1

Monetary Statistics

PART I – FINANCIAL STATISTICS

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

M1. = Currency with the public +. Demand deposits with the banking system + 'Other' deposits with the RBI. M2. = M1 + Savings deposits of post.

Typology: Summaries

1 / 16

This page cannot be seen from the preview

Don't miss anything!

Monetary Statistics

Monetary Statistics

Reserve Money = Currency in circulation + Bankers’ deposits with the RBI

M 1 =^ Currency^ with^ the^ public^ + Demand deposits with the banking system + ‘Other’ deposits with the RBI. M 2 = M 1 + Savings deposits of post office savings banks M 3 = M 1 + Time deposits with the banking system = Net bank credit to the Government + Bank credit to the commercial sector + Net foreign exchange assets of the banking sector + Government’s currency liabilities to the public

M 4 = M 3 + All deposits with post office savings banks (excluding National Savings Certificates). NM 1 = Currency with the public + Demand deposits with the banking system + ‘Other’ deposits with the RBI. NM 2 = NM 1 + Short-term time deposits of residents (including and up to the contractual maturity of one year). NM 3 = NM 2 + Long-term time deposits of residents + Call/Term funding from financial institutions.

Monetary Statistics

Manual on Financial and Banking Statistics

Manual on Financial and Banking Statistics

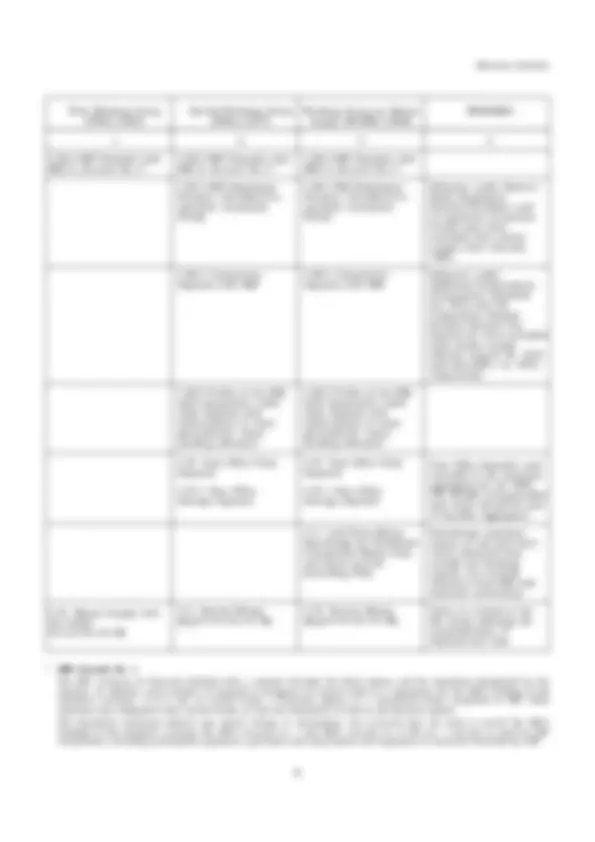

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

C.II.1 Demand Deposits with banks (including inter-bank demand deposits with state co- operative banks)

C.II.2 Time Deposits with banks (including inter- bank time deposits with state co-operative banks)

C.III. ‘Other’ deposits with the RBI (C.III.1-C.III.2)

C.III.1 Other Deposits with the RBI

C.II.1 Demand Deposits with the banking system.

C.II.2 Time Deposits with the banking system.

C.III. ‘Other’ deposits with the RBI (C.III.1- C.III.2-C.III.3-C.III.4- C.III.5)

C.III.1 Other Deposits with the RBI

C.II.1 Demand Deposits with the banking system.

