Download Netflix Financial Analysis: Revenue Growth and Margin Forecasts (2022) and more Lecture notes Business in PDF only on Docsity!

Important disclosures appear on the last page of this report.

The Henry Fund

Henry B. Tippie College of Business William Marietti [[email protected]]

NETFLIX INC. (NFLX) March 11, 2022

Communications – Entertainment Stock Rating HOLD

Investment Thesis Target Price $225-$

Netflix is a powerhouse in the streaming industry and is the status quo when it comes to this form of entertainment. The release of managements lower guidance has spooked investors resulting a significant drop in share price. We believe this devaluation is not a death sentence for Netflix and that slowing subscriber growth is just a reflection of a maturing industry.

Drivers of Thesis

- Netflix has and will likely continue to invest in gaming, leveraging its streaming platform and content licenses to enter an exploding industry.

- Regions like Asia will continue to see exponential subscriber growth driven by an increasingly diverse content library, reaching 34 million users by

- Further investments into exclusive original content will make Netflix stand out compared to lower budget competitors.

Risks to Thesis

- An increasingly competitive industry could eat into Netflix’s market share, requiring more investments into original content and lowering margins.

- Netflix might have to raise subscription costs significantly in order to keep up with content spending which could steer customers towards cheaper alternatives.

- The lack of a free, ad-based subscription offering puts Netflix at a potential disadvantage against peers.

Henry Fund DCF $ Henry Fund DDM $ EV/Subscribers $ Price Data Current Price $ 52wk Range $700 – $ Consensus 1yr Target $ Key Statistics Market Cap (B) $158. Shares Outstanding (M) 444. Institutional Ownership 94.9% Beta 0. Dividend Yield 0% Est. 5yr Growth 27.97% Price/Earnings (TTM) 33. Price/Earnings (FY1) 32. Price/Sales (TTM) 5. Price/Book (mrq) 9. Profitability Operating Margin 20.9% Profit Margin 17.23% Return on Assets (TTM) 12.2% Return on Equity (TTM) 38.0%

Earnings Estimates Year 2019 2020 2022 202 2E 2023 E 2024 E EPS HF est.

$4.13 $6.08 $11.24 $11. $12.

$14. $12.

$16. $13. growth 54.1% 47.2% 84.9% 0.30% 0.3 2 % 0. 35 % 12 Month Performance Company Description Netflix Inc. is a subscription-based entertainment service that allows users to stream content from multiple kinds of devices. Originally in the business of mailing DVD’s, Netflix has transitioned to becoming a leader in the streaming industry, with around 222 million subscribers globally. Netflix’s revenue primarily derives from monthly membership fees, which varies by geographic region. In recent years, the company has increased spending on originally produced content. Netflix also operates a gaming service that is included in a standard membership.

19.

3.

14.

16.

2.

12.

0

5

10

15

20

25

P/E (2022E) EV/Revenue EV/EBITDA

NFLX Sector Average

-60%

-40%

-20%

0%

20%

A M J J A S O N D J F M

NFLX S&P 500

Page 2

COMPANY DESCRIPTION

Netflix is an internet streaming service that allows users to watch movies and TV on multiple different devices. They operate two main segments, streaming and DVD. As DVD continues to die out, streaming has become the focal point of Netflix’s revenue. Netflix offers tier-based subscription pricing, with each tier allowing the user more flexibility in terms of accounts linked to the subscription and even video quality. The Basic plan starts at $9.99 a month and allows one user to access the account at a time. The Premium plan starts at $19.99 and can allow multiple users at once as well as 4k video quality.

Netflix is available in 190 countries with the US/Canada region being the largest and most profitable. Around 20.5% of the total adult populations of the US and Canada have a Netflix subscription. The second most developed region is Latin America, with 6% of the population having a subscription as of 2021^17.

Source: NFLX 10k

Netflix licenses media from multiple sources including production studios and other entertainment companies. In recent years, Netflix and others in the industry have shifted more towards in-house content production, with around 40% of their content being originally produced. This has been driven by increasing competition in the

industry, as many firms who once licensed content out now manage their own streaming platforms. The phenomenon has sparked increased M&A in the industry, such as Amazon acquiring MGM Studios this past year.

United States/Canada

The US and Canada (UCAN) make up Netflix’s largest customer base with around 75 million subscribers in total. On top of being the largest by number of customers, the region also is the most profitable, with revenue per subscriber of $14.37 per month. Subscriber growth in this region has been on the decline since 2017. While Netflix still attracts new members each year, the acceleration that was seen earlier in its lifespan has begun to reach an equilibrium.

Source: NFLX 10k

Revenue per subscriber has risen significantly since 2017. An influx of subscribers in 2020 due to the COVID- pandemic caused this number to become diluted, resulting in price hikes in 2021. Netflix currently has penetrated 20.5% of UCAN households. We project this penetration rate to rise to around 25.7% by 2031, implying one in four households will have a subscription by then. This will put Netflix at around 94 million subscribers in total. We also project revenue per subscriber to increase substantially in this region to around $21 by 2031. We believe price hikes in this region will be necessary to support the increased spending on content. The US and Canada will likely be less

33.91%

33.37%

18.01%

14.71%

Percentage of Total

Subscribers by Geographic

Region

US/Canada Europe/Middle East/Africa Latin America Asia Pacific

0

10

20

30

40

50

60

70

80

2017 2018 2019 2020 2021 2022E 2023E 2024E 2025E

US/Canada Subscribers

(millions)

Page 4

subscriber growth has been minimal over the last few years, with price cuts in 2020 resulting in -5.5% growth YoY. Despite these issues, Netflix has made good progress penetrating the region, with 6% of the population having a subscription. We project this share to grow to 14% of the population by 2031, driven by the similarity of the UCAN and LATAM markets in terms of preferred content. This will put the segments total subscriber’s around 92 million, roughly on par with the UCAN market. We do believe however that revenue per subscriber growth will be slow due to the economics of the region and the perceived sensitivity to price hikes.

Asia Pacific

The Asia Pacific (APAC) segment has the smallest subscriber base out of the group but has seen the largest amount of growth over the last four years. This region is vast and covers continental Asia which includes India. This excludes China, as it has been outlawed there. The segment has seen incredible growth due to Netflix’s overseas hits like SquidGame which launched Netflix into the spotlight in Korea as well as other Asian countries. Despite not being able to tap into the Chinese market due to regulation, Netflix has managed to enter a sizable portion of what initially seemed to be a very foreign market. After the release of SquidGame, it was realized that many overseas hits can be marketed toward UCAN consumers and vice versa.

Source: NFLX 10k

The chart above perfectly summarizes Netflix’s explosion in the APAC segment. With a current penetration rate of 0.72%, we believe Netflix can reach a 3% penetration in the APAC market by 2031, amassing 85.5 million subscribers. We also believe that price hikes are inevitable for this segment although not as high as the UCAN region. This is partly due to low entertainment prices in India limiting how high prices can go before users abandon ship for cheaper alternatives.

Cost Structure Analysis

Netflix’s largest cash expense category is their Cost of Subscription Revenue account. This account can be broken out into two main types of expenses. The first type of expense included in this account is the amortization of content assets. Content assets include all licensed and produced content. This account is amortized overtime on an accelerated basis to reflect higher viewership at the beginning of a show’s life on the platform. The other costs included in the Cost of Subscription Revenue account are expenses related to the acquisition, licensing, and production of content^17. These costs (not including amortization) have trended upward over the years, representing about 11% of total revenue in 2017 to making up 16.5% in 2021. We attribute this to Netflix’s aggressive plan to become self-reliant when it comes to content, resulting in increased spending on in-house production. We believe their cost of subscription revenue will remain at a steady margin going forward at 16.6% of revenue as the company continues to reach a steady-state and the expansive growth of the path winds down.

0

5

10

15

20

25

30

35

40

2017 2018 2019 2020 2021 2022E 2023E 2024E 2025E

APAC Subscribers (millions)

UCAN EMEA LATAM APAC

Revenue Per Subscriber (Per

Month)

Page 5

Source: NFLX 10k

Marketing expenses make up the second-largest expense that Netflix incurs. As of 2021, these costs make up about 8.6% of their revenue. This number has been on a steady decline since 2018 which was at 15% of revenue. The decrease in these costs is likely related to Netflix having the content it acquires “sell itself” in the sense that having popular shows/movies will encourage people to sign up better than any advertisement would. We project the margin here to elevate slightly and remain consistent through the forecasted period at 11.5% of revenue. Penetration into less developed markets may require increased spending to create brand awareness, despite having blockbuster hits on the platform.

Content spending makes up most of Netflix’s liabilities. These fees are marked down as liabilities once the content becomes available on Netflix to stream, rather than when they are purchased. They are then amortized on an accelerated basis and expensed on the income statement as Amortization of Content Assets.

Non-Streaming Products/Services

DVD

Netflix was originally started as an alternative to stores like Blockbuster, allowing users to order DVDs via mail and return them at a later date. The advent of streaming has made the industry obsolete, however, Netflix still allows US subscribers to sign up and receive DVDs at their door. Netflix essentially spun off this business back in 2011, rebranding it as DVD.com. As expected, this segment has

declined significantly over the last 10 years. While there are no plans to discontinue the service as of now, we have forecasted -20% growth in revenue during the first half of our period, accelerating to -40% during the second half. The graph below depicts DVD revenue in historical and forecasted periods.

Source: NFLX 10k

Netflix Games

In November of 2021, Netflix launched Netflix Games globally. The service allows users to play mobile games based on Netflix’s original content. Requiring a mobile device and a basic subscription, users can play games add- free from anywhere with an internet connection. Titles include many of Netflix’s most popular hits, including Stranger Things 3: The Game. Netflix has started to ramp up investing into this area, with two recent acquisitions of game design studios. We suspect that future endeavors may include allowing users to stream the latest blockbuster games to their TV.

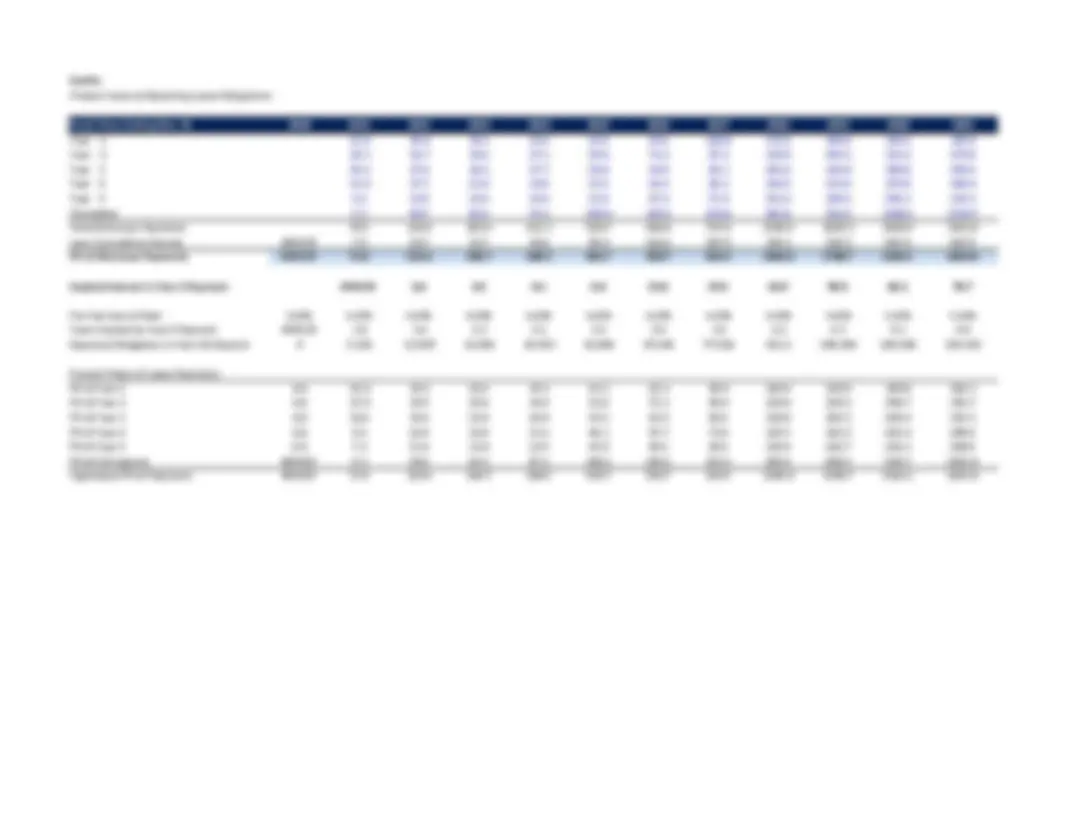

Debt Maturity Analysis

All of Netflix’s debt is in the form of unsecured bonds, totaling over $14.5 billion dollars, $700 million of which matured in mid-February 2022. Netflix has a credit rating of BBB from Standard and Poor’s Netflix had no reported issues paying off this principle and did not opt to refinance it either. As seen in the debt maturity schedule below, after February’s payment the next maturity will come in 2024 at around $400 million dollars. We believe Netflix will have no issue paying this off and will not likely refinance

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Historical and Forecasted

Margins

NI Margin Operating Margin

0

200

400

600

800

1000

1200

DVD Revenue (millions)

Page 7

growth, likely due to tougher economic conditions affecting discretionary spending.

Next Games Acquisition

On March 4th, 2022, Netflix announced it was acquiring Next Games, a video game developer from Finland. The all- cash deal is valued at $61.5 million and is expected to be completed by the end of June 202219. This deal is significant in the sense that it highlights Netflix’s desire to ramp up its gaming department. It has long been speculated that Netflix and others in the industry would move into the gaming space as they possess the necessary technology. As mentioned before, Netflix launched Netflix Games in late 2021, allowing subscribers to play mobile games based on popular Netflix titles. We suspect this acquisition will one of many more in the future as Netflix expands its reach into gaming.

INDUSTRY TRENDS

Original Content

As new firms enter the market, the need for high-quality original programming increases. Firms like Disney who once licensed their content to Netflix now operate in competition. This has forced Netflix and others to become self-reliant and create their own entertainment. The industry is now starting to realize that exclusive content is the best way to win new subscribers, whether these subscribers stick around will be discussed later. Shows like Disney’s The Mandalorian and AppleTV’s Ted Lasso have attracted new users to the platform in search of the best bang for their buck when it comes to content. Social media has also played a huge role in this trend too. People on Twitter and other platforms share their opinions on these shows, making others interested and the show going viral. Such as the case of Netflix’s SquidGame which became a global sensation after being praised on social media. Original content provides major value to subscribers who might be choosing between services. A service that consistently produces award-winning, original content is likely to outperform.

International Content

Netflix’s SquidGame became the most streamed television show on Netflix of all time in a matter of 4 weeks^11. Originally produced for the Korean market, SquidGame became a global sensation, pushing aside previous beliefs

that foreign content wouldn’t do well in American markets. This notion was soon dismissed as the show took over the globe like wildfire. Another example of this trend is the increasing popularity of anime, a Japanese style of cartoon targeted towards young adults. These shows have made their way on to almost every streaming platform. Crunchyroll, owned by Funimation, is a streaming service dedicated to these shows and has grown in popularity significantly over the years. The graph below shows the number of subscribers for Crunchyroll since 2012. Platforms like Netflix have increased the amount of anime they offer significantly over the years, as the shows have seen great success in American markets.

Source: Statista

The ability to air international content overseas is a huge benefit for streaming services as it allows them to maximize viewership.

Subscriber Retention Rates

Recent data has shown subscriber trends around key releases of content. New subscriptions tend to spike around anticipated releases, slowly trickling off months after the release. Some platforms see as much as 50% of their new sign ups leave after 6 months of a major release 5. Losing subscribers is not new for any of these platforms. Almost all lose some portion of subscribers every month, these are made up for though with new subscribers to have a net overall increase. This phenomenon however sees users leaving at much faster rates than previously seen. Firms have been trying to combat this by consistently

0

1

2

3

4

Number of Crunchyroll

Subscribers (millions)

Page 8

producing hits to keep people on board. The graph below shows the retention rates of subscribers after major releases.

Source: Wallstreet Journal

While this may strike an immediate concern for most, the net benefit companies realize make up for lost subscribers. Although many people leave, the net level of users is significantly higher than before the release. The population who leaves after these releases has created a new segment of customer. These individuals will likely continue this pattern of behavior in the short term, but we project this group to fully commit to a streaming service in the long term as content continues to be released on a more consistent basis.

MARKETS AND COMPETITION

Barriers to Entry

The video streaming industry has a large barrier to entry for most looking to join. Initial capital requirements including the latest tech and software make entry difficult. This is coupled with a highly skilled workforce required to maintain and innovate servers as well as perform viewership analytics. Along with physical capital requirements, a large and diverse library of digital content is necessary to stand out amongst the competition. This would require licensing from studios and possibly investing into original content. Companies that already have the technology to stream content as well as obtain media rights have a better chance at entering this industry than others. For example, a firm like Disney which already

owns a large amount of content had an easy time entering the industry. Their portfolio of content is a competitive advantage, and current industry participants need to be wary of others who could potentially enter too.

Threat of Substitutes

The threat of substitutes in this industry is extremely high and will only continue to increase. As mentioned before, the average U.S. household subscribes to around 3 streaming services. This creates major competition between players in the industry as they fight to get a spot on each household’s roster. Firms must continue to license popular content as well as produce their own hit pieces in order to keep up with the competition. With new services popping up all the time, firms must continually prove their worth to consumers. This usually comes in the form of acquiring the rights to blockbuster hits and original content. With monthly fees uniform throughout the industry, substitution is always a concern for players in this industry.

Peer Comparisons

The video streaming industry is dominated by entertainment and communications firms. The table below outlines the parent companies of the major streaming services. At the time of this report, the merger of Discovery and AT&T’s Warner Media is still pending. The acquisition would make HBO and Crunchyroll a part of Discovery+.

ViacomCBS

ViacomCBS is a media and entertainment conglomerate that operates television networks, film studios, and streaming services. Its streaming portfolio includes Paramount+, BET+, and PlutoTV. Offering some of the cheaper subscriptions in the industry, ViacomCBS offers bundling packages for a discount on their services. In total, ViacomCBS has around 4% total market share of the streaming industry 13.

Page 10

Lions Gate Entertainment

Lions Gate Entertainment own and operates several entertainment companies in the U.S. and Canada. Their flagship Lionsgate Films is a film production and distribution studio. Their streaming service STARZ has around 30 million subscribers globally making it one of the smaller players in the industry 16. STARZ has a smaller library of content than most streaming services, however, it does come with a plethora of original content from its history as a premium cable network. Lions Gate has also ventured into gaming by licensing out its content to video game studios.

ECONOMIC OUTLOOK

Consumer Spending

Consumer spending, also known as personal consumption expenditures (PCE) tracks the amount of money U.S. citizens spend on goods and services. PCE is very important to the economy as it is a direct reflection of how much companies will be earning during a given time period. It is especially relevant to streaming industry, as elevated consumption could directly tie into the number of subscribers earned. As seen from the graph below, PCE has risen significantly since 2020. This also happens to coincide with the growth of the streaming industry as a whole. We project consumption to continue to rise over the next 2 quarters but start to tail off thereafter. We believe that

when spending peaks as high as it is now, there will be some pull back in spending going forward. People will be less likely to spend on discretionary items, especially products or services they have never used before.

Source: Bloomberg

Unemployment

The COVID-19 pandemic raised unemployment levels to spectacular highs. Since then, unemployment has been going back down to normal levels. Unemployment has a huge impact on the streaming industry for obvious reasons. If people are not employed, they likely are not making purchases on things like entertainment. It should be noted however that the height of the pandemic saw a major increase in subscriptions, around the same time unemployment hit highs. We believe that the two are not correlated and that unemployed people are not driving the demand for subscriptions. We suspect unemployment will continue to fall as government stimulus ends and the effects of the pandemic continue to subside. We target unemployment to be around 4% over the next 6 months.

Source: Bloomberg

0

1

2

3

4

5

6

2/1/2012… 9/1/2012… 4/1/2013… 11/1/2013… 6/1/2014… 1/1/2015… 8/1/2015… 3/1/2016… 10/1/2016… 5/1/2017… 12/1/2017… 7/1/2018… 2/1/2019… 9/1/2019… 4/1/2020… 11/1/2020… 6/1/2021…

US Personal Consumption Expenditures

(%YoY)

0

2

4

6

8

10

12

14

3/1/2012 10/1/2012 5/1/2013 12/1/2013 7/1/2014 2/1/2015 9/1/2015 4/1/2016 11/1/2016 6/1/2017 1/1/2018 8/1/2018 3/1/2019 10/1/2019 5/1/2020 12/1/2020 7/1/

US Unemployment %

Page 11

Consumer Confidence Index

The consumer confidence index (CCI) measures the amount of pessimism or optimism in the economy. A CCI number below 100 means that there is general pessimism in the economy. People are less likely to make big purchases when the CCI is low. COVID-19 played a huge role in lowering the CCI in 2019, and since then it has been slow to recover. Although getting a streaming service isn’t necessarily a “large purchase”, consumer confidence still influences spending and could deter more vulnerable people from buying one. Spending during the pandemic increased, despite low consumer confidence. We attribute this to people being stuck at home with nothing to do and making purchases online. Moving forward, CCI will likely play a larger role in big purchases, especially with the threat of rising borrowing costs. We project CCI to remain at current levels for the next 2 years as the uncertainty of the pandemic remains and the realities around inflation continue to scare the public.

Source: OECD

GDP

GDP hit lows not seen in a decade during the height of the COVID-19 pandemic. It was able to rebound significantly mid-2020 and has since returned to levels slightly elevated from pre-pandemic. GDP is a broad indication of how healthy an economy is. Periods of low GDP often correspond to inefficient productivity in the economy. As a result, many industries, including the streaming industry, are tied to it. We project GDP to grow around 2.5% over the next 6 months and 5% over the next 2 years.

Source: FRED Database

VALUATION

Revenue Decomposition

We broke revenue down into two main drivers, the first being the number of subscribers each geographic segment has, and the second being the revenue per subscriber per month that Netflix generated in those regions. We believe that this is the most accurate way to represent their profits and subsequently base forecasts off.

Subscribers

As mentioned above, subscriber count was broken down into four geographies. By looking at historical growth rates for each of those geographies, it is visible that growth has been trending lower the last few years despite stronger numbers in 2020. We believe that as Netflix invests further into gaming and original content, they will reach almost 75 million subscribers in the UCAN region by 2025. We believe that the potential Netflix has in gaming and original content is underestimated and that there is likely to be a revolution in the way people consume entertainment from the cord-cutting trend. We project around 345 million users by 2031, implying a CAGR of 10.3%. We believe the amount of people who will have access to quality wireless internet by 2031 has been greatly underestimated. With technologies like Starlink which allow highspeed satellite internet already in use, we believe access to Netflix will increase dramatically and allow regions that were previously excluded to join in.

94

95

96

97

98

99

100

101

102

2018-01 2018-04 2018-07 2018-10 2019-01 2019-04 2019-07 2019-10 2020-01 2020-04 2020-07 2020-10 2021-01 2021-04 2021-07 2021-

Consumer Confidence Index

2016-10-01 2017-03-01 2017-08-01 2018-01-01 2018-06-01 2018-11-01 2019-04-01 2019-09-01 2020-02-01 2020-07-01 2020-12-01 2021-05-01 2021-10-

US GDP

Page 13

Contingent Liabilities

While we did not account for any potential legal liabilities, we did consider content liabilities not reflected on the balance sheet. Content liabilities are related to the acquisition of licensing and production of content. Netflix stated in their most recent 10K that around $15.8 billion worth of these liabilities are not reflected on the balance sheet. We accounted for these liabilities in our DCF model, which will be explained in further detail.

Valuation Models

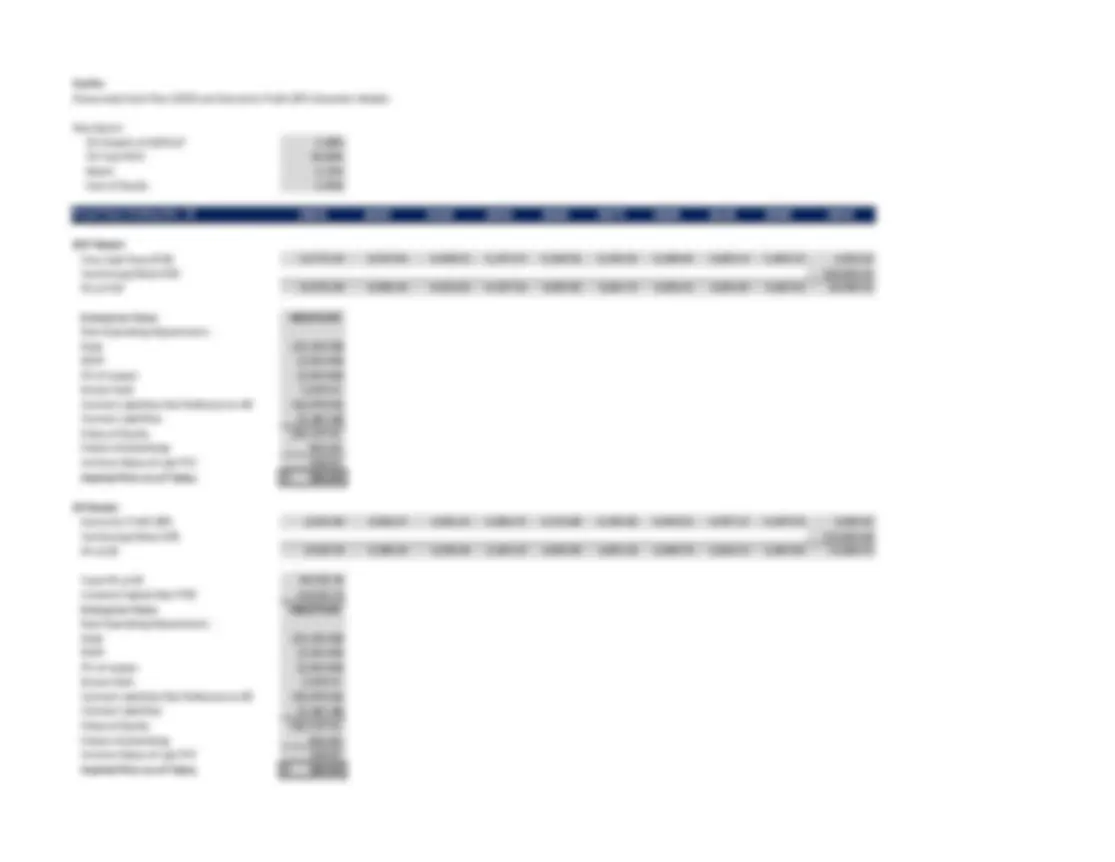

DCF

Our discounted cash flow model yielded a price of about $235. We assumed a continuing growth rate of 2% which we believe is very conservative and is a proxy for inflation growth. Using that growth rate, we calculated a continuing value of $164 billion. This number, along with free cash flows in our projection period, were discounted using the WACC. We estimated Netflix’s WACC to be 6.17%. We calculated this number by using a cost of equity implied by the CAPM. We used a beta of 0.94 and calculated this by levering the betas of comparable firms and then re- levering the average with Netflix’s inputs. Our cost of debt was acquired from the yield on one of Netflix’s 10-year bonds. We then summed the discounted cashflows, subtracted all claims on the firm and divided that number by the outstanding shares to arrive at our share price.

We place most emphasis on our DCF model because we were able to more accurately reflect our growth assumptions like subscriber count and revenue.

DDM

Our dividend discount model produced a share price of $195. We decided that this model did not best represent Netflix, as they do not pay dividends and will likely not in the future.

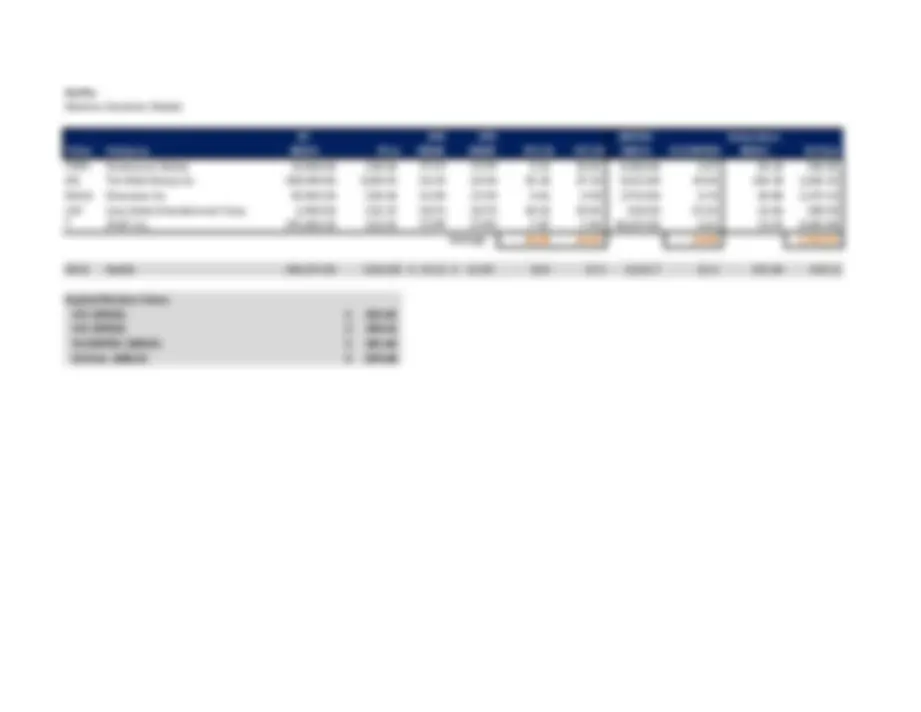

Relative Valuation

We used four different metrics when assessing the relative valuation of Netflix being forward P/E in 2022 and 2023, EV/EBITDA in 2021, and EV/Subscriber count in 2021. The comparable companies we chose were Paramount, Disney, Discovery, Lions Gate, and AT&T. We chose these comps because of the industries they operate in and the similarities in end users. Our forward P/E ratios resulted in

prices of $223 and $190 in 2022 and 2023 respectively. EV/EBITDA gave us a price of $181 and EV/Subscribers gave a price of $870. We took this valuation method less seriously compared to our DC. While Netflix and their comps operate in the same industry, only one company is on par with Netflix when it comes to subscriber count, and that’s Disney. Therefore, our EV/Sub ratio resulted in the highest price of them all.

Sensitivity Analysis

After performing a sensitivity analysis on our DCF, we found that there were several variables that our model was most effected by. The most significant of these was the estimated beta. We found that increasing and decreasing our beta by .05 resulted in a price range of $253-$220. If the beta were to increase more or less by .05, it could significantly alter the implied price, even changing the investment recommendation. This is why we opted to go through the process of un-levering and re- levering beta to get the most accurate depiction of Netflix.

We were surprised to find how little the pre-tax cost of debt played into the share price. A 10-basis point increase/decrease in the number resulted in prices of $ and $236 respectively. We believe this phenomenon to be caused by the low level of debt in the capital structure. Another notable result of our analysis was the model’s sensitivity to the risk-free rate. A 10-basis point difference in our assumed rate resulted in a price range of $229-$242. Provided ongoing geopolitical events in Eastern Europe persist, the risk-free rate (10-year treasury yield) could climb higher, resulting in a lower valuation. However, we believe that the fed is likely to further intervene in order to raise rates due to inflation at all-time highs, raising our valuation significantly.

Valuation Summary

We place most emphasis on our DCF model as it better reflects our assumptions about key drivers. We believe that our relative valuation provides some insight into where Netflix stands compared to its peers, despite not providing the best assessment of price. While metrics like EPS are above consensus estimates, we believe that this is justified through the number of new subscribers that will be brought on through Netflix’s original content and gaming investments.

Page 14

The price of Netflix dropped significantly after the announcement of lower subscriber addition guidance. We projected subscriber growth in 2022 to be slightly above guidance at a 1.25 million loss.

In conclusion, we believe that although Netflix has taken a major hit recently, the portfolio should continue to hold. Netflix still is a leader in the streaming industry, which we believe isn’t going anywhere anytime soon. Netflix’s multiples are trading closer to their peers than ever before, which we see as a sign that its fairly valued. At this point, exiting the position would ignore the possibilities that Netflix has in gaming, ad-based subscriptions, and fees for multiple users.

KEYS TO MONITOR

Catalysts for Growth

- Continued growth in underrepresented, highly populated regions, especially in APAC

- Additions of popular international content to compete with services native to each country

- Raising revenue per subscriber to maximum levels before deterring new customers

Risks to Thesis

- Spending on original content outpaces the addition of new subscriber revenue, reducing margins

- Continued inflation worldwide deterring discretionary spending

- Unsuccessful entry into gaming arena reducing the value associated with past acquisitions

REFERENCES

- Ibisworld Industry Report

- Forbes

- USNews

- Techjury

- Wall Street Journal

- Statista (SVOD monthly subscriptions)

- Statista (SVOD outlook)

- Variety

- Fiercevideo

- Netflix

- KoreaHerald

- Statista (crunchyroll users)

- Statista (USA SVOD Usage)

- OECD

- Statista (Pay TV Penetration Rate)

- Yahoo Finance Sustainability

- Yahoo Finance

- Sustainalyitcs

- Bloomberg

- Netflix 10k

- Alphabet 10k

- Discovery Communications 10k

- The Walt Disney Company 10k

- AT&T 10k

- Factset

DISCLAIMER

Henry Fund reports are created by graduate students in the Applied Securities Management program at the University of Iowa’s Tippie College of Business. These reports provide potential employers and other interested parties an example of the analytical skills, investment knowledge, and communication abilities of our students. Henry Fund analysts are not registered investment advisors, brokers or licensed financial professionals. The investment opinion contained in this report does not represent an offer or solicitation to buy or sell any of the aforementioned securities. Unless otherwise noted, facts and figures included in this report are from publicly available sources. This report is not a complete compilation of data, and its accuracy is not guaranteed. From time to time, the University of Iowa, its faculty, staff, students, or the Henry Fund may hold an investment position in the companies mentioned in this report.

