Download Small Business Financing and Credit Usage: 2020 Report and more Lecture notes Capstone Design in PDF only on Docsity!

SMALL BUSINESS

CREDIT SURVEY

2020 REPORT ON EMPLOYER FIRMS

Atlanta • Boston • Chicago • Cleveland • Dallas • Kansas City • Minneapolis

New York • Philadelphia • Richmond • St. Louis • San Francisco

F E D E R A L R E S E R V E B A N K S o f

TABLE OF CONTENTS

14 APPLICATIONS

15 LOAN/LINE OF CREDIT SOURCES

17 LOAN/LINE OF CREDIT APPROVALS

19 LENDER CHALLENGES

20 APPLICANT SATISFACTION

21 NONAPPLICANTS

22 FINANCIAL CHALLENGES:

NONAPPLICANTS AND APPLICANTS

23 NONAPPLICANT USE OF

FINANCING AND CREDIT

24 NONAPPLICANT LOAN/LINE

OF CREDIT SOURCES

25 U.S. SMALL EMPLOYER FIRM

DEMOGRAPHICS

29 FACILITIES

31 METHODOLOGY

i ACKNOWLEDGMENTS

ii EXECUTIVE SUMMARY

1 PERFORMANCE

3 GROWTH EXPECTATIONS

4 GROWTH AMBITIONS

5 FINANCIAL CHALLENGES

6 FUNDING BUSINESS OPERATIONS

8 RELIANCE ON PERSONAL FINANCES

9 LENDING RELATIONSHIPS

10 DEMAND FOR FINANCING

11 FINANCING NEEDS AND OUTCOMES

12 FINANCING RECEIVED

13 FINANCING RECEIVED AND

SHORTFALLS

SMALL BUSINESS CREDIT SURVEY | 2020 REPORT O N EMPLOYER F IRMS ii

EXECUTIVE SUMMARY 1 U.S. Small Business Administration, “2018 Small Business Profile,” https://www.sba.gov/sites/default/files/advocacy/2018-Small-Business-Profiles-US.pdf_._ 2 The Small Business Credit Survey collects information from both employer and nonemployer firms. The 2019 survey yielded 4,020 responses from nonemployers.

The publication of this report comes at a

particularly challenging time for our nation’s

small business sector. Small businesses

across the country are grappling with the

profound impact of the COVID-19 pandemic

on their operations and on their owners’ and

employees’ livelihoods. As policymakers and

service providers begin to enact programs to

help firms weather the economic challenges,

insights about the financial position of small

businesses can provide a useful perspective

on how best to target funds and services.

The Federal Reserve Banks’ Small Business

Credit Survey (SBCS), fielded in Q3 and Q

of 2019, offers baseline data on the financ-

ing and credit positions of small firms before

the onset of the crisis. The survey findings

provide insights into firms’ preparedness

to withstand the shock, their existing debt

levels, and the actions they may take in

response to an unexpected loss of revenues.

Understanding that the potential effects of

COVID-19 are substantial and will vary by

type of business, accompanying this report

is a separate analysis that explores small

business resiliency. This supplemental brief,

Can Small Firms Weather the Economic

Effects of COVID-19? , is published concur-

rently with this report. A subsequent report

will provide results from nonemployer firms.

The results of the survey raise several

important considerations in the current

environment: most firms are ill prepared for

a sustained period of revenue loss; firms’

reliance on personal funds could mean

severe repercussions for those individuals

and households in the event of failure; and

many small businesses do not rely on

traditional banks for credit, and, therefore,

any program designed to support them

should take that into consideration.

SURVEY FINDINGS

The importance of small businesses to our

nation’s economy cannot be overstated.

Small employer firms, those with 1–

employees, account for 47.5% of the

private-sector workforce^1 and are vital to

the fabric of local communities. The SBCS

delivers timely information on small business

financing needs, decisions, and outcomes to

policymakers, lenders, and service providers.

The 2019 survey yielded 5,514 responses

from small employer firms with 1–499 full-

or part-time employees (hereafter “firms”), in

the 50 states and the District of Columbia.^2

Overall, the survey finds

Firm performance was relatively strong

prior to the pandemic.

Small business respondents reported

a strong end to 2019. A majority of small

businesses (56%) reported that their firms

had experienced revenue growth, and

more than one-third added employees

to their payrolls.