C.II.2 Time Deposits held by Residents with the banking system. (CII.2.1+C.II.2.2+ C.II.2.3)

C.II.2.1 Certificates of Deposit (CDs)

C.II.2.2 Short-term^1 time deposits

C.II.2.2.1 Foreign Currency Repatriable short-term^1 ‘Fixed Deposits held by Non- Residents

C.II.2.3 Long-term 2 time deposits

C.II.2.3.1 Foreign Currency Repatriable long-term^2 Fixed Deposits held by Non- Residents

C.II.3 Savings Accounts

C.II.3.1 Time Liabilities portion of Savings Accounts

C.III. ‘Other’ deposits with the RBI (C.III.1-C.III.2- C.III.3-C.III.4-C.III.5)

C.III.1 Other Deposits with the RBI

(WGMS): Analytics and Methodology Compilation. The WGMS recommended that aggregate deposits should be on residency basis, thereby excluding repatriable foreign currency fixed deposits held by non-residents, e.g. , FCNR(B) deposits, from money supply.

The WGMS recommended a break-up of time deposits into CDs and other time deposits on the basis of maturity structure partitioned at one year.

Monetary Statistics

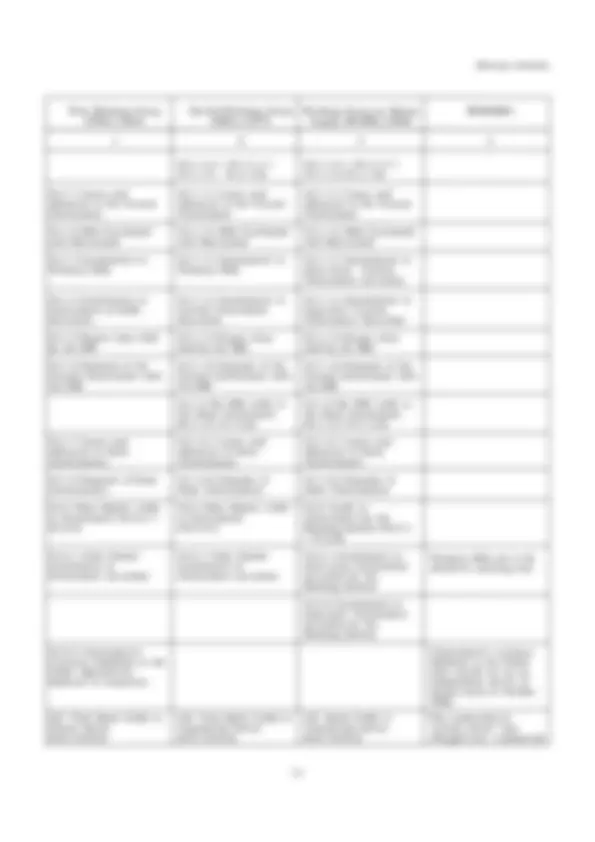

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

C.III.2 IMF Deposits with RBI in Account No.1 *

C.IV. Money Supply with the Public (=C.I+C.II.1+C.III)

C.III.2 IMF Deposits with RBI in Account No.1 *

C.III.3 RBI Employees’ Pension/ Provident/Co- operative Guarantee Funds

C.III.4 Compulsory Deposits with RBI

C.III.5 Profits of the RBI held temporarily under other deposits and subscriptions to state governments’ loans pending allotment

C.IV. Post Office Total Deposits

C.IV.1 Post Office Savings Deposits

C.V. Narrow Money (M 1 )(=C.I+C.II.1+C.III)

C.III.2 IMF Deposits with RBI in Account No.1 *

C.III.3 RBI Employees’ Pension/ Provident/Co- operative Guarantee Funds

C.III.4 Compulsory Deposits with RBI

C.III.5 Profits of the RBI held temporarily under other deposits and subscriptions to state governments’ loans pending allotment

C.IV. Post Office Total Deposits

C.IV.1 Post Office Savings Deposits

C.V. Call/Term Money Borrowings by Scheduled Commercial Banks from non-bank sources (excluding PDs)

C.VI. Narrow Money (M 1 )(=C.I+C.II.1+C.III)

Balances under Reserve Bank Employees’ Pension/Provident and Co-operative Guarantee Funds have been excluded from money supply since January

Balances under Additional Emoluments (Compulsory Deposits) Act 1974 and the Compulsory Deposit Scheme (Income Tax Payers) Act were excluded from money supply effective August 16, 1974 and December 13, 1974, respectively.