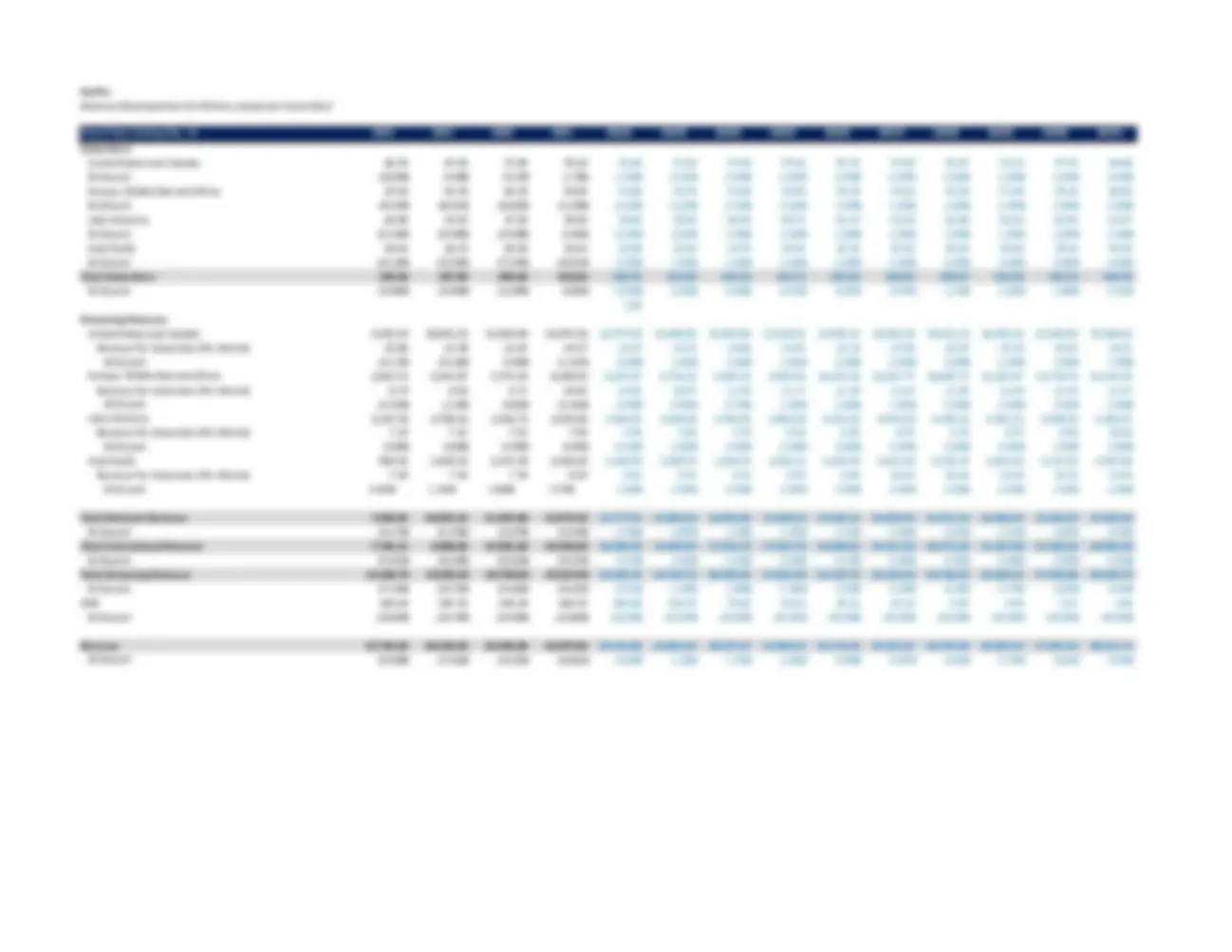

Netflix Income Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Revenue 15,794.34 20,156.45 24,996.06 29,697.84 29,512.02 29,862.49 30,375.97 31,094.32 32,174.93 33,451.07 34,795.50 36,095.25 37,401.34 38,911. Cost Of Subscription Revenue (^) 2,352.29 3,120.39 4,353.70 4,893.90 4,922.74 4,981.20 5,066.85 5,186.68 5,366.93 5,579.79 5,804.05 6,020.86 6,238.72 6,490. Amortization of Content Assets 7,532.09 9,216.25 10,806.91 12,230.40 8,943.29 9,049.50 9,205.10 9,422.79 9,750.26 10,136.98 10,544.39 10,938.27 11,334.07 11,791. Depreciation 83.16 103.58 115.71 208.40 416.73 426.71 435.22 443.51 452.63 464.04 477.97 493.94 511.11 529. Sales/Marketing/Advertising Expenses 2,369.47 2,652.46 2,228.36 2,545.10 3,398.55 3,438.91 3,498.04 3,580.76 3,705.21 3,852.16 4,006.99 4,156.66 4,307.07 4,481. Technology/Software Development Costs 1,221.81 1,545.15 1,829.60 2,273.94 2,508.07 2,537.86 2,581.50 2,642.54 2,734.38 2,842.83 2,957.09 3,067.55 3,178.55 3,306. General and Administrative Expenses 630.29 914.37 1,076.49 1,351.60 1,465.55 1,482.96 1,508.46 1,544.13 1,597.79 1,661.16 1,727.93 1,792.47 1,857.33 1,932. Operating Income 1,605.23 2,604.25 4,585.29 6,194.50 7,857.08 7,945.36 8,080.80 8,273.90 8,567.74 8,914.09 9,277.08 9,625.50 9,974.50 10,379.

Interest Expense (420.49) (626.02) (767.50) (765.60) (737.35) (686.99) (900.14) (1,166.64) (1,328.93) (1,029.74) (1,271.64) (1,461.86) (1,520.09) (1,576.76)

Interest and other Income (Expense) 41.73 84.00 (618.44) 411.20 137.88 553.87 791.18 1,055.39 1,271.38 1,269.85 1,535.88 1,783.11 1,974.46 2,173. Income Before Income Taxes 1,226.46 2,062.23 3,199.35 5,840.10 7,257.61 7,812.24 7,971.84 8,162.65 8,510.19 9,154.21 9,541.33 9,946.75 10,428.87 10,976.

Income Tax Expense (Benefit) 15.22 195.32 437.95 723.90 1,874.88 2,018.16 2,059.39 2,108.68 2,198.47 2,364.84 2,464.84 2,569.58 2,694.13 2,835.

Net Income 1,211.24 1,866.92 2,761.40 5,116.20 5,382.72 5,794.08 5,912.45 6,053.96 6,311.72 6,789.37 7,076.48 7,377.17 7,734.75 8,140.

Earnings Per Share:

Basic 2.78 4.26 6.26 11.54 12.11 12.99 13.21 13.48 14.00 14.99 15.56 16.15 16.86 17.

Weighted-Average Common Shares Outstanding Basic 435.37 437.80 440.92 443.20 444.51 445.95 447.50 449.16 450.93 452.79 454.74 456.78 458.90 461.

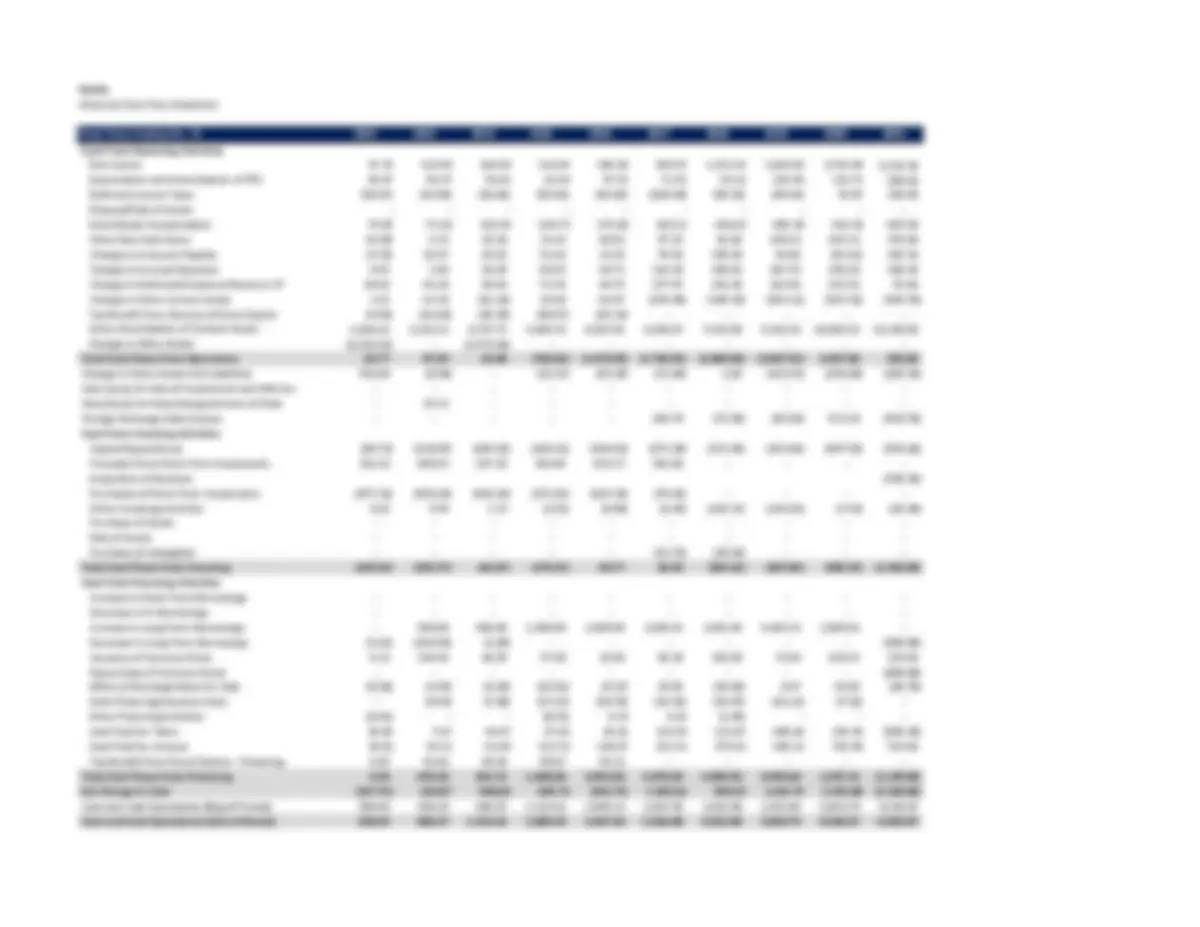

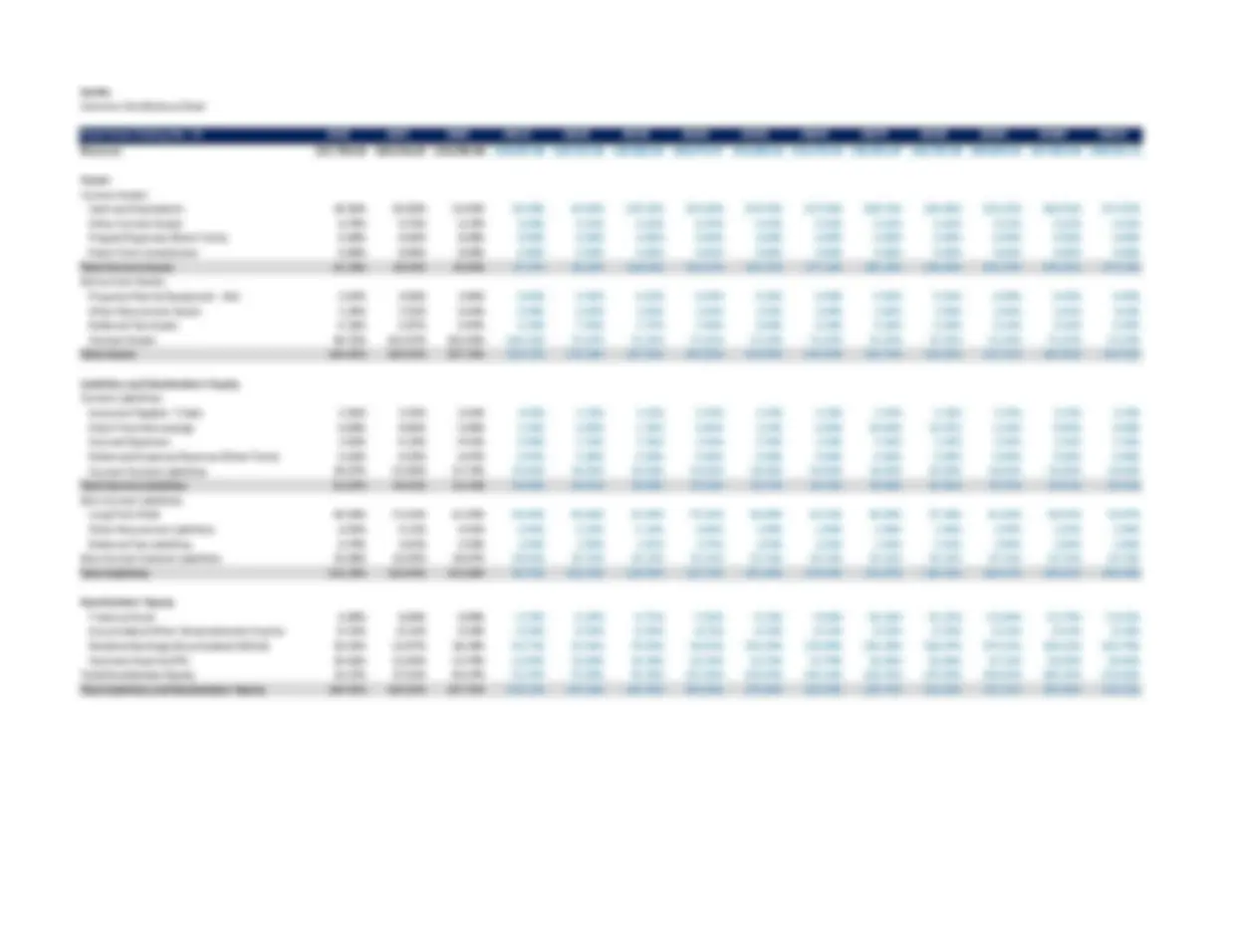

Netflix Balance Sheet

Fiscal Years Ending Dec. 31 (^) 2018 2019 2020 2021 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Assets Current Assets:

Cash and Equivalents 3,794.48 5,018.44 8,205.55 6,027.80 24,214.83 34,589.65 46,140.67 55,583.53 55,517.02 67,147.65 77,956.15 86,322.00 95,007.77 106,449. Other Current Assets 748.47 1,160.07 1,556.03 2,042.00 1,361.54 1,377.71 1,401.39 1,434.54 1,484.39 1,543.26 1,605.29 1,665.25 1,725.51 1,795. Prepaid Expenses (Short-Term) - - - - - - - - - - - - - - Short-Term Investments - - - - - - - - - - - - - - Total Current Assets (^) 9,694.14 6,178.50 9,761.58 8,069.80 25,576.37 35,967.36 47,542.07 57,018.07 57,001.41 68,690.92 79,561.44 87,987.25 96,733.28 108,244.

Noncurrent Assets:

Property Plant & Equipment - Net 418.28 565.22 960.18 1,323.50 1,355.19 1,382.24 1,408.56 1,437.52 1,473.77 1,518.00 1,568.74 1,623.24 1,680.43 1,742. Other Noncurrent Assets 211.61 1,524.34 1,706.19 2,670.45 1,186.28 1,139.26 1,107.06 1,094.49 1,119.67 1,163.19 1,210.21 1,247.49 1,280.80 1,332. Deferred Tax Assets 689.42 1203.077 1,468.46 1,601.36 2,231.27 2,318.88 2,410.54 2,506.30 2,606.25 2,710.51 2,819.18 2,932.41 3,050.35 3,173. Content Assets 14,960.95 24,504.57 25,383.95 30,919.60 21,032.58 21,282.35 21,648.30 22,160.25 22,930.38 23,839.85 24,798.00 25,724.31 26,655.13 27,731. Total Assets 25,974.40 33,975.71 39,280.36 44,584.70 51,381.70 62,090.08 74,116.53 84,216.62 85,131.48 97,922.47 109,957.56 119,514.70 129,399.99 142,224.

Liabilities and Stockholders' Equity Current Liabilities:

Accounts Payable - Trade 562.99 674.35 656.18 837.50 983.90 995.59 1,012.71 1,036.65 1,072.68 1,115.23 1,160.05 1,203.38 1,246.93 1,297. Short-Term Borrowings - - 499.88 699.80 - 400.00 1,835.00 1,000.00 1,480.00 3,500.00 4,318.00 2,252.00 - - Accrued Expenses 477.42 843.04 1,102.20 1,449.40 990.71 1,002.47 1,019.71 1,043.83 1,080.10 1,122.94 1,168.07 1,211.71 1,255.55 1,306. Deferred/Unearned Revenue (Short-Term) 760.90 924.75 1,117.99 1,209.30 1,416.37 1,433.19 1,457.83 1,492.31 1,544.17 1,605.42 1,669.94 1,732.32 1,795.00 1,867. Current Content Liabilities 4,686.02 4,413.56 4,429.54 4,293.00 5,319.35 5,382.52 5,475.07 5,604.55 5,799.32 6,029.34 6,271.66 6,505.94 6,741.35 7,013.

Total Current Liabilities 6,487.32 6,855.70 7,805.79 8,489.00 8,710.33 9,213.77 10,800.32 10,177.34 10,976.28 13,372.92 14,587.73 12,905.34 11,038.83 11,484.

Non Current Liabilities: Long Term Debt 10,360.06 14,759.26 15,809.10 14,693.10 14,341.56 18,391.16 22,519.66 26,742.52 20,016.78 23,046.64 26,199.56 29,481.34 32,916.37 36,525. Other Noncurrent Liabilities 4.24 1,034.19 1,352.63 1,324.35 1,244.25 1,230.12 1,226.78 1,237.46 1,274.39 1,324.51 1,377.87 1,425.60 1,471.58 1,531. Deferred Tax Liabilities 125.00 410.09 629.52 1,134.85 1,055.32 1,096.76 1,140.11 1,185.40 1,232.68 1,281.99 1,333.38 1,386.94 1,442.72 1,500. Non-Current Content Liabilities 3,759.03 3,334.32 2,618.08 3,094.10 4,517.90 4,571.55 4,650.15 4,760.12 4,925.55 5,120.91 5,326.72 5,525.70 5,725.64 5,956.