The shares of firms reporting revenue

growth, profitability, and employment

growth were all virtually unchanged

from 2018.

Profit margins were tightening for many.

Input costs increased for 76% of firms

over the prior year. Profit margins fell for

40% of firms. Of firms that reported higher

input costs, 61% raised the prices that

they charge.

Firms have common cash flow challenges,

and many rely on personal funds.

In the prior 12 months, 66% of employer

firms faced financial challenges; the

most common challenge was paying

operating expenses (43%).

If faced with a two-month revenue

loss, 86% of firms would need to take

some action to supplement funding

or cut expenses.

à The most common action (47% of

firms) would be to use the owner’s

personal funds.

à Another 17% of firms would have

to close.

à Among firms that applied for financing

in the prior 12 months, 46% would plan

to take out additional debt.

Owners’ personal finances remain deeply

intertwined with the finances of their

businesses, with 88% of firms relying on

an owner’s personal credit score to secure

financing. Additionally, 56% have used

funds from their personal savings, friends,

or family within the last five years to

support their business.

Debt holdings are common and typically

small dollar, and nearly half of recent credit

applicants have experienced funding gaps.

Forty percent of firms hold outstanding

debt in amounts up to $100,000. A majority

of firms used personal guarantees as

collateral to secure this debt.

Demand for new financing has been

steady, with 43% of firms applying for new

credit in 2019, in line with the 43% that

applied in 2018, and 40% in 2017.

Large and small banks remain small

firms’ top choices when applying for

credit, followed closely by online lenders;

having a relationship with a lender drives

many firms to apply to banks, but the

chances of being funded and speed of

credit decisions are top reasons firms

apply to an online lender.

Fifty-one percent of applicants received

the full amount of financing sought.

Of the firms that did not receive the full

amount, 20% indicated that the firm chose

to decline some or all of the approved

financing—most often because the

interest rate was too high.

SMALL BUSINESS CREDIT SURVEY | 2020 REPORT O N EMPLOYER F IRMS iii

EXECUTIVE SUMMARY (CONTINUED) 3 U.S. Census Bureau, County Business Patterns, 2017.

Though banks are the most broad-reaching

lending channel, many small businesses

do not use bank funding.

Less than half (44%) of small firms have

obtained funds from a bank in the last

five years. The most common source

of funding for firms overall was personal

savings or funds from friends or family.

Among firms that have obtained external

financing—outside of family or friend

networks—banks were the most common

channel (44% of firms), followed by online

lenders (22% of firms) and credit unions

(6% of firms).

The use of bank financing varies signifi-

cantly by race and ethnicity of owner, firm

revenue size, and credit risk, with highest

reported bank funding found among firms

with >$1M in annual revenues (57%), firms

with low credit risk (55%), and firms with

non-Hispanic white ownership (46%).

By contrast, firms with Non-Hispanic

black ownership are half as likely to

have obtained bank funds (23%), and

rates are similarly low among microbusi-

nesses (that is, $100,000 or less

in revenues)—24%—and those with

Latino ownership (34%).

ABOUT THE SURVEY

The SBCS is an annual survey of firms with

fewer than 500 employees. These types of

firms represent 99.8% of all employer estab-

lishments^3 in the United States. Respondents

are asked to report information about their

business performance, financing needs

and choices, and borrowing experiences.

Responses to the SBCS provide insights

on the dynamics behind lending trends and

shed light on noteworthy segments of the

small business population. The SBCS is not

a random sample; results should be analyzed

with awareness of potential biases that are

associated with convenience samples. For

detailed information about the survey design

and weighting methodology, please consult

the Methodology section.

Given the breadth of the 2019 survey data,

the SBCS can shed light on various segments

of the small business population, including

startups and growing firms, microbusiness-

es, minority-owned firms, women-owned

firms, firms located in low- and moderate-

income communities, and self-employed

individuals (nonemployer firms).

PERFORMANCE (CONTINUED) 1 Percentages may not sum to 100 due to rounding. 2 Approximately the second half of 2018 through the second half of 2019. 3 “Large” refers to a change of 4% or greater. “Small” refers to a nonzero change that is less than 4%. 76% of small firms saw their input costs increase over the prior year. 40% reported falling profit margins.

CHANGES IN COSTS, PRICES, AND PROFITABILITY,^1 Prior 12 Months^2

(% of employer firms)

Large increase^3

Small increase^3

No change

Small decrease^3

Large decrease^3

Change in cost

of labor/wages

N=5,

Change in

input costs

N=4,

Change in prices

the business

charges N=4,

Change in

profit margins

N=4,

2%^ 4%

Of firms that saw higher input costs, 61% raised the prices that they charge.

CHANGE IN PRICES CHARGED BY FIRMS WITH INCREASED INPUT COSTS N=3,

(% of employer firms with increased input costs)

39%

Did not raise prices

61%

Raised prices

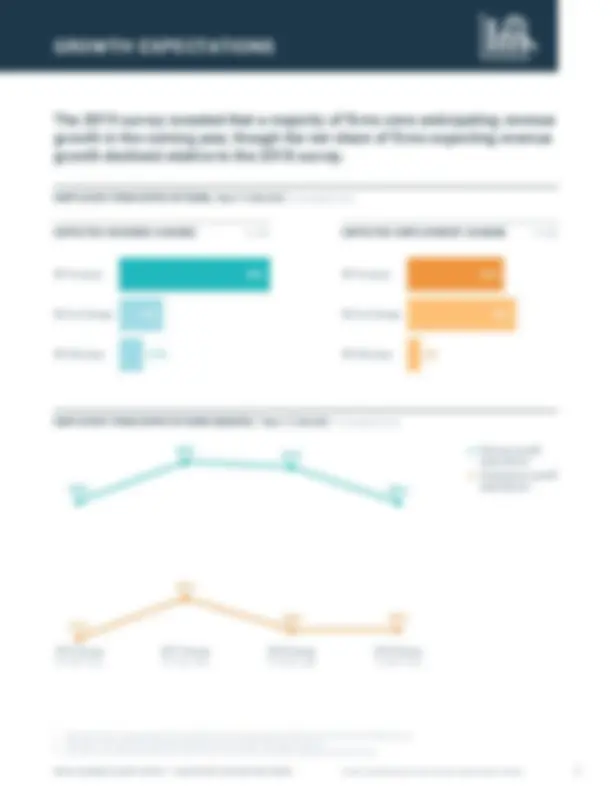

GROWTH EXPECTATIONS 1 Expected change in approximately the second half of the surveyed year through the second half of the following year. 2 The index is the share reporting expected growth minus the share reporting a reduction. 3 Questions were asked separately, thus the number of observations may differ slightly between questions. The 2019 survey revealed that a majority of firms were anticipating revenue growth in the coming year, though the net share of firms expecting revenue growth declined relative to the 2018 survey.

EMPLOYER FIRM EXPECTATIONS, Next 12 Months^1 (% of employer firms)

EXPECTED REVENUE CHANGE N=4,967 EXPECTED EMPLOYMENT CHANGE N=5,

Will increase 69%

Will not change

Will decrease

Will increase 44%

Will not change 50%

Will decrease

EMPLOYER FIRM EXPECTATIONS INDICES,^2 Next 12 Months^1 (% of employer firms)

2016 Survey

N^3 =9,765–9,

2017 Survey

N^3 =7,736–8,

2018 Survey

N^3 =6,450–6,

2019 Survey

N^3 =4,967–5,

Revenue growth

expectations

Employment growth

expectations

FINANCIAL CHALLENGES 1 Approximately the second half of 2018 through the second half of 2019. 2 Respondents could select multiple options. 66% of employer firms faced financial challenges in the prior 12 months.^1

FINANCIAL CHALLENGES,^2 Prior 12 Months^1 N=6,

(% of employer firms)

17% of firms would have to close if they experienced a two-month revenue loss.

ACTIONS BUSINESS WOULD TAKE IN RESPONSE TO A 2-MONTH REVENUE LOSS^2 N=5,

(% of employer firms)

Use owner's personal funds

Take out debt

Reduce salaries of owner

or employees

Lay off employees

Downsize operations (reduce

hours, services, or production)

Defer expenses/payments

Close or sell the business

No action; use cash reserves

to continue normal operations

19% 8%

Purchasing

inventory

or supplies

to fulfill

contracts

30%

Making payments

on debt

33%

Securing

credit

43%

Paying operating expenses

(including wages)

34%

No financial

challenges

Other financial challenge

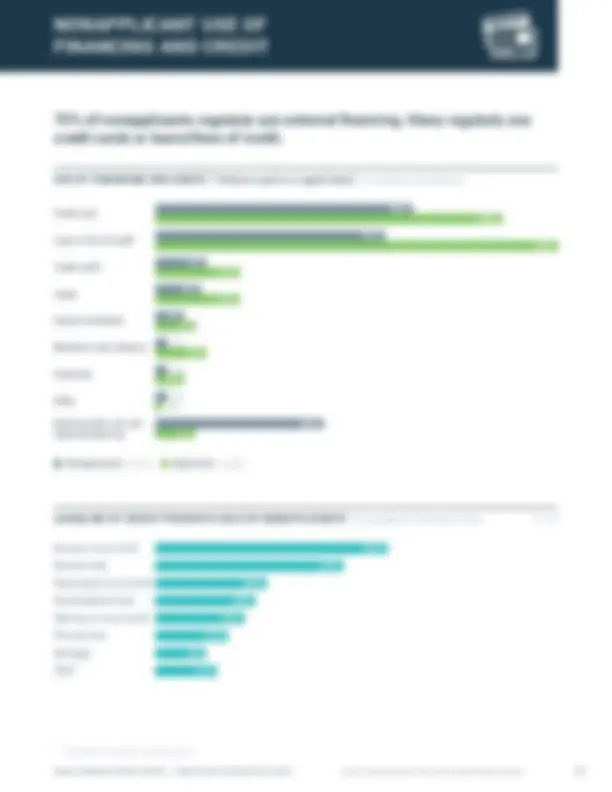

1 Percentages may not sum to 100 due to rounding. 2 Respondents could select multiple options. FUNDING BUSINESS OPERATIONS Loans, lines of credit, and credit cards are the most common types of external financing used by employer firms.

USE OF FINANCING AND CREDIT,^2 Products used on a regular basis (% of employer firms) N=5,

Loan or line of credit

Trade credit

Credit card

Leasing

Equity investment

Merchant cash advance

Factoring

Other

Business does not use

external financing

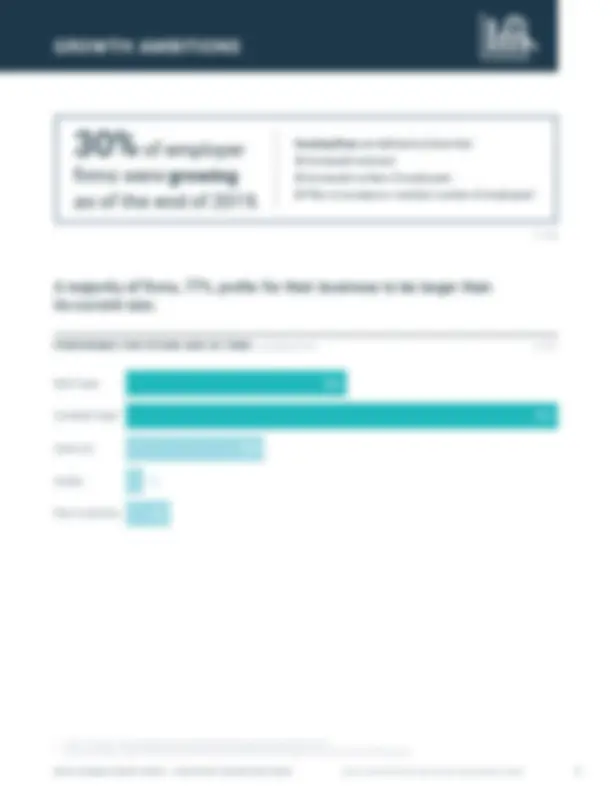

For 77% of firms, retained business earnings are the primary source of funding.

PRIMARY FUNDING SOURCE^1 (% of employer firms)

External financing

Personal funds

Retained business

earning

2016 Survey

N=9,

2017 Survey

N=8,

2019 Survey

N=5,

2018 Survey

N=6,

88% of employer firms rely on an owner’s personal credit score to obtain financing, similar to 2018.

