1. Interest receivable is computed as: Face amount x Stated interest rate or Nominal rate

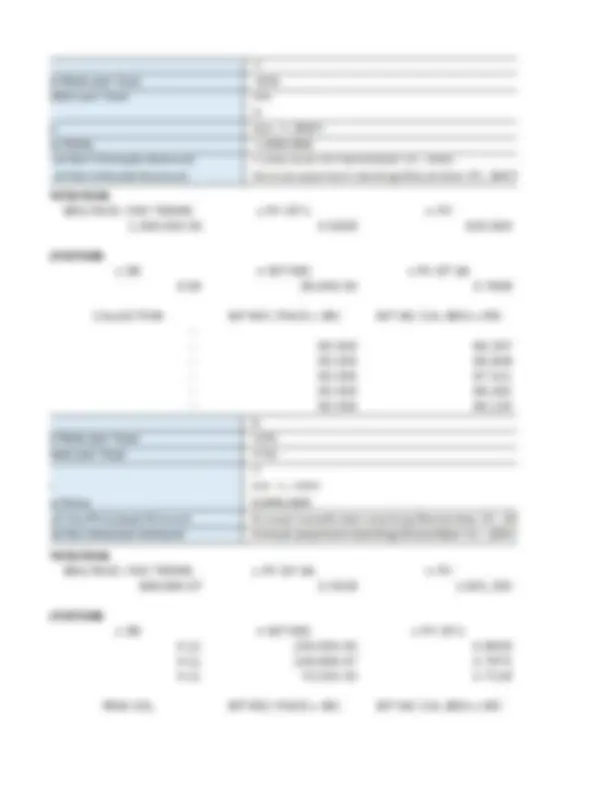

2. Jan 1, 20x1 Crybaby Co. received a noninterest bearing note with face amount of P2M

and appropriately recognized it at P1,241,843. The note matures in lump sum

on Dec. 31, 20x5. The effective interest rate is 10%. The unamortized discount

on Dec. 31, 20x2 is P497,370.

Jan 1, 20x1 - recognized at 1,241,843, face amount is 2M

Find the unamortized discount on Dec. 31, 20x2

Face amount - carrying amount on 20x2

recognized amount on Jan 1, 20x1 = 1,241,843

Dec 31, 20x1 1,241,843.00 +

Dec 31, 20x2 1,366,027.30 +

Dec 31, 20x3 1,502,630.03 +

Dec 31, 20x4 1,652,893.03 +

Dec 31, 20x5 1,818,182.34 +

Face amount 2,000,000.00

Dec 31, 20x2 (1,502,630.03)

Discount 20x2 497,369.97

3. Raining Co. receives a 3 year, noninterest bearing note of 1,000,000. Raining Co.

determines that the effective interest rate on the transaction is 10%

The initial carrying amount of the note receivable is computed as 1,000,000 x PV of 1

@10%, n=3.

As noninterest bearning note, meansno periodic interest payments

Face amount 3,000,000.00

PV of 1 @10%, n=3 0.75 lumpsum

Initial Carrying Amount 2,253,944.40

Unearned Interest 746,055.60

4. Wet Co. receives a noninterest-bearing note of 3,000,000. The note is collectible in 3 equal

annual installments of 1,000,000 due at the end of each year. Wet Co. determines that the effective

interest rate on the transaction is 10%. The initial carrying amount of the note receivable is computed

as 1,000,000 x PV of 1 @10%, n=3

Face amount 3,000,000.00

Per year payment 1,000,000.00

PV of OA @10%, n=3 2.45

Carrying Amount 2,448,685.20

Unearned Interest 551,314.80

5. Fold Co, received a 2 year, non-interest bearing note of 1.2M in exchange for the sale of commodity

If the customer had paid in cash at the sale date, the purchase price would have been 800K. At initial

recognition, Fold Co. records unearned interest of 400K.

6. 2 yr noninterest bearning note of 500K from the sale of equipment with cash price of 400k.

The note requires lump sum payment at maturity date. Bind Co. determined that the

effective interest rate on the transaction is 10%. The interest income in Year 1 is 50K.

Interest income = Present value x effective rate x time

Present value (cash price) 100,000.00