Total Liabilities 20,735.64 26,393.56 28,215.12 28,735.40 29,869.36 34,503.35 40,337.03 44,102.84 38,425.67 44,146.97 48,825.27 50,724.91 52,595.14 56,998.

Stockholders' Equity

Treasury Stock - - - (824.20) (1,264.20) (1,704.20) (2,144.20) (2,584.20) (3,024.20) (3,464.20) (3,904.20) (4,344.20) (4,784.20) (5,224.20) Accumulated Other Comprehensive Income (19.58) (23.52) 44.40 (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) (40.50) Retained Earnings (Accumulated Deficit) 2,942.36 4,811.75 7,573.14 12,689.40 18,072.12 23,866.20 29,778.65 35,832.61 42,144.34 48,933.70 56,010.19 63,387.36 71,122.11 79,262. Common Stock & APIC 2,315.99 2,793.93 3,447.70 4,024.60 4,744.92 5,465.23 6,185.55 6,905.86 7,626.18 8,346.49 9,066.81 9,787.13 10,507.44 11,227. Total Stockholders Equity 5,238.77 7,582.16 11,065.24 15,849.30 21,512.34 27,586.73 33,779.50 40,113.78 46,705.81 53,775.50 61,132.30 68,789.79 76,804.85 85,225.

Total Liabilities and Stockholders' Equity 25,974.40 33,975.71 39,280.36 44,584.70 51,381.70 62,090.08 74,116.53 84,216.62 85,131.48 97,922.47 109,957.56 119,514.70 129,399.99 142,224.

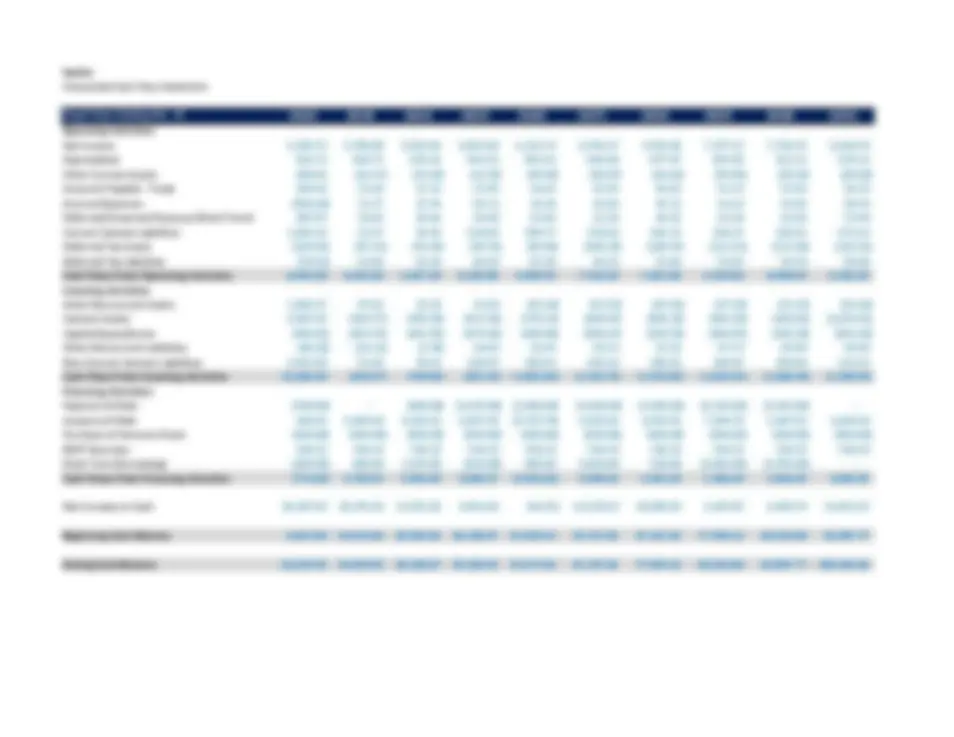

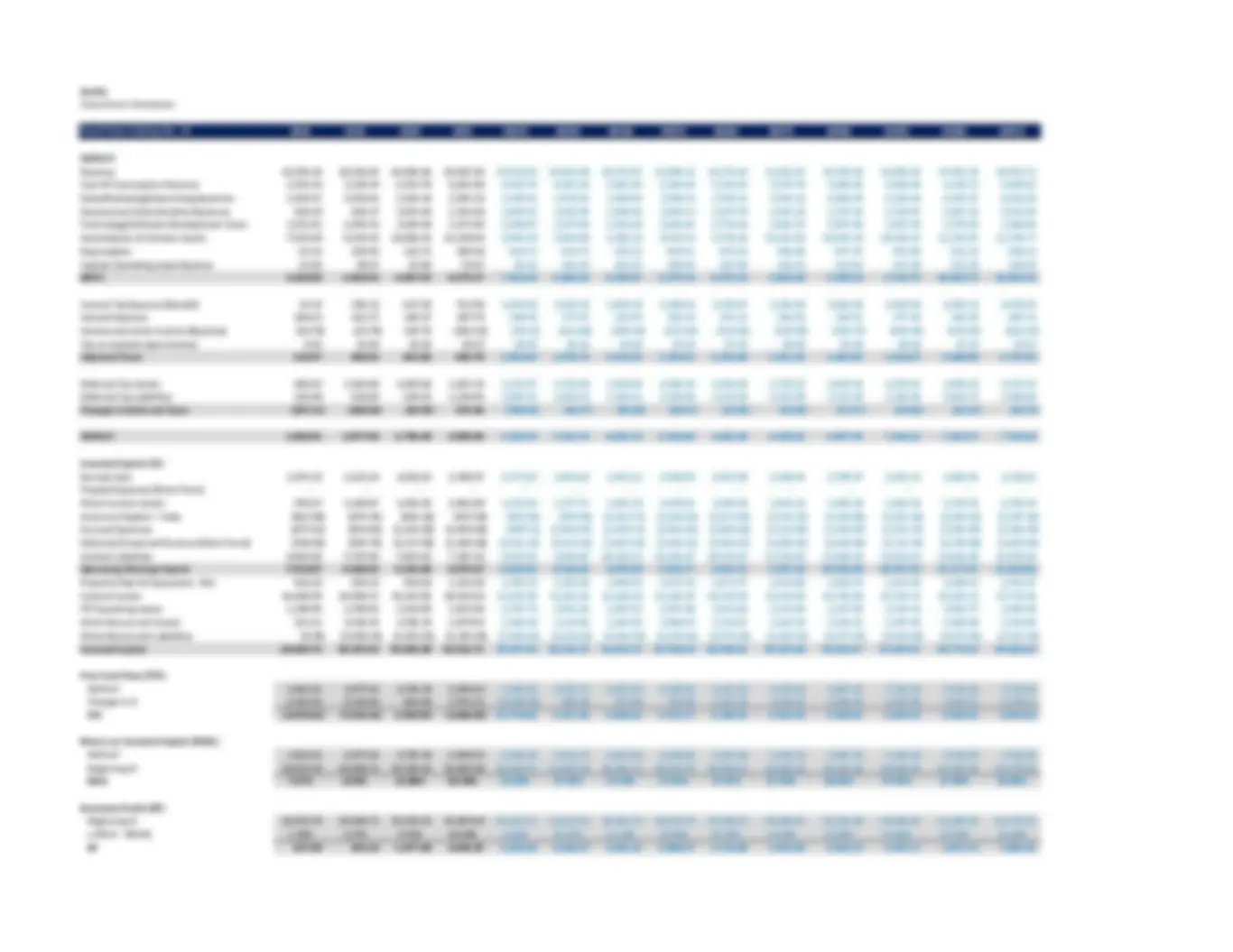

Netflix Forecasted Cash Flow Statement

Fiscal Years Ending Dec. 31 (^) 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Operating Activities:

Net Income 5,382.72 5,794.08 5,912.45 6,053.96 6,311.72 6,789.37 7,076.48 7,377.17 7,734.75 8,140. Depreciation 416.73 426.71 435.22 443.51 452.63 464.04 477.97 493.94 511.11 529.

Other Current Assets 680.46 (16.17) (23.69) (33.14) (49.85) (58.87) (62.03) (59.96) (60.26) (69.68) Accounts Payable - Trade 146.40 11.68 17.12 23.95 36.03 42.55 44.82 43.33 43.54 50.

Accrued Expenses (458.69) 11.77 17.24 24.11 36.28 42.84 45.13 43.63 43.85 50. Deferred/Unearned Revenue (Short-Term) 207.07 16.82 24.64 34.48 51.86 61.25 64.52 62.38 62.68 72.

Current Content Liabilities 1,026.35 63.17 92.55 129.48 194.77 230.02 242.33 234.27 235.41 272. Deferred Tax Assets (629.92) (87.61) (91.65) (95.76) (99.96) (104.25) (108.67) (113.23) (117.94) (122.81)

Deferred Tax Liabilities (79.53) 41.44 43.35 45.29 47.28 49.31 51.40 53.55 55.78 58. Cash Flows From Operating Activities 6,691.60 6,261.88 6,427.23 6,625.88 6,980.76 7,516.24 7,831.96 8,135.09 8,508.93 8,981.