Post Office Deposits were included in the monetary aggregates by the SWG. The WGMS recommended that these should be part of liquidity aggregates.

Borrowings represent money at call and short notice obtained from outside the banking system, but exclude refinance from RBI and financial institutions.

There is a break in the M1 series following the reclassification of demand and time

The IMF conducts its financial dealings with a member through the fiscal agency and the depository designated by the member. In addition, each member is required to designate its central bank as a depository for the IMF’s holding of the member’s currency, or if it has no central bank, a monetary agency or a commercial bank acceptable to IMF. Most members have designated their central banks as both the depository as well as the financial agency. The depository maintains without any service charge or commission, two accounts that are used to record the IMF’s holdings of the member’s currency the IMF’s account no. 1 and IMF’s account no. 2 The no. 1 account is used for IMF transactions, including subscription payments, purchases and repurchases and repayment of resources borrowed by IMF.

Monetary Statistics

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

S.I.1.1 Loans and Advances to the Central Government

S.I.1.2 Bills Purchased and Discounted

S.I.1.3 Investments in Treasury Bills

S.I.1.4 Investments in Government of India Securities

S.I.1.5 Rupee coins held by the RBI

S.I.1.6 Deposits of the Central Government with the RBI

S.I.1.7 Loans and Advances to State Governments

S.I.1.8 Deposits of State Governments

S.I.2 Other Banks’ credit to Government (S.I.2.1 + S.I.2.2)

S.I.2.1 Other Banks’ investments in Government securities

S.I.2.2 Government’s Currency Liabilities to the Public adjusted for balances in treasuries

S.II. Total Bank Credit to Private Sector (S.II.1+S.II.2)

S.I.1.1.1 Loans and Advances to the Central Government

S.I.1.1.2 Bills Purchased and Discounted

S.I.1.1.3 Investments in Treasury Bills

S.I.1.1.4 Investments in Central Government Securities

S.I.1.1.5 Rupee coins held by the RBI

S.I.1.1.6 Deposits of the Central Government with the RBI

S.I.1.2 Net RBI credit to the State Government (S.I.1.2.1-S.1.2.2)

S.I.1.2.1 Loans and Advances to State Governments

S.I.1.2.2 Deposits of State Governments

S.I.2 Other Banks’ credit to Government (=S.I.2.1)

S.I.2.1 Other Banks’ investments in Government securities

S.II. Total Bank Credit to Commercial Sector (S.II.1+S.II.2)

S.I.1.1.1 Loans and Advances to the Central Government

S.I.1.1.2 Bills Purchased and Discounted

S.I.1.1.3 Investments in short-term^1 Central Government securities

S.I.1.1.4 Investments in long-term^2 Central Government Securities

S.I.1.1.5 Rupee coins held by the RBI

S.I.1.1.6 Deposits of the Central Government with the RBI

S.I.1.2 Net RBI credit to the State Government (S.I.1.2.1-S.I.1.2.2)

S.I.1.2.1 Loans and Advances to State Governments

S.I.1.2.2 Deposits of State Governments

S.I.2 Credit to Government by the Banking System (S.I.2.

S.I.2.1 Investments in short-term Government securities by the Banking System

S.I.2.2 Investments in long-term^2 Government securities by the Banking System

S.II. Bank Credit to Commercial Sector (S.II.1+S.II.2)

Treasury Bills are to be valued at carrying cost.

Government’s currency liabilities to the Public were carved out as an independent source of money stock in October

The nomenclature “private sector” was changed into “commercial

Manual on Financial and Banking Statistics

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

S.II.1 RBI Credit to Commercial Sector (S.II.1.1+S.II.1.2+S.II.1.3)

S.II.1.1 RBI’s investments in shares/ bonds of financial institutions, ordinary debentures of co- operative sectors, CLMB debentures etc.

S.II.1.2 Loans to financial institutions

S.II.1.3 Internal Bills (under Bills Rediscounting Scheme)

S.II.2 Credit to the Commercial Sector by the Banking System (S.II.2.1 + S.II.2.2+ S.II.2.3 + S.II.2.4)

S.II.2.1 Bank Credit

sector” in 1970, as bank credit included credit given to commercial/ manufacturing enterprises in the public sector too.

On the establishment of National Bank for Agriculture and Rural Development (NABARD) on July 12, 1982, certain assets and liabilities of the RBI were transferred to NABARD, necessitating some reclassification of aggregates on the sources side of money stock since that date. The WGMS recommended the reclassification of the RBI’s refinance to NABARD as credit to commercial sector rather than as claims on banks as had been the practice hitherto.

With the introduction of the Bills Rediscounting Scheme, the commercial banks started discounting the internal bills with the RBI which have been included in the RBI credit to commercial sector since June 1971.

Includes loans, cash credit and overdrafts and internal and foreign bills purchased and

S.II.1 RBI Credit to Private Sector (S.II.1.1+S.II.1.2)

S.II.1.1 RBI’s investments in shares/bonds of financial institutions, ordinary debentures of co- operative sectors, Central Land Mortgage Bank (CLMB) debentures etc.

S.II.1.2 Loans to financial institutions

S.II.2 Other Banks’ net credit to Private Sector (S.II.2.1 + S.II.2.2-S.II.2. -S.II.2.4-S.II.2.5)

S.II.2.1 Bank Credit

S.II.1 RBI Credit to Commercial Sector (S.II.1.1+S.II.1.2+S.II.1.3)

S.II.1.1 RBI’s investments in shares/ bonds of financial institutions, ordinary debentures of co- operative sectors, CLMB debentures etc.

S.II.1.2 Loans to financial institutions

S.II.1.3 Internal Bills (under Bills Rediscounting Scheme)

S.II.2 Other Banks’ credit to Commercial Sector (S.II.2.1 + S.II.2.2)

S.II.2.1 Bank Credit

Manual on Financial and Banking Statistics

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

S.II.2.5 Time deposits held by Banks (including inter-bank time deposits held by state co-operative banks)

S.III Net Foreign Exchange Assets of the Banking Sector (S.III.1+S.III.2)

S.III.1 Net Foreign Exchange Assets of the RBI (S.III.1.1 + S.III.1.2 + S.III.1.3-S.III.1.4-S.III.1.5)

S.III.1.1 Gold Coin and Bullion

S.III.1.2 Foreign Securities

S.III Net Foreign Exchange Assets of the Banking Sector (S.III.1+S.III.2)

S.III.1 Net Foreign Exchange Assets of the RBI (S.III.1.1 + S.III.1.2 + S.III.1.3-S.III.1.4- S.III.1.5)

S.III.1.1 Gold Coin and Bullion

S.III.1.2 Foreign Securities

S.III Net Foreign Exchange Assets of the Banking Sector (S.III.1+S.III.2)

S.III.1 Net Foreign Exchange Assets of the RBI (S.III.1.1 + S.III.1.2- S.III.1.3+S.III.1.4)

S.III.1.1 Gold Coin and Bullion

S.III.1.2 Foreign Currency Assets of the RBI(S.III.1.2.1+S.III.1.2.2)

S.III.1.2 Foreign Securities

This adjustment was considered necessary since the FWG was concerned with M1. The presentation of data on bank credit to commercial sector on net basis was changed into gross basis in May 1974, as (i) time deposits are used not only for financing bank credit to commercial sector but also for lending to the Government and (ii) these are not owned by commercial enterprises who largely borrow from banks.