USE OF PERSONAL AND BUSINESS CREDIT SCORES^1 (% of employer firms) N=3,

Business score only Owner’s personal score only Both business and personal scores

RELIANCE ON PERSONAL FINANCES 1 Percentages may not sum to 100 due to rounding. 2 Respondents could select multiple options. 3 Response option “other” not shown. See Appendix for details. 4 “Online lenders” are defined as nonbank alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, Kabbage, and PayPal Working Capital. 5 “Finance company” includes nonbank lenders such as mortgage companies, equipment dealers, insurance companies, auto finance companies, etc. 6 Examples include payday lender, check cashing, pawn shop, money order/transmission service, etc. 7 Community development financial institutions (CDFIs) are financial institutions that provide credit and financial services to underserved markets and populations. CDFIs are certified by the CDFI Fund at the U.S. Department of the Treasury.

FUNDING SOURCES USED IN THE LAST FIVE YEARS2,3^ (% of employer firms) N=5,

Personal savings,

friends, or family

Nonprofit/community-

based funding source

Bank 44%

Alternative financial

source^6 3%

Online lender^4 20%

CDFI^7 1%

Finance company^5 9%

None 15%

Credit union 6%

56% of firms have relied on personal savings, friends, or family to fund their business in the last five years.

LENDING RELATIONSHIPS 44% of firms have used a bank for funding in the last five years, indicating a prior lending relationship. Banking relationships are more common among larger firms, firms with better credit scores, and firms with white ownership.

FUNDING SOURCES USED IN THE LAST FIVE YEARS, Select Sources (% of employer firms) N=5,

Bank 44%

Online 20%

lender

Credit 6%

union

FUNDING SOURCES USED IN THE LAST FIVE YEARS BY DEMOGRAPHIC CHARACTERISTICS,

Select Sources (% of employer firms)

Non-Hispanic white ownership N=3,

Low credit risk N=2,

Annual revenue of $100K–$1M N=1,

Annual revenue of $100K or less N=

Medium/high credit risk N=1,

Non-Hispanic Black ownership N=

Hispanic ownership N=

Annual revenue of >$1M N=2,

Bank

Online lender

Credit union

FINANCING NEEDS AND OUTCOMES 1 Based on the prior 12 months, which is approximately the second half of 2018 through the second half of 2019. 2 Discouraged firms are those that did not apply for financing because they believed they would be turned down.

FUNDING NEEDS AND OUTCOMES^1 (% of employer firms) N=5,

To gauge funding success and shortfalls, we combine applicants’ financing outcomes and nonapplicants’ reasons for not

applying. Firms that had their funding needs met emerge in two forms:

1) Applicant firms that received the full amount of financing sought; or

2) Nonapplicant firms that did not apply for financing because they already had sufficient financing.

The remaining firms may or may not have unmet funding needs. When applicant firms did not obtain the full amount of financing

sought, we consider them to have a funding shortfall. When nonapplicant firms did not report they had sufficient financings,

we consider them to have potentially unmet funding needs.

43% Applied for financing 9% 12% 22%

Received

none

Received

some

Received

all

57% Did not apply for financing 27% 14% 9% 7%

Sufficient

financing

Debt averse Discouraged^2 Other

21% Financing shortfall 49% Financing needs met 30% May have unmet financing needs

1 Respondents could select multiple options. 2 Credit risk is determined by the self-reported business credit score or personal credit score, depending on which is used to obtain financing for their business. If the firm uses both, the higher risk rating is used. “Low credit risk” is a 80–100 business credit score or 720+ personal credit score. “Medium credit risk” is a 50–79 business credit score or a 620–719 personal credit score. “High credit risk” is a 1–49 business credit score or a <620 personal credit score. FINANCING RECEIVED 51% of employer firms that applied for credit received all the financing they sought.

TOTAL FINANCING RECEIVED^1 (% of applicants)

All (100%)

Most (51%–99%)

Some (1%–50%)

None (0%)

2016 Survey

N=4,

2017 Survey

N=3,

2019 Survey

N=2,

2018 Survey

N=2,

47%^ 47%

Low-credit-risk applicants were more likely to obtain all the financing sought, compared to medium- or high-credit-risk applicants.