Investing Activities: Other Noncurrent Assets 1,484.17 47.02 32.19 12.58 (25.18) (43.53) (47.01) (37.28) (33.31) (52.10) Content Assets 9,887.02 (249.77) (365.94) (511.95) (770.13) (909.47) (958.15) (926.30) (930.82) (1,076.41)

Capital Expenditures (448.42) (453.75) (461.55) (472.46) (488.88) (508.27) (528.70) (548.45) (568.30) (591.25) Other Noncurrent Liabilities (80.10) (14.13) (3.34) 10.68 36.93 50.13 53.36 47.72 45.99 59.

Non-Current Content Liabilities 1,423.80 53.65 78.61 109.97 165.43 195.36 205.81 198.97 199.94 231. Cash Flows From Investing Activities 12,266.46 (616.97) (720.03) (851.19) (1,081.84) (1,215.79) (1,274.69) (1,265.34) (1,286.50) (1,428.93)

Financing Activities: Payment of Debt (700.00) - (400.00) (1,835.00) (1,000.00) (1,480.00) (3,500.00) (4,318.00) (2,252.00) -

Issuance of Debt 348.46 4,049.60 4,528.51 6,057.85 (5,725.74) 4,509.86 6,652.91 7,599.78 5,687.03 3,609. Purchase of Common Stock (440.00) (440.00) (440.00) (440.00) (440.00) (440.00) (440.00) (440.00) (440.00) (440.00)

ESOP Exercises 720.32 720.32 720.32 720.32 720.32 720.32 720.32 720.32 720.32 720. Short Term Borrowings (699.80) 400.00 1,435.00 (835.00) 480.00 2,020.00 818.00 (2,066.00) (2,252.00) -

Cash Flows From Financing Activities (771.02) 4,729.91 5,843.83 3,668.17 (5,965.42) 5,330.18 4,251.23 1,496.10 1,463.34 3,889.

Net Increase in Cash 18,187.03 10,374.82 11,551.02 9,442.86 (66.51) 11,630.63 10,808.49 8,365.85 8,685.78 11,441.

Beginning Cash Balance 6,027.80 24,214.83 34,589.65 46,140.67 55,583.53 55,517.02 67,147.65 77,956.15 86,322.00 95,007.

Ending Cash Balance 24,214.83 34,589.65 46,140.67 55,583.53 55,517.02 67,147.65 77,956.15 86,322.00 95,007.77 106,449.

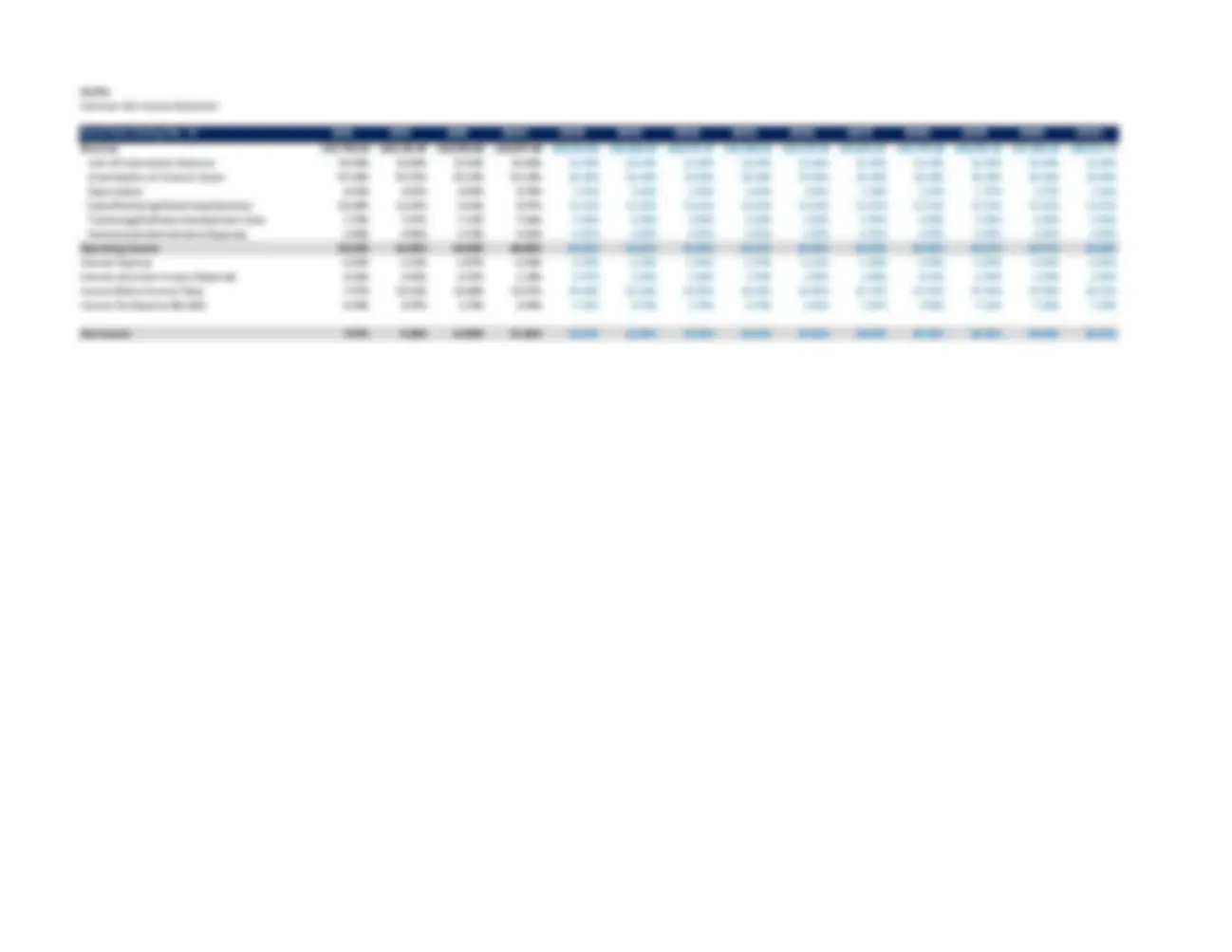

Netflix

Common Size Income Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E

Revenue $15,794.34 $20,156.45 $24,996.06 $29,697.84 $29,512.02 $29,862.49 $30,375.97 $31,094.32 $32,174.93 $33,451.07 $34,795.50 $36,095.25 $37,401.34 $38,911.

Cost Of Subscription Revenue 14.89% 15.48% 17.42% 16.48% 16.68% 16.68% 16.68% 16.68% 16.68% 16.68% 16.68% 16.68% 16.68% 16.68% Amoritization of Content Assets 47.69% 45.72% 43.23% 41.18% 30.30% 30.30% 30.30% 30.30% 30.30% 30.30% 30.30% 30.30% 30.30% 30.30% Depreciation 0.53% 0.51% 0.46% 0.70% 1.41% 1.43% 1.43% 1.43% 1.41% 1.39% 1.37% 1.37% 1.37% 1.36% Sales/Marketing/Advertising Expenses 15.00% 13.16% 8.91% 8.57% 11.52% 11.52% 11.52% 11.52% 11.52% 11.52% 11.52% 11.52% 11.52% 11.52% Technology/Software Development Costs 7.74% 7.67% 7.32% 7.66% 8.50% 8.50% 8.50% 8.50% 8.50% 8.50% 8.50% 8.50% 8.50% 8.50% General and Administrative Expenses 3.99% 4.54% 4.31% 4.55% 4.97% 4.97% 4.97% 4.97% 4.97% 4.97% 4.97% 4.97% 4.97% 4.97%

Operating Income 10.16% 12.92% 18.34% 20.86% 26.62% 26.61% 26.60% 26.61% 26.63% 26.65% 26.66% 26.67% 26.67% 26.68%

Interest Expense -2.66% -3.11% -3.07% -2.58% -2.50% -2.30% -2.96% -3.75% -4.13% -3.08% -3.65% -4.05% -4.06% -4.05%

Interest and other Income (Expense) 0.26% 0.42% -2.47% 1.38% 0.47% 1.85% 2.60% 3.39% 3.95% 3.80% 4.41% 4.94% 5.28% 5.58%

Income Before Income Taxes 7.77% 10.23% 12.80% 19.67% 24.59% 26.16% 26.24% 26.25% 26.45% 27.37% 27.42% 27.56% 27.88% 28.21%

Income Tax Expense (Benefit) 0.10% 0.97% 1.75% 2.44% 6.35% 6.76% 6.78% 6.78% 6.83% 7.07% 7.08% 7.12% 7.20% 7.29%

Net Income 7.67% 9.26% 11.05% 17.23% 18.24% 19.40% 19.46% 19.47% 19.62% 20.30% 20.34% 20.44% 20.68% 20.92%