Download Optimal Portfolio Allocation with Parameter and Model Uncertainty: Multi-Prior Approach and more Slides Banking and Finance in PDF only on Docsity!

Comparison with Bayes-Stein Approach

I Bayes-Stein portfolio

wBS = φBS wM IN + (1 − φBS) wM V , (11)

where φBS =

N + (N +2)+T (ˆμ−μM IN 1 N )>Σ−^1 (ˆμ−μM IN 1 N )

I Multi-prior portfolio

wM P = φM P wM IN + (1 − φM P ) wM V , (12)

where φM P (�) =

( (^) √ ε γσ P∗ +

√ ε

)

=

√ �

(T −1)N T (T −N )

γσ∗ P +

√ �

(T −1)N T (T −N )

Example 3 - General Case

Uncertainty about expected returns estimated for subsets of

assets

I Let Jm = {i 1 ,... , iNm}, m = 1,... , M , be M subsets of { 1 ,... , N },

each representing a subset of assets.

I The constraint set for each subset of assets is

{ Tm(Tm − Nm)

(Tm − 1)Nm

(ˆμJm − μJm)

Σ

− 1 Jm (ˆμJm^ −^ μJm)^ ≤^ �m

}

Example 4

Uncertainty about factor-generating model and expected returns

I N risky assets and K factors

I Return-generating model model (excess returns)

rat = α + βrf t + ut, cov(ut, u

t ) = Ω,^ (15)

I Hence, mean and variance of the returns can always be expressed as

μ =

( α + βμf

μf

)

( βΣf f β

Σf f β

Σf f

)

Multi-Prior Asset Allocation

max w

minμa,μf w

μ −

γ

w

Σw, (17)

subject to

(ˆμa − μa)

Σ

− 1

aa (ˆμa^ −^ μa)^ ≤^ �a,^ (18)

(ˆμf − μf )

Σ

− 1

f f (ˆμf^ −^ μf^ )^ ≤^ �f^.^ (19)

I If �f = 0 and asset pricing model holds

- μˆa = βμf

- equation (18) is a multi-prior version of model uncertainty

- If �a = 0 ⇒ investor believes dogmatically in the model

I If �f > 0 , allocation depends on

- relative degree of uncertainty aversions: �f vs. �a

Empirical Application 1

Uncertainty about Expected Returns:

International Data

I Data

- MSCI month-end US$ value of equity index: Jan 1970–Jul 2001

- for 8 countries (CA, FR, GE, JP, IT, SW, UK, US)

I Rolling Windows

- Determine portfolio based on 60-month-window, and

- With these weights, calculate return in 61

st

month.

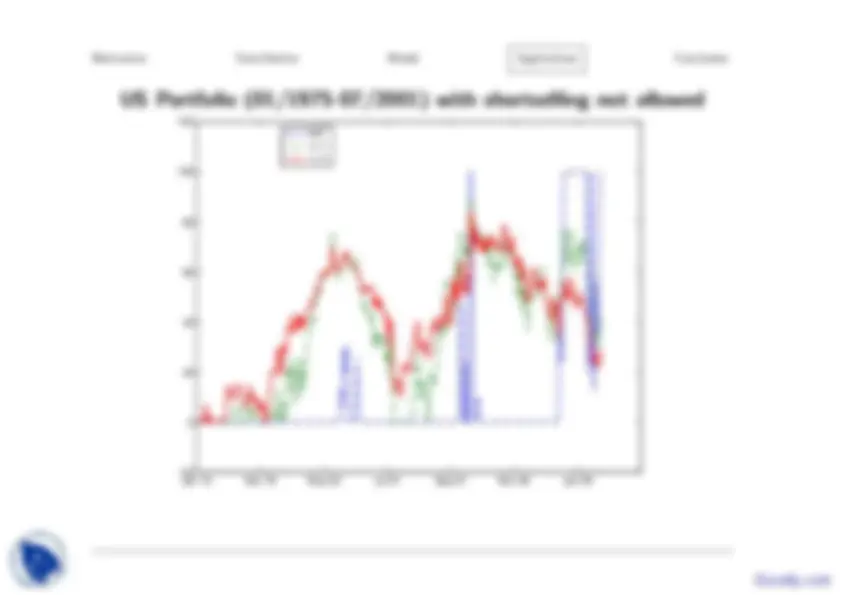

I Short-Selling Constraints Consider two cases:

- Short-selling is allowed, and

- Short-selling is not allowed.

