Download Fund Balance Calculation for Recharge Centers: A Guide for Financial Management and more Study notes Financial Statement Analysis in PDF only on Docsity!

i

- I. INTRODUCTION CONTENTS

- PURPOSE..................................................................................................................................................................

- CONTENTS AND ORGANIZATION

- GETTING STARTED

- II. MANAGING RECHARGE CENTERS USING FUND BALANCE.......................................................................................

- INSTRUCTION & DEPARTMENTAL FUNCTION RECHARGE CENTERS AND PUBLIC SERVICE ACTIVITIES - FUND BALANCE - ACCEPTABLE FUND BALANCE - ASSESSING THE CURRENT FUND BALANCE - PROJECTING YEAR-END FUND BALANCE

- FLOW-THROUGH ACTIVITIES - OCCASIONAL FLOW-THROUGH SALES IN RECHARGE CENTERS

- GENERAL SERVICE CENTERS AND SPECIALIZED SERVICE FACILITIES - FUND BALANCE - ACCEPTABLE FUND BALANCE - ASSESSING THE CURRENT FUND BALANCE - PROJECTING YEAR-END FUND BALANCE - EXAMPLE: DETERMINATION AND ANALYSIS OF ACCEPTABLE FUND BALANCE - EXAMPLE: FUND BALANCE PROJECTION FOR A GENERAL SERVICE CENTER

- III. SETTING RATES......................................................................................................................................................

- THE RATE CYCLE

- PROJECTING RATE YEAR EXPENDITURES

- STATEMENT OF INCOME AND EXPENSE REPORT

- RECHARGE CENTER

- STATEMENT OF INCOME AND EXPENSE WORKSHEET TEMPLATE

- PROJECTING FUND BALANCE

- CALCULATING THE RATE PER UNIT

- SALARY AND WAGE SCHEDULE

- SALARY AND WAGE SCHEDULE EXAMPLE #1..............................................................................................................

- SALARY AND WAGE SCHEDULE EXAMPLE #2..............................................................................................................

- RATE COMPUTATION METHODS

- ONE PRODUCT: ONE RATE

- WHEN IT’S NOT THAT SIMPLE....

- EXAMPLE OF SETTING AN EXTERNAL CUSTOMER RATE

- SPECIAL RATE-SETTING CONSIDERATIONS

- SUBSIDIES: CHARGING INTERNAL CUSTOMERS AT LESS THAN BREAK-EVEN

- CAPITAL EQUIPMENT

- USING MARKET RATES........................................................................................................................................... ii

- STOREROOM MARKUP CALCULATIONS (STOREROOM OPERATIONS ONLY)

- IV. SUBMITTING A RATE REQUEST

- (1) REQUEST FOR RATE APPROVAL MEMORANDUM......................................................................................................

- (2) SUPPORTING FINANCIAL DOCUMENTATION

- a. PROJECTED STATEMENT OF INCOME AND EXPENSE

- b. RATE CALCULATION

- c. SALARY AND WAGE SCHEDULE

- V. PURCHASE AND DEPRECIATION OF CAPITAL EQUIPMENT

- (1) TRANSFER FUNDING FOR INITIAL PURCHASE OF EQUIPMENT......................................................................................

- (2) PURCHASE OF EQUIPMENT...................................................................................................................................

- (3) ESTABLISH DEPRECIATION RECOVERY ACCOUNT (XXX DEPT-DEPR)

- (4) TRANSFER DEPRECIATION EXPENSE TO DEPRECIATION RECOVERY ACCOUNT

- (5) USE OF FUNDS IN DEPRECIATION RECOVERY ACCOUNT.............................................................................................

- (6) EQUIPMENT SOLD INTERNALLY FROM ONE RECHARGE CENTER TO A DIFFERENT RECHARGE CENTER

- (7) FUNDS RECEIVED BY SELLING DEPARTMENT TRANSFERRED TO DEPRECIATION RECOVERY ACCOUNT

- EXAMPLE: INTER-DEPARTMENTAL SALE OF EQUIPMENT

- APPENDIX A - USEFUL DEFINITIONS

- APPENDIX B EXAMPLE: RATE REQUEST & SUPPORTING DOCUMENTATION - EXAMPLE: REQUEST FOR RATE APPROVAL - EXAMPLE: STATEMENT OF INCOME AND EXPENSE WORKSHEET, WITH PROJECTED FUND BALANCE - SALARY AND WAGE SCHEDULE - SUPPLIES & EXPENSES SCHEDULE - DEPRECIATION SCHEDULE....................................................................................................................................... - BREAK-EVEN RATE PER UNIT……………………………………………………………………………………………………………………………. - RATES TO BE CHARGED.......................................................................................................................................... - DOCUMENT USED TO CAPTURE BILLING INFORMATION

