Econometrics

Chapter 6: Multiple Regression

Model

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

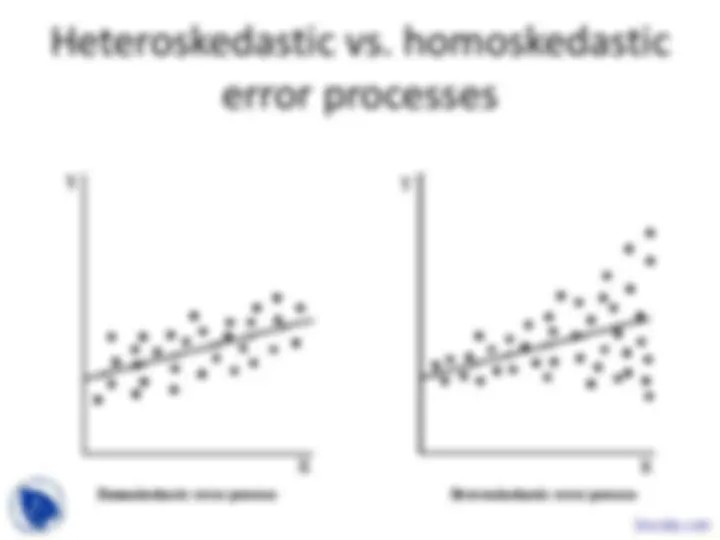

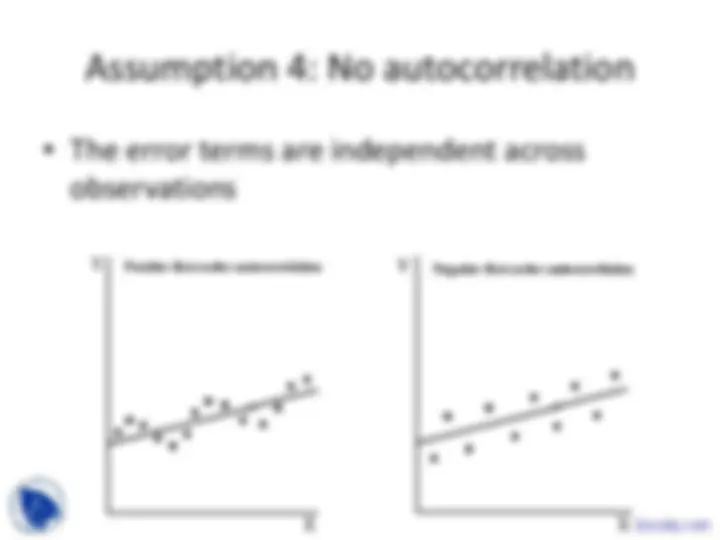

Its the important key points of lecture slides of Econometrics are:Multiple Regression Model, Population Regression Function, Sample Regression Function, Classical Regression, Lowest Variance, Unbiased Estimators, Linearity, Homoskedasticity, Possible Combinations, No Autocorrelation`

Typology: Slides

1 / 23

This page cannot be seen from the preview

Don't miss anything!

Chapter 6: Multiple Regression Model

With a bit of algebraic manipulation: