MODUL-8

Financial Accounting

Financial Statement Analysis

By

MUH. ARIEF EFFENDI,SE,MSI,AK,QIA

Magister Accounting Program (MAKSI)

BUDI LUHUR UNIVERSITY

Jakarta - Indonesia

2010

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

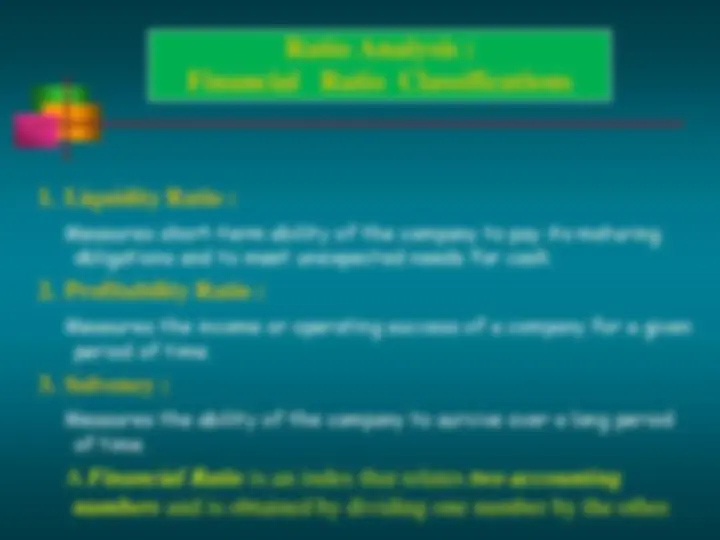

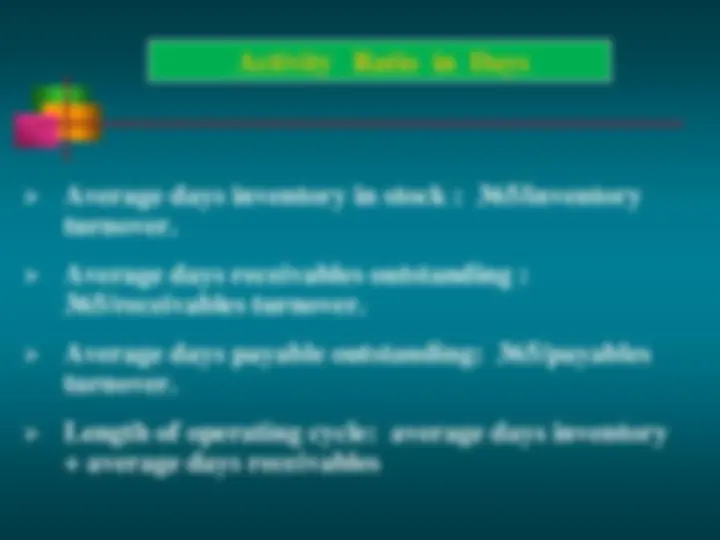

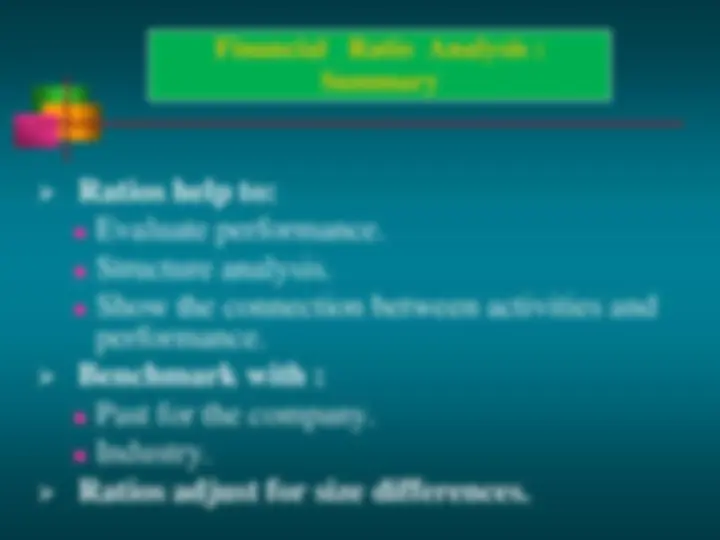

Limitations of Ratio Analysis. 8. Understand the Classification of Financial Ratio Analysis (Liquidity, Profitability, and solvency Ratio).