Inclusive of valuation of Gold following its revaluation close to international market price effective October 17,

Since July 1996, foreign currency assets are being valued at the exchange rate prevailing at the end of every week. Such revaluation has a corresponding effect on Reserve Bank’s net non- monetary liabilities (capital account).

Certain foreign securities e.g. , IBRD shares, Commonwealth bonds etc. which were part of RBI’s claims on

Monetary Statistics

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

S.III.1.3 Balances held abroad

S.III.1.4 IMF A/c No.

S.III.1.5 Special Currency withdrawn from Gulf States held under Other deposits of the RBI if any.

S.III.2 Net Foreign Exchange Assets of Banking System

S.IV. Net non-monetary Liabilities of the Banking Sector (S.IV.1+S.IV.2)

S.IV.1 Net non-monetary Liabilities of the RBI (S.IV.1.1 + S.IV.1.2 + S.IV.1.3 + S.IV.1.4 + S.IV.1.5 - S.IV.1.6 + S.IV.1.7)

S.IV.1.1 Paid-up Capital

S.IV.1.2 Reserves

S.III.1.3 Balances held abroad

S.III.1.4 IMF A/c No.

S.III.1.5 Quota subscription in rupees.

S.III.2 Net Foreign Exchange Assets of Banking System (Authorised Dealers’ Balances)

S.IV. Government’s Currency Liabilities to the Public

S.V. Net non-monetary Liabilities of the Banking Sector (S.V.1+S.V.2)

S.V.1 Net non-monetary Liabilities of the RBI (S.V.1.1 + S.V.1.2 + S.V.1.3 + S.V.1.4 + S.V.1.5 + S.V.1.6 + S.V.1.7 + S.V.1.8 - S.V.1.9)

S.V.1.1 Paid-up Capital

S.V.1.2 Reserves

S.III.1.2.2 Balances held abroad

S.III.1.3 IMF A/c No.

S.III.1.4 Quota subscription in rupees.

S.III.2 Net Foreign Currency Assets of Banking System(S.III.2.1- S.III.2.2-S.III.2.3)

S.III.2.1 Foreign Currency Assets of the Banking System

S.III.2.2. Overseas Borrowings of the Banking System

S.III.2.3 Non-Resident Repatriable Foreign Currency Fixed Deposits with the Banking System (C.II.2.2.1+C.II.2.3.1)

S.IV. Government’s Currency Liabilities to the Public

S.V. Capital Account of the Banking Sector (S.V.1+S.VI.2)

S.V.1 Capital Account of the RBI (S.V.1.1 + S.V.1.2 + S.V.1.3 + S.V.1.4 + S.V.1.5 + S.V.1.6)

S.V.1.1 Paid-up Capital

S.V.1.2 Reserves

Government were reclassified as part of its foreign assets by the SWG.

Includes balances held abroad ( i.e. , the cash component of nostro accounts, etc. ) and investments in eligible foreign securities and bonds.

Net of Indian currency returned by Pakistan awaiting adjustment.

The WGMS has bifurcated the non- monetary liabilities of the banking sector into the capital account and other items (net).

Monetary Statistics

First Working Group Second Working Group Working Group on Money REMARKS (FWG) (1961) (SWG) (1977) Supply (WGMS) (1998)

1 2 3 4

S.VI.1.5 Contingency ReservesS.VI.1. Exchange Fluctuation Reserve / Currency and Gold Revaluation Account

S.VI. 1.7 Exchange Equalisation Account

S.VI.1.8 IMF Quota Subscription and other payments in rupees included in IMF A/c No.

S.VI.1.9 Other Assets net of Gold in Banking department

S.VI.2 Other items (net) of the Banking System (residual)

Source: Report of the Working Group on Money Supply: Analytics and Methodology of Compilation (Chairman: Dr. Y.V. Reddy) (1998), Reserve Bank of India.