FINANCING RECEIVED BY CREDIT RISK OF FIRM^2 (% of applicants)

All (100%)

Most (51%–99%)

Some (1%–50%)

None (0%)

Low credit risk

N=

Medium credit risk

N=

High credit risk

N=

APPLICATIONS

FINANCING AND CREDIT PRODUCTS SOUGHT^1 (% of applicants) N=2,

Loan or line of credit 88%

Credit card 29%

Trade credit 10%

Merchant cash advance 9%

Leasing 9%

Equity investment 5%

Factoring 4%

Other 1%

APPLICATION RATE FOR LOANS/LINES OF CREDIT^1 (% of loan/line of credit applicants) N=1,

Business loan 49%

Business line of credit 40%

SBA loan 20%

Auto/equipment loan 14%

Personal loan 10%

Mortgage 5%

Home equity line of credit 8%

Other product 10%

1 Respondents could select multiple options. Applicants were most often seeking loans or lines of credit.

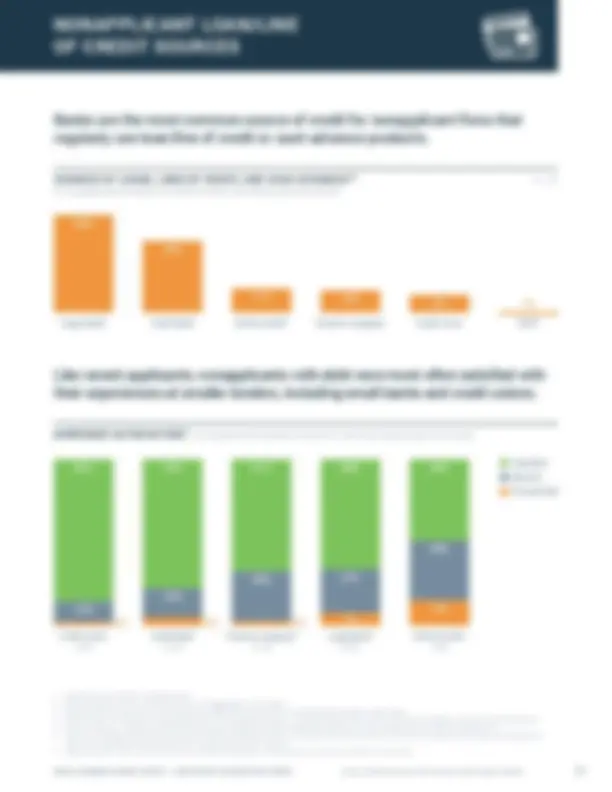

LOAN/LINE OF CREDIT SOURCES Large and small banks receive the most credit applications from small firms. Medium/high-credit-risk applicants, however, were more inclined to apply to online lenders.

CREDIT SOURCES APPLIED TO1,2,3^ (% of loan/line of credit and cash advance applicants) N=1,

CREDIT SOURCES APPLIED TO BY CREDIT RISK OF FIRM1,2,4^ (% of loan/line of credit and cash advance applicants)

Low credit risk N=861 Medium/high credit risk N=

Large bank^5 Small bank Online lender^6 Finance company^7 Credit union CDFI^8

Large bank^5 Small bank Online lender^6 Finance company^7 Credit union CDFI^8

1 Respondents could select multiple options. 2 Due to the addition of the “Finance company” option, source application rates are not comparable to those of previous survey years. 3 Respondents who selected “other” were asked to describe the source. They most frequently cited auto/equipment dealers, farm-lending institutions, friends/family/ owner, nonprofit organizations, private investors, and government entities. 4 Credit risk is determined by the self-reported business credit score or personal credit score, depending on which is used to obtain financing for their business. If the firm uses both, the higher risk rating is used. “Low credit risk” is a 80–100 business credit score or 720+ personal credit score. “Medium credit risk” is a 50–79 business credit score or a 620–719 personal credit score. “High credit risk” is a 1–49 business credit score or a <620 personal credit score. 5 Respondents were provided a list of large banks (those with at least $10B in total deposits) operating in their state. 6 “Online lenders” are defined as nonbank alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, Kabbage, and PayPal Working Capital. 7 “Finance company” includes nonbank lenders such as mortgage companies, equipment dealers, insurance companies, auto finance companies, etc. 8 Community development financial institutions (CDFIs) are financial institutions that provide credit and financial services to underserved markets and populations. CDFIs are certified by the CDFI Fund at the U.S. Department of the Treasury.