Typology: Study notes

1 / 58

This page cannot be seen from the preview

Don't miss anything!

By MUH. ARIEF EFFENDI,SE,MSI,AK,QIA

After studying this topic, students should be able to:

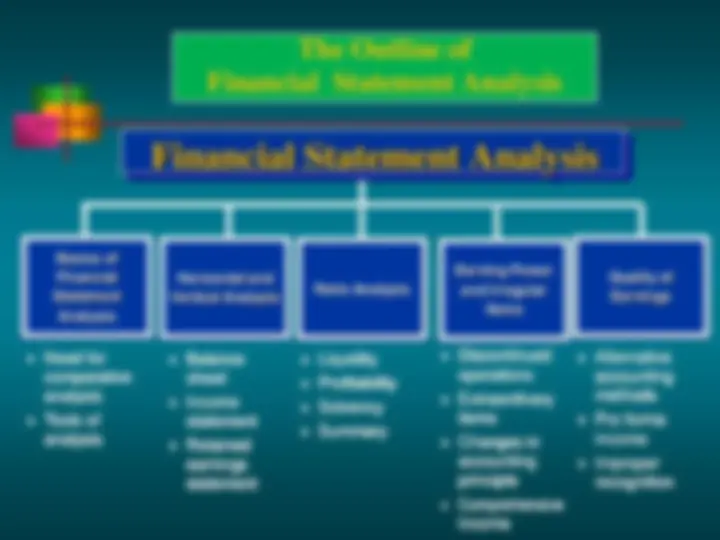

Analyzing financial statements involves:

Characteristics Comparison Bases Tools of Analysis

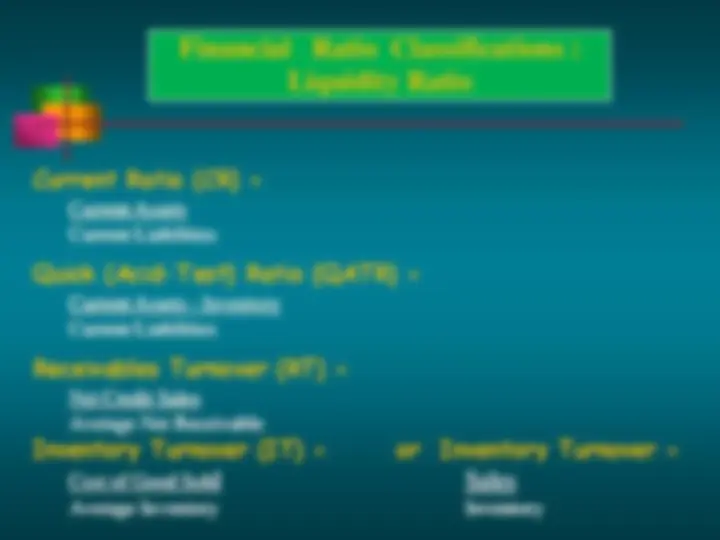

Liquidity

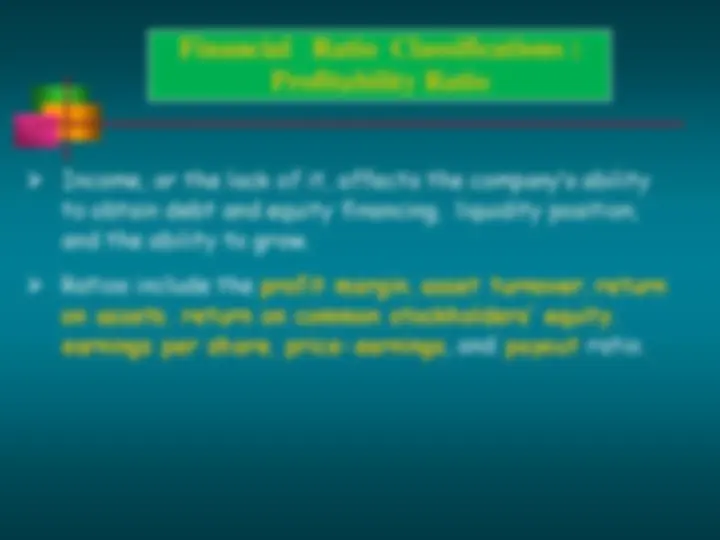

Profitability

Solvency

Intracompany Industry averages Intercompany

Horizontal Vertical Ratio

Basics of Financial Statement Analysis

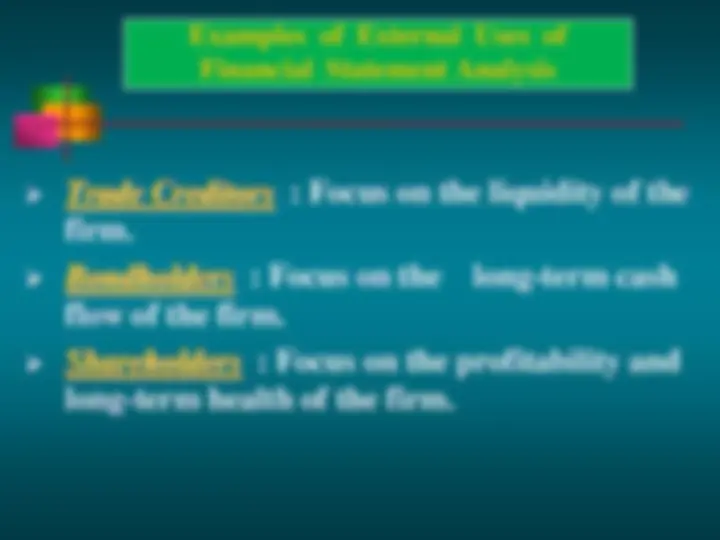

Examples of External Uses of Financial Statement Analysis

Analytical Tools Used Sources and Uses Statement Statement of Cash Flows Cash Budgets

Trend / Seasonal Component How much funding will be required in the future? Is there a seasonal component?

