Download Portfolio Theory Lecture Notes and more Lecture notes Investment Management and Portfolio Theory in PDF only on Docsity!

Lecture 8: Portfolio TheoryLecture 8: Portfolio Theory

_ _ _ _ _ _ _ _

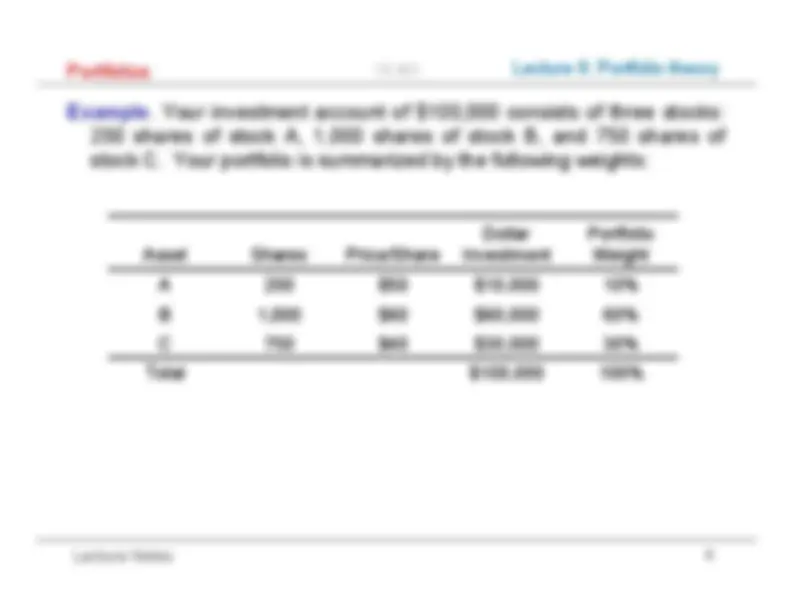

Example. Your investment account of $100,00 0 consists of three stocks: 200 shares of stock A, 1 , 000 shares of stock B, and 750 shares of stock C. Your portfolio is summarized by the following weights: Asset Shares Price/Share Dollar Investment Portfolio Weight A 200 $50 $10,000 10% B 1,000 $60 $60,000 60% C 750 $40 $30,000 30% Total $100,000 100%

Example (cont). Your broker informs you that you only need to keep $ 50 , 000 in your investment account to support the same portfolio of 200 shares of stock A, 1 , 000 shares of stock B, and 750 shares of stock C; in other words, you can buy these stocks on margin. You withdraw $ 50 , 000 to use for other purposes, leaving $ 50 , 000 in the account. Your portfolio is summarized by the following weights: Asset Shares Price/Share Dollar Investment Portfolio Weight A 200 $50 $10,000 20% B 1,000 $60 $60,000 120% C 750 $40 $30,000 60% Riskless Bond −$50,000^ $1 −$50,000^ −100% Total $50,000 100%

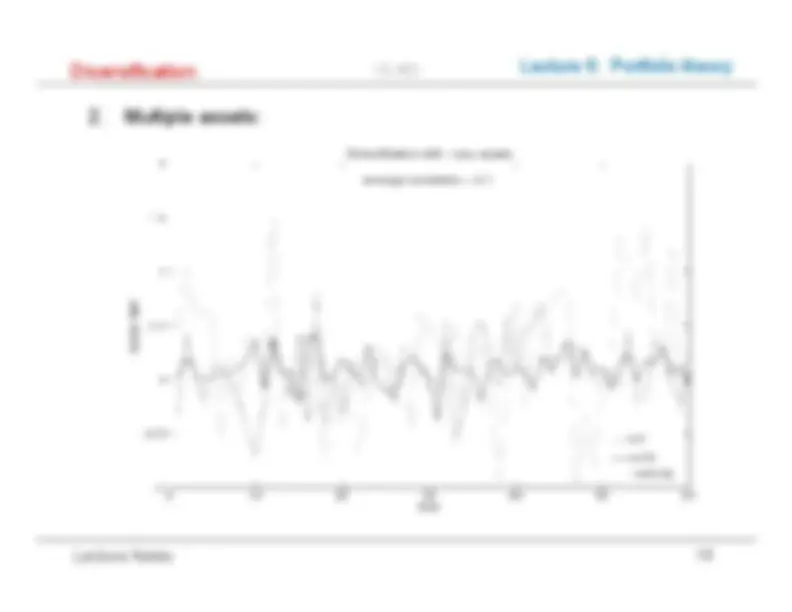

Why not pick the best asset instead of forming a portfolio? We don’t know which stock is best! Portfolios provide diversification, reducing unnecessary risks Portfolios can enhance performance by focusing bets Portfolios can customize and manage risk/reward trade-offs How do we chose a “good” portfolio? What does “good” mean? What characteristics of a portfolio do we care about? risk and reward (expected return) higher expected returns are preferred higher risks are not preferred

_

_

_

_

_

_

_

_