- APPENDIX C MAPS

- IDENTIFICATION OF RECHARGE CENTER TYPE

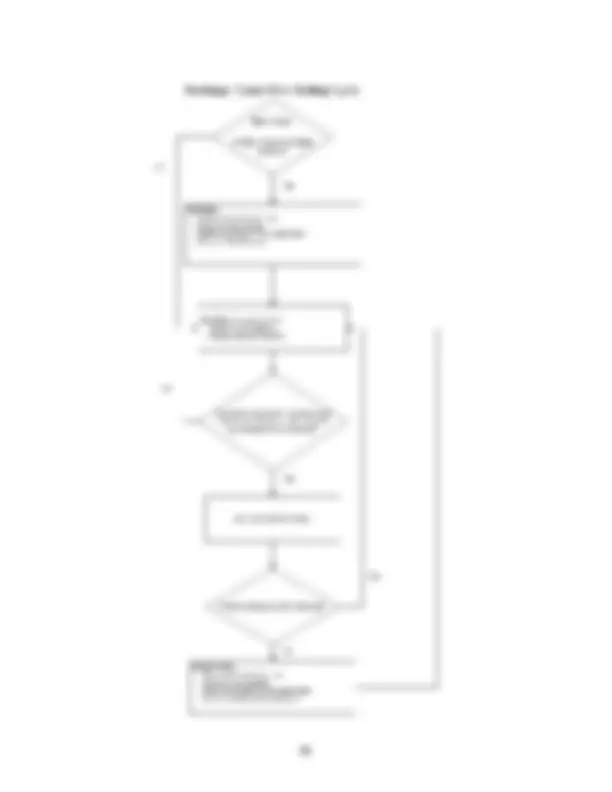

- RATE SETTING CYCLE

- RATE APPROVAL ROUTING PROCESS

GETTING STARTED

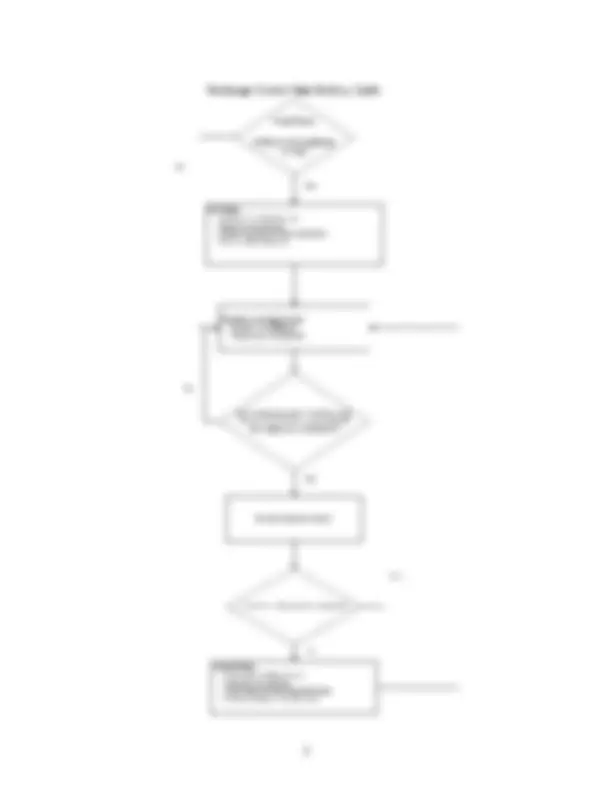

First: Review the Rate Setting Cycle diagram on page 3.

Each projected rate year is twelve months in length, and begins the first of any month, depending on what best meets the management need. This rate year could coincide with the fiscal year, the calendar year or any twelve-month period. A new rate year begins twelve months later or whenever a new rate is approved and implemented.

Next: Develop an understanding of what type of recharge center you have, and how the Recharge Center Policy applies to that center. Use the IDENTIFICATION OF RECHARGE CENTER TYPE Map (page 85 ) to determine the appropriate center category and which portions of the Recharge Center Policy apply.

Then: It will be helpful to become familiar with the Useful Definitions in Appendix A.

Much of the information in this manual applies to all recharge centers. In some instances, procedures and rules are different for departmental function centers than for general service centers, etc. Sections that apply only to general service centers or storeroom operations, for example, are clearly labeled.

We usually think of this “ -$5,000 to + $5,000 or 10 percent of revenue or two months of cash expenses, whichever amount is larger” range as our “tolerance zone”. Our goal is for each recharge center to recover costs of goods and services provided – but, over time, to incur neither a profit nor a loss. In other words, if we decided to eliminate a particular recharge center at any point in time, after we closed all the income and expense at year-end, collected the receivables and paid the liabilities, the fund balance of the center would be zero (or very, very close to zero).