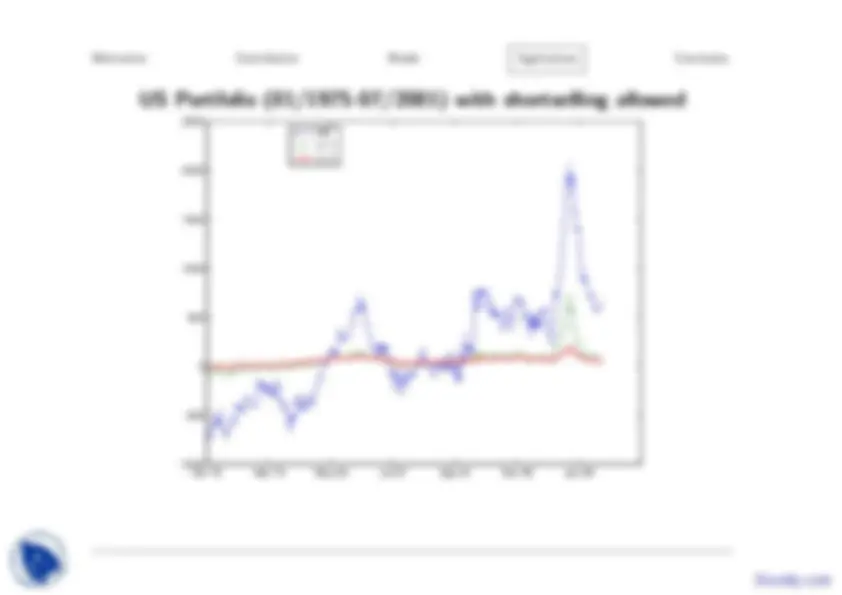

US Portfolio (01/1975-07/2001) with shortselling allowed

Jan 75 Mar 79 May 83 Jul 87 Sep 91 Nov 95 Jan 99

−

−

0

500

1000

1500

2000

2500 MV ε= 1 ε= 3

Out-of-Sample Performance Analysis

I From the rolling-windows-portfolios, compute the out-of sample

1. Mean

2. Volatility

3. Ratio of mean to volatility

I Compare performance of multi-prior portfolio with

1. Mean-variance portfolio

2. Bayes-Diffuse-Prior (with μ = ˆμ and Σ =

(

1 +

1 T

)

3. Bayes-Stein (with μ = ωμmvp + (1 − ω)ˆμ)

Panel A: Short sales allowed

Strategy Mean Std.Dev.

Mean Std.Dev.

- Mean-Variance -0.517 42.085 -0.

- Bayesian approach

- Diffuse Prior -0.491 41.394 -0.

- Empirical Bayes-Stein -0.162 17.508 -0.

- Multi-prior approach

Empirical Application 2

Uncertainty on Expected Returns and Pricing Model:

US Domestic Data

I Data

- Assets. Monthly returns on HML and SMB: Jul 1926 to Dec 2002.

- Factor. Monthly excess return on MKT

NYSE, AMEX and NASDAQ stocks (from CRSP)

I Rolling Windows

- Determine portfolios based on 120-month window, and

- With these weights, calculate return in 121

st

month.

Portfolio weights

I Consider weights in SMB, HML, MKT

- When CAPM is used for estimating expected returns

(aversion to both parameter and model uncertainty)

- “Skeptical Bayesian” uses MLE (Maximum Likelihood Estimates).

- “Dogmatic Bayesian” uses CAPM (Capital Asset Pricing Model).

I Compare to Bayesian “Data and Model” approach of Pastor and

Stambaugh

Out-of-sample Sharpe Ratios (MLE reference estimate)

Strategy Sharpe Ratio

- Mean-Variance 0.

- Bayesian approach

- Bayes-Stein 0.

- Pastor-Stambaugh

with data only 0.

with ω = 0. 00 0.00 0.50 1.00 1.

% (0.0) (38.20) (68.07) (86.37)

�a %

Out-of-sample Sharpe Ratios (with CAPM used for estimation)

Strategy Sharpe Ratio

- Mean-Variance 0.

- Bayesian approach

- Bayes-Stein 0.

- Pastor-Stambaugh

with model only 0.

with ω = 1. 00 0.0 0.5 1.0 2.0 2.5 3.

% (0.0) (38.20) (68.07) (95.22) (98.62) (99.67)

�a %