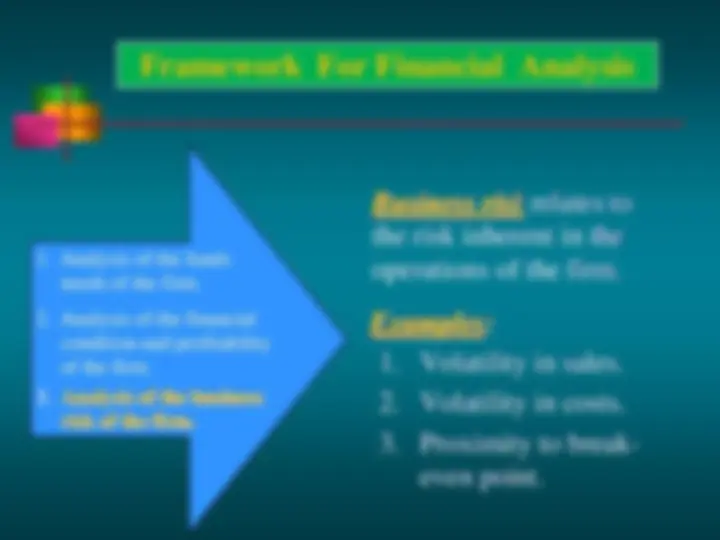

Health of a Firm

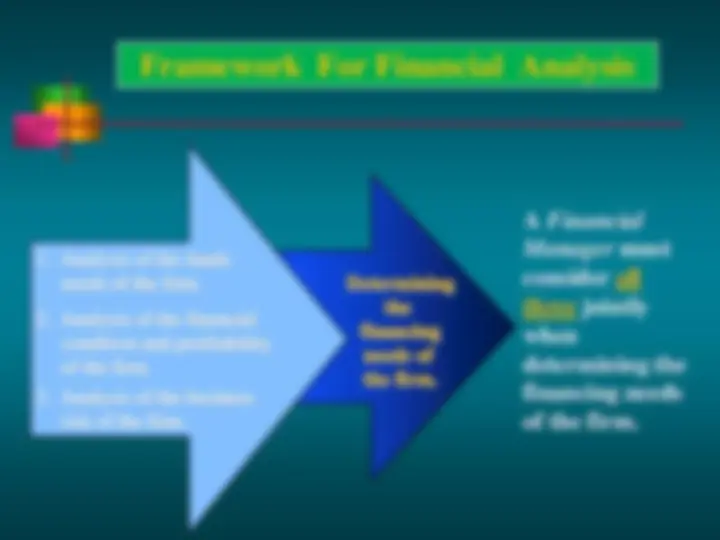

A Financial Manager must consider all three jointly when determining the financing needs of the firm.

Determining the financing needs of the firm.

Analysis of the funds needs of the firm.

Analysis of the financial condition and profitability of the firm.

Analysis of the business risk of the firm.

Negotiations with suppliers of capital.

Determining the financing needs of the firm.

Quantitative Financial Analysis

Financial Ratios : is an index that relates two

accounting numbers and is obtained by dividing one number by the other.

Growth / trend Analysis / Horizontal Analysis.

Quarterly analysis.