Year-end fund balance should be projected frequently to assure that the balance will fall within the “tolerance zone” (between -$5,000 and the greater of +$5,000 or 10% of projected income for the year or two months of cash expenses).

ACCEPTABLE FUND BALANCE

DETERMINING THE “TOLERANCE ZONE“ FOR: INSTRUCTION & DEPARTMENTAL FUNCTION RECHARGE CENTERS ORGANIZED ACTIVITIES & PUBLIC SERVICE ACTIVITIES

A. Is projected income for the year less than $50,000? If so, is the projected fund balance at fiscal year-end between -$5,000 and +$5,000? If so, the balance is acceptable. We can think of the - $5,000 to +$5,000 range as the “fund balance tolerance zone”. B. If projected income for the year is greater than $50,000, we proceed to the next step of the test: Determining 10% of the sum of income for the year and determining two months of cash expenses (average expenses based on an entire year of data). The greater of these two amounts becomes the upper limit of the acceptable fund balance range. In this instance, the “fund balance tolerance zone” is either from -$5,000 to 10% of revenue OR from -$5,000 to two months of cash expenses.

C. If a fund balance of 10% of income or two months of cash expenses is used, discretion should be used in determining that these balances are appropriate fund balances to be carried. For example, if income is significantly greater than expenses for the year, the recharge center may be overcharging. If this is the case, 10% of income would not a reasonable fund balance to use.

MANAGEMENT ACTION: If the current month fund balance is not within the fund balance tolerance zone, we need to ask:

- Does our financial position fit the pattern of prior years at this same time?

- Is our financial position approximately what was projected at this time?

- Are there unusual income or expense items this period?

- Where will we be at year-end?

Reminder: The goal is for each recharge center to cover costs of goods and services provided – but, over time, to incur neither a profit nor a loss. In other words, if we decide to eliminate a particular recharge center at any point in time, after we close all the income and expense at year-end, collected the receivables and paid the liabilities, the fund balance of the center would be zero (or very, very close to zero)

ASSESSING THE CURRENT FUND BALANCE

FOR: INSTRUCTION & DEPARTMENTAL FUNCTION RECHARGE CENTERS ORGANIZED ACTIVITIES & PUBLIC SERVICE ACTIVITIES

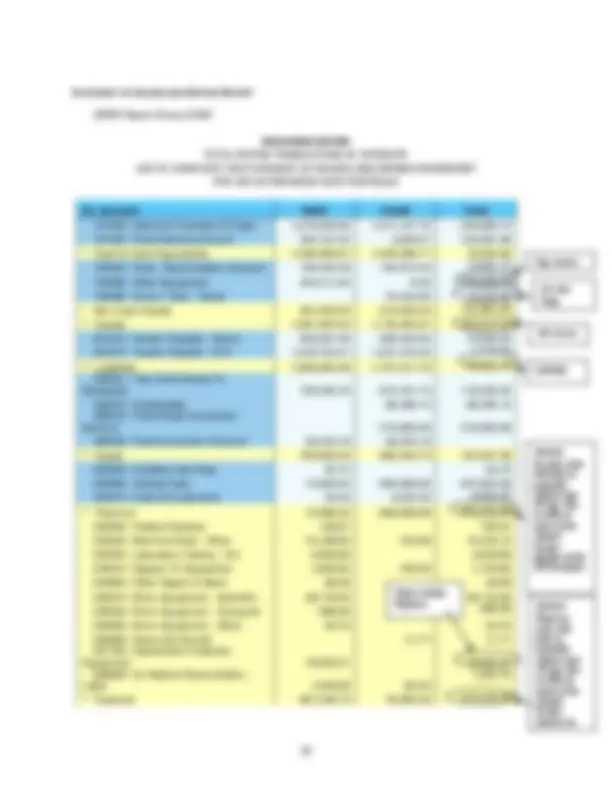

There are several ways to determine current fund balance: The necessary information can be calculated from figures derived from GR55 (Report Group Z100), or from using the recharge fund balance transaction code listed below.

The most straight-forward approach is to:

Run the transaction code GR55 (Report Group ZRCH) in SAP:

The transaction code will provide the recharge’s life-to-date fund balance status. It prompts you to enter your recharge center fund(s) – use operating fund(s) only, the applicable fiscal year, and the from and to periods. Please be aware that if you are running the report to calculate fund balance, you must run the report from period 0****.

