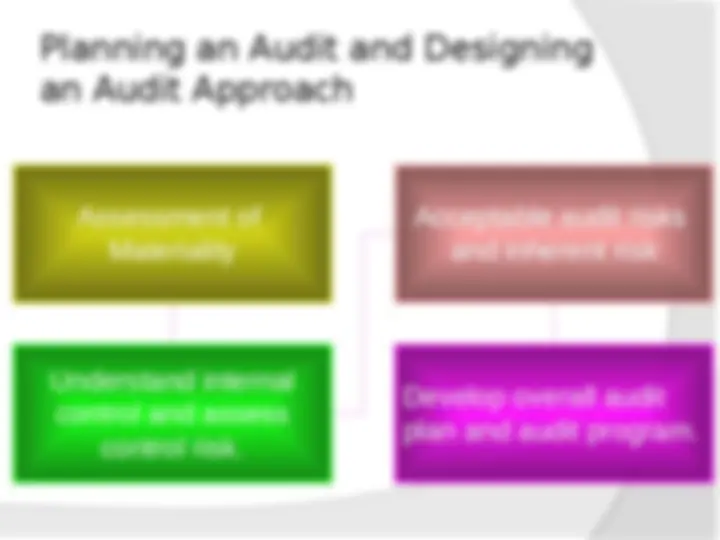

Assessment of Materiality Understand internal control and assess control risk. Acceptable audit risks and inherent risk Develop overall audit plan and audit program.

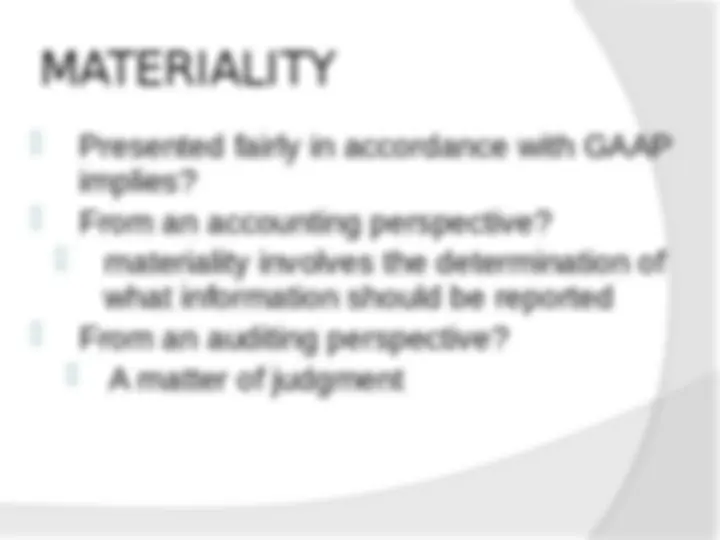

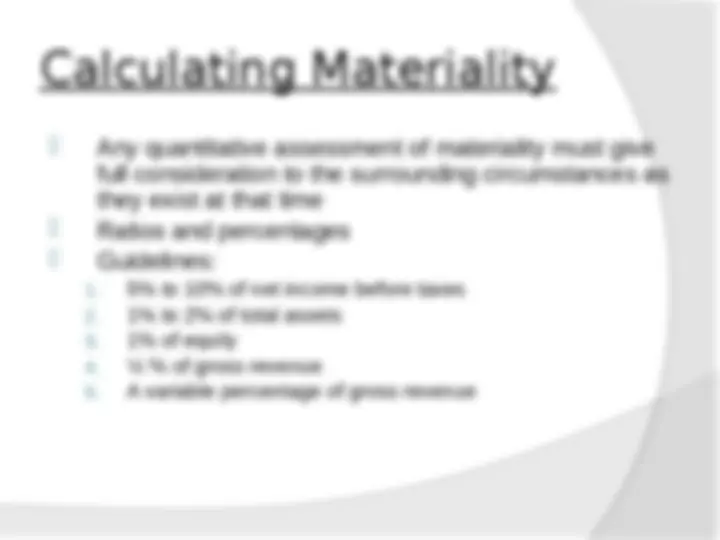

(^) It requires the auditor to consider (^) Circumstances of the company (^) The users of the F/S (^) The auditor makes a preliminary judgment about materiality levels in planning the audit (^) May ultimately differ from materiality levels used in evaluating audit findings

(^) Materiality involves both qualitative and quantitative considerations (^) In assessing the quantitative amount it is

amount to the F/S (^) In planning, the auditor is usually concerned with just the quantitative (^) Qualitative?

Qualitative Factors Should answer the following questions

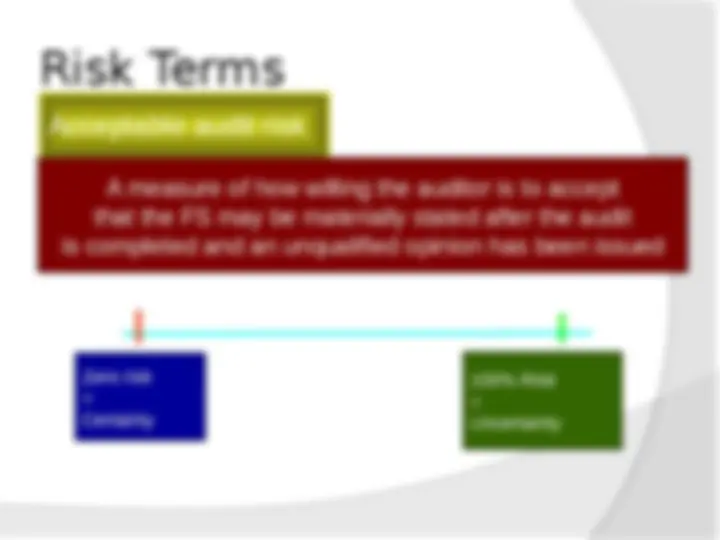

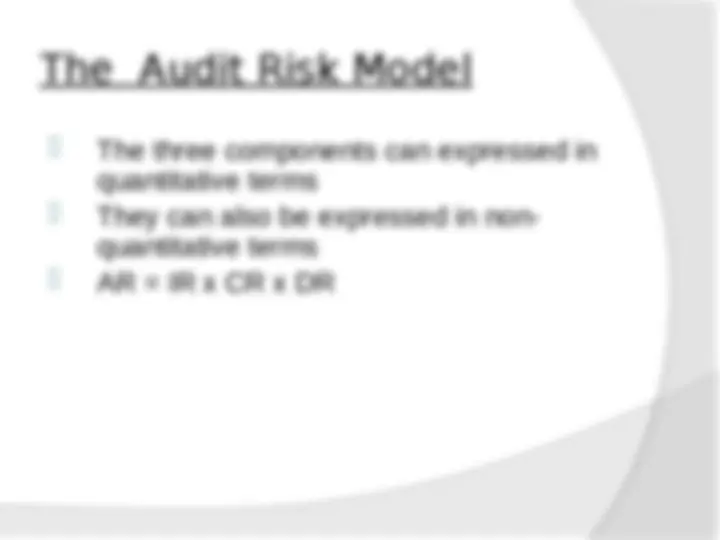

On the basis of the initial information gathered by the auditor, he then assesses the AUDIT RISK Control risk Detection Risk Inherent risk