Download Exercise on Activity-Based Costing: Inventory Management and Travel Expenses and more Exams Cost Accounting in PDF only on Docsity!

7-

Quiz

Exercise 7-1 (10 minutes)

a. Various individuals manage the parts inventories. Product-level b. A clerk in the factory issues purchase orders for a job. Batch-level c. The personnel department trains new production workers.

Organization- sustaining d. The factory’s general manager meets with other department heads, such as marketing, to coordinate plans.

Organization- sustaining e. Direct labor workers assemble products. Unit-level f. Engineers design new products. Product-level g. The materials storekeeper issues raw materials to be used in jobs. Batch-level h. The maintenance department performs periodic preventative maintenance on general-use equipment.

Organization- sustaining Some of these classifications are debatable and may depend on the specific circumstances found in particular companies.

7-

Exercise 7-2 (15 minutes)

Travel

Pickup and Delivery

Customer Service Other Totals Driver and guard wages ......................... $336,000 $378,000 $ 84,000 $ 42,000 $ 840, Vehicle operating expense ..................... 202,500 13,500 0 54,000 270, Vehicle depreciation .............................. 105,000 15,000 0 30,000 150, Customer representative salaries and expenses ............................................ 0 0 153,000 27,000 180, Office expenses..................................... 0 10,000 14,000 16,000 40, Administrative expenses ........................ 0 17,000 187,000 136,000 340, Total cost ............................................. $643,500 $433,500 $438,000 $305,000 $1,820,

Each entry in the table is derived by multiplying the total cost for the cost category by the percentage taken from the table below that shows the distribution of resource consumption:

Travel

Pickup and Delivery

Customer Service Other Totals Driver and guard wages ......................... 40% 45% 10% 5% 100% Vehicle operating expense ..................... 75% 5% 0% 20% 100% Vehicle depreciation .............................. 70% 10% 0% 20% 100% Customer representative salaries and expenses ............................................ 0% 0% 85% 15% 100% Office expenses..................................... 0% 25% 35% 40% 100% Administrative expenses ........................ 0% 5% 55% 40% 100%

7-

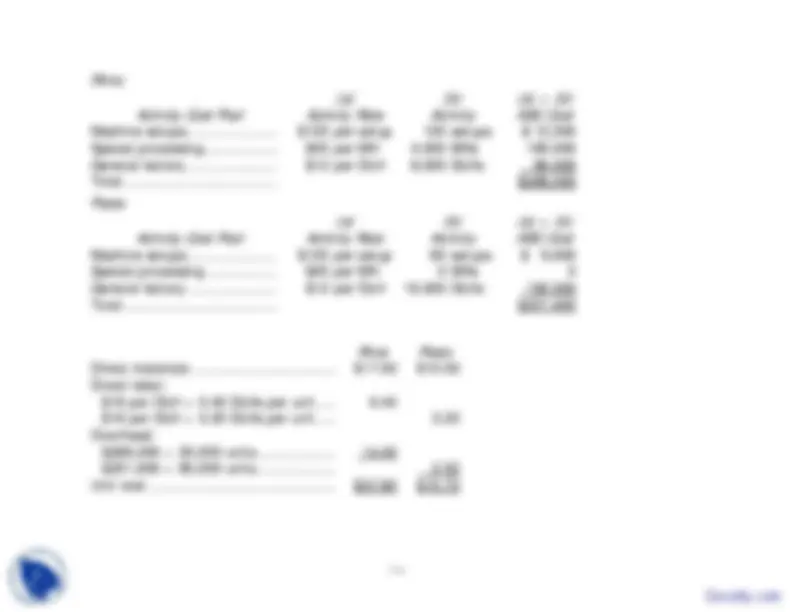

Rims:

Activity Cost Pool

(a) Activity Rate

(b) Activity

(a) × (b) ABC Cost Machine setups ..................... $120 per setup 100 setups $ 12, Special processing ................. $45 per MH 4,000 MHs 180, General factory ..................... $12 per DLH 8,000 DLHs 96, Total .................................... $288,

Posts:

Activity Cost Pool

(a) Activity Rate

(b) Activity

(a) × (b) ABC Cost Machine setups ..................... $120 per setup 80 setups $ 9, Special processing ................. $45 per MH 0 MHs 0 General factory ..................... $12 per DLH 16,000 DLHs 192, Total .................................... $201,

Rims Posts Direct materials .................................. $17.00 $10. Direct labor: $16 per DLH × 0.40 DLHs per unit..... 6. $16 per DLH × 0.20 DLHs per unit..... 3. Overhead: $288,000 ÷ 20,000 units................... 14. $201,600 ÷ 80,000 units................... 2. Unit cost ............................................ $37.80 $15.