The report will provide you with the following fields:

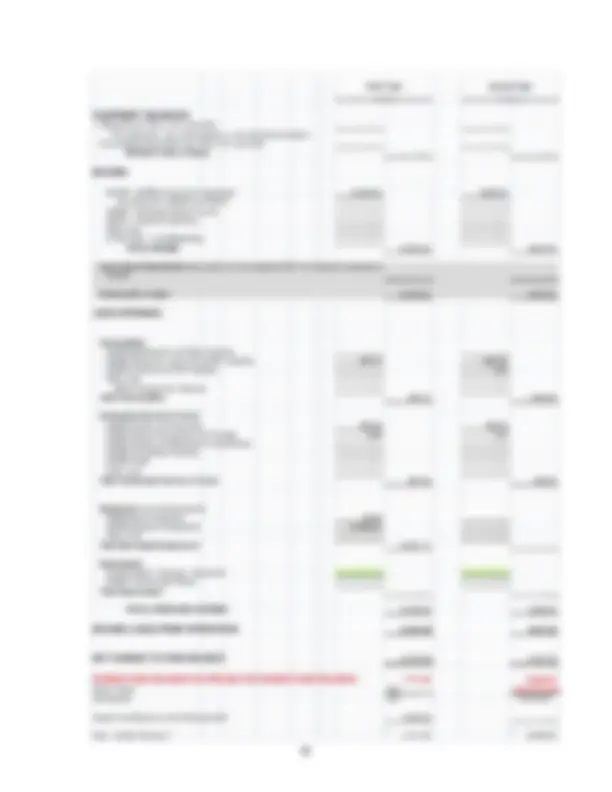

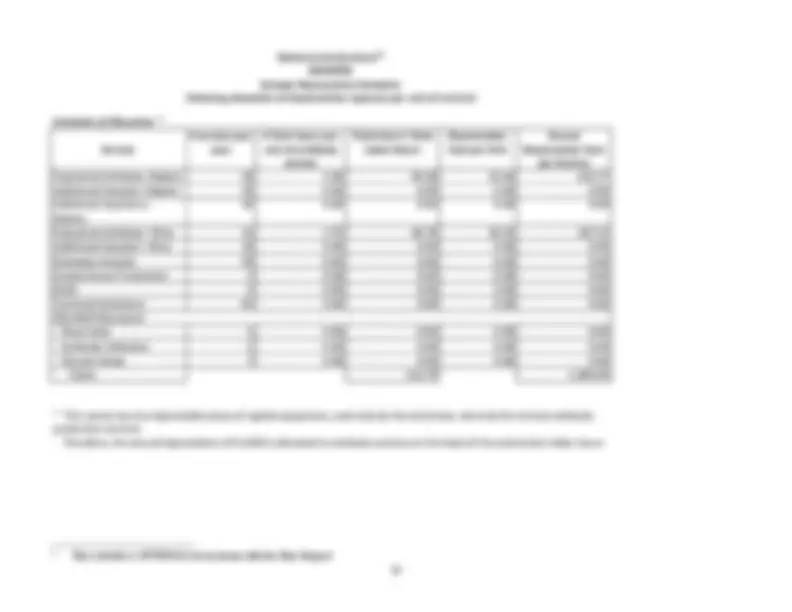

‘Cash’ – the total of 101xxx G/L accounts ‘CurrAsst’ = Other Current Assets – current assets other than cash. This amount excludes capitalized assets and accumulated depreciation. ‘Liab’ = Current Liabilities – all 2-type G/L accounts ‘Fund Bal’ = Fund Balance – this is the calculation of fund balance, otherwise known as the working capital balance. The calculation of fund balance is: Cash + Other Current Assets + Liability = Fund Balance. ‘TFB-10%Inc’ = Tolerable Fund Balance based on 10% of Income – o Formula for Calculation of Tolerable Fund Balance based on 10% of Income is as follows: o ‘Annual Inc’ column * 10% = Tolerable Fund Balance based on 10% of Income ‘TFB-TwoMoExp’- Tolerable Fund Balance based on two months of cash expenses – o Formula for Calculation of Tolerable Fund Balance based on two months of cash expenses is as follows: o ‘Annual Exp’ column – ‘Depr Exp’ column - ‘PLA’ column = Total Cash Expenses * 2/12 * (-1) = Tolerable Fund balance based on two months of cash expenses. ‘Annual Inc’ = Annual Income – all 4-type G/L accounts excluding 49-type G/L accounts ‘Annual Exp’ = Annual Expenses – all 5-type G/L accounts excluding 59-type G/L accounts ‘Tran In’ = Transfers In – all 49-type G/L accounts ‘Tran Out’ = Transfers Out – all 59-type G/L accounts ‘CptlAssts’ = Capital Assets – all 155xxx type G/L accounts ‘AccumDepr’ = Accumulated Depreciation – all 156xxx type G/L accounts ‘Depr Exp’ = Depreciation Expense – all 557xxx type G/L accounts (this amount is already included in the ‘Annual Exp’ column) ‘PLA’ = Plant Assets Retired – G/L 568020 (this amount is already included in the ‘Annual Exp’ column) “Rchg Subsidy’ = Recharge Subsidy – G/L 433080 (this amount is already included in the ‘Annual Inc’ column)