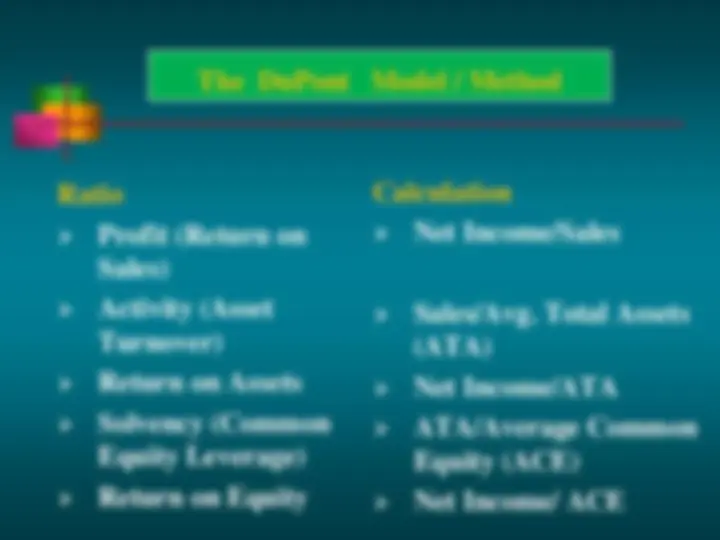

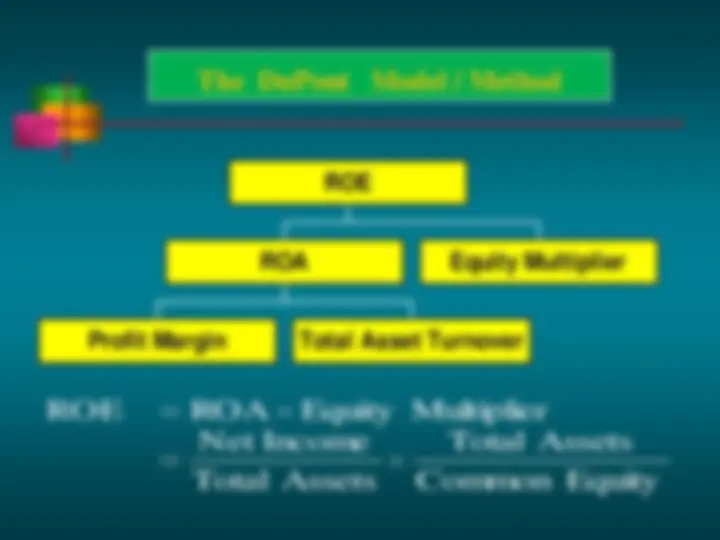

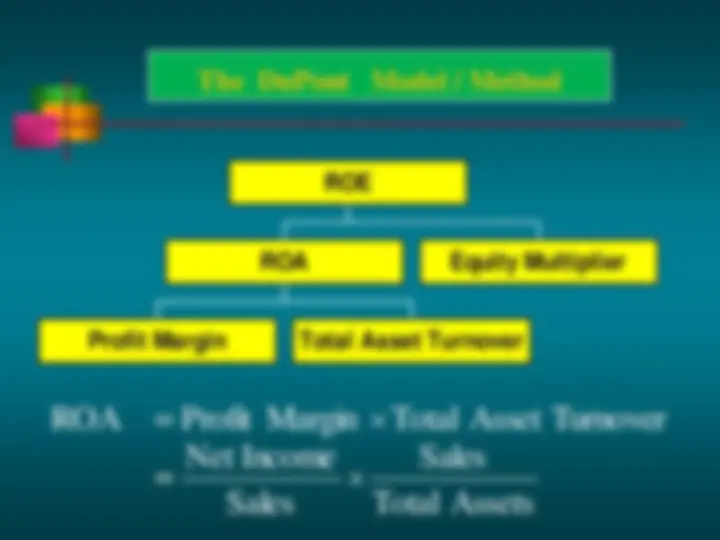

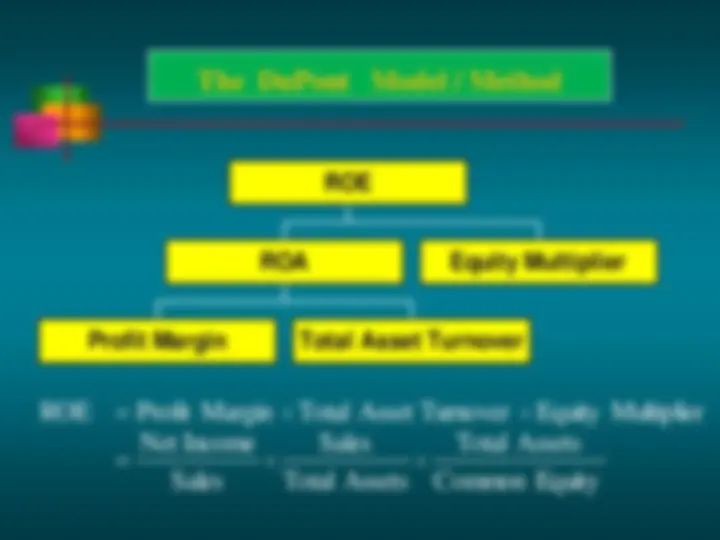

The DuPont Model / Method.

Earning Quality / Normalizing Earning..

Quantitative Financial Analysis

Tools of Analysis : Horizontal Analysis / Trend Analysis / Growth Analysis

Horizontal analysis , also called trend analysis , is a

technique for evaluating a series of Financial Statement (FS) data over a period of time.

Its purpose is to determine the increase or decrease

that has taken place.

Horizontal analysis is commonly applied to the Balance

Sheet (BS), income statement, and Statement of Retained Earnings (RE).

Quantitative Financial Analysis : Growth Analysis (Period- By-Period Change)

Long-term trends over time can be significant. Are current year performance measures consistent with earlier years (e.g., maintaining consistent ratios while sales are rising smoothly)?

As a first step, present growth rates (including % increases) for the last 5-10 years.

Declining or negative growth rates might be obvious red flags; Red flags and other indicators of poor growth performance require further analysis.

Quantitative Financial Analysis : Quarterly Analysis

The most recent financial data is presented quarterly (e.g., 10-Q). [The one exception is at year end, with annual information is presented].

Financial analysts focus on quarterly data and the quarterly earnings announcement is the most important (& earliest) information.

Common-size and ratios analysis is conducted, and compared over earlier quarters: particularly important are current quarter data to (1) the previous quarter and (2) the same quarter one year ago.

Tools of Analysis : Vertical Analysis

Vertical analysis , also called common-size analysis ,

is a technique that expresses each Financial Statement (FS) item as a percent of a base amount.

On an Income Statement (IS) , we might say that

selling expenses are 16% of net sales.

Vertical analysis is commonly applied to the Balance

Sheet (BS) and the Income Statement (IS).