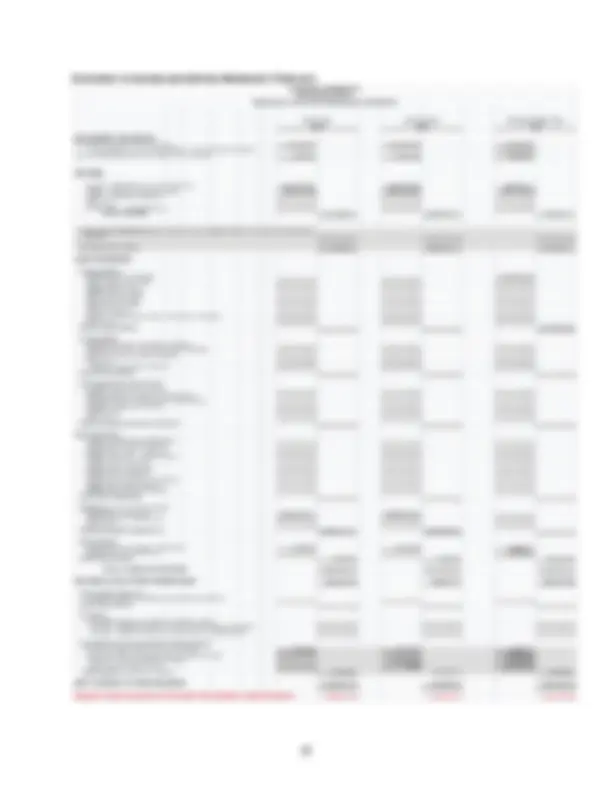

It should also be noted that there is a pretty big discrepancy between Annual Income and Annual Expenses within this recharge. Because Annual Income is so much greater, we should be cautious using 10% of Net Income as a tolerable fund balance, because it appears that we are overcharging within this recharge, and we do not want that to increase our tolerable fund balance. If there is a justifiable reason for income being drastically higher than expense, then we are okay to use it as a fund balance. Examples of reasonable justifications would be that the recharge was billed a large expense that will be paid at the beginning of the following year, which will bring expenses in line with the income; or the approved copy of the rate request is allowing for the recharge to recover a deficit, and therefore income is greater than expenses for this period. If there is a situation like this in the recharge center, please be prepared to justify using the tolerable fund balance zone used in your review.

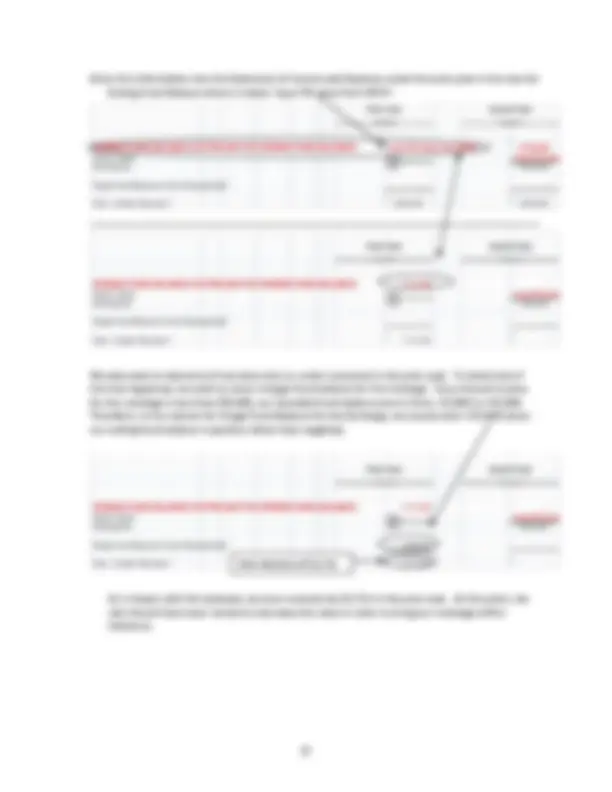

The following print screen is an example of a negative fund balance:

Continued:

The fund balance of this recharge is -$4,528. Although this fund balance is negative, it is still within tolerable fund balance range because it is within the -$5,000 to +$5,000 range. Fund balance should never go below -$5,.

WHAT TO DO WHEN DEPRECIATION IS RECOVERED AS PART OF THE RATE

Depreciation is a non-cash expense used in accounting to try to match the expense of an asset to the income that the asset helps the recharge center earn. This means that depreciation expense will hit the recharge center’s expense G/L accounts, but will not decrease cash each year (or increase current liabilities that you will have to pay in the future) like a normal expense would. So if you recover depreciation through your rate, you are essentially collecting income (cash or an account receivable that you will recover in the future) to cover an expense that you do not actually have to ‘pay’. Because we are not technically ‘paying’ this amount, but we are recovering the cost, the income received to cover that cost will cause an increase in cash or accounts receivable (which are current assets) in our recharge center operating fund(s). Current assets are included in the working capital fund balance calculation, so this accumulation of cash or accounts receivable causes an increase in fund balance in the recharge operating fund(s). This will appear in an operating fund balance as a surplus, and can cause the recharge center to become out-of-tolerance.

For this reason, cash equal to the amount of depreciation expense recovered through the rate must be transferred to a depreciation recovery account on a periodic basis (monthly/quarterly/annually). This allows for the funds to be separated and therefore easily identifiable when reviewing the recharge center operating fund balance, as well as the fund balance of the depreciation recovery account. Then when the equipment within the recharge center needs to be replaced, the funds for the purchase are readily available and easily identifiable without any further analysis of the recharge center operating fund(s).

Examples of the entries made to purchase capital equipment and to transfer depreciation into the depreciation recovery account on a monthly/quarterly/annual basis are shown on page 57.

When Annual Income + Subsidies + Transfers In > Annual Expenses + Transfers Out + Capital Purchases, fund balance increases. When Annual Income + Subsidies + Transfers In < Annual Expenses + Transfers Out + Capital Purchases, fund balance decreases.

FLOW-THROUGH ACTIVITIES

Certain goods or services, such as copy services and postage, are provided to the University community by transferring the exact, actual cost to the user. There is no mark-up involved and no rate calculations are conducted at the operating unit level to determine the cost of the good or service.

The Recharge Center Policy states: Costs for these (flow-through) expenses will be incurred in the department’s operating account and recharges will be treated as reduction of expense.

To record expense recovery amounts associated with flow-through activities, simply credit the appropriate expense G/L account for the sale (i.e., postage, copy machine charges) on an intramural invoice voucher (when recovering from Purdue departments where there is an approved rate), a journal voucher (when recovering from Purdue departments where there is not an approved rate), or cash receipts voucher (when payment is received in cash or check).

As a simple example ignoring the payables entry, let’s assume that the Chemistry department needs a chemical that is only sold in increments of 5,000 gallons. So the chemistry department purchases 5,000 gallons of the chemical for $5,000. The entry for this purchase is as follows:

DR CR G/L account Fund Cost Center Amount DR 523020 Chemicals 21010000 4018004000 (Chemistry) 5,000. CR 101000 Cash 21010000 4018004000 (Chemistry) 5,000.

This entry increases the expense for chemicals within the chemistry department and decreases the cash within the chemistry department (because cash was used to purchase the chemicals).

However, the chemistry department realizes that they only need 2,000 gallons of the chemical, and they would like to sell the remaining amount of chemical to recover the cost. The chemistry department decides to sell the remaining 3,000 gallons of the chemical to the biology department. That entry would look as follows:

DR CR G/L account Fund Cost Center Amount DR 523020 Chemicals 21010000 4018003000 (Biology) 3,000. CR 523020 Chemicals 21010000 4018004000 (Chemistry) 3,000.

This entry decreases the amount of the expense for chemicals within the chemistry department (crediting an expense G/L account represents a decrease in the expense), while increasing the amount of the expense for chemicals within the biology department (debiting an expense G/L account represents an increase in the expense).

ACCEPTABLE FUND BALANCE FOR:

GENERAL SERVICE CENTERS AND SPECIALIZED SERVICE FACILITIES

A. DETERMINE TWO MONTHS OF CASH EXPENSES

Note: Two months of cash expenses can easily be found by using the transaction code GR55 (Report Group ZRSC), which will return the target fund balance, as well as the tolerable upper and lower limits for fund balance based on two months of expenses. However, if you would like to see how this amount is calculated, please follow the steps below:

- Add all expenses (except for depreciation and plant assets retired) for the current month and previous eleven months. These expenses consist of labor, fringe benefits, cost of sales, other department expenses, and administrative and general expenses. {At the end of the fiscal year, total annual expenses can be found by running the GR55 (Report Group ZRSC) transaction code. This number will be found under the ‘Annual Exp’ column. This amount includes depreciation expense and plant assets retired, so in order to get the two months of cash expenses, subtract the amounts in the ‘Depr Exp’ and ‘PLA’ columns from the amount in the ‘Annual Exp’ column. This amount will be your total annual cash expenses.}

- Divide this figure by twelve and multiply by two to arrive at two months of cash expenses. {At the end of the fiscal year, two months of cash expenses can be found by running the GR55 (Report Group ZRSC) transaction code. This number will be found under the ‘Target FB’ (Target Fund Balance) column on the second page of the report. If you are in the middle of a fiscal year and would like an estimate of what your tolerable fund balance should be, you can use the ZRSC report from the previous year for a reasonable estimate, provided that the activity within the recharge has not increased or decreased drastically within the year.

B. DETERMINE THE UPPER AND LOWER LIMITS OF THE FUND BALANCE TOLERANCE ZONE (+10% AND -10%) BY MULTIPLYING THE TWO MONTHS OF CASH EXPENSES BY:

- 90% (to arrive at the lower fund balance limit) – this amount can also be found in the ‘TFB- Lower’ column on the ZRSC Report – and

- 110% (to arrive at the upper fund balance limit) – this amount can also be found in the ‘TFB- Upper’ column on the ZRSC Report

MANAGEMENT ACTION: If the current month fund balance is not within the fund balance tolerance zone, we need to ask:

- Does our financial position fit the pattern of prior years at this same time?

- Is our financial position approximately what was projected at this time?

- Are there unusual income or expense items this period?

- Where will we be at year-end?

ASSESSING THE CURRENT FUND BALANCE

FOR: GENERAL SERVICE CENTERS AND SPECIALIZED SERVICE FACILITIES

There are several ways to determine current fund balance: The necessary information can be calculated from figures derived from GR55 (Report Group Z100), or from using the recharge fund balance transaction code listed below.

The most straight-forward approach is to:

Run the transaction code GR55 (Report Group ZRSC) in SAP:

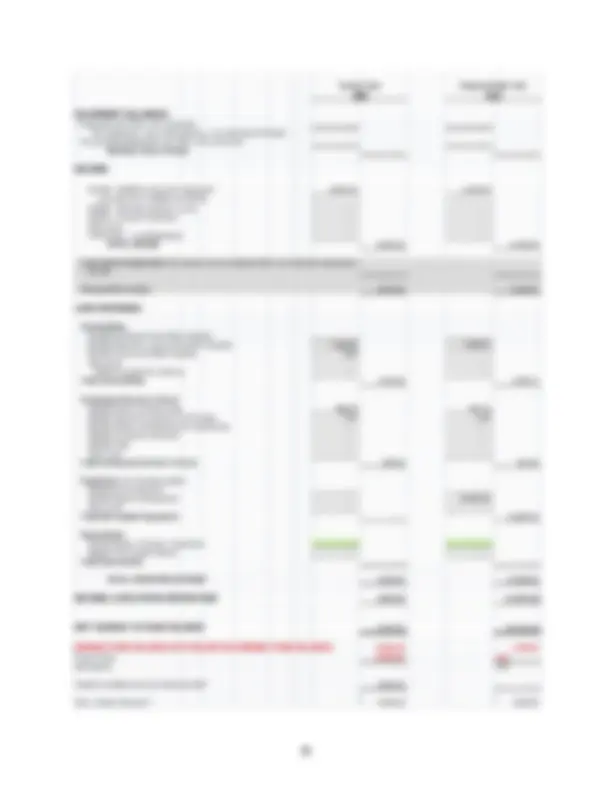

The transaction code will provide the recharge’s life-to-date fund balance status. It prompts you to enter your recharge center fund, the applicable fiscal year and the from and to periods. Please make sure that if you are running the report to calculate fund balance, you must run the report from period 0****. The report will provide you with the following fields:

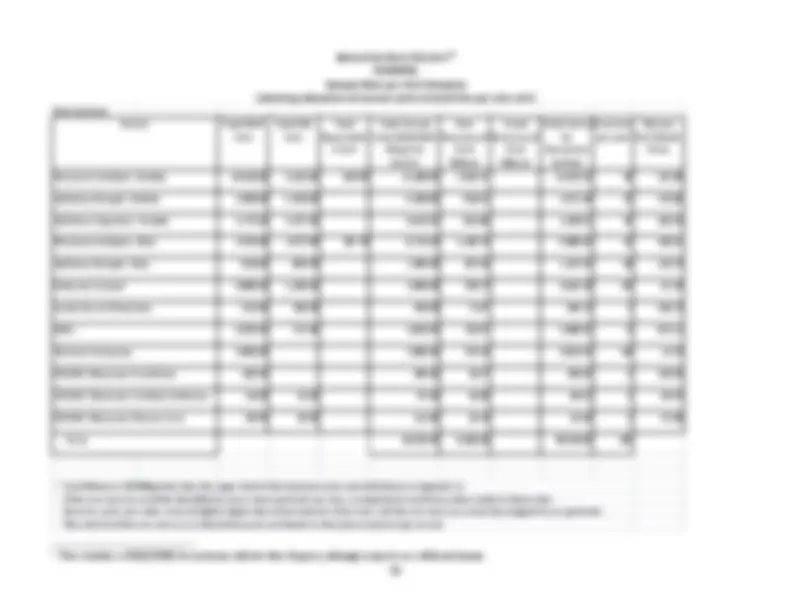

‘Cash’ – the total of 101xxx G/L accounts ‘CurrAsst’ = Other Current Assets – current assets other than cash. This amount excludes capitalized assets and accumulated depreciation. ‘Liab’ = Current Liabilities – all 2-type G/L accounts ‘Fund Bal’ = Fund Balance – this is the calculation of fund balance, otherwise known as the working capital balance. The calculation of fund balance is: Cash + Other Current Assets + (-Liability) = Fund Balance. ‘TFB-Lower’ = Lower limit of Tolerable Fund Balance based two months of cash expenses – o Formula for Calculation of Tolerable Fund Balance based on 10% of Income is as follows: o ‘Target FB’ column * 90% = Lower limit of Tolerable Fund Balance for General Service Center ‘TFB-Upper’- Upper limit of Tolerable Fund Balance based two months of cash expenses – o Formula for Calculation of Tolerable Fund Balance based on two months of cash expenses is as follows: o ‘Target FB’ column * 110% = Upper limit of Tolerable Fund Balance for General Service Center ‘Annual Inc’ = Annual Income – all 4-type G/L accounts excluding 49-type G/L accounts ‘Annual Exp’ = Annual Expenses – all 5-type G/L accounts excluding 59-type G/L accounts ‘Target FB’ = Target Fund Balance – Target Fund Balance based on two months of cash expenses – o Formula for Calculation of Target Fund Balance based on two months of cash expenses is as follows: o ‘Annual Exp’ column – ‘Depr Exp’ column - ‘PLA’ column = Total Cash Expenses * 2/12 = Target Fund balance based on two months of cash expenses. ‘Tran In’ = Transfers In – all 49-type G/L accounts ‘Tran Out’ = Transfers Out – all 59-type G/L accounts ‘CptlAssts’ = Capital Assets – all 155xxx type G/L accounts ‘AccumDepr’ = Accumulated Depreciation – all 156xxx type G/L accounts

is $51,684. The ‘TFB-Upper’ column shows us that the upper limit of tolerable fund balance is $63,169. So the fund balance tolerance zone would be from $51,684 to $63,169. Fund balance is $54,847, which is within this tolerance zone. Therefore, this service center is within tolerance because it is within the fund balance tolerance zone.

The following print screen is an example of a negative fund balance:

Continued:

Negative fund balances in General Service Centers are never within tolerance because in order to maintain a target fund balance of two months of cash expenses – because this is the estimated

amount of expenses that would need to be paid if the recharge were to shut down – a positive fund balance is required (since we cannot pay our debts with negative cash).

WHAT TO DO WHEN DEPRECIATION IS RECOVERED AS PART OF THE RATE

Depreciation is a non-cash expense used in accounting to try to match the expense of an asset to the income that the asset helps the recharge center earn. This means that depreciation expense will hit the recharge center’s expense G/L accounts, but will not decrease cash each year (or increase current liabilities that you will have to pay in the future) like a normal expense would. So if you recover depreciation through your rate, you are essentially collecting income (cash or an account receivable that you will recover in the future) to cover an expense that you do not actually have to ‘pay’. Because we are not technically ‘paying’ this amount, but we are recovering the cost, the income received to cover that cost will cause an increase in cash or accounts receivable (which are current assets) in our recharge center operating fund(s). Current assets are included in the working capital fund balance calculation, so this accumulation of cash or accounts receivable causes an increase in fund balance in the recharge operating fund(s). This will appear in an operating fund balance as a surplus, and can cause the recharge center to become out-of-tolerance.

For this reason, cash equal to the amount of depreciation expense recovered through the rate must be transferred to a depreciation recovery account on a periodic basis (monthly/quarterly/annually). This allows for the funds to be separated and therefore easily identifiable when reviewing the recharge center operating fund balance, as well as the fund balance of the depreciation recovery account. Then when the equipment within the recharge center needs to be replaced, the funds for the purchase are readily available and easily identifiable without any further analysis of the recharge center operating fund(s).

Examples of the entries made to purchase capital equipment and to transfer depreciation into the depreciation recovery account on a monthly/quarterly/annual basis are shown on page 57.